챗봇 시장은 2025년 93억 달러에서 2026년에는 114억 5,000만 달러로 성장하고 2026년에서 2031년에 걸쳐 CAGR 23.15%를 나타내 2031년까지 324억 5,000만 달러에 달할 것으로 예측되고 있습니다.

이러한 지속적인 확장은 메시징 앱의 보급, 대규모 언어 모델의 성능의 급속한 진보, 전통적인 컨택 센터 운영에 대한 비용 압력 증가로 추진되고 있습니다. 고객 경험의 리더은 현재 음성, 텍스트, 멀티모달 인터페이스를 통해 인간과 같은 대화를 유지하면서 서비스 비용을 절감하는 자율적이고 상시 가동 채널을 우선하고 있습니다. 플랫폼 공급업체는 이에 대응하고 개발주기를 단축하고 도입을 민주화하는 검색 강화 생성 기술, 다국어 모델, 도메인 특화형 에이전트를 포함하고 있습니다. 기업이 측정 가능한 ROI를 추구하는 가운데, 벤더는 성과 연동형 가격 설정, 사전 활성 컴플라이언스 툴, 규제 산업의 가치 실현 기간을 단축하는 수직 통합 지식 팩을 중시하고 있습니다. 경쟁의 격화가 진행되고 있으며, 세계의 하이퍼스케일러, 독립 전문가, CX 아웃소서가 인수, 파트너십, 전략적 자본 주입을 통해 능력을 통합하고 있습니다.

WhatsApp는 현재 30억 명의 사용자에게 서비스를 제공하고 매일 1억 7,500만 개의 비즈니스 대화를 지원하며, 챗봇 시장에 거대한 기성 유통 채널을 제공합니다. 기업은 7억 6,400만 개의 WhatsApp 비즈니스 계정을 개설하고 있으며, 메일의 20%에 대해 98%의 개봉율을 달성하여 획득 비용을 극적으로 절감하고 있습니다. 광범위한 메시징 에코시스템에는 전 세계 2억 개 이상의 기업이 참여하고 있으며 소매, 은행, 의료 분야에서 봇의 투자 대 효과를 높이는 강력한 네트워크 효과를 창출하고 있습니다. 기업은 리치 미디어 템플릿을 활용하여 앱 다운로드 없이 마케팅 프롬프트에서 전체 퍼널 거래로 상호작용을 마이그레이션하고 있습니다. 사용자의 숙련도가 높아짐에 따라 메시지 기반 저니는 서비스 문의, 주문 추적, 채널 내 결제의 기본 인터페이스가 되고 있습니다.

GPT-4.5와 향후 GPT-5 모델의 출현으로 챗봇은 인간에게 가까운 유창하고 복잡한 다중 턴 상호작용을 처리할 수 있게 되었습니다. 모건 스탠리와 같은 기업은 내부 지식 검색에 GPT-4를 도입하여 어드바이저의 검색 시간 단축과 컴플라이언스 신뢰성 향상을 실현하고 있습니다. 벤더는 검색 확장 생성 기능을 내장하여 봇이 실시간 데이터를 얻으면서 대화의 흐름을 유지할 수 있도록 하여 기존의 지식 단절이라는 과제를 해결하고 있습니다. Yellow.ai는 연간 160억 건이 넘는 대화를 처리하는 다중 LLM 파이프라인을 구축하고 쿼리별로 전문 모델을 선택하여 비용과 정확성을 최적화합니다. 이러한 혁신은 교육 데이터 요구를 줄이고 대규모 라벨링된 데이터 세트가 없는 중소기업에서도 고급 대화형 AI를 사용할 수 있게 되었습니다.

수십 년이 넘는 시스템을 보유한 기업에서는 챗봇을 메인프레임, CRM, ERP에 연결할 때 몇 달에 걸쳐 일정 지연이 발생합니다. 47%의 기업이 데이터 파이프라인을 관리하기 위해 생성형 AI를 자체 개발하고 있으며 통합에 대한 우려를 반영합니다. 미들웨어 오케스트레이션, 실시간 동기화 및 엄격한 보안 심사는 특히 데이터 단편화가 심각한 은행 및 통신 업계에서 프로젝트 예산을 부풀리고 전개 배포를 지연시킵니다. 그 결과 신규 진입의 디지털 네이티브 기업이 시장 출시까지의 시간적 우위성을 획득하고 기존 기업은 API의 근대화에 대한 투자를 강요받고 있습니다.

