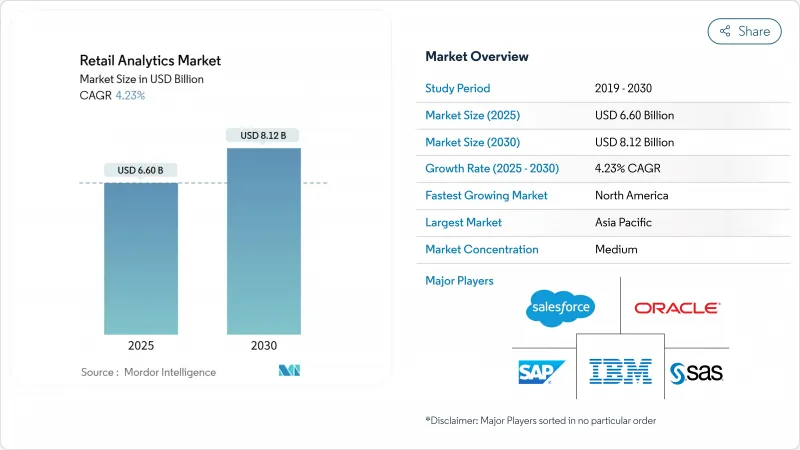

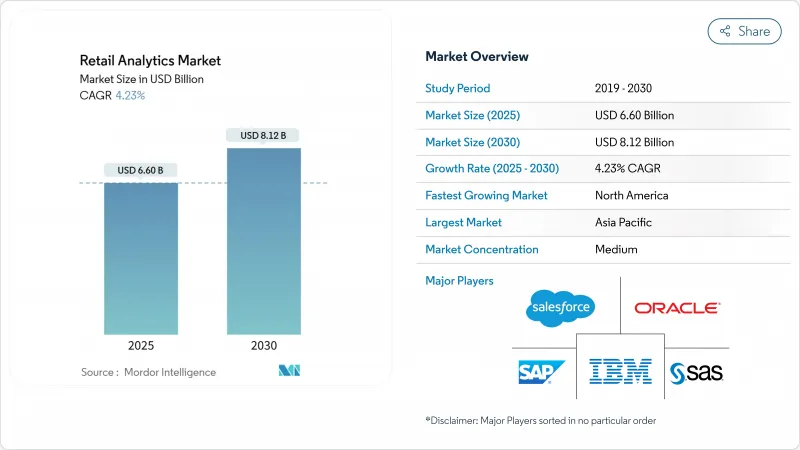

리테일 애널리틱스 시장 규모는 2025년에 66억 달러로 추정되고, 2030년에는 81억 2,000만 달러에 이를 것으로 예상되며, 기간 중 CAGR은 4.23%를 나타낼 전망입니다.

옴니채널 커머스의 확대, 데이터량의 급증, AI 주도의 의사결정 엔진의 급속한 도입으로 소매업체는 매일 프로세스에 애널리틱스를 통합하게 되었습니다. 클라우드 제공 모델은 소유 비용을 줄이고 배포 주기를 단축하여 중견 체인은 한때 세계 리더에 한정된 기능을 활용할 수 있습니다. 실시간 개인화, 처방전 인벤토리 도구 및 고급 프로모션 최적화를 통해 수익률이 줄어들어도 전환율과 주문 수익성이 향상됩니다. 경쟁 우위는 예측, 처방 및 생성의 각 기능을 통합 플랫폼으로 이동하고 분석이 재량 지출에서 소매의 기본 요구 사항으로 전환하고 있음을 보여줍니다.

소매 기업은 현재 거래, 행동, 소셜 신호를 방대하게 축적하고 있습니다. 데이터 증가 속도는 상점, 전자상거래 및 타사 피드를 통합하고 거의 실시간 보고를 지원하는 통합 데이터 레이크에 대한 투자를 촉진합니다. 신속한 패턴 인식에 익숙한 사업자는 가격 설정의 민첩성을 향상시키고 수요 예측을 선명하게 하고 재고 회전율을 높임으로써 총체적으로 조익률 향상을 뒷받침합니다. 이러한 급증을 관리함으로써 클라우드 수요도 가속화됩니다. 왜냐하면, 탄력성이 있는 인프라가 피크시의 퍼포먼스 병목을 막기 때문입니다. 그 결과 분석의 성숙도가 상업적 회복력의 기압계가 됩니다.

