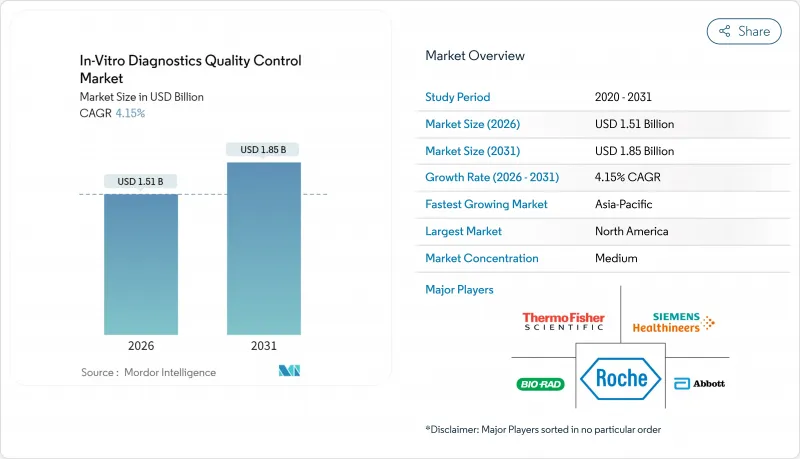

체외진단약(IVD) 품질 관리 시장은 2025년 14억 5,000만 달러로 평가되었으며, 2026년 15억 1,000만 달러에서 2031년까지 18억 5,000만 달러에 이를 것으로 예측됩니다. 예측기간(2026-2031년)의 CAGR은 4.15%로 예상됩니다.

이러한 꾸준한 성장은 검사기관의 실시간 모니터링으로의 급속한 전환, 포인트 오브 케어 검사의 보급 확대, 엄격한 인증 요건의 증가를 반영합니다. 아시아태평양은 정부 주도 검사 네트워크와 ISO 15189 규격의 도입으로 제3자 재료의 수요가 높아지면서 가장 급속한 확대를 보이고 있습니다. 품질 관리 제품은 여전히 수익의 대부분을 차지하지만 데이터 관리 솔루션은 급속히 확대되고 있습니다. 이는 검사실이 환자에게 도달하기 전에 편차를 비교할 수 있는 벤치마크 대시보드를 찾는 움직임 때문입니다. 정밀의료 프로토콜에 견인되는 분자진단 분야에서는 복잡한 유전자 기반 검사를 검증할 수 있는 합성 대조 시료의 필요성이 높아지고 있습니다. 시장의 선도기업은 컴플라이언스 업무 흐름을 효율화하는 소프트웨어와 시료를 통합한 번들 제품으로 이에 대응하고 있습니다.

분자종양학 패널과 고처리량 감염증 검사가 많은 임상 판단의 기반이 되는 가운데, 검사실은 분석 정밀도를 강화할 수밖에 없습니다. 복잡한 다중검사에는 환자 시료를 모방하고 다양한 시약 로트에서 기능하는 대조 시료가 필요하며, 이는 국제 기준에 소급 가능한 제3자 재료의 도입을 촉진하고 있습니다. 세계보건기구(WHO)는 견고한 검사실 품질 관리가 적시에 신뢰할 수 있는 검사 결과의 기반이 된다고 지적합니다. 분석의 복잡성이 높아짐에 따라 Levy-Jennings 차트의 추이를 실시간으로 표시하는 소프트웨어 대시보드가 표준화되고 있으며, 편차가 결과에 영향을 미치기 전에 관리자가 개입할 수 있게 되었습니다. 벤더는 이러한 분석 기능을 시스템과 번들하고 품질을 일상 업무에 통합함으로써 검사실이 ISO 15189의 지속적인 개선에 관한 조항을 충족하도록 뒷받침하고 있습니다.

