하이브리드 전기자동차 배터리 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Hybrid Electric Vehicle Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1636178

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

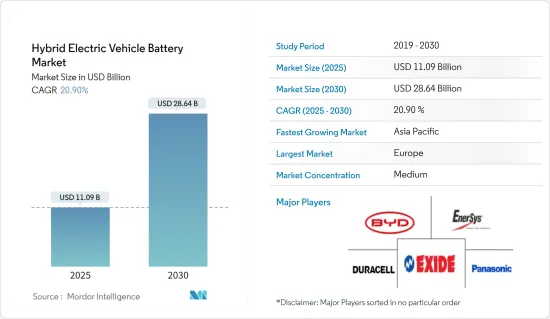

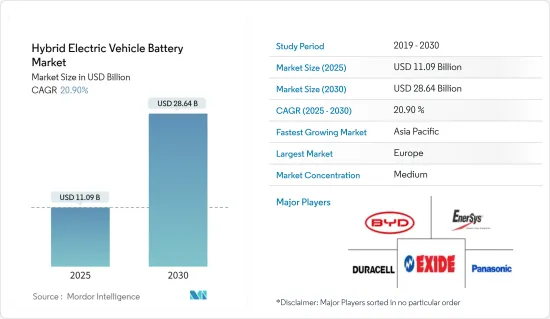

하이브리드 전기자동차 배터리 시장 규모는 2025년 110억 9,000만 달러로 추정되며, 예측 기간(2025-2030년) 동안 20.9%의 CAGR로 2030년에는 286억 4,000만 달러에 달할 것으로 예상됩니다.

주요 하이라이트

중기적으로는 전기자동차(EV) 보급대수 증가와 리튬이온 배터리 가격 하락이 예측기간 동안 하이브리드 전기자동차 배터리 수요를 견인할 것으로 예상됩니다.

한편, 원료 매장량 부족은 하이브리드 전기자동차 배터리 시장의 성장을 크게 억제할 수 있습니다.

에너지 밀도 향상, 충전 시간 단축, 안전성 향상, 수명 연장 등 배터리 재료의 기술 발전은 가까운 미래에 하이브리드 전기자동차 배터리 시장 진입 기업들에게 큰 기회를 제공할 것으로 예상됩니다.

아시아태평양은 전기자동차의 채택이 증가함에 따라 예측 기간 동안 세계 하이브리드 전기자동차 배터리 시장에서 가장 빠르게 성장하는 지역입니다.

하이브리드 전기자동차 배터리 시장 동향

리튬이온 배터리 타입이 시장을 독점

세계 리튬 이온 전기자동차 배터리 시장은 기회와 도전의 매력적인 풍경을 제시하고 있습니다. 리튬 이온 이차전지는 유리한 용량 대 중량 비율로 인해 다른 배터리 기술보다 더 많은 인기를 얻고 있습니다. 리튬 이온 이차전지의 보급을 촉진하는 다른 요인으로는 향상된 성능(긴 수명, 낮은 유지보수), 향상된 저장성, 가격 하락 등이 있습니다.

리튬이온 배터리의 가격은 일반적으로 다른 배터리보다 높습니다. 그러나 시장 전반의 주요 기업들이 규모의 경제를 달성하기 위한 투자 및 성능 향상을 위한 연구개발 활동을 진행하면서 경쟁이 치열해졌고, 그 결과 리튬이온 배터리의 가격이 하락하고 있습니다.

전기자동차(EV)와 배터리 에너지 저장 시스템(BESS)의 평균 배터리 팩 가격이 상승함에 따라 배터리 가격은 2023년 139달러/kWh로 13% 이상 하락할 것으로 예상됩니다. 기술 혁신과 제조 강화로 인해 배터리 팩 가격은 더욱 하락하여 2025년에는 113달러/kWh, 2030년에는 80달러/kWh까지 하락할 것으로 예상됩니다.

