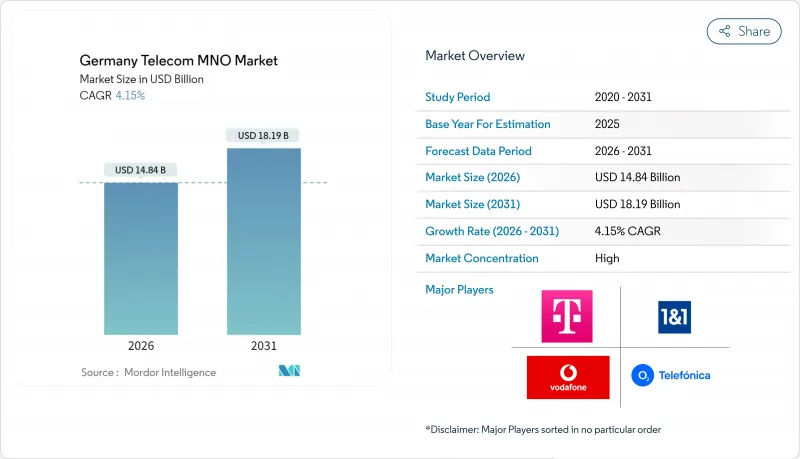

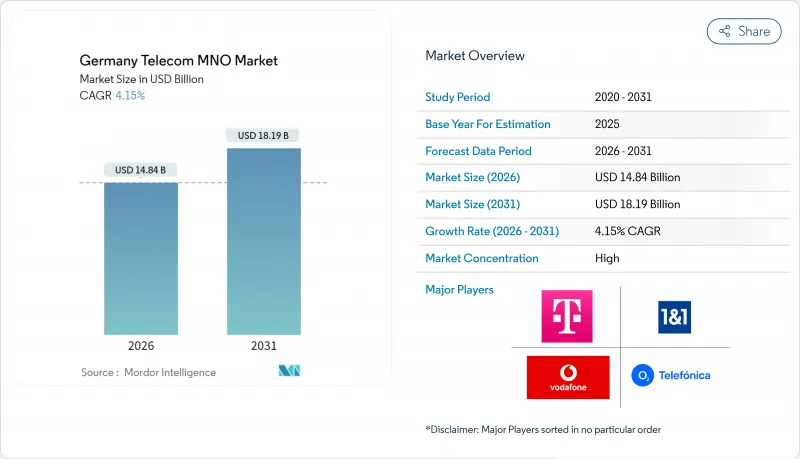

독일의 이동통신망 사업자(MNO) 시장은 2025년에 142억 5,000만 달러로 평가되었고, 2026년 148억 4,000만 달러에서 2031년까지 181억 9,000만 달러에 이를 것으로 예측됩니다.

예측 기간(2026-2031년) CAGR은 4.15%로 성장이 전망됩니다.

2030년까지 500억 유로에 달하는 네트워크 근대화 투자, 연방 기가바이트 전략, 신속한 5G 독립형 전개가 경제 성장이 둔화되는 가운데서도 기세를 유지하고 있습니다. 사업자는 평균 이용자 단가(ARPU) 강화 및 운영 비용 절감을 위해 FTTH(광섬유 가정내 도입)의 커버율 확대, 고정 및 이동체 융합 번들, AI를 활용한 네트워크 자동화를 우선하고 있습니다. 제조업 및 자동차 산업 클러스터를 중심으로 한 기업의 디지털화가 프리미엄 연결 수요를 가속화하고 있습니다. 반면 소비자 데이터 트래픽은 스트리밍 수요를 배경으로 계속 증가하고 있습니다. 엄격한 에너지 효율 규제 및 전파 커버리지 의무를 포함한 규제 압력은 자본 배분의 우선 순위를 검토하고 중소 사업자는 제휴 또는 철수로 이끌고 있습니다.

독일의 기가바이트 전략은 2025년까지 전체 가구의 50%를 광섬유 연결하고 2030년까지 거의 전국적인 커버리지를 달성할 것을 요구하며 적극적인 자본 계획을 촉진하고 있습니다. 연방 정부의 기가바이트 지원 프로그램 'Gigabitforderung 2.0'에 의한 30억 유로의 보조금이 서비스가 잘 되지 않는 지역에서의 구축을 가속화하고 있습니다. 한편 독일 텔레콤은 2030년까지 1,000만 회선 이상의 추가 광섬유 도입을 목표로, 보더폰은 유니티 미디어의 자산을 활용하여 2,500만 가구에 서비스 제공을 목표로 하고 있습니다. 보다 광범위한 광섬유 네트워크를 보유한 사업자는 멀티플레이 번들과 프리미엄 기업용 회선을 통해 높은 ARPU를 실현하고 있습니다. 조기 전개는 일시적인 시장 분단을 낳고 광섬유망이 충실한 지역에 유리하게 작용하지만 장기적인 경쟁력 유지에는 전국적인 전개가 여전히 필수적입니다. 이 전략의 성공은 데이터 집약적인 서비스의 용량 확장을 통해 독일 통신 시장의 수익 성장 궤도를 직접 촉진합니다.