빈발하는 감염증 유행과 암 이환율이 높은 고령화 인구의 증가로 분자 검사 수요가 확대되면서 정확한 품질 관리의 중요성이 높아지고 있습니다. COVID-19 위기에서는 300가지 유형 이상의 분자검사가 긴급사용허가를 취득했지만, 성능에는 큰 편차가 보였고, 기존 품질 관리 모델의 한계가 노출되었습니다. 360Dx 코로나바이러스 검사 트래커는 미국, EU 및 아시아 전역에서 수많은 새로운 검사 방법을 기록했습니다. 이를 통해 돌연변이 균주의 출현과 함께 검사실은 신속하게 유연하고 조정 가능한 병원체 특이 대조군으로 대응했습니다. 유사한 혁신은 호흡기 패널과 유전성 암 선별검사로 확대되고 있으며, 합성 컨트롤이 워크플로를 안정화시켜 생물안전 위험을 억제하고 있습니다.

공공제도 및 민간보험사에 의한 지불액의 하락이 임상검사실의 이익률을 축소시켜, 종합적인 품질 관리 프로그램에 대한 자금 조달이 곤란한 상황입니다. 미국은 최근 메디케어 보상 체계를 줄이고 유럽에서는 유사한 수수료를 재검토함으로써 일상적인 화학 검사 및 면역 측정 검사의 허용 청구액이 감소한 반면, 고급 제3자 관리 시약의 추가 비용은 보장되지 않았습니다. 많은 병원 네트워크는 다년간의 검사 가격 상한을 설정하는 일괄 계약을 협상하고 있으며, 여기에는 새로운 QC 플랫폼에 대한 투자 유연성이 더욱 제한되어 있습니다. 소규모 독립 검사 기관이 특히 영향을 받고 있으며 소프트웨어 업그레이드를 연기하고 최소한의 일상 관리 기능만을 계속 사용하여 표준 준수를 충족하는 경우가 적습니다. 제조업체 각사는 환급 상한이 고정된 시장에서 프리미엄 데이터 분석 패키지의 도입이 둔화하고 있다고 보고하고 있습니다.

2025년에는 품질 관리 제품이 매출의 대부분을 차지하면서 체외진단약(IVD) 품질 관리 시장에서 71.32%의 점유율을 확보했습니다. 일상적인 검사 및 검증에 필수적인 반면, 그 성장은 급격하기보다는 꾸준합니다. 검사실 관리자는 미들웨어, 피어 분석 및 인증 문서를 통합하는 데이터 관리 플랫폼으로 전환하고 있습니다. 이 플랫폼은 2031년까지 10.67%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측되며 이는 예방적 품질 모델로의 구조적 전환을 반영합니다. 조기 도입자는 문제 해결 사이클의 단축과 기능 시험의 불합격률 감소를 보고하고 있으며, 이러한 결과는 ISO 15189 인증 감사를 직접 뒷받침합니다.

디지털 툴은 공급업체가 클라우드 스토리지, 모바일 알림, 예지보전 등의 구독 서비스를 업셀링하는 수단이 됩니다. 이를 통해 얻은 지속적인 수익은 제조업체의 가시성을 높이고 동시에 검사실에서 수작업으로 시행되는 기록 작업을 줄입니다. 이 플랫폼은 여러 분석 장비에 걸친 시약 로트의 변동을 추적하므로 물리적 제어 소비를 줄이고 세계 공급의 부족 시 압박을 완화합니다. 인식이 확산됨에 따라 더 많은 이해관계자가 데이터 관리 솔루션이 더 이상 추가 기능이 아니라 현대적인 품질 생태계의 핵심 요소라고 인식하고 있습니다. 이는 체외진단약(IVD) 품질 관리 시장이 서비스 주도형 모델로 진화하는 기반이 되고 있습니다.

