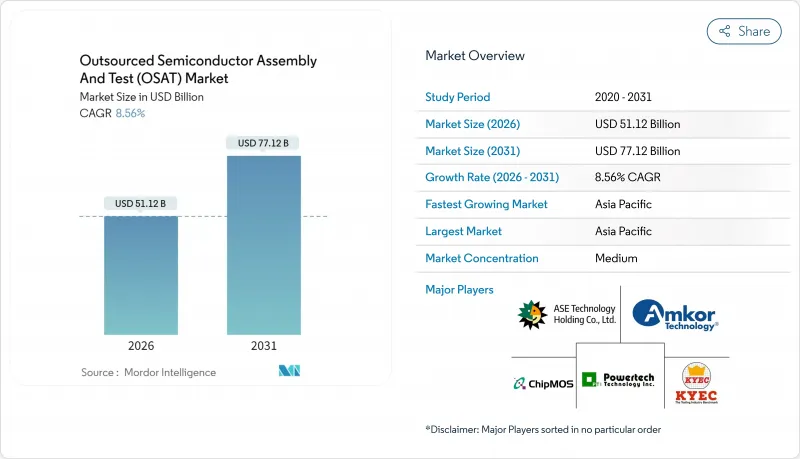

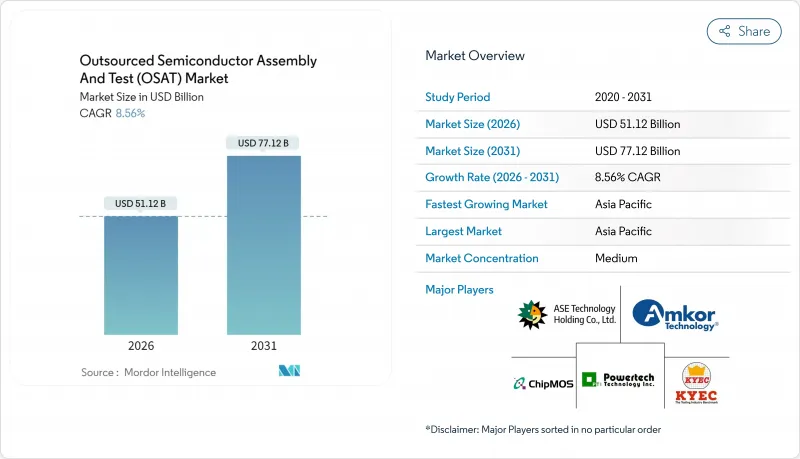

반도체 외주 조립 및 검사(OSAT) 시장은 2025년에 470억 9,000만 달러로 평가되었고, 2026년 511억 2,000만 달러에서 2031년까지 771억 2,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 8.56%로 예상됩니다.

인공지능, 고성능 컴퓨팅, 자동차 전동화의 지속적인 발전으로 첨단 패키징 기술과 안전성이 매우 중요한 검사 흐름에 대한 수요가 높아져 전문적인 백엔드 서비스 제공업체의 총 시장 규모가 확대되었습니다. 아시아태평양의 공급업체는 성숙한 생태계를 통해 가격 결정력을 유지했지만 북미 및 유럽에서 정책 주도의 생산 능력 확대가 세계 공급 배분 구조의 재편으로 이어졌습니다. 하이브리드 칩렛 아키텍처는 이기종 집적의 중요성을 높여 팬아웃 웨이퍼 레벨 및 2.5D/3D 플랫폼에 대한 전략적 투자를 촉진하고 있습니다. 한편, 무역규제의 강화와 지속가능성에 대한 요구로 고객은 작업부하의 일부를 단위처리량당 에너지 사용량이 낮음을 입증할 수 있는 지리적으로 분산된 거점으로 이전하게 되었습니다. 파운더리 생산 능력에 대한 압박 상태가 계속되는 가운데, 팹라이트형 반도체 기업은 백엔드 공정의 외부 위탁을 지속하여, 다음 계획 사이클에서의 반도체 외주 조립 및 검사 시장의 구조적인 중요성을 더욱 강화했습니다.

