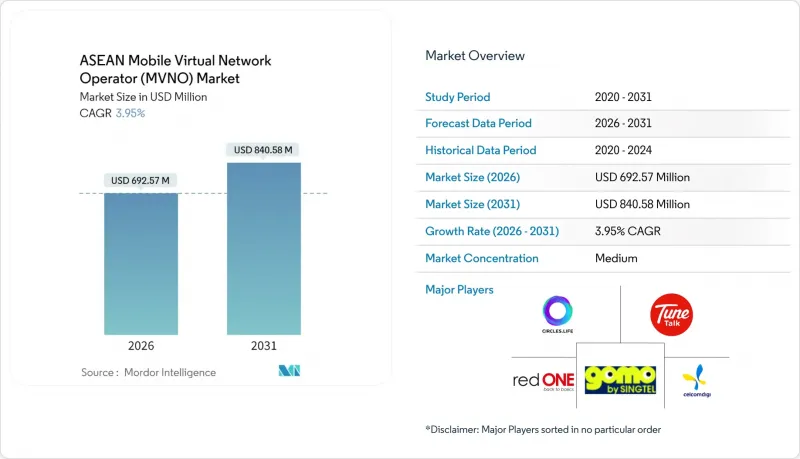

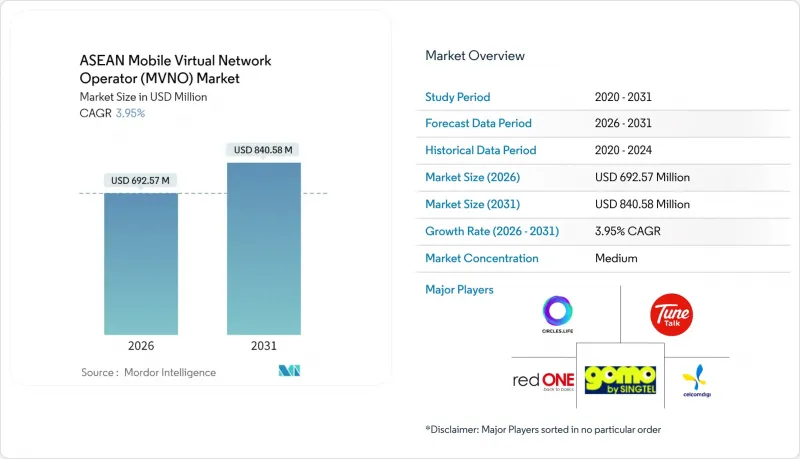

ASEAN 모바일 가상 네트워크 사업자(MVNO) 시장은 2025년 6억 6,625만 달러에서 2026년에는 6억 9,257만 달러로 성장하여 2026년부터 2031년까지 CAGR 3.95%를 기록하며 2031년까지 8억 4,058만 달러에 달할 것으로 예측됩니다.

가입자 수 측면에서 시장 규모는 2025년 814만 명에서 2030년까지 945만 명으로 확대될 것이며, 예측 기간(2025-2030년) 동안 연평균 3.03%의 CAGR을 기록할 것으로 예측됩니다. 이러한 성장의 배경에는 가상 통신 사업자들이 기존 이동통신사(MNO)의 인프라 제약을 피하기 위해 하이브리드 아키텍처를 채택하면서 위성 및 기타 비지상파 네트워크(NTN)가 확대되고 있는 것이 주요 원인으로 꼽힙니다. 클라우드 네이티브 코어, 국경을 초월한 eSIM 패키지, 규제 완화가 결합하여 경쟁 환경을 재구성하고, 민첩한 신규 진입자가 대규모 설비 투자 없이도 규모를 확장할 수 있게 되었습니다. 젊은 층을 위한 데이터 요금제 및 기업용 IoT 연결에 대한 수요가 트래픽을 확대하는 한편, 이동통신사의 디지털 서브 브랜드는 가격 경쟁이 치열해지면서 부가가치 서비스를 통한 차별화가 요구되고 있습니다. 주권 데이터 규제와 지역 로밍 요건의 상호 작용으로 인해, 규정 준수에 대한 전문 지식은 아세안 MVNO 시장의 모든 참가자들에게 전략적 자산이 되고 있습니다.

2025년 아세안 지역의 스마트폰 보유율은 67%를 넘어섰고, 4억 4,000만 명 이상의 모바일 인터넷 사용자들은 대용량 데이터 통신과 원활한 앱 경험을 기대하고 있습니다. 베트남의 새로운 통신법은 M2M(Machine to Machine) 통신을 기본 서비스로 규정하고, MVNO가 부가가치 서비스 허가 없이도 IoT 연결을 판매할 수 있도록 허용했습니다. 이러한 명확화로 인해 특히 중국 본토 이외의 지역으로 다각화를 추진하고 있는 전자기기 및 의류 산업 클러스터에서 산업 도입이 가속화되고 있습니다. 가상 통신 사업자들은 기존 음성 비용을 제거한 데이터 전용 요금제를 제공함으로써 이익을 얻고 있지만, 데이터 사용량 급증으로 인해 단가가 압축되어 아세안 MVNO 시장에서 수익률을 유지하기 위해서는 고도의 트래픽 관리 도구가 요구되고 있습니다.