머신러닝을 활용한 수요 감지는 공급망 오류 및 판매 기회 손실을 줄이는 반면, 컴퓨터 비전 용도는 인텔리전스를 매장으로 확장합니다. AI를 추천 엔진에 통합한 소매업체는 새로운 크로스셀 수익원을 획득하고, 출력이 설명적인 대시보드에서 자동화된 의사결정으로 이행함으로써 평생 고객 가치를 향상시킵니다. 언어, 시각, 구조화된 데이터를 융합한 멀티모달 모델은 기능의 사일로화를 해소하는 통합 인텔리전스 레이어를 만들어 냅니다. 이러한 변화에 따라 소매업체가 요구하는 인재상이 재정의되고, 벤더의 선정 기준도 재구축되고 있으며, 현재는 사전 구축된 설명 가능한 모델이 중시되고 있습니다.

GDPR(EU 개인정보보호규정) 및 CCPA와 같은 개인 정보 보호법의 강화로 소매 기업은 동의 및 최소화 규칙을 준수하기 위해 데이터 파이프라인을 재구성해야 합니다. 현대화 예산은 기밀 정보를 암호화하고 관리하는 보안 도구에 할당되는 비율이 증가하고 애널리틱스의 혁신에서 자금이 유출되도록 되어 있습니다. 국경을 넘어서는 소매업체는 복잡한 컴플라이언스 매트릭스에 직면하여 세계 배포의 배포주기가 장기화되고 있습니다. 프라이버시 바이 디자인 프레임워크는 법규제의 영향을 줄이는 데 도움이 되지만 데이터 입도가 제한되므로 엄격한 시장에서의 고급 분석 범위가 좁아질 수 있습니다. 따라서 보호 의무와 애널리틱스의 야망 간의 상호작용은 여전히 중요한 전략적 균형 행위가 되고 있습니다.

클라우드 도입은 2024년 프로젝트의 62.00%를 차지했고, 2030년까지의 CAGR은 9.60%를 나타낼 전망입니다. 구독 가격은 자본 확약을 최소화하고 탄력적인 컴퓨팅을 통해 소매업체는 성능 저하없이 홍보 피크를 수용 할 수 있습니다. 소블린 및 대기 시간 요구 사항을 충족하기 위해 기밀 데이터를 현장에서 유지하는 체인도 있지만, 로컬 데이터 스토리지와 클라우드 컴퓨팅을 융합시킨 하이브리드 아키텍처가 전략적 중간 지점으로 부상하고 있습니다. 이러한 하이브리드 설계는 사기 감지와 같은 미션 크리티컬 워크로드의 왕복 시간을 단축하는 반면, 분석 모델 교육에 클라우드의 경제성을 활용합니다. 그 결과, 클라우드 퍼스트나 On-Premise와 같은 일률적인 스탠스가 아니라 워크로드의 특성에 따른 도입의 선택이 점점 중요해지고 있습니다.

퓨어플레이의 전자상거래 소매업체는 2024년에는 도입 건수의 60.00%를 차지했고, CAGR 9.20%로 다른 업태를 능가하는 것으로 보입니다. 그들의 디지털 네이티브 아키텍처는 레거시 통합 장애물 없이 예측 모델의 신속한 도입을 가능하게 하며 클릭할 때마다 경험을 개선할 수 있습니다. 실제 상점 사업자는 센서, RFID 및 컴퓨터 비전을 추가하여 상점에서의 행동을 실용적인 데이터로 변환하고 데이터 갭을 채우고 있습니다. 옴니채널 체인은 온라인 및 상점 인사이트를 통합하는 통합 커머스 애널리틱스를 채택하여 크로스채널에서의 재고 배분 및 완성 라우팅을 개선합니다. 이러한 다양한 우선순위는 비즈니스 모델이 애널리틱스 로드맵을 결정한다고 말하지만, 더 빠르고 세밀한 인사이트가 필요하다는 점에서 모든 형식이 일치합니다.