또한, 환경 문제에 대한 관심이 높아지면서 세계 각국 정부는 전기자동차를 대대적으로 추진하고 있습니다. 정부는 순 탄소 배출 제로 목표에 큰 관심을 기울이고 있습니다. 리튬은 전기자동차에 저장 용량을 제공하는 배터리에 필수적인 요소입니다. 세계 주요 기업들은 리튬이온 배터리에 대한 수요 증가를 충족시키기 위해 리튬을 추출하고 있습니다.

예를 들어, 2023년 11월 엑손모빌(Exxon Mobil Corporation)은 중요한 리튬 광맥이 있는 것으로 알려진 아칸소주 남서부 지역에서 북미 리튬 생산의 첫 번째 단계를 시작할 가능성이 높다고 발표했습니다. 첫 생산은 2027년을 목표로 하고 있습니다. 이러한 프로젝트는 리튬 생산을 가속화하여 예측 기간 동안 리튬이온 배터리의 수요 증가를 충족시킬 가능성이 높습니다.

또한, 세계 각국 정부는 전기자동차 활성화를 위해 다양한 정책과 인센티브를 시행하고 있습니다. 이러한 정책은 리튬이온 배터리 수요에 긍정적인 영향을 미치고 있습니다. 각국 정부는 지역 전체에서 전기자동차 보급을 촉진하기 위해 여러 가지 이니셔티브를 발표했습니다.

예를 들어, 영국은 2030년까지 신차 판매량의 80%, 밴 판매량의 70%를 무공해 차량으로 의무화하고, 2035년까지 100%에 도달하도록 ZEV 의무화를 제정했습니다. 또한, 2030년까지 휘발유차와 디젤차, 밴의 신차 판매를 금지하고, 2035년까지 모든 신차와 밴이 테일파이프에서 배출가스 제로가 되도록 의무화할 것으로 보입니다. 이러한 노력은 향후 몇 년 동안 국가 전체에서 전기자동차 생산과 수요를 가속화하여 예측 기간 동안 리튬이온 배터리에 대한 수요를 증가시킬 가능성이 높습니다.

이러한 프로젝트와 투자는 예측 기간 동안 지역 전체의 전기자동차 생산량을 증가시켜 리튬이온 배터리에 대한 수요를 증가시킬 가능성이 높습니다.

아시아태평양이 괄목할 만한 성장을 이뤄

아시아태평양의 하이브리드 전기자동차(HEV) 배터리 시장은 환경 인식의 증가, 정부 지원 정책, 기술 발전으로 인해 빠르게 성장하고 있는 시장입니다.

중국, 일본, 한국, 인도 등 아시아태평양은 HEV 배터리 시장에서 괄목할 만한 성장세를 보이고 있습니다. 그 배경에는 친환경 자동차에 대한 수요 증가와 이산화탄소 배출량 감축을 위한 정부의 강력한 지원책이 있습니다.

하이브리드 전기자동차(HEV)에 대한 수요는 이 지역 전체에서 크게 증가하고 있습니다. 이 지역에서 중국은 HEV의 주요 생산국입니다. 예를 들어, 국제에너지기구(IEA)에 따르면 2023년 플러그인 하이브리드 전기자동차의 판매량은 270만 대에 달할 것으로 예상되며, 일본이 5만 2,000대를 판매할 것으로 예상됩니다. 아시아태평양 전역에 수많은 전기자동차 생산 공장이 설립되고 하이브리드 전기자동차(HEV)용 배터리에 대한 수요가 증가함에 따라 향후 몇 년 동안 전기자동차 판매는 증가할 것입니다.

이 지역 정부는 하이브리드 및 전기자동차의 도입을 촉진하기 위해 다양한 정책과 인센티브를 시행하고 있습니다. 여기에는 보조금, 세제 혜택, 엄격한 배기가스 규제 등이 포함되며, 제조업체는 더 많은 HEV를 생산하도록 장려하고 있습니다.

