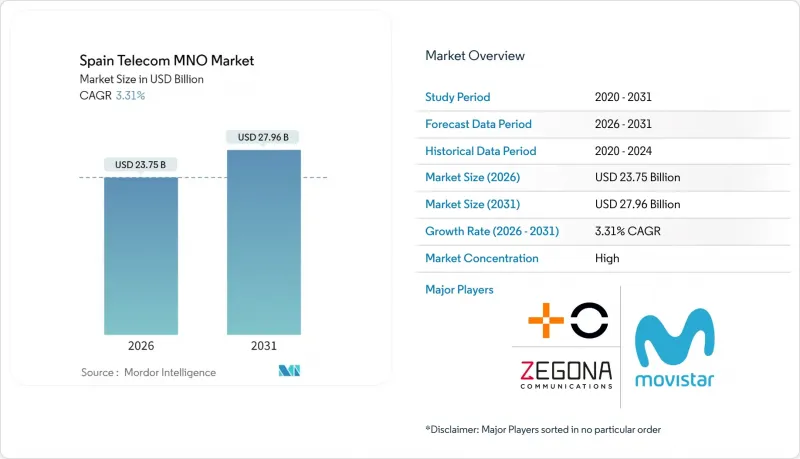

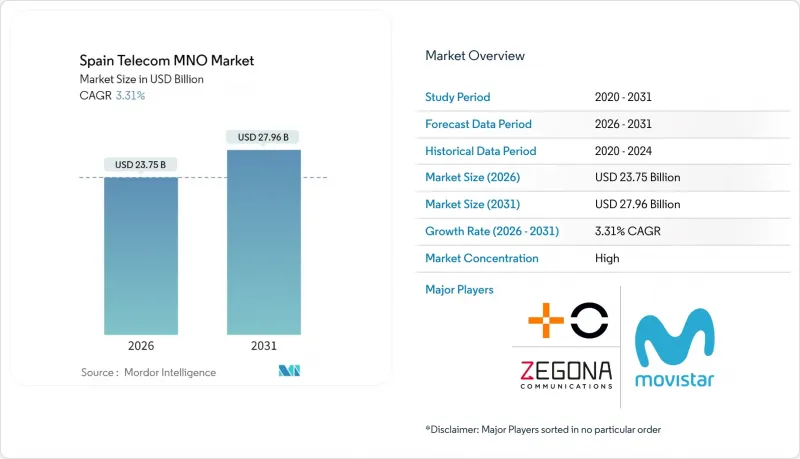

스페인의 이동통신 사업자(MNO) 시장 규모는 2026년에 237억 5,000만 달러로 추정되고 있습니다.

이는 2025년 229억 9,000만 달러에서 성장한 수치이며, 2031년에는 279억 6,000만 달러에 달할 것으로 예측되고 있습니다. 2026-2031년에는 CAGR 3.31%로 성장이 전망되고 있습니다.

이러한 완만한 성장은 사업자들이 데이터 중심 매출, 네트워크 공유 효율화, 체계적인 자본 배분에 집중하는 성숙된 환경을 반영합니다. 현재 95.2%의 가구를 커버하는 FTTH(광가입자망) 보급률 증가는 가격 경쟁에도 불구하고 프리미엄 통합형 번들 서비스를 통한 가입자당 평균매출(ARPU)을 지원하고 있습니다. 산업 재편으로 경쟁 구도가 바뀌었습니다. 오렌지와 매스모바일의 제휴로 탄생한 매스오렌지가 가입자 점유율 42%를 차지하며 텔레포니카의 25%와 격차를 좁히는 한편, 보다폰과의 90-100억 유로 규모의 파이버코 제휴 등 새로운 협업 모델이 생겨나고 있습니다. 에너지 비용 변동(영업비용의 10-15% 차지)과 미해결된 주파수 사용료 소송이 이익률 확대의 걸림돌로 작용하고 있습니다. 한편, 정부가 지원하는 10억 유로 규모의 단독 지방 5G 펀드를 통해 인구의 96%를 커버하는 통신망이 확보되어 스페인의 첨단 모바일 기술 리더십이 강화되고 있습니다.