리테일 애널리틱스 시장은 솔루션(소프트웨어 및 서비스), 배포(클라우드, On-Premise, 하이브리드), 기능(고객 관리, 공급망 관리, 마케팅 및 머천다이징) - 가격/수율 및 기타 기능- 주문 관리), 소매업태(오프라인 매장, 퓨어플레이 E-Commerce, 옴니채널 소매), 지역(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)으로 구분됩니다.

북미는 견고한 클라우드 인프라, 전자상거래의 깊은 침투, 주요 분석 벤더와의 근접성 등에 힘입어 2024년 매출 점유율 38.20%로 리테일 애널리틱스 시장을 선도했습니다. 미국의 소매업체는 2025년 기술 예산을 증액할 계획으로 고객 데이터 플랫폼과 AI 기반 의사결정 엔진에 최대 배분을 합니다. 캐나다는 성숙한 시장에서 차별화를 위해 고객 분석에 많은 투자를 하고 멕시코는 물류 불안정성을 해결하기 위해 공급망 최적화에 중점을 둡니다.

아시아태평양은 전자상거래의 폭발적인 성장, 스마트폰의 보급 확대, 야심찬 디지털 전환 프로그램에 힘입어 2030년까지의 CAGR이 6.30%로 가장 빠릅니다. 중국은 결제, 배송, 커뮤니티 참여 데이터를 통합하고 엔드 투 엔드 인사이트 루프를 생성하는 소셜 커머스 애널리틱스의 선구자입니다. 인도에서는 다양한 소비자 동향을 배경으로 도시와 농촌 지역에서 구색을 조정하는 예측 모델의 도입이 진행되고 있습니다. 일본과 한국은 실제 매장를 활성화하기 위해 컴퓨터 비전에 의한 풋폴 측정 등 매장 중심의 애널리틱스를 중시하고 있습니다.

유럽은 영국, 독일, 프랑스의 정교한 소매 시스템을 중심으로 중요한 발자국을 남깁니다. 엄격한 개인 정보 보호 규칙은 데이터 레지던시와 클라우드 확장성의 균형을 이루는 하이브리드 배포의 추진력이 되었습니다. Sustainability Analytics는 소매업체가 환경 지표를 사용하여 조달 및 패키징 결정을 내릴 때 사용되고 인기를 얻고 있습니다. 중남미의 성장은 브라질과 아르헨티나에 집중되어 있으며, 애널리틱스는 환율 변동 관리 및 지역별 프로모션 최적화에 도움이 됩니다. 중동 및 아프리카는 아직 소규모이지만 이스라엘과 아랍에미리트(UAE) 등 시장에서 활발하고 고급 소매점과 관광업이 고객 경험 분석의 도입을 가속화하고 있습니다.

The retail analytics market size is estimated at USD 6.60 billion in 2025 and is projected to reach USD 8.12 billion by 2030, registering a 4.23% CAGR across the period.

Broader omnichannel commerce, surging data volumes, and rapid adoption of AI-driven decision engines are encouraging retailers to embed analytics into day-to-day processes. Cloud delivery models are cutting ownership costs and trimming deployment cycles, which allows mid-tier chains to access capabilities once limited to global leaders. Real-time personalization, prescriptive inventory tools, and advanced promotion optimisation are lifting conversion rates and order profitability even as margins tighten. Competitive advantage is shifting toward platforms that integrate predictive, prescriptive, and generative capabilities, signaling that analytics has moved from a discretionary spend to a fundamental retail requirement.

Retailers now ingest vast pools of transaction, behavioural, and social signals that dwarf prior years and mandate scalable analytics platforms. The pace of data growth is prompting investments in unified data lakes that consolidate store, e-commerce, and third-party feeds to support near real-time reporting. Operators that master rapid pattern recognition improve pricing agility, sharpen demand forecasts, and raise inventory turns, which collectively push gross-margin lift. Managing this surge also accelerates cloud demand because elastic infrastructure prevents performance bottlenecks during peak events. Consequently, analytic maturity becomes a barometer for commercial resilience.

