중동의 민간 항공기 기내 엔터테인먼트 시스템 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)

Middle East Commercial Aircraft In-Flight Entertainment System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1693715

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

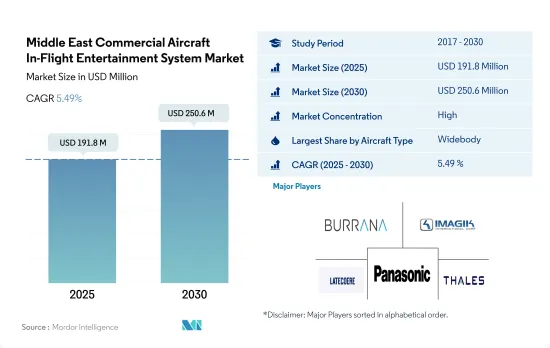

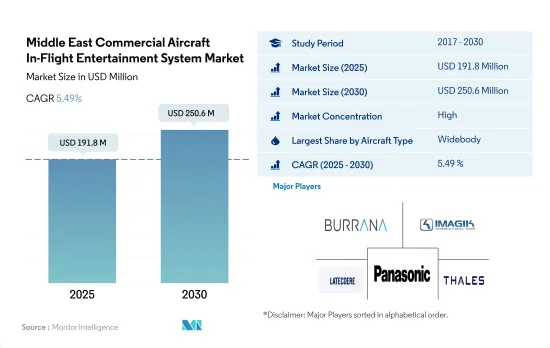

중동의 민간 항공기 기내 엔터테인먼트 시스템 시장 규모는 2025년에 1억 9,180만 달러, 2030년에는 2억 5,060만 달러에 달할 것으로 예상되며, 예측 기간(2025-2030년) 동안 5.49%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다.

중동에서는 와이드바디 항공기의 인기가 높아지고 승객의 편안함과 엔터테인먼트를 우선시하는 항공사가 증가함에 따라 민간 항공기 기내 엔터테인먼트 시스템에 대한 수요가 급증할 것으로 예측됩니다.

최근 몇 년 동안 기내 엔터테인먼트는 기내 인테리어의 필수 요소로 자리 잡았으며, 승객의 전체 비행 경험을 결정하는 중요한 역할을 하고 있습니다. 이 지역, 특히 사우디아라비아와 아랍에미리트에서 와이드바디 부문의 항공기 인도 대수가 압도적으로 많았으며, 2017-2022년 전체 점유율은 52%에 달했습니다. 협동체와 와이드바디를 포함한 전체 여객기 카테고리는 2020년에 30%의 감소를 보였습니다. 이는 대륙간 및 국제선 노선의 이동이 제한되었기 때문입니다. 또한, 항공사의 신규 항공기 증설 지연으로 인해 신규 항공기 조달도 영향을 받았습니다.

2022년에는 이 지역에 인도된 모든 협동체형 항공기의 IFE 시스템 중 캐빈 클래스, 이코노미, 프리미엄 이코노미가 약 90%를 차지할 것으로 예측됩니다. 중동의 많은 항공사들이 장거리 노선에 협동체 항공기를 도입하고 있으며, 이에 따라 IFE 시스템 도입이 증가하고 있습니다. 이 지역의 주요 항공사인 Emirates는 IFE 시스템 부문에서 비즈니스 클래스 좌석을 늘리고 고객 경험을 개선하는 데 주력하고 있습니다.

2023-2030년 사우디아라비아, 카타르, 아랍에미리트 등 주요 시장을 중심으로 약 543대의 협동기와 401대의 와이드바디 항공기가 이 지역에 인도될 예정입니다. 이 지역의 항공기 보유 대수 확대 계획은 협동체 및 와이드바디 항공기 조달을 촉진할 것으로 예측됩니다. 이러한 요인들은 예측 기간 동안 민간 항공기 IFE 시스템의 성장을 가속할 것으로 예측됩니다.

아랍에미리트는 아랍에미리트 항공사가 대량의 항공기를 주문하고 있어 이 지역에서 더 높은 성장이 예상되고 있습니다.

항공사의 경우, 고객 경험은 항상 최우선 순위입니다. 승객은 여행할 때마다 긍정적인 경험을 해야 합니다. 최고의 경험을 제공하기 위해 지역 항공사는 여행 중 완벽한 승객 경험을 정의하는 데 점점 더 중요한 역할을하는 최신 IFE 시스템을 제공하는 데 주력하고 있습니다.