2025년 시점에서 플랫폼 소프트웨어 제공은 챗봇 시장의 64.12%를 차지하고 기반 인프라로서의 역할을 강조했습니다. 한편 서비스 분야는 2031년까지 연평균 복합 성장률(CAGR) 24.12%로 시장 전체를 웃도는 성장을 이루고 있습니다. 대화형 AI의 복잡성이 증가함에 따라 기업은 권고, 통합 및 최적화에 대한 전문 지식을 점점 더 추구하고 있습니다. Yellow.ai는 전략적 입안, 맞춤형 모델 조정 및 지속적인 거버넌스를 다루는 전체 수명주기 지원을 제공하며 서비스 수요를 이끌고 있습니다. 고객 기업의 경우 전문 파트너는 통합시 과제 해결과 컴플라이언스 확보를 실현하고 벤더의 노하우를 프리미엄 요금에 맞는 구체적인 비즈니스 성과로 전환합니다.

배포 컨설팅은 가동 시간 보장, 재교육 및 분기별 성능 검토를 정한 관리형 서비스 SLA와 함께 제공되는 것이 일반적입니다. 이러한 변화로 인해 수익 구성이 지속적인 서비스 계약으로 전환되어 공급업체의 현금 흐름을 안정화할 수 있습니다. AI 툴의 성숙에 따라 차별화 요인은 기반 기술보다 성과에 중점을 둔 참여로 이행하여 깊은 업계별 노하우와 견고한 파트너 에코시스템을 가진 프로바이더가 우위가 됩니다. 챗봇 시장에서는 플랫폼 통합이 지속되는 동시에, 성장하는 지갑 공유를 획득하는 서비스 계층의 성장이 예상됩니다.

2025년 시점에서 고객 지원은 챗봇 시장 점유율의 41.82%를 차지하며 높은 조회량과 입증된 투자 대 효과를 반영했습니다. 한편, 인사·채용 분야의 이용 사례는 2031년까지 연평균 복합 성장률(CAGR) 24.86%로 가장 급속한 성장을 보이고 있습니다. 봇이 후보자의 사전 스크리닝, 인터뷰 스케줄링, 정책 질문에 대한 답변을 제공함으로써 인사부문은 고부가가치 업무에 주력할 수 있습니다. 기업은 반복적인 문의의 90%가 자동화되어 채용까지의 시간이 단축되었다고 보고되어, 이는 측정 가능한 생산성 향상으로 이어지고 있습니다.

영업 및 마케팅 봇은 개인화된 지속적인 대화로 리드를 육성하고 IT 서비스 데스크 에이전트는 비밀번호 재설정 및 하드웨어 문제를 진단합니다. 신흥의 사내 지식 어시스턴트는 구조화 및 비구조화 컨텐츠를 집계하여 검색 사이클을 단축합니다. 이러한 기능의 다양화는 대화형 AI의 범용성을 뒷받침해 틈새 보조 도구가 아닌 핵심 자동화 기반으로서의 지위를 확고하게 하고 있습니다.

북미는 2025년 챗봇 시장 규모의 38.72%를 차지하며 LLM의 조기 도입과 높은 인건비가 자동화 투자 회수를 촉진했습니다. 미국 금융기관과 소매업체는 고급 음성 + 시각 에이전트를 도입하고 캐나다 기업은 내부 지식 검색에 GPT-4를 활용하고 있습니다. 성숙한 디지털 인프라와 활발한 벤처 자금이 지속적인 실험을 지원하고 니어 쇼어 서비스 거점을 통해 라틴아메리카에 파급하고 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 24.71%로 가장 빠른 성장을 보일 것으로 전망됩니다. 정부의 AI 투자 지원과 모바일 상거래의 보급이 배경에 있습니다. 중국은 AI 프로젝트에 21억 달러를 투입, 인도의 챗봇 시장은 연률 25%로 성장, 싱가포르는 AI 거버넌스의 실증 거점으로 자리매김하고 있습니다. 높은 스마트폰 보급률과 슈퍼 앱 에코시스템이 방대한 대화 트래픽을 만들어 은행·여행·공공 서비스 분야에서의 도입을 가속화하고 있습니다. 현지 벤더는 지역 방언에 맞는 다국어 봇을 개발하여 종합적인 디지털 액세스를 촉진하고 있습니다.

