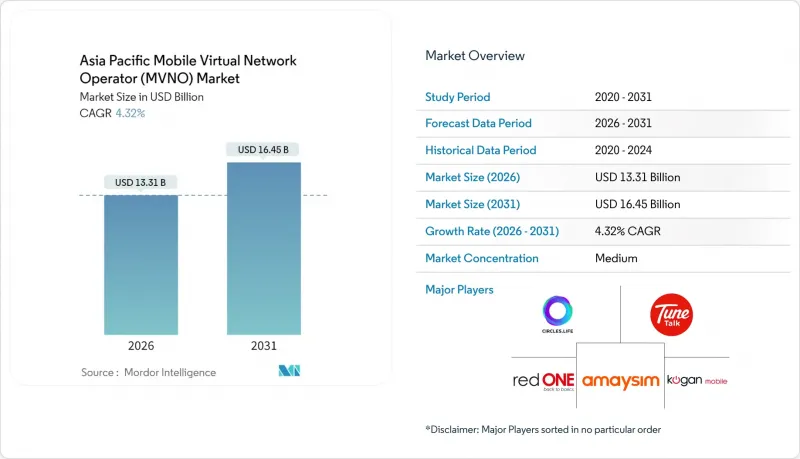

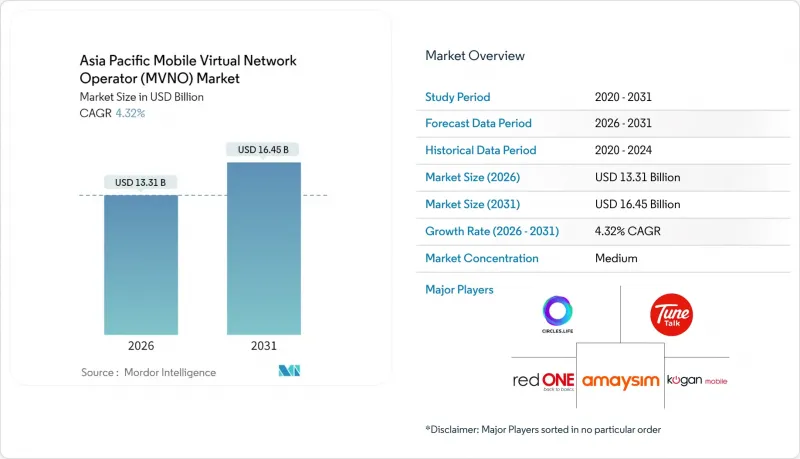

아시아태평양의 모바일 가상 네트워크 사업자(MVNO) 시장 규모는 2026년에 133억 1,000만 달러로 추정됩니다.

2025년 127억 6,000만 달러에서 성장하여 2031년에는 164억 5,000만 달러에 달할 것으로 예상됩니다. 2026년부터 2031년까지 CAGR 4.32%로 성장할 것으로 예상됩니다.

가입자 수는 2025년 8,367만 명에서 2030년까지 9,954만 명으로 확대될 것으로 예상되며, 예측 기간(2025-2030년) 동안 연평균 3.54%의 CAGR을 기록할 것으로 예측됩니다. 시장 확대는 적극적인 5G 구축, IoT 도입 확대, 규제당국 주도의 도매요금 개혁으로 진입장벽을 낮추면서 경쟁을 강화하는 등 시장 확대가 추진되고 있습니다. 클라우드 네이티브 운영 모델, 위성 통합, 핀테크 연계는 비용 효율성과 차별화를 위한 주요 수단으로, 가상 통신 사업자가 기존 이동통신사가 수익화하기 어려운 미개척 소비자 틈새 시장과 기업 사용 사례를 확보할 수 있게 해줍니다. 특히 제조업, 물류, 스마트 시티 프로그램에서의 네트워크 슬라이싱 서비스에 대한 수요 확대는 아시아태평양 MVNO 시장의 잠재 고객층을 더욱 확대시키고 있습니다. 한편, 위성/NTN 기술의 도입으로 기존에는 수익성이 떨어졌던 지방의 커버리지 영역이 개방되고 있습니다. 시장은 여전히 세분화되어 있지만, 클라우드의 확장성과 슈퍼앱의 유통 채널을 결합한 선도기업들은 이미 고객 확보 비용을 압축하고 기존 사업자들에게 도매요금 양보를 강요하고 있습니다.

