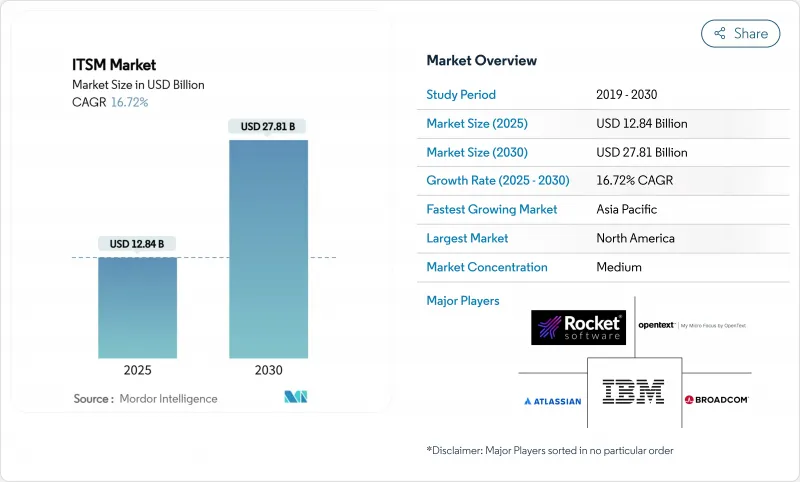

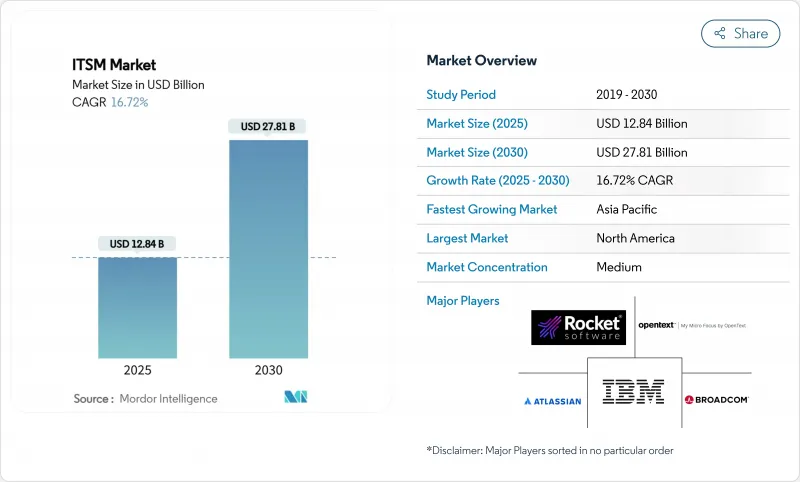

IT 서비스 관리(ITSM) 시장의 2025년 시장 규모는 128억 4,000만 달러로 평가되었고, 2030년에 CAGR은 16.72%를 나타낼 것으로 예측되며, 278억 1,000만 달러로 성장할 것으로 예측됩니다.

이 가속은 AI 기반 자동화의 기업 내 급속한 도입, 클라우드 네이티브 아키텍처로의 전환, 하이브리드 및 멀티클라우드 환경 전반에 걸친 통합 관리의 필요성입니다. 기업들은 기술 인력 부족을 상쇄하기 위해 로우코드 오케스트레이션도 도입하고 있으며, 핀옵스(FinOps) 및 그린옵스(GreenOps) 보고는 지속가능성과 비용 통제 지표를 IT 워크플로우에 직접 내재화합니다. 엣지 컴퓨팅과 5G 도입은 분산된 디바이스가 실시간 지원을 필요로 함에 따라 IT 서비스 관리 시장의 범위를 더욱 확장합니다.

클라우드 네이티브 도입은 기존 시스템과 연관된 연간 40,000달러의 유지보수 부담을 제거하여 혁신을 위한 예산을 확보합니다. 하이퍼스케일러와의 전략적 제휴는 AI 기능을 위한 탄력적 컴퓨팅을 가능하게 하여 2025년 1분기 구독 매출이 전년 동기 대비 19% 성장했습니다. 제조업체의 클라우드 전환으로 지원 시간이 30분에서 6분으로 단축되며 생산성 향상이 두드러졌습니다. 얼리 어답터는 비용 및 속도 이점을 확보하여 클라우드 네이티브 역량이 IT 서비스 관리 시장 전반의 기본 요건으로 자리매김했습니다.