호주 정부는 전기자동차 구매를 보다 저렴하게 구매할 수 있도록 세제 혜택과 리베이트를 도입하고 있습니다. 여기에는 전기자동차 수입 관세 인하, 인프라 개발에 대한 보조금 제공 등이 포함됩니다. 일부 주에서는 자체적인 EV 인센티브를 제공하고 있습니다. 예를 들어, 뉴사우스웨일즈 주에서는 6만 8,750달러 이하로 판매되는 첫 2만 5,000대의 전기자동차에 대해 3,000달러의 리베이트를 제공하고 있으며, 2030년까지 모든 승용차를 전기자동차로 전환하는 것을 목표로 하고 있습니다. 빅토리아주는 6만 8,740달러 이하의 전기자동차 판매량 2만 대에 대해 3,000달러의 보조금을 지급하고 인지세도 면제해줍니다.

또한, 인도 정부는 2030년 이후 신차 판매를 완전 전기화하겠다는 야심찬 목표를 세웠습니다. 인도 정부는 2030년까지 자가용의 30%, 상용차의 70%, 이륜차 및 삼륜차의 80%를 전기자동차가 차지한다는 목표를 세웠습니다. 또한 정부는 1kWh당 1만 인도 루피(120달러)에서 1만 5,000 인도 루피(180달러)의 보조금 혜택도 제공하고 있습니다. 이러한 노력으로 향후 몇 년 동안 전국적으로 전기자동차 생산과 수요가 가속화될 것이며, 예측 기간 동안 HEV용 배터리에 대한 수요가 증가할 가능성이 높습니다.

이러한 프로젝트 개발은 EV의 배터리 에너지 저장 시스템을 위한 HEV 배터리 솔루션의 실현 가능성과 중요성을 보여주며, 향후 몇 년 동안 국가 전체 HEV 배터리 수요를 증가시킬 가능성이 높습니다.

하이브리드 전기자동차 배터리 산업 개요

하이브리드 전기자동차 배터리 시장은 반분할되어 있습니다. 주요 진출 기업(순서는 무관)은 BYD Company Ltd., Duracell Inc., Exide Industries Ltd., EnerSys, Panasonic Holdings Corporation 등이 있습니다.

기타 혜택

엑셀 형식의 시장 예측(ME) 시트

3개월간 애널리스트 지원

목차

제1장 소개

조사 범위

시장 정의

조사 가정

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

소개

2029년까지 시장 규모와 수요 예측(단위 : 달러)

최근 동향과 개발

정부 정책 및 규정

시장 역학

성장 촉진요인

전기자동차(EV) 생산 증가

리튬이온 배터리 가격 하락

성장 억제요인

원료 매장량 부족

공급망 분석

산업의 매력 - Porter's Five Forces 분석

공급 기업의 교섭력

소비자의 협상력

신규 참여업체의 위협

대체품의 위협 제품·서비스

경쟁 기업 간의 경쟁 관계

투자 분석

제5장 시장 세분화

배터리 유형

리튬이온 배터리

납축배터리

나트륨 이온 배터리

기타

2029년까지 시장 규모·수요 예측(지역별)

북미

미국

캐나다

기타 북미

유럽

독일

프랑스

영국

이탈리아

스페인

북유럽

러시아

터키

기타 유럽

아시아태평양

중국

인도

호주

일본

한국

말레이시아

태국

인도네시아

베트남

기타 아시아태평양

중동 및 아프리카

사우디아라비아

아랍에미리트

나이지리아

이집트

카타르

남아프리카공화국

기타 중동 및 아프리카

남미

브라질

아르헨티나

콜롬비아

기타 남미

제6장 경쟁 구도

M&A, 합작투자, 제휴, 협정

주요 기업의 전략과 SWOT 분석

기업 개요

BYD Company Ltd

Duracell Inc.

EnerSys

Panasonic Holdings Corporation

Energizer

Exide Industries Ltd

Saft Groupe SA

AMTE Power

Amperex Technology Co. Limited

Gotion High tech Co Ltd

기타 저명한 기업 리스트

시장 순위/점유율 분석

제7장 시장 기회와 향후 동향

배터리 재료 기술 진보

ksm

영문 목차

영문목차

The Hybrid Electric Vehicle Battery Market size is estimated at USD 11.09 billion in 2025, and is expected to reach USD 28.64 billion by 2030, at a CAGR of 20.9% during the forecast period (2025-2030).