자동차 제조업체는 소프트웨어 정의 플랫폼으로의 전환을 진행하여 차량당 반도체 부품 비용을 밀어 올리는 동시에 고신뢰성 패키지에 대한 수요를 가속화했습니다. 폭스바겐 그룹과 온세미 간의 트랙션 인버터 기술 제휴는 내열성이 뛰어난 파워 패키지를 필요로 하는 탄화규소 디바이스의 도입 확대를 부각시켰습니다. ASE, BMW, Bosh가 지원하는 Imec의 자동차 칩렛 프로그램은 기능 안전 준수를 위한 표준화 칩렛 패키징에서 밸류체인 전반의 협력을 보여주었습니다. AEC-Q100 및 ISO 26262에 부합하는 OSAT 제공업체는 전기자동차 공급업체로부터 새로운 설계 주문을 획득하여 다년간 생산 능력을 확보했습니다.

상용 5G 기지국의 전개에 의해 무선 프론트엔드는 mm파 영역으로 이행해, 저손실 기판, 컨포멀 실드, 컴팩트한 SiP 풋 프린트가 요구되고 있습니다. Finwave Semiconductor사의 E 모드 MISHEMT를 GlobalFoundries로 통합한 사례는 특수 RF 패키징을 필요로 하는 신규 질화갈륨 디바이스의 상용 전개를 나타내고 있으며, 2026년 양산을 목표로 하고 있습니다. 6G 테스트베드 파이프라인에는 이미 공동 패키지 광학 부품이 내장되어 있으며, OSAT 기업은 혼성 신호 조립 능력과 첨단 열 솔루션의 확장이 시급합니다.

TSMC의 '웨이퍼 Manufacturing 2.0' 전략은 패키징과 검사 공정을 통합하고 턴키 서비스를 제공함으로써 독립형 OSAT 기업의 대응 가능량을 축소시켰습니다. 삼성도 비슷한 길을 추구하고 있으며 인텔은 파운드리 서비스를 확장하여 고급 인터포저를 도입했습니다. 이러한 움직임은 고수익 부문의 제3자 점유율을 축소시켜 OSAT 기업이 자동차 안전 및 포토닉스와 같은 틈새 분야에 주력하도록 만듭니다.

검사 분야는 2026년부터 2031년에 걸쳐 CAGR 10.35%를 나타낼 전망이며, 패키징 분야의 확대 페이스를 웃도는 반면 훨씬 작은 기반에서 시작됩니다. AI 및 고성능 컴퓨팅 설계는 다양한 전압 하에서 칩렛 상호 연결 대기 시간, 동적 열 조절 및 심층 학습 워크로드의 성능을 검증하는 시스템 레벨 검사 커버리지를 요구합니다. 반면 반도체 외주 조립 및 검사 시장에서는 자동검사장치(ATE)와 적응형 머신러닝 알고리즘의 통합이 진행되어 검사 시간의 단축과 고장 개소의 특정 정밀도 향상을 도모하고 있습니다.

패키징 분야는 2025년 수익의 76.80%를 유지했지만, 그 구성은 팬아웃 패널 레벨, 2.5D 인터포저 및 공동 패키지 광학 라인으로 전환했습니다. 고객이 공급업체를 통합하는 가운데 OSAT 그룹은 지그 설계, 최종 검사 및 물류를 통합한 턴키 솔루션을 제공했습니다. 아드반테스트사는 V93000 시리즈에 AI 대응 분석 기능을 추가하여 조립 검사 장치 분야에서 6년 연속 선두 지위를 유지했습니다.

볼 그리드 어레이 기술은 기계적 견고성을 중시하는 민간 및 산업 플랫폼용의 주류로 2025년에도 23.85%의 점유율을 유지했습니다. 그러나 모바일 프로세서와 AI 가속기가 고밀도 재배선층으로 이동하는 가운데 팬아웃 웨이퍼 레벨 패키지는 CAGR 11.02%로 확대될 전망입니다. 이 동향은 수율 변동 없이 대형 패널 포맷을 처리할 수 있는 벤더가 한정되어 있기 때문에 반도체 외주 조립 및 검사 시장을 강화했습니다.

ASE에 의한 310mm×310mm 유리 패널로의 2억 달러 규모의 패널 레벨 확장은 비용 효율적인 대면적 제조를 위한 설비 투자의 의지를 나타냈습니다. 고대역 메모리 스택에서는 실리콘 관통 비아(TSV)와 유리 관통 비아(TGV)의 변형이 보급되었습니다. FC-BGA 기판은 선진 노드의 도입에 의해 혜택을 받아 네트워크용 ASIC용 유기 적층 기판과 실리콘 인터포저 사이의 갭을 메우는 역할을 했습니다.

