남미의 하이브리드 전기자동차 배터리 시장 : 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

South America Hybrid Electric Vehicle Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1636518

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

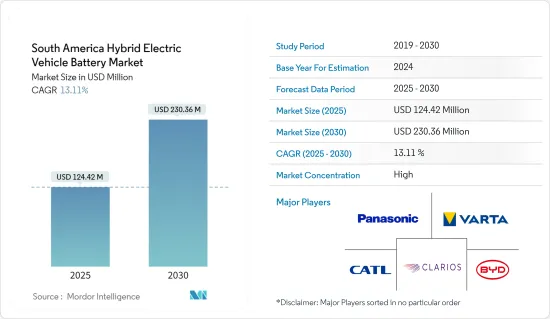

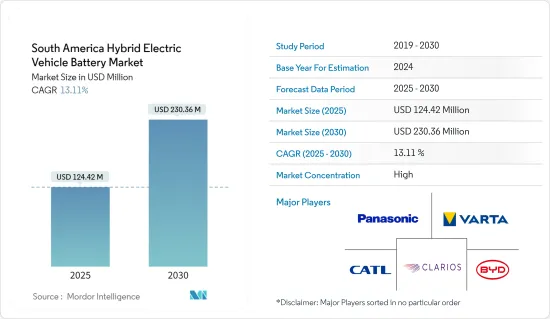

남미의 하이브리드 전기자동차 배터리 시장 규모는 2025년 1억 2,442만 달러, 2030년 2억 3,036만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 13.11%에 이를 것으로 예측됩니다.

주요 하이라이트

중기적으로는 정부의 다양한 지원제도에 따라 전기차 도입이 확대되고 있으며 예측기간 중 남미의 하이브리드 전기차용 배터리 시장 수요를 견인할 것으로 예상됩니다.

한편, 원재료의 수급 불균형이 예측기간 동안 시장 성장을 방해할 것으로 예상됩니다.

그럼에도 불구하고 전기자동차에 솔리드 스테이트 배터리를 채택하고 자동차 및 배터리 제조업체의 협업은 미래에 남미 하이브리드 전기자동차 배터리 시장에 큰 기회를 가져올 것으로 예상됩니다.

브라질은 배출가스를 억제하기 위해 전기자동차를 늘리는 것을 목표로 하는 정부의 이니셔티브로 상당한 성장이 예상됩니다.

남미의 하이브리드 전기자동차 배터리 시장 동향

리튬 이온 배터리가 크게 성장

예측 기간 동안 리튬 이온 배터리는 남미 하이브리드 전기자동차 배터리 시장을 독점할 전망입니다. 리튬 이온 배터리의 인기가 증가하고 다른 유형의 배터리를 능가하는 것은 유리한 용량 대 중량비, 우수한 성능(긴 수명, 최소 유지 보수 등), 인상적인 보존 기간, 현저한 가격 감소로 인한 것입니다.

기존의 납 배터리와 비교하면 리튬 이온(Li-ion) 배터리는 기술적으로 명확한 이점을 보여줍니다. 리튬 이온 배터리는 일반적으로 5,000 사이클 이상이며 납 배터리의 400-500 사이클과는 대조적입니다. 또한 리튬 이온 배터리는 유지 보수 및 교체 빈도가 적습니다. 또한 방전 사이클을 통해 일정한 전압을 유지하기 때문에 전기 부품의 효율도 오래 걸립니다.

최근 업계의 대기업은 리튬 이온 배터리의 성능을 높이기 위해 규모의 경제와 연구 개발에 중점을 두고 투자를 강화하고 있습니다. 이러한 경쟁이 급증함에 따라 리튬 이온 배터리의 가격이 현저하게 떨어지고 있습니다. 기술 발전, 제조 최적화, 원재료 비용 감소로 인해 리튬 이온 배터리의 평균 가격은 2013년 780달러/kWh에서 2023년 139달러/kWh로 급락했습니다. 예측은 2025년에는 약 113달러/kWh, 2030년에는 80달러/kWh까지 더 하락할 것입니다. 이러한 배터리 비용의 감소 동향은 하이브리드 EV를 포함한 전기자동차(EV) 산업의 모든 배터리 중에서 리튬 이온 배터리를 유리한 옵션으로 만들 가능성이 높습니다.