스페인은 단독 5G에서 유럽을 선도하고 있으며, 지방 기지국에 대한 10억 유로의 공공 자금을 원동력으로 2025년까지 96%의 인구 커버리지를 달성할 것입니다. Movistar, MasOrange, Vodafone의 700MHz 대역의 공동 사용은 교외 지역으로의 확산을 가속화하면서 도입 비용을 절감할 수 있습니다. MasOrange와 에릭슨의 Open RAN 프로그램은 탄력적인 용량 확장이 가능한 소프트웨어 정의 네트워크의 실현을 이끌어냅니다. 유럽연합 집행위원회 5G 관측소에 따르면 2024년 3월 기준 스페인의 가구 커버리지는 92.3%에 달하고, EU 평균을 크게 상회하고 있습니다. 이러한 성과로 인해 통신사업자들은 기업용 서비스 및 저지연 용도의 5G-SA 수익화에 자원을 집중할 수 있게 되었습니다.

구매력 평가 기준 17.39달러의 무제한 요금제는 유럽에서 가장 저렴한 수준이며, 대도시 지역에서 높은 이용률을 보이고 있습니다. 2024년 초 트래픽 성장률은 전년 대비 12%로 둔화됐지만, 통신사들은 GB당 비용 효율적인 단계적 5G 제안으로 가치를 지키고 있습니다. 저가 브랜드로의 경쟁적 전환이 심화되면서 기존 사업자들은 가격 중심의 신흥 사업자들에게 점유율을 빼앗겼습니다. 전략적 대응은 대폭적인 할인에 의존하지 않고 부가가치 번들, 프리미엄 컨텐츠, 로열티 프로그램을 통해 서비스 품질을 향상시키는 데 초점을 맞추었습니다.

2025년 3월 기준 활성 SIM 수는 6,162만 개로 주민 100명당 125.6회선에 해당합니다. 자연 증가에 의한 사용자 확대의 여지가 제한적이라는 것을 보여줍니다. 번호이동 건수는 전년 대비 7.6% 증가하여 순증보다는 점유율을 둘러싼 제로섬 경쟁 양상이 나타나고 있습니다. 고정형 브로드밴드도 전 가구 보급률에 가까워지고 있으며, 사업자들은 디지털 서비스에서 수입원 발굴에 박차를 가하고 있습니다. 고령화가 진행되는 인구구조는 정체 현상을 부추기고 있으며, 고령층은 데이터 소비가 많은 서비스를 이용하지 않는 경향이 있습니다. 그 결과, 스페인 통신 MNO 시장은 소비자 시장의 포화를 피하기 위해 기업용 서비스, IoT, 엣지 클라우드 제안으로 자본을 이동하고 있습니다.

2025년 기준, 데이터 통신과 인터넷이 스페인 MNO 시장 점유율의 50.39%를 차지했습니다. 이는 타의 추종을 불허하는 광섬유 보급률과 적극적인 무제한 모바일 요금제 제공을 반영하고 있습니다. 음성서비스는 컨버지드 요금제를 통해 안정세를 유지하고 있지만, SMS 매출은 감소 추세가 지속되고 있습니다. IoT 및 M2M 회선은 기반 규모는 작지만 물류, 에너지, 스마트 시티 솔루션의 추진으로 3.40%의 가장 빠른 CAGR을 기록하고 있습니다. 위성 NTN의 지방 커버리지 장벽이 해소됨에 따라 IoT 중심의 연결성을 대상으로 한 스페인 통신 MNO 시장 규모는 꾸준히 확대될 것으로 예측됩니다. OTT 및 유료 TV 서비스는 보급된 FTTH를 활용하여 사업자는 기존 통신량 범위 내에서 대역폭을 흡수하는 프리미엄 동영상 및 클라우드 게임 등을 포함시킬 수 있습니다.

사업자는 기업 사용자를 위한 최선의 노력형 4G와 보장형 5G-SA 슬라이스를 통해 스페인 MNO 시장 규모의 차이를 수익화할 수 있습니다. 네트워크 API를 통해 개발자가 온디맨드 품질 기능을 용도에 통합하여 증분 매출을 창출할 수 있습니다. 클라우드 게임과 같은 지연에 민감한 서비스가 성숙해짐에 따라 사업자들은 기존 음성 서비스의 상품화를 상쇄하는 프리미엄 계층에서 두 자릿수 성장을 예상하고 있습니다.