반도체 외주 조립 및 검사(OSAT) 시장은 서비스 종별(패키징, 검사), 패키지 종별(볼 그리드 어레이, 칩 스케일 패키지 등), 용도(통신, 소비자용 전자기기, 자동차, 컴퓨팅 및 네트워킹 등), 기술 노드(28nm 이상, 16/14nm, 10/7nm 등), 지역(북미, 남아메리카, 남미)별로 구분됩니다.

아시아태평양은 2025년 반도체 외주 조립 및 검사 시장 수익의 72.90% 점유율을 달성했으며 2031년까지 연평균 복합 성장률(CAGR) 9.45%를 나타낼 전망입니다. 대만, 중국, 한국은 파운드리와 기판 제조업체와의 근접성으로 이 클러스터의 핵심을 담당해왔으나 무역 마찰의 격화에 의해 말레이시아, 베트남, 필리핀으로의 다양화가 진행되고 있습니다. 인도는 우대 조치를 가속화했으며 구자라트의 케이네스 테크놀로지사의 4억 1,300만 달러 규모 공장과 아쌈의 타타 일렉트로닉스사의 30억 달러 규모 패키지 검사 복합 시설의 건설을 승인했습니다.

북미는 CHIPS법에 의한 자금 지원을 통해 전략적 중요성을 회복했습니다. 암콜사는 애리조나주에 첨단 패키징 시설을 착공해 국내 자동차 및 AI 기업에게 공급을 계획하고 있습니다. 텍사스 인스트루먼트사는 여러 웨이퍼 공장과 후공정 설비에 600억 달러를 투입하였으며, 스카이워터사는 인피니언사의 오스틴 공장을 9,300만 달러에 인수하여 국가 수준의 이중화 능력을 확보했습니다.

유럽은 틈새 연구 개발에서 양산 체제로 이행하고 있습니다. 실리콘 박스사는 이탈리아에 13억 유로(14억 7,000만 달러)를 투입하는 패널 레벨 공장의 건설을 EU로부터 승인받아 연간 1억개 이상의 SiP 유닛 생산을 목표로 하고 있습니다. 탈레스사, 레이디얼사, 폭스콘사는 방위 및 항공우주용 프랑스 OSAT 연합 구축을 검토 중입니다. 온세미는 체코 공화국에 20억 달러를 투자하여 실리콘 카바이드 생산 라인을 건설하고 전기이동성 프로젝트를 위한 현지 공급력을 확보했습니다. 중동 및 아프리카는 신흥 시장으로 성장을 계속하고 이스라엘과 UAE는 후공정 투자자 유치를 위한 정책 틀을 검토 중입니다.

The outsourced semiconductor assembly and test market was valued at USD 47.09 billion in 2025 and estimated to grow from USD 51.12 billion in 2026 to reach USD 77.12 billion by 2031, at a CAGR of 8.56% during the forecast period (2026-2031).

Sustained progress in artificial intelligence, high-performance computing, and automotive electrification raised demand for advanced packages and safety-critical test flows, thereby widening the total addressable opportunity for specialized backend service providers. Asia-Pacific suppliers preserved pricing leverage owing to mature ecosystems, yet policy-driven capacity build-outs in North America and Europe began to reshape global supply allocation. Hybrid chiplet architectures elevated the importance of heterogeneous integration, motivating strategic investments in fan-out wafer-level and 2.5D/3D platforms. Meanwhile, tighter trade controls and sustainability mandates encouraged customers to shift part of the workload to geographically diversified sites that can demonstrate lower energy use per unit throughput. As foundry capacity remained strained, fab-lite semiconductor companies continued to outsource backend steps, reinforcing the structural relevance of the outsourced semiconductor assembly and test market in the next planning cycle.

Automotive OEMs transitioned toward software-defined platforms, lifting semiconductor bill-of-materials per car and intensifying demand for high-reliability packages. Volkswagen Group's traction inverter partnership with onsemi highlighted the rising adoption of silicon carbide devices that need thermally robust power packages.Imec's Automotive Chiplet Program, supported by ASE, BMW, and Bosch, illustrated cross-value-chain alignment on standardized chiplet packaging for functional safety compliance. OSAT providers that qualify to AEC-Q100 and ISO 26262, therefore, captured new design wins and secured multiyear capacity reservations with electric-vehicle suppliers.