북미는 2025년 매출의 44.73%를 차지하면서 선두를 유지했습니다. 이는 약 320,000개의 검사기관이 일상적인 QC 성과를 문서화할 것을 의무화하는 CLIA의 감독체제에 의해 뒷받침됩니다. 이 지역에는 주요 시약 제조업체의 대부분이 거점을 두어 당일 보충과 광범위한 현지 서비스 지원을 가능하게 하고 있습니다. 의료 시스템에서는 병원 체인 전체에서 QC 데이터를 집계하는 엔터프라이즈 미들웨어의 규모가 확대되고 있으며, 사이버 보안 요건을 준수하는 상호 운용 가능한 관리 시약 및 분석의 구독에 대한 수요가 증가하고 있습니다. 또한, 환급 압력은 검사실에서 환자 기반의 실시간 QC를 도입하고 있으며, 이는 소모품을 줄이는 한편, 견고한 소프트웨어 알고리즘에 대한 의존도가 높아지고 있습니다.

아시아태평양은 10.89%의 지역 CAGR을 유지하며 체외진단약(IVD) 품질 관리 시장에서 탁월한 성장엔진으로 지속되고 있습니다. 중국의 검사 결과 상호 승인 추진과 인도의 전국 암 검진 플랫폼 확대가 주요 원동력이 되고 있습니다. 중국에서는 많은 성급 센터가 ISO 15189로 이행하여 편향이 없는 시험 기준을 충족하는 제3자 관리 시약에 대한 수요를 창출하고 있습니다. 지역 유통업체는 콜드체인 물류에 대응하는 동결건조 화학제어에 대한 관심이 높아지고 있다는 보고가 있으며, 인증 추적성을 간소화하는 중국어와 힌디어 대응 클라우드 QC 포털이 급속히 보급되고 있습니다.

유럽은 성숙하면서도 꾸준히 진화하는 시장 환경을 보여줍니다. 국경을 넘어서는 검사 결과의 조화로운 교환이 서로 다른 분석장치 간의 비교가능성을 확보하여 상호 환산 가능한 참조 기준으로 검증된 컨트롤에 대한 투자를 촉진하고 있습니다. 유럽에서는 태스크 이동의 동향이 강해지면서 1차 의료 현장에서의 신속 검사가 증가하고 있습니다. 이를 통해 상세한 원격 트레이닝 모듈과 함께 제공되는 컴팩트한 QC 바이알에 대한 수요가 확대되고 있습니다. 바코드가 달린 로트 등록 기능을 현지 검사 정보 관리 시스템(LIMS)에 통합하는 공급업체는 입찰의 주문률을 높이고 문서화된 추적성을 중시하는 규제 환경 하에서 적절한 단일 자릿수 성장을 실현합니다.

The In-Vitro Diagnostics Quality Control Market was valued at USD 1.45 billion in 2025 and estimated to grow from USD 1.51 billion in 2026 to reach USD 1.85 billion by 2031, at a CAGR of 4.15% during the forecast period (2026-2031).

This steady pace reflects laboratories' rapid move toward real-time monitoring, wider point-of-care adoption, and stringent accreditation demands. Asia-Pacific is expanding the fastest, helped by government-funded testing networks and ISO 15189 rollouts that lift demand for third-party materials. Quality control products still dominate revenue, yet data management solutions are scaling quickly as labs seek peer benchmarking dashboards that flag errors before they reach patients. Molecular diagnostics, driven by precision-medicine protocols, is sharpening the need for synthetic controls that can verify complex gene-based assays. Market leaders are responding with integrated software-plus-material bundles that streamline compliance workflows.

Molecular oncology panels and high-throughput infectious disease assays now underpin many clinical decisions, forcing labs to tighten analytical precision. Complex multiplex tests require controls that mimic patient samples and perform across varied reagent lots, driving adoption of third-party materials traceable to international standards. The World Health Organization notes that robust laboratory quality management underpins timely, reliable test outcomes. As assay complexity rises, software dashboards that trend Levy-Jennings plots in real time are becoming routine, letting supervisors intervene before deviation affects results. Vendors are bundling such analytics with controls to embed quality into daily workflows, helping labs satisfy ISO 15189 clauses on continual improvement.