유럽에서는 EU AI법의 그림자 하에서 진전을 볼 수 있어 혁신과 엄격한 컴플라이언스의 균형을 이루고 있습니다. 독일, 프랑스, 영국에서는 제조, 의료 및 공공 행정에 챗봇이 통합되어 연간 컴플라이언스 예산이 총소유비용(TCO) 계산에 통합됩니다. 표준화된 거버넌스 프레임워크는 국경을 넘어서는 협력을 강화하고 사실상 세계 기준을 확립합니다. 신흥 지역인 남미, 중동, 아프리카에서는 클라우드 비용의 저하와 광대역의 확대에 의해 통신, 에너지, 운송 분야에서의 신규 도입이 촉진되고 있습니다.

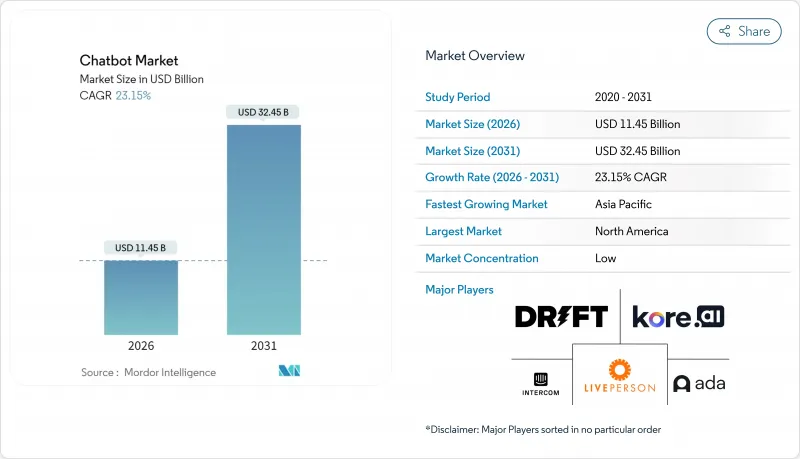

The Chatbot market is expected to grow from USD 9.30 billion in 2025 to USD 11.45 billion in 2026 and is forecast to reach USD 32.45 billion by 2031 at 23.15% CAGR over 2026-2031.

This sustained expansion is propelled by ubiquitous messaging-app reach, rapid advances in large-language-model performance, and mounting cost pressures on traditional contact-center operations. Customer experience leaders now prioritize autonomous, always-on channels that lower service costs while sustaining human-like interactions across voice, text, and multimodal interfaces. Platform vendors respond by embedding retrieval-augmented generation, multilingual models, and fine-tuned domain agents that reduce development cycles and democratize deployment. As enterprises seek measurable ROI, vendors emphasize outcome-linked pricing, proactive compliance tooling, and verticalized knowledge packs that accelerate time-to-value in regulated industries. Competitive intensity is rising as global hyperscalers, independent specialists, and CX outsourcers consolidate capabilities through acquisitions, partnerships, and strategic capital infusions.

WhatsApp now serves 3 billion users and supports 175 million daily business conversations, giving the Chatbot market an immense, ready-made distribution channel. Businesses have opened 764 million WhatsApp Business accounts that achieve 98% open rates versus 20% for email, dramatically lowering acquisition costs. The broader messaging ecosystem engages more than 200 million businesses worldwide, creating strong network effects that improve bot ROI across retail, banking, and healthcare. Firms leverage rich-media templates that shift interactions from marketing prompts to full-funnel transactions without requiring app downloads. As user familiarity rises, message-based journeys become the default interface for service queries, order tracking, and in-channel payments.