남미의 리튬 이온 배터리 제조 산업은 아직 초기 단계에 있지만, 이 대륙에 풍부하게 매장되어 있는 필수 원재료와 다양한 최종 사용자로부터의 급증하는 수요는 시장의 급속한 확대를 시사하고 있습니다.

예를 들면, 남미는 리튬 이온 전지의 기초가 되는 방대한 리튬 매장량을 자랑하고 있습니다. 리튬 트라이앵글이라 불리는 이 지역에는 아르헨티나, 볼리비아, 칠레가 포함되어 있어 세계의 리튬 매장량의 절반 이상이 확인되고 있습니다. 칠레는 아타카마 사막에 리튬을 풍부하게 함유한 칸수이 광상이 있기 때문에 주요 생산국으로서 두드러지고 있습니다. 볼리비아는 우유니 소금 호수에 대량의 리튬을 매장하고 있지만 채굴의 과제에 직면하고 있습니다. 이들 국가들이 세계의 리튬 이온 전지 생산 공급 체인에 필수적인 존재가 되고 있습니다.

미국 지질 조사소에 따르면 2023년 리튬 생산량은 주목할 만합니다. 칠레 생산량은 약 4만 4,000톤, 아르헨티나는 9,600톤, 브라질은 4,900톤입니다. 이 총 생산량은 세계의 리튬 상황에서 남미가 매우 중요한 역할을 담당하고 있음을 강조합니다.

남미 국가는 전기자동차 공급망에 대한 참여를 깊게하는 노력을 강화하고 있습니다. 아르헨티나, 칠레, 볼리비아, 브라질 등의 국가들은 광물 자원을 풍부하게 활용하고, 가공 능력을 강화하고, 자동차 제조를 시야에 넣어 채굴된 리튬을 더 많은 배터리 화학물질로 변환하고, 결국 배터리와 EV로 변환하는 전략을 세우고 있습니다. 그러나 이러한 협력적인 노력은 생산과 가격 조정에 미치지 못합니다.

2023년 4월 중국의 주요 전기자동차 제조업체 BYD는 칠레의 안토파가스타 지방에 2억 9,000만 달러의 리튬 양극 공장을 건설할 계획을 발표했다고 칠레 경제개발기관 CORFO가 보도했습니다. 이러한 투자는 향후 수년간 급증할 것으로 예상됩니다.

2023년 중반, 아르헨티나 정부는 최초의 리튬 이온 배터리 공장의 계획을 밝혔습니다. 이 공장에서는 미국의 주요 광산회사 Livent Corporation이 현지에서 조달·가공한 탄산리튬을 이용합니다. 국영 YPF의 자회사인 YPF Tecnologia(Y-TEC)가 건설하는 이 공장은 아르헨티나의 풍부한 리튬 매장량에 부가가치를 부여하려는 움직임을 의미합니다. 700만 달러를 투자해 연간 생산 능력 13MWh, 거치형 축전지 1,000대를 목표로 합니다. 게다가 리튬이온전지의 생산을 시야에 넣고 있는 현지 기업과의 기술이전을 촉진하려고 하고 있습니다.

리튬 이온 전지는 경량으로, 급속 충전이 가능하고, 충전 사이클이 길고, 비용이 싸고, 리튬 매장량도 풍부한 것으로부터, 향후 수년에 급성장을 이룰 것으로 예상됩니다.

현저한 성장을 이루는 브라질

브라질은 가까운 미래에 남미 하이브리드 전기자동차(HEV) 배터리 시장에서 지배적인 선수로 등장할 준비가 되어 있습니다. 이 급성장의 주요 요인은 전동 이동성을 비롯한 다양한 분야에서 배터리 수요가 증가하고 있다는 것입니다. 또한 브라질의 급성장 EV 산업은 정부의 지원책과 기술적 진보에 의해 지원되고 있습니다.

최근 브라질은 정부의 장려책으로 EV의 보급이 급속히 진행되고 있습니다. 이 기세를 보듯 2023년 브라질의 EV 판매량은 약 5만 2,000대와 2022년 1만 8,500대에서 크게 급증했습니다. 이 EV 판매 대수의 급증은 향후 수년간 HEV 시장의 배터리를 강화할 것입니다.