한국, 일본, 중국 도시 지역에서의 적극적인 5G 커버리지 확대와 최대 52%에 달하는 도매대가 인하가 동시에 진행되면서, MVNO는 저렴한 용량과 최첨단 네트워크 슬라이싱 기능을 모두 확보할 수 있게 되었습니다. 슬라이스 기반 SLA를 통해 가상 사업자는 클라우드 게임, AR 쇼핑, 산업용 로봇을 위한 지연 보증 계층을 구축하고 있습니다. 초기 파일럿에서 공유형 Best Effort 요금제 대비 35-40ms의 지연 감소가 확인되어, 주파수 비용 부담 없이 프리미엄 ARPU를 향상시킬 수 있는 것으로 나타났습니다. 이러한 슬라이스를 기업용 VPN에 번들로 제공함으로써, MVNO는 가격 중심의 재판매업체가 아닌 관리형 서비스 통합업체로 자리매김하고 있습니다. 차이나모바일 인터내셔널이 말레이시아 파트너사와 함께 진행한 국경 간 슬라이스와 같은 지역 간 상호운용성 테스트는 슬라이스 '로밍'이 실현 가능하다는 것을 보여주며, 수출 의존도가 높은 제조업 회랑에서 차별화된 가치를 창출하고 있습니다.

일본의 스마트 팩토리 로드맵부터 중국의 '중국제조 2025' 재가동까지, 아시아의 산업정책 추진으로 인해 기존 통신사업자들이 단편적인 과금체계와 경직된 로밍 요금으로 인해 충분히 서비스를 제공하지 못하는 셀룰러 M2M 계약이 대량으로 발생하고 있습니다. 소라콤(Soracom)과 1NCE와 같은 전문 IoT MVNO는 160개국 이상에서 여러 IMSI 프로파일을 통합하여 OEM 제조업체가 사전 연결된 디바이스를 출하할 수 있도록 지원하고 있습니다. API 기반 포털을 통해 프로비저닝 리드타임을 몇 분으로 단축하고, 정액제 세계 플랜으로 수출업체의 인보이스 쇼크 리스크를 제거합니다. NB-IoT RedCap과 위성 NB-IoT가 성숙해짐에 따라, 이들 MVNO는 하나의 SIM으로 지상파와 비지상파 통신 방식을 전환할 수 있게 됩니다. 상업적 성과로, 적은 데이터 통신량에도 불구하고 기기당 ARPU가 일반 소비자 대비 2-3배에 달하고 있습니다.

인도는 소매가격이 1GB당 0.01달러 내외로 형성되어 있는 전형적인 가격 경쟁 환경이지만, MVNO 도매가격은 여전히 이보다 22-30% 이상 높은 수준이어서 차익거래의 여지가 없는 상황입니다. 또한, 기존 사업자 BSNL의 가상 브랜드 수용 능력이 제한적이기 때문에 시장 점유율 확대의 여지도 제한되어 있습니다. 말레이시아에서는 Digital Nasional Berhad의 5G 대상에서 제외된 4G 계층에서 유사한 구조적 불균형이 지속되고 있으며, 필리핀에서는 MVNO가 주파수 대역별로 상이한 접속료에 직면하고 있습니다. 이로 인한 수익률 압박은 마케팅 예산을 압박하고 손익분기점을 5년 이상 지연시키고 있습니다.

클라우드 구성은 2025년 아시아태평양 MVNO 시장 점유율의 69.58%를 차지했으며, 2031년까지 CAGR 8.54%를 기록할 것으로 예상됩니다. AWS와 Azure의 퍼블릭 클라우드 코어는 설비투자를 최대 45% 절감하고, 서비스 개시 기간을 18개월에서 6개월 이내로 단축할 수 있습니다. 이것이 2024년 이후 설립된 7개 MVNO 중 5개사가 완전한 SaaS 스택을 채택한 이유입니다. 하이퍼스케일러가 인도네시아와 태국에 새로운 구역을 개설하여 데이터 주권 요건을 충족하는 로컬 워크로드를 가능하게 함으로써, 아시아태평양의 클라우드 도입에 따른 MVNO 시장 규모는 더욱 확대될 것으로 예상됩니다. 수익배분형 상업모델을 통해 사업자는 라이선스 비용에서 자유로워지고, 운영비용을 가입자 증가 속도에 연동하여 운영할 수 있습니다.