Commercial 5G base-station roll-outs moved the radio front-end into millimetre-wave territory, necessitating low-loss substrates, conformal shielding, and compact SiP footprints. Finwave Semiconductor's E-mode MISHEMT integration at GlobalFoundries signalled commercial deployment of novel gallium-nitride devices that require specialised RF packaging, with mass qualification targeted for 2026. The pipeline for 6G testbeds already incorporates co-packaged optics, urging OSAT firms to expand mixed-signal assembly capabilities and advanced thermal solutions.

TSMC's Wafer Manufacturing 2.0 strategy integrated packaging and testing flows, offering turnkey services that reduced addressable volume for stand-alone OSAT companies. Samsung pursued a similar path, while Intel grew its foundry services to include advanced interposers. These moves compressed third-party share in high-margin segments and obliged OSAT firms to double down on niches such as automotive safety or photonics.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Testing captured a 10.35% CAGR forecast for 2026-2031, a pace outstripping packaging's expansion yet starting from a smaller base. AI and high-performance computing designs demanded system-level test coverage that verifies chiplet interconnect latency, dynamic thermal throttling, and deep-learning workload performance under varied voltages. The outsourced semiconductor assembly and test market responded by integrating adaptive machine-learning algorithms in automatic test equipment, cutting test time while improving fault isolation.

Packaging retained 76.80% of 2025 revenue, but its composition evolved toward fan-out panel-level, 2.5D interposer, and co-packaged optics lines. As customers consolidated suppliers, OSAT groups bundled turnkey offerings that merge fixture design, final test, and logistics. Advantest secured its sixth consecutive leadership in assembly test equipment after adding AI-enabled analytics to its V93000 series.

Ball grid array technology maintained a 23.85% share in 2025 by serving mainstream consumer and industrial platforms that value mechanical robustness. However, fan-out wafer-level packages expanded at 11.02% CAGR as mobile processors and AI accelerators transitioned to high-density redistribution layers. This trend strengthened the outsourced semiconductor assembly and test market because only a limited pool of vendors can process larger panel formats without yield drift.

ASE's USD 200 million panel-level expansion to 310 mm X 310 mm glass panels illustrated a cap-ex commitment toward cost-effective, large-area builds. Through-silicon-via and through-glass-via variants proliferated in high-bandwidth memory stacks. FC-BGA substrates benefited from advanced node adoption, bridging the gap between organic laminates and silicon interposers for networking ASICs.

Outsourced Semiconductor Assembly and Test (OSAT) Market is Segmented by Service Type (Packaging, and Testing), Packaging Type (Ball Grid Array, Chip-Scale Package, and More), Application (Communication, Consumer Electronics, Automotive, Computing and Networking, and More), Technology Node (>=28 Nm, 16/14 Nm, 10/7 Nm, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

Asia-Pacific retained 72.90% share of outsourced semiconductor assembly and test market revenue in 2025 and posted a 9.45% CAGR outlook through 2031. Taiwan, China, and South Korea anchored the cluster owing to proximity to foundries and substrate makers, yet escalating trade frictions prompted diversification into Malaysia, Vietnam, and the Philippines. India accelerated incentive programmes, endorsing Kaynes Technology's USD 413 million plant in Gujarat and Tata Electronics' USD 3 billion Assam package-test complex.

North America regained strategic weight following the CHIPS Act funding. Amkor broke ground on an advanced packaging facility in Arizona designed to supply domestic automotive and AI customers. Texas Instruments earmarked USD 60 billion for multiple wafer fabs and corresponding backend capacity, while SkyWater's USD 93 million acquisition of Infineon's Austin fab added sovereign redundancy.

Europe moved from niche R&D toward scaled production. Silicon Box obtained EU approval for a EUR 1.3 billion (USD 1.47 billion) panel-level plant in Italy, targeting >100 million SiP units per year. Thales, Radiall, and Foxconn explored a French OSAT alliance to serve defence and aeronautics users. Onsemi committed USD 2 billion to a silicon-carbide line in the Czech Republic, assuring local supply for e-mobility projects. The Middle East and Africa remained an emerging frontier, with Israel and the UAE assessing policy frameworks to attract backend investors.