브라질은 2024년 1월부터 수입되는 100% 전기자동차(EV)에 10%의 과세를 하고, 7월에는 18%, 2026년 7월에는 35%로 끌어올릴 예정입니다. 이에 따라 중국의 자동차 제조업체 몇사가 현지 투자를 활발하게 하고 있습니다. 특히 BYD는 2024년 후반부터 2025년 전반의 생산을 목표로 제조 복합단지를 설립하고 있으며, Great Wall Motor 공장은 2024년 조업을 시작할 예정입니다. 이러한 움직임은 브라질의 국내 EV 제조, 나아가서는 HEV용 배터리 수요를 강화하는 자세입니다.

세계 동향을 반영하여 브라질은 이산화탄소 배출을 억제하고 화석 연료에 대한 의존도를 낮추는 데 적극적으로 노력하고 있습니다. 이 전기 이동성으로의 전환을 촉진하기 위해 정부는 다양한 보조금과 인센티브를 전개하고 있습니다. 2023년 후반에 시작된 '그린 모빌리티 혁신 프로그램'은 저배출 가스 교통 기술을 개척하는 기업에 대해 2024년부터 2028년까지 190억 BRA를 넘는 세제 우대 조치를 제공하는 것으로 헌신을 보이고 있습니다. 이러한 노력은 HEV를 포함한 EV를 추진하고 HEV 배터리 시장을 활성화합니다.

브라질 배터리 원료의 진보는 HEV 배터리 공급 체인을 강화합니다. 예를 들어, 2024년 5월, 저명한 리튬 공급업체인 AMG Critical Materials가 브라질에서 채굴 사업 확대 계획을 발표했습니다. 이 회사의 리튬 정광 공장은 현재 연 생산량 9만 톤이지만, 2024년 4분기까지 연 생산량 13만 톤의 전체 생산 능력을 달성할 예정입니다.

또 다른 중요한 움직임으로 현지 광산 사업체인 Sigma Lithium은 국가개발은행의 지원을 받아 2024년 2월에 9,940만 달러의 투자를 선언했습니다. 미나스 제라이스에 위치한 Sigma의 두 번째 공장은 연간 생산량을 거의 두 배의 51만 톤으로 만드는 것을 목표로 하고 있습니다. 이러한 개발은 브라질의 리튬 이온 배터리 공급망을 강화할 것입니다.

이러한 역학을 고려하면, 브라질의 HEV용 배터리 시장은 향후 몇 년동안 크게 성장할 수 있습니다.

남미 하이브리드 전기자동차 배터리 산업 개요

남미의 하이브리드 전기자동차 배터리 시장은 반고착화되고 있습니다. 이 시장의 주요 기업(순부동)에는 Panasonic Holdings Corporation, Clarios(구 Johnson Controls International PLC), VARTA AG, Contemporary Amperex Technology Co.Limited, BYD Company Ltd. 등이 있습니다.

기타 혜택:

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

소개

2029년까지 시장 규모 및 수요 예측(단위: 달러)

최근 동향과 개발

정부의 규제와 정책

시장 역학

성장 촉진요인

유리한 정부 정책

전기자동차의 보급 확대

억제요인

원재료의 수급 미스매치

공급망 분석

업계의 매력도 - Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협 제품 및 서비스

경쟁 기업간 경쟁 관계

투자 분석

제5장 시장 세분화

전지 유형별

리튬 이온 배터리

납축전지

나트륨 이온 전지

기타

차량 유형별

승용차

상용차

지역별

브라질

콜롬비아

아르헨티나

기타 남미

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 프로파일

BYD Company Ltd

Contemporary Amperex Technology Co. Limited

Clarios(Formerly Johnson Controls International PLC)

LG Energy Solutions Ltd

VARTA AG

Panasonic Holdings Corporation

Duracell Inc.

기타 유명 기업 일람

시장 랭킹/점유율 분석

제7장 시장 기회와 앞으로의 동향

전기자동차에 고체 전지 채용

JHS

영문 목차

영문목차

The South America Hybrid Electric Vehicle Battery Market size is estimated at USD 124.42 million in 2025, and is expected to reach USD 230.36 million by 2030, at a CAGR of 13.11% during the forecast period (2025-2030).