온프레미스 솔루션은 국가 공공안전망이나 저지연이 필수적인 공장 자동화 등 규제 대상 분야에서는 여전히 유효합니다. 일본의 엣지 마이크로 데이터센터에서는 프라이빗 5G 코어를 호스팅하고 퍼블릭 인터넷을 거치지 않고 기업 WAN으로 트래픽을 전송하여 10-15밀리초의 지연을 줄였습니다. 그러나 이러한 도입 사례에서도 쿠버네티스 패키징의 활용이 늘어나면서 온프레미스와 클라우드의 경계가 점차 모호해지고 있습니다. 예측 기간 동안 클라우드의 하위 변형, 멀티 클라우드 재해 복구, 서버리스 과금, API 마켓플레이스가 혁신의 대부분을 주도하며 클라우드의 주도권을 강화할 것으로 보입니다.

리셀러/라이트형 사업자는 2025년에도 아시아태평양 MVNO 시장에서 56.62%의 점유율을 차지하며 계속 우위를 점할 것으로 예상되며, 풀 MVNO는 18.88%의 CAGR을 기록할 것으로 전망됩니다. 핵심 요소를 제어할 수 있는 풀 MVNO는 차별화된 로밍 정책 수립과 위성통신 통합이 가능하기 때문에 공급망 중심 기업에게 매우 중요합니다. 라이카 모바일이 프랑스에서 자체 코어로 전환한 결과, 국경 간 음성 마진이 22% 확대되었습니다. 이는 시그널링 플레인의 소유권이 수익화할 수 있는 기능으로 이어진다는 증거입니다.

서비스 사업자형은 절충안입니다. 고객 지원과 OSS는 자체적으로 담당하고, 코어 네트워크는 호스트 MNO에 의존하는 형태입니다. 풀코어에 대한 규제 수수료가 여전히 높은 신흥 시장에 적합합니다. 그러나 5G 슬라이싱, API 공개, 멀티 클라우드 오케스트레이션에 대한 수요가 증가함에 따라 야심 찬 브랜드는 완전한 통제권으로 전환하고 있습니다. MVNE-as-a-service 플랫폼을 통해 투자 장벽을 완화하고 초기 비용을 55% 절감할 수 있습니다. 그 결과, 기업들이 아세안 무역 통로에서 맞춤형 SLA를 요구하는 가운데, 완전 MVNO의 보급률은 2031년까지 27.4%의 볼륨 점유율에 도달할 것으로 예상됩니다.

아시아태평양 모바일 가상 네트워크 사업자(MVNO) 시장 보고서는 도입 모델(클라우드/온프레미스), 운영 모드(서비스 사업자/기타), 가입자 유형(소비자/기타), 애플리케이션(할인/기타), 네트워크 기술(2G/3G/기타), 유통 채널(온라인/디지털 전용/기타), 국가별로 구분하여 조사되었습니다. 채널(온라인/디지털 전용/기타), 국가별로 분류되어 있습니다. 시장 예측은 금액(달러) 및 수량(가입자 수) 측면에서 제공됩니다.

Asia Pacific Mobile Virtual Network Operator (MVNO) Market size in 2026 is estimated at USD 13.31 billion, growing from 2025 value of USD 12.76 billion with 2031 projections showing USD 16.45 billion, growing at 4.32% CAGR over 2026-2031.

In terms of subscriber volume, the market is expected to grow from 83.67 million subscribers in 2025 to 99.54 million subscribers by 2030, at a CAGR of 3.54% during the forecast period (2025-2030). The market's expansion is propelled by aggressive 5G roll-outs, proliferating IoT deployments, and regulator-led wholesale tariff reforms that lower entry barriers while intensifying competition. Cloud-native operating models, satellite integration, and fintech tie-ups are now primary levers for cost efficiency and differentiation, enabling virtual operators to capture underserved consumer niches and enterprise use cases that traditional MNOs find hard to monetize. Intensifying demand for network-sliced services, especially in manufacturing, logistics, and smart-city programs, further widens the addressable pool for the Asia-Pacific MVNO market, while satellite/NTN technology adoption unlocks previously uneconomic rural coverage zones. Fragmentation persists, yet early movers that combine cloud scalability with super-app distribution channels are already compressing customer acquisition costs and pushing incumbents toward wholesale rate concessions.