베트남 법령 163/2024는 비차별적 도매 조건을 의무화하고, 해외 클라우드 서비스에 대한 명확한 절차를 규정하며, 해외에서 호스팅되는 MVNO 코어의 승인 주기를 단축합니다. 말레이시아의 단일 도매 네트워크 모델은 인구 커버리지 80%까지 할인된 5G 요금을 제공하지만, 중앙 집중식 구조로 인해 MNO의 제품 차별화를 제한하고 기업용 수직 시장을 겨냥한 완전 MVNO의 기회를 확대할 수 있습니다. 태국은 지역 블록 단위의 주파수 경매를 계속 시행하고 있으며, MVNO는 여러 지역에서 로밍 협상을 해야 하는 상황입니다. 이러한 정책 전환을 통해 아세안 MVNO 시장은 신규 진입자에게 개방되고, 서로 다른 규제 환경을 조정하면서 균일한 서비스 품질을 유지할 수 있게 됩니다.

경쟁 촉진 정책이 존재함에도 불구하고, 진정한 비용 기반의 도매 요금을 협상하는 것은 여전히 어렵고, 특히 기존 사업자가 주파수 우위를 가지고 있는 지역에서는 더욱 그러합니다. 태국의 지역별 주파수 파편화로 인해 MVNO는 여러 개의 로밍 계약을 체결하게 되어 협상력을 약화시키고 있습니다. 5G 인프라 비용의 급등으로 인해 이동통신사들은 프리미엄 액세스 추가 요금을 부과하는 경향이 있으며, 이는 가상 사업자가 수익성을 유지할 수 있는 엔트리 레벨 요금제를 구축하는 능력을 제한하고 있습니다. 이러한 제약으로 인해 아세안 MVNO 시장의 많은 브랜드들은 부가가치 서비스로 높은 네트워크 요금을 상쇄하거나 위성 오프로드 전략을 모색해야 하는 상황에 처해 있습니다.

클라우드 기반 코어 네트워크는 2025년 아세안 MVNO 시장 규모의 65.32%를 차지했으며, 가상 사업자들이 설비 투자보다 운영 비용을 중시하고 신속한 국경 간 확장을 추구함에 따라 2031년까지 CAGR 8.83%로 확대될 것으로 전망됩니다. 베트남 법령 163/2024에 따른 규제 명확화(해외 클라우드를 라이선싱이 아닌 등록제로 취급)로 인해 도입이 더욱 가속화되고 있습니다. 클라우드의 확장성은 틈새 브랜드의 진입 비용을 낮추고, 아세안 MVNO 시장 전체에 걸쳐 가격, 마케팅, 부정행위 방지 최적화를 위한 실시간 분석을 가능하게 합니다.

지연, 이중화, 데이터 거주 규칙이 비용 측면을 능가하는 분야에서는 온프레미스 도입이 지속될 것입니다. 금융기관이나 공공안전기관은 국내 데이터센터 내 프라이빗 코어를 요구하는 경우가 많습니다. 하이브리드형은 클라우드 제어와 엣지 프로세싱을 융합하고, 5G 비지상파 네트워크 게이트웨이를 활용하여 커버리지를 확장합니다. 이 혼합 모델을 채택한 사업자들은 광섬유 장애 시 서비스 연속성 향상과 확정적 성능을 중요시하는 산업 고객층에 대한 매력도 강화를 보고하고 있습니다.

리셀러/라이트 모델은 최소한의 인프라로 빠른 상용화가 가능해 아세안 MVNO 시장 점유율 60.85%를 차지하고 있습니다. 그러나 호스트 사업자에 대한 의존도가 높기 때문에 서비스 커스터마이징에 제약이 발생합니다. 풀 MVNO는 자본 집약적이지만, 기업의 라우팅 자율성, 네트워크 슬라이싱 기능, 차별화된 IoT 및 기업용 서비스를 위한 직접 상호접속 수요로 인해 18.12%의 CAGR로 성장하고 있습니다. 이들 사업자는 IMS 코어, 퍼블리셔 프로비저닝 서버, 도매 조달을 직접 관리하여 사용자당 평균 수익(ARPU)을 높이고 있습니다.

서비스 사업자형 MVNO는 중간적인 포지셔닝으로 HLR/HSS 등의 요소를 소유하는 반면, 무선접속 제어는 MNO에 맡깁니다. 이는 로열티 통합을 중시하는 동시에 대규모 통신 투자를 피하고 싶어하는 EC 대기업에게 매력적입니다. 따라서 아세안 MVNO 시장의 사업 형태는 순수 브랜딩 사업부터 수직계열화 된 스타트업까지 다양하며, 각 사별로 대상 부문의 경제성에 맞는 아키텍처를 채택하고 있습니다.

아세안 모바일 가상 네트워크 사업자(MVNO) 시장 보고서는 도입 모델(클라우드/온프레미스), 운영 형태(서비스 사업자 등), 가입자 유형(소비자 등), 용도(할인 서비스 등), 네트워크 기술(2G/3G 등), 유통 채널(온라인/디지털 전용 등), 국가별로 세분화하여 조사 분석하였습니다. 디지털 독점 등), 국가별로 세분화되어 있습니다. 시장 예측은 금액(달러) 및 수량(가입자 수) 측면에서 제공됩니다.