Machine-learning-powered demand sensing is reducing supply-chain errors and missed sales opportunities, while computer vision applications extend intelligence to the sales floor. Retailers that embed AI into recommendation engines capture new cross-sell revenue streams and improve lifetime customer value as output moves from descriptive dashboards to automated decisions. Multimodal models that blend language, vision, and structured data produce unified intelligence layers that break down functional silos. These shifts are redefining the talent profiles retailers seek and are reshaping vendor selection criteria, with emphasis now on pre-built, explainable models.

Tightening privacy laws such as GDPR and CCPA compel retailers to re-engineer data pipelines to uphold consent and minimisation rules. Modernisation budgets now allocate growing shares to security tooling that encrypts and governs sensitive information, diverting funds from analytics innovation. Cross-border retailers face complex compliance matrices that elongate deployment cycles for global rollouts. Privacy-by-design frameworks help reduce regulatory exposure but also limit data granularity, which may curb the scope of advanced analytics in high-stringency markets. The interplay between protection mandates and analytics ambitions, therefore, remains a key strategic balancing act.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cloud deployments captured 62.00% of projects in 2024 and will grow at a 9.60% CAGR to 2030. Subscription pricing minimises capital commitments, and elastic compute equips retailers to handle promotional peaks without performance dips. Although some chains retain sensitive data on-site to satisfy sovereignty and latency requirements, hybrid architectures that blend local data storage with cloud compute are emerging as a strategic middle ground. These hybrid designs reduce round-trip times for mission-critical workloads such as fraud detection while leveraging cloud economics for analytics model training. As a result, deployment choices increasingly hinge on workload characteristics rather than a blanket cloud-first or on-premises stance.

Pure-play e-commerce retailers captured 60.00% of deployments in 2024 and will continue to outgrow other formats at a 9.20% CAGR. Their digital-native architectures enable rapid adoption of predictive models without legacy integration hurdles, allowing them to refine experiences at every click. Brick-and-mortar operators are bridging the data gap by adding sensors, RFID, and computer vision to convert in-store behaviour into actionable data. Omnichannel chains adopt unified commerce analytics that merge online and store insights to improve cross-channel stock allocation and fulfilment routing. These varied priorities illustrate that business model dictates analytics roadmaps, yet all formats converge on the need for faster, more granular insights.

Retail Analytics Market is Segmented by Solutions (Software and Services), Deployment (Cloud, On-Premises, Hybrid), Function (Customer Management, Supply Chain Management, Marketing and Merchandising - Pricing/Yield, Other Functions - Order Management), Retail Format (Brick-And-Mortar Stores, Pure-Play E-Commerce, Omnichannel Retailers), Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa).

North America led the retail analytics market with 38.20% revenue share in 2024, supported by robust cloud infrastructure, deep e-commerce penetration, and proximity to leading analytics vendors. United States retailers plan to raise technology budgets in 2025, directing the largest allocations to customer-data platforms and AI-based decision engines. Canada trails slightly yet invests heavily in customer analytics to differentiate in a mature market, while Mexico emphasises supply-chain optimisation to address logistics volatility.

Asia-Pacific is set to post the fastest CAGR at 6.30% through 2030, propelled by explosive e-commerce growth, increasing smartphone adoption, and ambitious digital transformation programs. China pioneers social-commerce analytics that integrate payment, delivery, and community engagement data, producing end-to-end insight loops. India's diverse consumer landscape encourages retailers to deploy predictive models that tailor assortments across urban and rural zones. Japan and South Korea emphasise store-centric analytics such as computer-vision footfall measurement to revitalise physical outlets.

Europe retains a meaningful footprint anchored by sophisticated retail systems in the United Kingdom, Germany, and France. Stringent privacy rules drive adoption of hybrid deployments that balance data residency with cloud scalability. Sustainability analytics is gaining traction as retailers use environmental metrics to guide sourcing and packaging decisions. Latin American growth concentrates in Brazil and Argentina, where analytics helps manage currency volatility and optimise localised promotions. Middle East and Africa remain smaller but active in markets such as Israel and the United Arab Emirates, where luxury retail and tourism accelerate the adoption of customer experience analytics.