The launch of GPT-4.5 and expected GPT-5 models enabled chatbots to manage complex multi-turn dialogues with near-human fluency. Enterprises such as Morgan Stanley showcased GPT-4 for internal knowledge retrieval, reducing advisor search time and boosting compliance confidence. Vendors embed retrieval-augmented generation so bots pull real-time data yet maintain conversation flow, addressing historical knowledge-cutoff limits. Yellow.ai orchestrates multi-LLM pipelines over 16 billion annual conversations, selecting specialized models per query to optimize cost and accuracy. These innovations cut training-data demands and open advanced conversational AI to SMEs lacking large labeled datasets.

Enterprises with decades-old systems face month-long timeline overruns when wiring chatbots into mainframes, CRMs, and ERPs. Forty-seven percent of firms build generative AI in-house to control data pipelines, reflecting integration anxiety. Middleware orchestration, real-time synchronization, and stringent security vetting inflate project budgets and delay full rollout, especially in banking and telecom, where data fragmentation is acute. As a result, greenfield digital-native firms gain time-to-market advantage, pressing incumbents to invest in API modernization.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Platform and software offerings retained a 64.12% share of the Chatbot market in 2025, underscoring their role as foundational infrastructure. Services, however, outpace overall growth at a 24.12% CAGR through 2031. Enterprises increasingly seek advisory, integration, and optimization expertise as conversational AI complexity rises. Yellow.ai packages full-lifecycle support covering strategy, custom model tuning, and ongoing governance, driving services demand. For clients, expert partners mitigate integration pain points and ensure compliance, turning vendor know-how into tangible business outcomes that justify premium fees.

Implementation consulting is often bundled with managed-service SLAs that guarantee uptime, retraining, and quarterly performance reviews. This shift nudges revenue mix toward recurring service contracts, smoothing vendor cash flows. As AI tooling matures, differentiation hinges less on base technology and more on outcome-driven engagement, favoring providers with deep vertical playbooks and robust partner ecosystems. The Chatbot market expects continued platform consolidation alongside a flourishing services layer that captures expanding wallet share.

Customer support commanded 41.82% of the Chatbot market share in 2025, reflecting high ticket volumes and proven ROI. HR and recruiting use cases, however, register the quickest rise with a 24.86% CAGR through 2031. Bots prescreen candidates, schedule interviews, and answer policy questions, freeing HR teams for high-touch activities. Enterprises report 90% automation of repetitive inquiries and accelerated time-to-hire, translating into measurable productivity gains.

Sales and marketing bots nurture leads via personalized drip conversations, while IT service-desk agents reset passwords and diagnose hardware issues. Emerging internal knowledge assistants aggregate structured and unstructured content, cutting search cycles. This functional diversification underscores conversational AI's versatility and cements its status as a core automation pillar rather than a niche support add-on.

The Chatbot Market Report is Segmented by Component (Platform/Software and Services), Application (Customer Support, Sales and Marketing, and More), Deployment Mode (Cloud and On-Premise), Organization Size (Small and Medium Enterprises and Large Enterprises), End-User Industry (Retail and ECommerce, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America contributed 38.72% to the Chatbot market size in 2025, anchored by early LLM adoption and high labor costs that sharpen automation payback. U.S. financial institutions and retailers implement advanced voice-plus-vision agents, and Canadian enterprises tap GPT-4 for internal knowledge retrieval. Mature digital infrastructure and vibrant venture funding support continuous experimentation that spills over into Latin America through nearshore service hubs.

Asia-Pacific posts the fastest 24.71% CAGR through 2031 as governments back AI investments and mobile commerce proliferates. China poured USD 2.1 billion into AI projects, India's chatbot segment grows 25% annually, and Singapore positions itself as an AI governance testbed. High smartphone penetration and super-app ecosystems generate massive conversational traffic, accelerating adoption in banking, travel, and public services. Local vendors tailor multilingual bots to regional dialects, fostering inclusive digital access.

Europe advances under the shadow of the EU AI Act, balancing innovation with rigorous compliance. Germany, France, and the U.K. integrate chatbots into manufacturing, healthcare, and public administration, with annual compliance budgets absorbed into total cost of ownership calculations. Standardized governance frameworks enhance cross-border collaborations and set de-facto global norms. Emerging regions, South America, the Middle East, and Africa benefit from falling cloud costs and expanding broadband, unlocking greenfield deployments across telecom, energy, and transport.