Spain Telecom MNO Market size in 2026 is estimated at USD 23.75 billion, growing from 2025 value of USD 22.99 billion with 2031 projections showing USD 27.96 billion, growing at 3.31% CAGR over 2026-2031.

Moderate growth reflects a mature environment where operators focus on data-centric revenues, network-sharing efficiency, and disciplined capital allocation. Intensifying fiber-to-the-home penetration, which now covers 95.2% of premises, sustains premium converged bundles that lift average revenue per user despite price competition. Consolidation has reshaped rivalry after the Orange-MasMovil tie-up created MasOrange with 42% subscriber share, narrowing the gap with Telefonica's 25% stake while prompting new partnering models such as the EUR 9-10 billion FibreCo with Vodafone. Energy-cost volatility, which absorbs 10-15% of operating expenses, and unresolved spectrum-fee litigation temper margin expansion. Meanwhile, government-backed EUR 1 billion funding for rural standalone 5G ensures 96% population coverage, reinforcing Spain's leadership in advanced mobile technology.

Spain leads Europe in standalone 5G, achieving 96% population coverage by 2025 on the strength of EUR 1 billion public funding for rural base-stations. Joint use of the 700 MHz band by Movistar, MasOrange, and Vodafone reduces deployment cost while speeding suburban roll-outs. MasOrange's Open RAN program with Ericsson ushers in software-defined networks capable of elastic capacity scaling. The European Commission's 5G Observatory confirms Spain's 92.3% household coverage by March 2024, well ahead of the EU mean . These achievements allow operators to pivot resources toward 5G-SA monetization in enterprise and low-latency applications.

Unlimited bundles priced at USD 17.39 purchasing-power-parity rank among Europe's cheapest, stimulating heavy usage in metropolitan corridors. Although traffic growth slowed to 12% year-over-year in early-2024, operators defend value through tiered 5G propositions with superior cost-per-GB economics. Competitive migration toward low-cost brands intensified, with incumbents losing share to price-focused challengers. The strategic response centers on value-added bundles, premium content, and loyalty programs that elevate perceived service quality without relying solely on heavy discounts.

Active SIMs reached 61.62 million by March 2025, equating to 125.6 lines per 100 residents and signaling limited room for organic user growth. Portability volumes climbed 7.6% year-over-year, underlining a zero-sum battle for share rather than net additions. Fixed broadband likewise nears total household penetration, intensifying operators' hunt for incremental revenue in digital services. Demographic aging compounds stagnation because older cohorts adopt fewer data-intensive offerings. Consequently, the Spain telecom MNO market shifts capital toward enterprise, IoT, and edge-cloud propositions that sidestep consumer saturation.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Data and internet generated 50.39% of Spain telecom MNO market share in 2025, reflecting unmatched fiber penetration and aggressive unlimited mobile bundles. Voice remains sticky via converged offers, whereas SMS revenue declines continue. IoT and M2M lines constitute a smaller base but post the fastest 3.40% CAGR, propelled by logistics, energy, and smart-city solutions. The Spain telecom MNO market size for IoT-centric connectivity is projected to expand steadily as satellite NTNs remove rural coverage barriers. OTT and PayTV services leverage ubiquitous FTTH, enabling operators to embed premium video and cloud gaming that absorb bandwidth within existing allowances.

Operators monetize the Spain telecom MNO market size differential between best-effort 4G and guaranteed 5G-SA slices for corporate users. Network APIs open incremental revenue as developers integrate quality-on-demand features into applications. As latency-sensitive services such as cloud gaming mature, operators expect double-digit growth in premium tiers that counterbalance the commoditization of legacy voice.

The Spain Telecom MNO Market is Segmented by Service Type (Voice Services, Data and Internet Services, Messaging Services, Iot and M2M Services, OTT and PayTV Services, and Other Services), and End User (Enterprises, Consumer). The Market Forecasts are Provided in Terms of Value (USD).