국내 3대 통신사업자는 2024년까지 99%의 커버율 목표를 달성하였고, 독일 텔레콤은 2025년까지 인구 커버율 99%를 계획하고 있습니다. 독립형 아키텍처는 저지연 네트워크 슬라이싱을 제공하며 BMW, 메르세데스 벤츠, 폭스바겐 제조 및 자동차 캠퍼스에서 매우 중요합니다. 소비자 측에서도 수익 향상이 전망되고 있습니다. 각 통신 사업자에 있어서 모바일 데이터 이용량이 전년대비 30-34% 증가하여 대용량 플랜 및 무제한 플랜에 의한 수익화가 진행되고 있습니다. 통신 사업자는 레거시 코어의 폐지 및 주파수 대역의 통합에 의해 효율화를 도모해, 기가바이트 당 비용 절감 및 사용자 체험의 향상을 동시에 실현하고 있습니다. 이러한 배경에서 5G SA를 조기에 도입한 사업자는 지속적인 경쟁 우위를 확보하고 독일 통신 시장의 성장을 가속하는 역할을 담당하고 있습니다.

2024년 7월에 시행된 'Nebenkostenprivileg(광열비 특례)'의 폐지에 의해 케이블 TV 요금 임대료에 대한 자동 임베디드가 철폐되었습니다. 이에 따라 보더폰의 집합주택용 가입자 기반이 직접 경쟁에 노출되어 가입자수는 850만 건에서 400만 건으로 격감했습니다. 업계 전반에 걸쳐 연간 약 8억 유로의 수익이 위기에 노출되어 텔레콜럼버스는 단 몇 개월 만에 TV 고객의 40%를 잃었습니다. 넷플릭스, 아마존 프라임, 와이프, 자투 등의 스트리밍 플랫폼은 네트워크 비용을 부담하지 않고 같은 가구를 쟁탈하고 가격 경쟁을 격화시키고 있습니다. 사업자는 점유율을 보호하기 위해 컨버전스 번들 내에서 TV 위치를 재검토해야 하지만 단기적인 해지율 증가와 EBITDA 압축은 여전히 우려됩니다.

데이터 및 인터넷 서비스는 2025년에 61억 5,000만 달러(독일 통신 시장 점유율 43.12%)를 창출했으며, 동영상 스트리밍 및 기업용 클라우드 접속의 견조한 수요를 배경으로, 2031년까지 연평균 복합 성장률(CAGR) 4.33%로 추이할 것으로 예측되고 있습니다. 각 사업자는 모바일 데이터의 상당한 증가를 기록했습니다. 보더폰은 34% 증가한 18억GB, 독일 텔레콤은 30% 증가한 24억GB, O2는 30억GB를 넘어섰습니다. 반면 고정통신 소비량은 1,210억 GB를 넘었고, 가구당 월간 평균 사용량은 275GB였습니다. 5G 독립형 및 광섬유 업그레이드는 네트워크 슬라이스 보증을 요구하는 산업 사용자로부터 프리미엄 가격을 획득하는 차별화된 서비스 계층을 지원합니다. 결과적으로 독일의 통신 시장 규모는 부문 수준에서 기존 카테고리를 뛰어 넘을 것으로 예측됩니다.

음성 서비스는 2025년 시점에서 여전히 39억 1,000만 달러(공유 27.45%)를 창출하고 있지만, OTT로의 이행과 2028년까지의 2G 서비스 종료 계획에 의해 점감 경향이 예상됩니다. 텔레포니카 도이츄란트사에서는 이미 통화의 80%를 VoLTE 경유로 라우팅하고 있으며, 독일 텔레콤사와 보더폰사도 주파수 대역을 5G로 재분배 중입니다. IoT 및 M2M 서비스는 2025년 13억 6,000만 달러 규모로 4.45%라는 가장 빠른 CAGR을 나타냅니다. 이는 독일이 커넥티드 팩토리 및 자동차 텔레매틱스 분야에서 주도적인 입장에 있음을 반영합니다. 유료 TV 및 기타 부가가치 서비스는 스트리밍 서비스와의 직접적인 경쟁에 직면하고 있지만 국제 여행의 회복과 함께 로밍 및 도매 트래픽은 회복 경향이 있습니다. 데이터 중심 제품이 음성 서비스를 능가하는 동안 전체 포트폴리오 구성은 성장률이 높고 이익률 향상에 기여하는 범주로 이동하고 있습니다.