Frequent outbreaks and an aging population with higher cancer prevalence expand molecular testing volumes, raising the stakes for accurate QC. During the COVID-19 crisis, more than 300 molecular tests gained emergency authorization, yet performance varied widely, exposing gaps in legacy QC models. The 360Dx Coronavirus Test Tracker recorded scores of new assays across the US, EU, and Asia. Developers responded with flexible, pathogen-specific controls that laboratories could calibrate quickly as variants emerged. Similar innovation is extending to respiratory panels and hereditary cancer screens, where synthetic controls stabilize workflows and curb biosafety risks.

Lower payment schedules from public and private insurers are squeezing clinical laboratory margins, making it difficult to fund comprehensive quality control programs. Recent Medicare fee-schedule cuts in the United States and similar tariff reviews in Europe have reduced allowable charges for routine chemistry and immunoassay tests, yet they do not cover the incremental costs of advanced third-party controls. Many hospital networks now negotiate bundled contracts that cap test prices for multiple years, further limiting flexibility to invest in new QC platforms. Smaller independent labs are especially affected; they often postpone software upgrades and continue using minimal daily controls that meet only baseline compliance. Manufacturers report slower uptake of premium data analytics packages in markets where reimbursement ceilings remain static.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Quality control products generated the bulk of revenue in 2025, securing 71.32% of the in-vitro diagnostics quality control market size. They remain essential for daily assay validation, yet their growth is steady rather than spectacular. Laboratory managers are pivoting toward data management platforms that integrate middleware, peer analytics, and accreditation documentation. These platforms are forecast to post an 10.67% CAGR through 2031, reflecting a structural leap toward preventive quality models. Early adopters report shorter troubleshooting cycles and reduced proficiency-testing failures, outcomes that directly support ISO 15189 accreditation audits.

Digital tools also allow vendors to upsell subscription services such as cloud storage, mobile alerts, and predictive maintenance. The resulting recurring revenue improves manufacturers' visibility while reducing manual charting for laboratories. Because these platforms track reagent lot shifts across multiple analyzers, they lower the volume of physical controls consumed, easing supply pressures during global shortages. As awareness spreads, more stakeholders recognize that data management solutions are no longer optional add-ons but core components of a modern quality ecosystem, underpinning the in-vitro diagnostics quality control market's evolution into a service-driven model.

The in Vitro Diagnostics Quality Control Market Report is Segmented by Products and Services (Quality Control Products, Data Management Solutions, Quality Assurance Services), Application (Immunochemistry, Clinical Chemistry, Hematology, and More), End User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America led with 44.73% of 2025 revenue, bolstered by CLIA's oversight of roughly 320,000 laboratory entities that must document daily QC performance. The region also hosts most top reagent makers, enabling same-day replenishment and extensive field-service support. Health systems are scaling enterprise middleware that aggregates QC data across hospital chains, raising orders for interoperable control materials and analytics subscriptions that align with cybersecurity mandates. Furthermore, reimbursement pressures are prompting laboratories to adopt patient-based real-time QC, which cuts consumables yet depends heavily on robust software algorithms.

Asia-Pacific, with an 10.89% regional CAGR, remains the standout growth engine for the in-vitro diagnostics quality control market. China's push for mutual recognition of lab results and India's expansion of national cancer screening platforms are major tailwinds. Many provincial centers in China have upgraded to ISO 15189, creating demand for third-party controls that satisfy unbiased testing criteria. Regional distributors report heightened interest in lyophilized chemistry controls that tolerate warm-chain logistics, and cloud QC portals localized in Mandarin or Hindi experience rapid adoption as they simplify accreditation traceability.

Europe presents a mature yet steadily evolving landscape. Harmonized test-result exchange across borders is stimulating investments in controls verified against commutable reference standards to ensure comparability between different analyzers. The European trend toward task-shifting sees more rapid tests executed in primary care, expanding need for compact QC vials packaged with detailed remote-training modules. Suppliers that integrate barcoded lot registration into local Laboratory Information Management Systems enjoy stronger tender wins, supporting mid-single-digit growth in a regulatory environment that prizes documented traceability.