ServiceNow는 AI 계약에서 분기 대비 150% 성장을 기록했으며, 2025년 ServiceNow에서 AI 고객 1,000사를 돌파했습니다. AIOps는 평균 해결 시간(MTTR)을 최대 60% 단축하여 티켓 백로그를 감소시킵니다. IBM의 생성형 AI 매출은 2025년 60억 달러에 달하며, 자율 운영에 대한 기업의 수요를 입증했습니다. 대화형 인터페이스를 내장한 벤더들은 접근성을 더욱 민주화하여 구매자 기대치를 변화시키고 경쟁 차별화를 강화합니다.

기업들은 기존 시스템당 연간 40,000달러를 투자하며 주당 17시간을 유지보수 작업에 소모합니다. 보안 취약점은 위험을 높이지만, 데이터를 보호하는 단계적 마이그레이션은 전환 후 최대 277%의 ROI를 제공합니다. 비용은 기존 공급업체의 입지를 유지하는 장벽이 되지만, 현대화를 추진하는 조직은 상당한 효율성 향상을 누립니다.

클라우드 전개는 2024년 IT 서비스 관리 시장의 64.8%를 차지했으며, 2030년까지 연평균 18.3% 성장할 것으로 전망됩니다. 기업들은 자본 지출 없이 AI 기능을 활용하고 글로벌 운영을 관리하기 위해 클라우드를 선택합니다. 방위 산업과 같은 데이터 주권 환경에서는 온프레미스 방식이 여전히 필수적입니다. 마이크로소프트가 내부 ServiceNow 인스턴스를 Azure로 마이그레이션한 사례와 같이, 클라우드의 혁신 확장 역할은 실제 사례에서 입증됩니다.

클라우드는 사전 구축된 통합 기능을 제공하므로 멀티클라우드 환경과도 부합합니다. ServiceNow와 AWS의 전략적 협력은 다양한 산업 분야의 AI 기반 애플리케이션을 아우르며 이러한 추세를 보여줍니다. 결과적으로 클라우드는 현대적 IT 서비스 관리 시장 역량을 확보하기 위한 기본 경로로 자리매김하고 있습니다.

서비스 데스크 및 인시던트 관리는 IT 지원의 기초 관문으로서 2024년 35.3% 점유율을 유지했습니다. 자산 탐색 수요에 힘입은 구성 및 자산 관리는 연평균 17.9% 성장할 전망입니다. 탐색, 종속성 매핑, 인시던트 워크플로우를 통합하는 결합 플랫폼 접근법은 예산 우선순위를 변화시킵니다. 구성 및 자산 관리 분야의 IT 서비스 관리 시장 규모는 2025년부터 2030년 사이에 두 배로 성장할 것으로 전망됩니다.

AI는 모든 애플리케이션의 성능을 한 단계 끌어올립니다. ServiceNow의 AI 에이전트 오케스트레이터는 티켓 해결을 위해 여러 자율 에이전트가 협력하여 수동 작업을 줄이는 방식을 보여줍니다. DevOps 및 하이브리드 아키텍처가 통합된 가시성을 요구함에 따라 변경, 릴리스, 네트워크, 데이터베이스 관리 부문은 꾸준히 성장하고 있습니다.

북미는 2024년 매출의 37.2%를 차지하며 기업 및 공공 부문 내 확고한 설치 기반을 바탕으로 주도권을 유지하고 있습니다. 최근 연방 계약 건당 100만 달러를 초과하며 지속적인 플랫폼 업등급를 강조하고 있습니다. 지역적 초점은 초기 전개에서 고급 AI 및 크로스 도메인 가시성으로 전환되고 있습니다.

아시아태평양 지역은 가장 빠르게 성장하는 지역입니다. 기업들이 민첩성을 유지하기 위해 ITSM을 아웃소싱함에 따라 2025년 관리형 서비스 수요가 32% 급증했습니다. 중국 제조업체와 은행들은 대규모로 운영을 디지털화하고 있으며, 일본의 미쓰비시 UFJ 은행은 2025년 ServiceNow 도입을 통해 연간 2,200시간을 절감했습니다. 인도의 글로벌 아웃소싱 리더십과 함께 국내 수요도 강화되고 있습니다.

유럽, 남미, 중동, 아프리카는 다양한 기회를 보여줍니다. 유럽 기업들은 엄격한 데이터 보호법과 향후 도입될 AI 거버넌스 프레임워크를 준수하는 ITSM 솔루션이 필요합니다. 지속가능성 보고는 FinOps 및 GreenOps 모듈의 전망을 밝게 합니다. 라틴 아메리카는 클라우드 도입을 통해 채택 속도가 가속화되는 반면, GCC 국가들은 스마트 시티 이니셔티브를 위해 ITSM에 투자하고 있습니다. 아프리카의 통신 및 정부 부문은 초기 단계이지만 저렴한 클라우드 기반 플랫폼을 위한 유망한 시장으로 부상하고 있습니다.