Key Highlights

Over the medium term, the growing adoption of electric vehicles due to various supportive government schemes is expected to drive the demand for the South American hybrid electric vehicle battery market during the forecast period.

On the other hand, the demand-supply mismatch of raw materials is expected to hinder the market's growth during the forecast period.

Nevertheless, the adoption of solid-state batteries for electric vehicles and automaker-battery manufacturer collaborations are expected to create vast opportunities for the South American hybrid electric battery market in the future.

Brazil is poised for substantial growth, driven by government initiatives aimed at increasing the number of electric vehicles to curb emissions.

South America Hybrid Electric Vehicle Battery Market Trends

Lithium-ion Batteries to Witness Significant Growth

During the forecast period, lithium-ion batteries are poised to dominate the South American hybrid electric vehicle battery market. Their rising popularity, outpacing other battery types, can be attributed to a favorable capacity-to-weight ratio, superior performance (including extended life and minimal maintenance), an impressive shelf life, and a notable decrease in price.

When compared to traditional lead-acid batteries, lithium-ion (Li-ion) batteries showcase distinct technical advantages. Li-ion batteries typically offer over 5,000 cycles, a stark contrast to the 400-500 cycles of lead-acid counterparts. Moreover, Li-ion batteries demand less frequent maintenance and replacement. They also maintain consistent voltage throughout their discharge cycle, ensuring prolonged efficiency for electrical components.

In recent years, major industry players have ramped up investments, focusing on economies of scale and R&D to boost lithium-ion battery performance. This surge in competition has led to a notable drop in lithium-ion battery prices. Due to technological advancements, manufacturing optimizations, and falling raw material costs, the average price of lithium-ion batteries plummeted from USD 780/kWh in 2013 to USD 139/kWh in 2023. Projections suggest a further dip to approximately USD 113/kWh by 2025 and USD 80/kWh by 2030. Such declining trends in battery costs are likely to make it a lucrative choice among all batteries in the electric vehicle (EV) industry, including hybrid EVs.

While the lithium-ion battery manufacturing industry in South America is still in its nascent stages, the continent's rich reserves of essential raw materials and the surging demand from diverse end-users signal a rapid market expansion.

For instance, South America boasts vast lithium reserves, a cornerstone for lithium-ion batteries. The region, often dubbed the Lithium Triangle, encompasses Argentina, Bolivia, and Chile, collectively housing over half of the globe's known lithium reserves. Chile stands out as the primary producer, thanks to its extensive lithium-rich brine deposits in the Atacama Desert. Bolivia, with its massive lithium reserves in Salar de Uyuni, faces extraction challenges, while Argentina's Puna region salt flats also play a significant role. Together, these nations are integral to the global lithium-ion battery production supply chain.

According to the US Geological Survey, in 2023, lithium production figures were notable: Chile produced around 44,000 metric tons, Argentina contributed 9,600 metric tons, and Brazil added 4,900 metric tons. This combined output underscores South America's pivotal role in the global lithium landscape.

South American countries are intensifying efforts to deepen their involvement in the electric vehicle supply chain. By capitalizing on their mineral wealth, boosting processing capacities, and eyeing vehicle manufacturing, nations like Argentina, Chile, Bolivia, and Brazil are strategizing to convert more mined lithium into battery chemicals and eventually into batteries and EVs. However, these collaborative efforts don't extend to production or pricing coordination.

In April 2023, BYD Co Ltd, China's leading electric vehicle manufacturer, announced plans for a USD 290 million lithium cathode factory in Chile's Antofagasta region, as reported by Chile's economic development agency, CORFO. Such investments are expected to proliferate in the coming years.

In mid-2023, the Argentinean government revealed plans for its inaugural lithium-ion battery plant. This facility will utilize lithium carbonate sourced and processed locally by US mining giant Livent Corporation. Constructed by YPF Tecnologia (Y-TEC), a subsidiary of the state-owned YPF, the plant signifies Argentina's move to add value to its rich lithium reserves. With a USD 7 million investment, the facility aims for an annual production capacity of 13MWh, translating to 1,000 stationary energy storage batteries. Additionally, it seeks to foster technology transfer with local firms eyeing lithium-ion battery production.