Key Highlights

Over the medium term, rising adoption of electric vehicles (EV) and declining lithium-ion battery prices are expected to drive the demand for hybrid electric vehicle batteries during the forecast period.

On the other hand, the lack of raw material reserves can significantly restrain the growth of the hybrid electric vehicle battery market.

Nevertheless, technological advancements in battery materials like higher energy density, faster charging times, improved safety, and longer lifespan are expected to create significant opportunities for hybrid electric vehicle battery market players in the near future.

Asia Pacific is the fastest-growing region in the global hybrid electric vehicle battery market during the forecast period due to the rising adoption of electric vehicle.

Hybrid Electric Vehicle Battery Market Trends

Lithium-Ion Battery Type Dominate the Market

The lithium-ion electric vehicle battery market worldwide presents a fascinating landscape of opportunities and challenges. Due to their favorable capacity-to-weight ratio, lithium-ion rechargeable batteries are gaining more popularity than other battery technologies. Other factors contributing to boosting their adoption include better performance (long life and low maintenance), better shelf life, and decreasing price.

The price of lithium-ion batteries is usually higher than that of other batteries. However, major players across the market have been investing to gain economies of scale and R&D activities to enhance their performance, increasing the competition and, in turn, resulting in declining prices of lithium-ion batteries.

Owing to the increasing average battery pack prices of electric vehicles (EV) and battery energy storage systems (BESS), the battery prices declined in 2023 to USD 139 /kWh, a decrease of over 13%. The trajectory of technological innovation and manufacturing enhancements is anticipated to decrease the battery pack prices further, projecting the price to reach USD 113/kWh in 2025 and USD 80/kWh in 2030.

Furthermore, governments all over the world are significantly promoting electric vehicles due to rising environmental concerns. The government is significantly focused on net zero carbon emission targets. Lithium is a vital element in batteries that provides the storage capacity for EVs. The leading companies around the globe are extracting lithium to fulfill the rising demand for lithium-ion batteries.

For instance, in November 2023, Exxon Mobil Corporation announced that it was likely to start the first phase of North American lithium production in southwest Arkansas, an area known to hold significant lithium deposits. The first production is targeted for 2027. Such projects are likely to accelerate the production of lithium and fulfill the rising demand for lithium-ion batteries during the forecast period.

Additionally, the government worldwide has implemented various policies and incentives to promote electric vehicles. These policies have positively impacted the demand for lithium-ion batteries. The government announced numerous initiatives to promote EVs across the region.

For instance, the United Kingdom has established a ZEV mandate that requires 80% of new cars and 70% of new vans sold to be zero-emission by 2030, reaching 100% by 2035. Furthermore, the sale of new petrol and diesel cars and vans is likely to be banned by 2030, with all new cars and vans required to be zero-emission at the tailpipe by 2035. Such initiatives are likely to accelerate the production and demand of EVs across the country in the coming years and are likely to raise the demand for lithium-ion batteries in the forecast period.

Such type of projects and investments likely to increase the EV production across the region and rising demand of lithium-ion battery during the forecast period.

Asia Pacific to Witness Significant Growth

The Asia Pacific hybrid electric vehicle (HEV) battery market is a rapidly growing sector driven by increasing environmental awareness, supportive government policies, and technological advancements.

The Asia Pacific region, including countries like China, Japan, South Korea, and India, is experiencing significant growth in the HEV battery market. This is due to rising demand for eco-friendly vehicles and a robust governmental push towards reducing carbon emissions.

The demand for hybrid electric vehicles (HEV) is rising significantly across the region. China is the leading producer of HEV in the region. For instance, according to the International Energy Agency (IEA), in 2023, the sale of Plug-in Hybrid Electric Vehicles was 2.7 million units, followed by Japan with 52 thousand units. EV Sales are rising in the coming years as numerous EV production plants are set up across the Asian Pacific region, and the demand for hybrid electric vehicle (HEV) batteries is increasing.