독일의 통신 사업자 시장은 서비스 유형별(음성 서비스, 데이터 인터넷 서비스, 메시징 서비스, IoT 및 M2M 서비스, OTT 및 유료 TV 서비스 등) 및 최종 사용자별(기업, 소비자)로 시장 세분화됩니다. 시장 예측은 금액(달러) 및 수량(가입자 수)으로 제공됩니다.

The Germany Telecom MNO Market was valued at USD 14.25 billion in 2025 and estimated to grow from USD 14.84 billion in 2026 to reach USD 18.19 billion by 2031, at a CAGR of 4.15% during the forecast period (2026-2031).

Network-modernization investments approaching EUR 50 billion through 2030, the federal Gigabit Strategy, and swift 5G standalone roll-outs are sustaining momentum even as economic growth moderates. Operators are prioritizing fiber-to-the-home coverage, fixed-mobile convergence bundles, and AI-enabled network automation to strengthen average revenue per user (ARPU) and cut operating costs. Enterprise digitalization, particularly in manufacturing and automotive clusters, is accelerating premium connectivity demand, while consumer data traffic keeps climbing on the back of streaming. Regulatory pressure, including stringent energy-efficiency rules and spectrum-coverage obligations, is reshaping capital-allocation priorities and nudging smaller players toward partnership or exit.

Germany's Gigabit Strategy requires 50% of premises to be fiber-connected by 2025 and near-universal coverage by 2030, spurring aggressive capital programs. EUR 3 billion in federal Gigabitforderung 2.0 subsidies accelerates builds in underserved districts, while Deutsche Telekom aims for 10 million additional fiber lines by 2030 and Vodafone leverages Unitymedia assets to pass 25 million homes. Operators with deeper fiber footprints command higher ARPU through multi-play bundles and premium enterprise links. Early deployments create temporary market fragmentation favoring fiber-rich localities, yet nationwide roll-out remains a prerequisite for long-term competitiveness. Successful execution directly lifts German telecom market revenue trajectories by expanding capacity for data-heavy services.

All three national carriers met initial 99% coverage targets by 2024, and Deutsche Telekom plans 99% population reach in 2025. Standalone architecture unlocks low-latency network slicing crucial for manufacturing and automotive campuses at BMW, Mercedes-Benz, and Volkswagen sites. Consumers are also driving revenue uplift as mobile data usage rose 30-34% year-over-year across operators, monetized via larger allowances and unlimited plans. Operators gain efficiency from retiring legacy cores and converging frequency layers, which lowers per-gigabyte costs while improving user experience. Early 5G SA adopters therefore secure durable competitive advantages and stimulate incremental German telecom market growth.

The July 2024 repeal of the Nebenkostenprivileg removed automatic inclusion of cable TV in rental bills, exposing Vodafone's MDU subscriber base to direct competition and slashing the cohort from 8.5 million to 4 million accounts. An estimated EUR 800 million in annual revenue is at risk sector-wide, with Tele Columbus losing 40% of TV customers in mere months. Streaming platforms such as Netflix, Amazon Prime, Waipu, and Zattoo now vie for the same households without bearing network costs, intensifying price pressure. Operators must reposition TV within convergent bundles to defend share, yet short-term churn spikes and EBITDA compression remain likely.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Data and Internet Services delivered USD 6.15 billion in 2025, 43.12% of the German telecom market share, and are CAGR-forecast at 4.33% through 2031 on buoyant video streaming and enterprise cloud connectivity. Operators documented mobile data surges-Vodafone 34% to 1.8 billion GB, Deutsche Telekom 30% to 2.4 billion GB, and O2 beyond 3 billion GB-while fixed consumption surpassed 121 billion GB with average household loads of 275 GB monthly. 5G standalone and fiber upgrades underpin differentiated service tiers that fetch premium pricing from industrial users seeking network-slice guarantees. Consequently, German telecom market size gains at the segment level will continue to eclipse legacy categories.

Voice Services still produced USD 3.91 billion (27.45% share) in 2025, but OTT migration and planned 2G shutdowns by 2028 portend gradual contraction. Telefonica Deutschland already routes 80% of calls via VoLTE, and both Deutsche Telekom and Vodafone are reallocating spectrum to 5G. IoT and M2M Services, worth USD 1.36 billion in 2025, exhibit the fastest 4.45% CAGR, reflecting Germany's leadership in connected-factory and automotive telematics. Pay-TV and other value-added services face direct streaming competition, yet roaming and wholesale traffic are recovering alongside international travel. As data-centric products outpace voice, overall portfolio mix shifts toward higher-growth, margin-accretive categories.

The Germany Telecom MNO Market is Segmented by Service Type (Voice Services, Data and Internet Services, Messaging Services, Iot and M2M Services, OTT and PayTV Services, and More), and End User (Enterprises, and Consumer). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Subscribers).