The IT service management market was valued at USD 12.84 billion in 2025 and is forecast to grow to USD 27.81 billion by 2030, reflecting a 16.72% CAGR.

The acceleration stems from three forces: rapid enterprise adoption of AI-driven automation, the migration to cloud-native architectures, and the need for unified management across hybrid and multicloud estates. Enterprises are also embracing low-code orchestration to offset skills shortages, while FinOps and GreenOps reporting embed sustainability and cost-control metrics directly into IT workflows. Edge-computing and 5G onboarding further expands the scope of the IT service management market as distributed devices require real-time support.

Cloud-native adoption removes the USD 40,000 annual maintenance burden linked to legacy systems, freeing budgets for innovation. Strategic alliances with hyperscalers enable elastic compute for AI features, driving 19% year-over-year subscription growth in Q1 2025. Migrating manufacturers cut support times from 30 minutes to 6 minutes, highlighting productivity gains. Early adopters gain cost and speed advantages, making cloud-native capability a baseline requirement across the IT service management market.

ServiceNow recorded 150% quarter-over-quarter growth in AI deals and surpassed 1,000 AI customers in 2025 ServiceNow. AIOps shortens mean time to resolution by up to 60%, reducing ticket backlogs. IBM's generative AI revenue reached USD 6 billion in 2025, underscoring enterprise appetite for autonomous operations.Vendors embedding conversational interfaces further democratize access, altering buyer expectations and sharpening competitive differentiation.

Enterprises devote USD 40,000 annually per legacy system and lose 17 hours a week to maintenance tasks.Security vulnerabilities heighten risk, yet phased migrations that safeguard data deliver up to 277% ROI post-transition. The expense forms a barrier, preserving incumbent vendor positions, but organizations that modernize enjoy significant efficiency gains.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cloud deployments accounted for 64.8% of the IT service management market in 2024 and are projected to grow at 18.3% CAGR to 2030. Organizations select cloud to access AI functions and manage global operations without capital outlays. On-premise remains essential for data-sovereign environments such as defense. Real-world cases such as Microsoft migrating internal ServiceNow instances to Azure show cloud's role in scaling innovation.

Cloud also aligns with multicloud realities because it offers pre-built integrations. ServiceNow's strategic collaboration with AWS covers AI-powered applications across diverse industries and illustrates the momentum. Consequently, cloud is becoming the default path to modern IT service management market capabilities.

Service Desk and Incident Management retained 35.3% share in 2024 as the foundational gateway to IT support. Configuration and Asset Management, fueled by asset discovery needs, will expand at 17.9% CAGR. A combined platform approach that unifies discovery, dependency mapping, and incident workflows changes budget priorities. The IT service management market size for Configuration and Asset Management is forecast to double between 2025 and 2030.

AI further elevates every application. ServiceNow's AI Agent Orchestrator demonstrates multiple autonomous agents collaborating on ticket resolution to cut manual toil. Change, Release, Network, and Database Management segments climb steadily because DevOps and hybrid architectures demand integrated visibility.

IT Service Management Market Report is Segmented by Deployment (Cloud, On-Premises), Application (Service Desk and Incident Management, Configuration and Asset Management, and More), End-User Industry (BFSI, Manufacturing, IT and Telecommunications, and More), Enterprise Size (Large Enterprises, Smes), Service Type (Solutions, Services), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America retains leadership with 37.2% of 2024 revenue and an entrenched install base among enterprises and the public sector. Recent federal contracts surpass USD 1 million each, underscoring continued platform upgrades. Regional focus is shifting from first-time deployments toward advanced AI and cross-domain observability.

Asia-Pacific is the fastest-growing region. Managed services demand surged 32% in 2025 as companies outsource ITSM to stay agile. Chinese manufacturers and banks digitize operations at scale, while Japan's Mitsubishi UFJ Bank recorded 2,200 hours saved annually through its 2025 ServiceNow rollout. India's domestic demand strengthens alongside its global outsourcing leadership.

Europe, South America, Middle East, and Africa illustrate diverse opportunities. European enterprises need ITSM solutions that respect stringent data-protection laws and upcoming AI governance frameworks. Sustainability reporting brightens prospects for FinOps and GreenOps modules. Latin American adoption accelerates through cloud uptake, whereas GCC states invest in ITSM for smart-city initiatives. African telco and government segments form an early-stage but promising arena for affordable, cloud-based platforms.