Governments in the region are implementing various policies and incentives to promote the adoption of hybrid and electric vehicles. These include subsidies, tax benefits, and stringent emission norms which encourage manufacturers to produce more HEVs.

The Australian government has introduced tax incentives and rebates to make EVs more affordable. This includes reducing the import duty on EVs and offering grants for infrastructure development. Several states have their own EV incentives. For instance, New South Wales offers a USD 3,000 rebate for the first 25,000 EVs sold under USD 68,750 and aims for its entire passenger fleet to be electric by 2030. Victoria provides a USD 3,000 subsidy for the first 20,000 EVs sold under USD 68,740, along with stamp duty exemptions.

Morover, The Indian government set an ambitious target for new vehicle sales after 2030 to be fully electric. The Indian government set a target of EV sales accounting for 30% of private cars, 70% of commercial vehicles, and 80% of two and three wheelers by 2030. Further, the government has also offered subsidy incentives from INR 10,000 per kWh (USD 120) to INR 15,000 per kWh (USD 180). Such initiatives are likely to accelerate the production and demand of EVs across the country in the coming years and are likely to raise the demand for HEV batteries during the forecast period.

Such project developments showcase the feasibility and importance of HEV battery solutions for battery energy storage systems in EVs and are likely to raise the demand for HEV batteries across the country in the coming year.

Hybrid Electric Vehicle Battery Industry Overview

The hybrid electric vehicle battery market is semi-fragmented. Some key players (not in particular order) are BYD Company Ltd, Duracell Inc., Exide Industries Ltd, EnerSys, and Panasonic Holdings Corporation, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 The Increasing Electric Vehicle (EV) Production

4.5.1.2 Declining Lithium-ion Battery Prices

4.5.2 Restraints

4.5.2.1 Lack of Raw Material Reserves

4.6 Supply Chain Analysis

4.7 Industry Attractiveness - Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

4.8 Investment Analysis

5 MARKET SEGMENTATION

5.1 Battery Type

5.1.1 Lithium-ion Battery

5.1.2 Lead-Acid Battery

5.1.3 Sodium-ion Battery

5.1.4 Others

5.2 Geography [Market Size and Demand Forecast till 2029 (for regions only)]

5.2.1 North America

5.2.1.1 United States

5.2.1.2 Canada

5.2.1.3 Rest of North America

5.2.2 Europe

5.2.2.1 Germany

5.2.2.2 France

5.2.2.3 United Kingdom

5.2.2.4 Italy

5.2.2.5 Spain

5.2.2.6 NORDIC

5.2.2.7 Russia

5.2.2.8 Turkey

5.2.2.9 Rest of Europe

5.2.3 Asia-Pacific

5.2.3.1 China

5.2.3.2 India

5.2.3.3 Australia

5.2.3.4 Japan

5.2.3.5 South Korea

5.2.3.6 Malaysia

5.2.3.7 Thailand

5.2.3.8 Indonesia

5.2.3.9 Vietnam

5.2.3.10 Rest of Asia-Pacific

5.2.4 Middle East and Africa

5.2.4.1 Saudi Arabia

5.2.4.2 United Arab Emirates

5.2.4.3 Nigeria

5.2.4.4 Egypt

5.2.4.5 Qatar

5.2.4.6 South Africa

5.2.4.7 Rest of Middle East and Africa

5.2.5 South America

5.2.5.1 Brazil

5.2.5.2 Argentina

5.2.5.3 Colombia

5.2.5.4 Rest of South America

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted & SWOT Analysis for Leading Players

6.3 Company Profiles

6.3.1 BYD Company Ltd

6.3.2 Duracell Inc.

6.3.3 EnerSys

6.3.4 Panasonic Holdings Corporation

6.3.5 Energizer

6.3.6 Exide Industries Ltd

6.3.7 Saft Groupe SA

6.3.8 AMTE Power

6.3.9 Amperex Technology Co. Limited

6.3.10 Gotion High tech Co Ltd

6.4 List of Other Prominent Companies

6.5 Market Ranking/ Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Technological Advancements in Battery Materials