중동 시장에서는 탈레스, 사프란, 파나소닉이 IFE 시스템을 제공하는 주요 기업입니다. 에미레이트 항공, 카타르 항공, 사우디아라비아 항공, 에티하드 항공, 이란 항공, 플라이 두바이 항공 등 주요 항공사는 A320, A330, A380, Boeing777, Boeing737 MAX 8, Boeing787 Dreamliner 등 새로 납품된 항공기의 모든 캐빈 클래스에 상기 OEM의 IFE 시스템을 채택하고 있습니다. 또한, 이들 항공사는 4K 스크린과 OLED 디스플레이의 채택에 중점을 두고 기존 서비스를 개선하고 신규 고객을 유치하기 위해 IFE 시스템의 가용성을 높이고 있습니다.

중동의 민간 항공기 기내 엔터테인먼트 시스템에 대한 수요는 다양한 항공사의 항공기 교체 주문과 장거리 비행을 위한 연료 효율이 높은 항공기의 필요성에 기인합니다. 에어 아라비아, 에미레이트 항공, 에티하드 항공과 같은 이 지역의 주요 항공사들은 391대의 협폭동체 항공기와 413대의 광폭동체 항공기를 주문했습니다. 이 중 에미레이트항공, 에티하드항공, 플라이두바이 등 아랍에미레이트의 주요 항공사가 361대를 주문했습니다. Boeing에 따르면 중동은 향후 20년간 급증하는 승객 수를 충족시키기 위해 3,400대의 제트기가 필요할 것으로 예상되며, 이러한 대규모 주문으로 인해 아랍에미리트는 더 높은 성장이 예상되고 있습니다. 기술 혁신과 고객 선호도 증가가 예측 기간 동안 시장을 견인할 것으로 예측됩니다.

중동 민항기용 기내 엔터테인먼트 시스템 시장 동향

시장 성장의 주요 원인은 중동 국가들의 항공기 보유 대수 확대와 여객 항공 수요 증가

중동의 항공 산업은 기타 중동 및 아프리카보다 빠르게, 그리고 강력하게 코로나19 팬데믹에서 회복했으며, 2021년 중동의 항공 승객 수는 3억 2천만 명에 달하며, 2020년 대비 249%, 2019년 대비 25% 성장했습니다. 항공 승객 수 증가는 결국 항공기의 신규 조달을 촉진하고 이 지역의 객실 인테리어 시장을 촉진할 수 있습니다. 주요 항공사는 항공기 확장 전략을 채택하고 있습니다.

2017-2022년 이 지역에서는 총 498대의 항공기가 새로 인도되었으며, 2023-2030년에는 약 1,058대의 항공기가 새로 인도될 것으로 예측됩니다. 예측 기간 동안 대부분의 항공기는 협동체가 될 것으로 예측됩니다. 또한, 작고 경제적인 항공기의 인기, 저가 항공사의 성공, 항속거리가 긴 협동체 항공기의 등장 등이 이러한 추세에 박차를 가하고 있습니다. 사우디아라비아와 아랍에미레이트가 항공기 인도 대수의 대부분을 차지하는 주요 국가입니다.

이 지역의 다양한 항공사가 LED 기내 조명, 무선 경량 IFES, 편안하고 가벼운 좌석, 기타 기내 제품 등 첨단 항공기 시스템 및 구성 요소를 선택하고 있기 때문에 새로운 항공기 인도 및 주문 잔고는 객실 내장재에 대한 수요를 창출할 것으로 예측됩니다. 2022년 11월 현재 에미레이트 항공, 카타르 항공, 사우디아라비아 항공, 에티하드 항공, 플라이 두바이 항공 등 주요 항공사는 총 1,013대 이상의 항공기를 주문했으며, 이 중 589대가 협동체 제트기일 것으로 예측됩니다. 이러한 요인들은 예측 기간 동안 객실 내장재 시장을 긍정적으로 견인할 것으로 예측됩니다.

지속적인 항공 여행 성장으로 중동 항공 여객 수송량 증가 견인

국제 여행객과 무역의 중계지로서 인기가 높은 중동은 비즈니스 및 레저 여행객의 출발지 및 목적지로서도 성장하고 있으며, 2020년 중동의 항공 여객 수송량은 코로나19 팬데믹으로 인한 여행 제한으로 64% 감소했습니다. 그러나 2022년에는 백신 접종률 상승과 휴가철 수요 증가로 인해 이 지역의 항공 여객 수송량은 3억 4,950만 명으로 2021년 대비 16%, 2019년 대비 45% 성장했습니다. 아랍에미리트와 사우디아라비아 등 주요 국가들이 전체 항공 여객 수송량의 42%를 차지하며 기타 중동 국가들에 비해 신형 항공기에 대한 높은 수요를 창출했습니다.