Given their lightweight nature, rapid charging capabilities, extended charging cycles, decreasing costs, and the region's abundant lithium reserves, lithium-ion batteries are set for rapid growth in the coming years.

Brazil to Witness Significant Growth

Brazil is poised to emerge as a dominant player in the South American hybrid electric vehicle (HEV) battery market in the near future. This surge is primarily fueled by the escalating demand for batteries across diverse sectors, notably electric mobility. Furthermore, the country's burgeoning EV industry is bolstered by supportive government initiatives and technological strides.

Recently, Brazil has seen a swift uptick in EV adoption, thanks to government-backed incentives. Illustrating this momentum, Brazil's EV car sales soared to approximately 52,000 units in 2023, a substantial leap from 18,500 units in 2022. This surge in EV sales is set to bolster batteries for the HEV market in the years ahead.

Starting in January 2024, Brazil imposed a 10% tax on imported 100% electric vehicles (EVs), with plans to escalate this to 18% in July and a steep 35% by July 2026. In response, several Chinese automakers are ramping up local investments. Notably, BYD is establishing a manufacturing complex, eyeing production by late 2024 or early 2025, while Great Wall Motor's plant is set to commence operations in 2024. Such moves are poised to bolster Brazil's domestic EV manufacturing and, consequently, the demand for HEV batteries.

Echoing a global trend, Brazil is actively working to curb carbon emissions and lessen its fossil fuel reliance. To facilitate this shift towards electric mobility, the government has rolled out various subsidies and incentives. A testament to this commitment is the Green Mobility and Innovation Programme launched in late 2023, offering over BRA 19 billion in tax incentives from 2024 to 2028 for companies pioneering low-emission transport technologies. Such endeavors are set to propel the EV landscape, including HEVs, thereby invigorating the HEV battery market.

Brazil's advancements in battery raw materials are poised to fortify its HEV battery supply chain. For instance, in May 2024, AMG Critical Materials, a prominent lithium supplier, unveiled plans to expand its mining operations in Brazil. Their lithium concentrate plant, currently ramping up from 90,000 mt/year, is on track to hit a full capacity of 130,000 mt/year by Q4 2024.

In another significant move, Sigma Lithium, a local mining entity, declared a USD 99.4 million investment in February 2024, with backing from the National Development Bank. Sigma's second plant in Minas Gerais aims to nearly double its output to 510,000 metric tons annually. Such developments are set to bolster Brazil's lithium-ion battery supply chain.

Given these dynamics, Brazil's HEV battery market is on the brink of substantial growth in the forthcoming years.

South America Hybrid Electric Vehicle Battery Industry Overview

The South America hybrid electric vehicle battery market is semi-consolidated. Some of the key players in the market (not in any particular order) include Panasonic Holdings Corporation, Clarios (Formerly Johnson Controls International PLC), VARTA AG, Contemporary Amperex Technology Co. Limited, and BYD Company Ltd.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Favourable Government Policies

4.5.1.2 Growing Adoption of Electric Vehicles

4.5.2 Restraints

4.5.2.1 Demand-Supply Mismatch of Raw Materials

4.6 Supply Chain Analysis

4.7 Industry Attractiveness - Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

4.8 Investment Analysis

5 MARKET SEGMENTATION

5.1 Battery Type

5.1.1 Lithium-ion Battery

5.1.2 Lead-Acid Battery

5.1.3 Sodium-ion Battery

5.1.4 Others

5.2 Vehicle Type

5.2.1 Passenger Cars

5.2.2 Commercial Vehicles

5.3 Geography

5.3.1 Brazil

5.3.2 Colombia

5.3.3 Argentina

5.3.4 Rest of South America

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 BYD Company Ltd

6.3.2 Contemporary Amperex Technology Co. Limited

6.3.3 Clarios (Formerly Johnson Controls International PLC)

6.3.4 LG Energy Solutions Ltd

6.3.5 VARTA AG

6.3.6 Panasonic Holdings Corporation

6.3.7 Duracell Inc.

6.4 List of Other Prominent Companies

6.5 Market Ranking/ Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Adoption of Solid-State Batteries for Electric Vehicles