The ASEAN Mobile Virtual Network Operator Market is expected to grow from USD 666.25 million in 2025 to USD 692.57 million in 2026 and is forecast to reach USD 840.58 million by 2031 at 3.95% CAGR over 2026-2031.

In terms of subscriber volume, the market is expected to grow from 8.14 million subscribers in 2025 to 9.45 million subscribers by 2030, at a CAGR of 3.03% during the forecast period (2025-2030). Behind this headline growth, satellite and other non-terrestrial networks (NTN) expand as virtual operators adopt hybrid architectures that bypass traditional mobile-network-operator (MNO) infrastructure constraints. Cloud-native cores, cross-border eSIM packages, and regulatory liberalization collectively reshape competitive dynamics, allowing nimble entrants to scale without heavy capex. Demand for youth-centric data plans and enterprise IoT connectivity amplifies traffic volumes, while MNO digital sub-brands intensify price competition and force differentiation through value-added services. The interplay of sovereign data rules and regional roaming requirements makes compliance expertise a strategic asset for every participant in the ASEAN MVNO market.

Smartphone ownership surpassed 67% of the ASEAN population in 2025, translating into more than 440 million mobile internet users who expect high-data allowances and seamless app experiences. Vietnam's new telecom framework classifies machine-to-machine (M2M) traffic as a basic service, enabling MVNOs to sell IoT connectivity without value-added service permits . The clarification accelerates industrial adoption, especially in electronics and garment clusters that diversify beyond mainland China. Virtual operators capitalize by offering data-only plans free from legacy voice costs, yet the surge in data usage compresses unit prices and demands sophisticated traffic-management tools to sustain margins within the ASEAN MVNO market.

Vietnam's Decree 163/2024 mandates nondiscriminatory wholesale terms and codifies clear procedures for offshore cloud services, reducing approval cycles for MVNO cores hosted outside the country . Malaysia's single-wholesale-network model offers discounted 5G rates until 80% population coverage, but its centralized structure limits MNO product differentiation and widens opportunities for full MVNOs targeting enterprise verticals. Thailand continues to auction spectrum in regional blocks, compelling MVNOs to negotiate roaming in multiple provinces. Collectively, these policy shifts open the ASEAN MVNO market to new entrants that can juggle divergent regimes while maintaining uniform quality of service.

Despite pro-competition mandates, negotiating genuinely cost-based wholesale rates remains difficult, particularly where incumbent operators wield spectrum advantages. Thailand's provincial spectrum fragmentation forces MVNOs into multiple roaming contracts that dilute bargaining power. Elevated 5G infrastructure costs prompt MNOs to impose premium access surcharges, limiting the ability of virtual players to craft entry-level plans that preserve margin. This restraint compels many brands in the ASEAN MVNO market to offset higher network charges with value-added services or to explore satellite offload strategies.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cloud-based cores generated 65.32% of the ASEAN MVNO market size in 2025 and will rise at an 8.83% CAGR to 2031 as virtual operators favor opex over capex and pursue rapid cross-border launches. Regulatory clarity under Vietnam's Decree 163/2024, which treats offshore clouds as registrable rather than licensable, further accelerates adoption. Cloud elasticity lowers onboarding costs for niche brands and empowers real-time analytics that optimize pricing, marketing, and fraud controls across the ASEAN MVNO market.

On-premise deployments persist in sectors where latency, redundancy, or data-residency rules override cost considerations. Financial institutions and public-safety agencies often demand private cores within domestic data centers. Hybrid variants blend cloud control with edge processing, leveraging 5G non-terrestrial-network gateways to extend coverage. Operators adopting this mix report smoother service continuity during fiber outages and a stronger appeal among industrial clients that value deterministic performance.

Reseller/light models still represent 60.85% of ASEAN MVNO market share because they require minimal infrastructure and yield fast commercialization. Yet their dependence on host operators curbs service customization. Full MVNOs, while capital-intensive, grow at 18.12% CAGR as firms seek routing autonomy, network-slicing capabilities, and direct interconnects that enable differentiated IoT and enterprise offerings. These players directly manage IMS cores, issuer provisioning servers, and wholesale procurement, culminating in higher average revenue per user.

Service-operator MVNOs occupy a midpoint, owning elements such as HLR/HSS but leaving radio-access control to MNOs. They appeal to e-commerce majors that value loyalty integration but shun deep telecom investment. The operational spectrum within the ASEAN MVNO market thus ranges from pure-branding ventures to vertically integrated challengers, each aligning architecture with target segment economics.

The ASEAN Mobile Virtual Network Operator (MVNO) Market Report is Segmented by Deployment Model (Cloud, On-Premise), Operational Mode (Service Operator, and More), Subscriber Type (Consumer, and More), Application (Discount, and More), Network Technology (2G/3G, and More), Distribution Channel (Online/Digital-only, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Subscribers).