Aggressive nationwide 5G coverage in South Korea, Japan, and urban China is arriving alongside wholesale rate reductions of up to 52%, arming MVNOs with both affordable capacity and cutting-edge network-slicing features. With slice-based SLAs, virtual operators are crafting latency-guaranteed tiers for cloud gaming, AR shopping, and industrial robotics. Early pilots indicate latency cuts of 35-40 ms versus shared best-effort plans, translating into premium ARPU uplift without incurring spectrum costs. Bundling these slices into enterprise VPNs is letting MVNOs position themselves as managed-service integrators rather than price-led resellers. Regional interoperability trials, such as China Mobile International's cross-border slice with Malaysian partners, show that slice "roaming" is achievable, creating differentiated value in export-heavy manufacturing corridors.

Asia's industrial policy drives, from Japan's Smart Factory Roadmap to China's "Made in 2025" reboot, are spawning high-volume cellular M2M deals that conventional operators underserve because of fragmented billing and rigid roaming tariffs. Specialized IoT MVNOs such as Soracom and 1NCE aggregate multi-IMSI profiles across 160+ countries, enabling OEMs to ship pre-connected devices. Their API-driven portals cut provisioning lead times to minutes, and flat-rate global plans remove bill-shock risk for exporters. As NB-IoT RedCap and satellite NB-IoT mature, these MVNOs can toggle between terrestrial and non-terrestrial bearers from a single SIM. The commercial result is per-device ARPU that is 2-3 times consumer levels despite low data payloads.

India typifies a price war environment where retail tariffs hover near USD 0.01 per GB, yet MVNO wholesale offers remain 22-30% above that level, leaving no room for arbitrage . Additionally, incumbent BSNL's limited capacity to host virtual brands caps addressable share. Similar structural imbalances persist in Malaysia's 4G layers outside Digital Nasional Berhad's 5G scope, while Philippines MVNOs face differentiated access fees across spectrum bands. The resulting margin compression stifles marketing budgets and delays breakeven beyond the five-year mark.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cloud configurations retained 69.58% of the Asia-Pacific MVNO market share in 2025 and are tracking an 8.54% CAGR through 2031. Public-cloud cores from AWS and Azure lower capex by up to 45% while time-to-launch shrinks from 18 months to under six, explaining why 5 of 7 MVNOs launched since 2024 used a full SaaS stack. The Asia-Pacific MVNO market size for cloud deployments will widen further as hyperscalers open new zones in Indonesia and Thailand, enabling localized workloads that meet data-sovereignty mandates. Revenue-share commercial models free operators from license fees, aligning opex with subscriber ramp-up.

On-premise solutions remain relevant for regulated segments such as national public-safety networks and latency-critical factory automation. Edge-microdata centers in Japan host private 5G cores that export traffic to corporate WANs without traversing public Internet, shaving 10-15 ms latency. Yet even these deployments increasingly leverage Kubernetes packaging, blurring the line between on-premise and cloud. Over the forecast horizon, cloud sub-variants, multi-cloud disaster recovery, serverless billing, and API marketplaces will drive most innovation, reinforcing cloud's leadership.

Reseller/light constructs still dominate the Asia-Pacific MVNO market with a 56.62% share in 2025, but full MVNOs are projected to post a 18.88% CAGR. Control over core elements lets full MVNOs craft differentiated roaming policies and integrate satellite switching, critical for supply-chain-centric enterprises. Lycamobile's migration onto its own core in France yielded 22% cross-border voice margin expansion, evidence that ownership of signaling planes translates into monetizable features .

Service-operator formats provide a compromise: they assume customer care and OSS but rely on host-MNO cores. This suits emerging markets where regulatory fees on full cores remain onerous. However, the mounting need for 5G slices, API exposure, and multi-cloud orchestration is nudging ambitious brands toward full control. Investment hurdles are mitigated by MVNE-as-a-service platforms, cutting upfront spend by 55%. Consequently, full MVNO penetration is set to reach 27.4% volume share by 2031 as enterprises seek bespoke SLAs across ASEAN trade corridors.

The Asia Pacific Mobile Virtual Network Operator (MVNO) Market Report is Segmented by Deployment Model (Cloud, and On-Premise), Operational Mode (Service Operator, and More), Subscriber Type (Consumer, and More), Application (Discount, and More), Network Technology (2G/3G, and More), Distribution Channel (Online/Digital-only, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Subscribers).