2022년 여객 수송능력은 2021년 대비 73.8% 증가했고, 여객 탑승률은 24.6% 증가한 75.8%를 기록했습니다. 이 지역의 항공 여행 회복세는 계속 탄력을 받고 있으며, 항공 여객 수송량은 향후 20년 내에 두 배로 늘어날 것으로 예측됩니다. 바레인, 쿠웨이트, 오만, 사우디아라비아, 아랍에미리트, 이라크, 이란, 요르단, 예멘, 카타르 등 중동의 주요 국제선 노선 중 상당수는 이미 코로나19 이전 수준을 넘어섰습니다. 이는 항공 여행이 회복세를 보이고 있으며, 계속해서 탄력을 받고 있음을 보여줍니다. 중동 내에서도 많은 주요 국제선 노선이 이미 코로나19 이전 수준을 넘어섰습니다. 높은 관광 및 여행 의욕이 중동 및 아프리카의 항공 산업 회복을 지속적으로 견인하고 있습니다. 항공 여객 수송량은 2022년에 비해 2030년에 34% 증가할 것으로 예측됩니다.

중동 민항기 기내 엔터테인먼트 시스템 산업 개요

중동의 민항기용 기내 엔터테인먼트 시스템 시장은 상당히 통합되어 있으며, 상위 5개 업체가 75.46%를 차지하고 있습니다. 이 시장의 주요 기업으로는 Burrana, IMAGIK International Corp., Latecoere, Panasonic Avionics Corporation, Thales Group 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 오퍼

제3장 서론

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

항공 여객 운송량

신규 항공기 납입수

1인당 GDP(현행 가격)

항공기 제조업체의 판매량

항공기 수주잔고

수주 총액

공항 건설 지출(지속 중)

항공사 연료비

규제 프레임워크

밸류체인과 유통 채널 분석

제5장 시장 세분화

항공기 유형

내로우 바디

와이드 바디

국가별

사우디아라비아

아랍에미리트(UAE)

기타 중동

제6장 경쟁 구도

주요 전략적 움직임

시장 점유율 분석

기업 상황

기업 개요

Burrana

IMAGIK International Corp.

Latecoere

Panasonic Avionics Corporation

Thales Group

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보원과 참고 문헌

도표

주요 인사이트

데이터 팩

용어집

LSH

영문 목차

영문목차

The Middle East Commercial Aircraft In-Flight Entertainment System Market size is estimated at 191.8 million USD in 2025, and is expected to reach 250.6 million USD by 2030, growing at a CAGR of 5.49% during the forecast period (2025-2030).

The Middle East is expected to experience a surge in demand for commercial aircraft in-flight entertainment systems as a result of the increasing popularity of widebody aircraft and airlines that prioritize passenger comfort and entertainment

In-flight entertainment has become an integral component of cabin interiors over recent years, playing an increasingly crucial part in defining a passenger's entire flight experience. The widebody segment dominated the deliveries in the region, especially the deliveries across Saudi Arabia and the United Arab Emirates, accounting for an overall share of 52% during 2017-2022. The overall passenger aircraft category, including narrowbody and widebody aircraft, witnessed a decline of 30% in 2020. This was due to the restrictions on travel across intercontinental and international routes. The procurement of new aircraft was also affected due to delays by airline companies in adding new aircraft to their fleet sizes.

In 2022, cabin class, economy, and premium economy accounted for around 90% of the overall IFE systems of all narrowbody aircraft delivered in the region. The adoption of narrowbody aircraft in long-haul routes of many Middle Eastern airlines has increased, thereby increasing the deployment of IFE systems. Emirates, the major airline in the region, is focused on increasing the number of its business-class seats and improving customer experience in the IFE systems segment.

It is expected that around 543 narrowbody aircraft and 401 widebody aircraft are scheduled to be delivered in the region with major markets such as Saudi Arabia, Qatar, and the United Arab Emirates during 2023-2030. The fleet expansion plans in the region are expected to aid the procurement of both narrowbody and widebody aircraft. These factors will drive the growth of commercial aircraft IFE systems during the forecast period.

The UAE is expected to witness higher growth in the region due to huge aircraft orders placed by the country's airlines

Customer experience is always a top priority for airlines. Passengers must have a positive experience every time they travel. To provide the best experience, regional airlines are focusing on providing the latest IFE systems that play an increasingly important role in defining the complete passenger experience during their travel.

Thales, Safran, and Panasonic are the major players in providing IFE systems in the Middle Eastern market. Major airlines, such as Emirates, Qatar Airways, Saudia Arabia Airlines, Etihad Airways, Iran Air, and FlyDubai Airlines are some of the carriers that have opted for the abovementioned OEMs' IFE systems in their newly delivered aircraft, such as A320, A330s, A380s, Boeing 777s, Boeing 737 MAX 8, and Boeing 787 Dreamliner in all cabin classes. Additionally, these airlines are emphasizing the adoption of 4K screens and OLED displays and increasing the availability of IFE systems to improve their existing services and attract new customers.

The demand for commercial aircraft in-flight entertainment systems in the Middle East is based on the aircraft orders that different airlines are putting out as part of their fleet renewal and the need for fuel-efficient aircraft over long distances. Some of the biggest airlines in the region, like Air Arabia, Emirates, and Etihad, have ordered 391 narrowbody planes and 413 widebody planes. Out of this, UAE's leading airlines like Emirates, Etihad, and Flydubai have ordered 361 planes. The UAE is expected to see higher growth due to these huge orders. According to Boeing, the Middle East will need a fleet of 3,400 jets over the next two decades to keep up with the fast-growing passenger numbers. Innovations and rising customer preferences are expected to drive the market during the forecast period.

Middle East Commercial Aircraft In-Flight Entertainment System Market Trends

The main reasons for market growth are the expansion of the fleet and the increased demand for passenger air travel in Middle Eastern countries

The aviation industry in the Middle East recovered from the COVID-19 pandemic faster and stronger than the rest of the world. In 2021, air passenger traffic in the Middle East reached 302 million, a growth of 249% compared to 2020 and 25% compared to 2019. The increase in air passenger traffic may eventually drive new aircraft procurements, boosting the cabin interior market in the region. Major airlines have adopted fleet expansion strategies.

A total of 498 new aircraft were delivered in the region between 2017 and 2022. During 2023-2030, around 1,058 new aircraft are expected to be delivered in the region. During the forecast period, the majority of aircraft are expected to be narrowbody. In addition, the popularity of small and economical aircraft, the success of low-cost carriers, and the advent of narrowbodies with long ranges have contributed to this trend. Saudi Arabia and the United Arab Emirates are the major countries accounting for a significant number of aircraft deliveries.

New aircraft deliveries and backlogs are expected to generate demand for cabin interiors, as various airlines in the region are opting for advanced aircraft systems and components such as LED cabin lights, wireless lightweight IFES, comfortable, lightweight seats, and other cabin products. As of November 2022, major airlines, such as Emirates, Qatar Airways, Saudia Arabia Airlines, Etihad Airways, and FlyDubai Airlines, together had a backlog of over 1,013 aircraft, of which 589 were expected to be narrowbody jets. Factors such as these are expected to drive the cabin interior market positively during the forecast period.

Consistent growth in air travel is the driving factor for air passenger traffic in the Middle East

The Middle East, a popular connection point for international travelers and trade, is also growing as a starting point and destination for business and leisure passengers. In 2020, air passenger traffic in the Middle East dropped by 64% due to travel restrictions caused by the COVID-19 pandemic. However, in 2022, due to the rising vaccination rates and strong demand over the holiday season, air passenger traffic in the region reached 349.5 million, a growth of 16% compared to 2021, while the growth was at 45% compared to 2019. Major countries, such as the United Arab Emirates and Saudi Arabia, accounted for 42% of the total air passenger traffic, generating higher demand for new aircraft compared to other Middle Eastern countries.

In 2022, passenger capacity increased by 73.8%, and passenger load factor grew by 24.6% to 75.8% compared to 2021. Air travel recovery in the region continues to gather momentum, and air passenger traffic is expected to double within the next 20 years. Many major Middle Eastern international route areas in Bahrain, Kuwait, Oman, Saudi Arabia, the United Arab Emirates, Iraq, Iran, Jordan, Yemen, and Qatar are already exceeding pre-COVID-19 levels. Such factors indicate that air travel has recovered and continues to gather momentum. Many major international routes, even within the Middle East, are already exceeding pre-COVID-19 levels. Tourism and the high willingness to travel continue to foster the industry's recovery in the Middle East & Africa. The air passenger traffic levels are expected to grow by 34% in 2030 compared to 2022.

Middle East Commercial Aircraft In-Flight Entertainment System Industry Overview

The Middle East Commercial Aircraft In-Flight Entertainment System Market is fairly consolidated, with the top five companies occupying 75.46%. The major players in this market are Burrana, IMAGIK International Corp., Latecoere, Panasonic Avionics Corporation and Thales Group (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Air Passenger Traffic

4.2 New Aircraft Deliveries

4.3 GDP Per Capita (current Price)

4.4 Revenue Of Aircraft Manufacturers

4.5 Aircraft Backlog

4.6 Gross Orders

4.7 Expenditure On Airport Construction Projects (ongoing)

4.8 Expenditure Of Airlines On Fuel

4.9 Regulatory Framework

4.10 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

5.1 Aircraft Type

5.1.1 Narrowbody

5.1.2 Widebody

5.2 Country

5.2.1 Saudi Arabia

5.2.2 United Arab Emirates

5.2.3 Rest of Middle East

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles

6.4.1 Burrana

6.4.2 IMAGIK International Corp.

6.4.3 Latecoere

6.4.4 Panasonic Avionics Corporation

6.4.5 Thales Group

7 KEY STRATEGIC QUESTIONS FOR COMMERCIAL AIRCRAFT CABIN INTERIOR CEOS