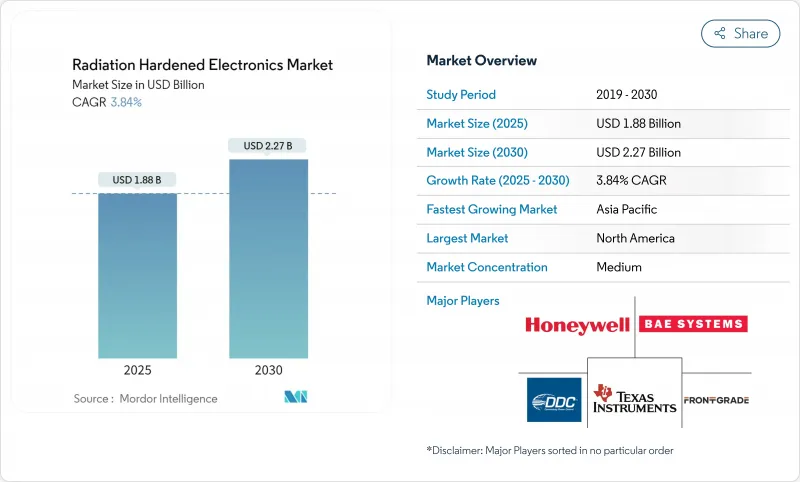

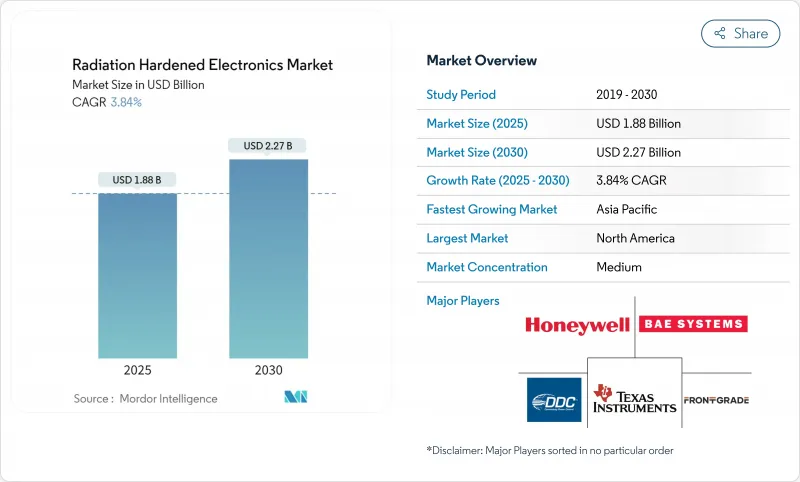

세계의 방사선 경화 전자 시장 규모는 2025년에 18억 8,000만 달러로, 2030년까지 22억 7,000만 달러에 달할 것으로 예측되며, CAGR은 3.84%로 예상됩니다.

수요는 계속해서 심우주 및 전략적 방위 임무를 위한 초고신뢰성 부품과 급증하는 저궤도(LEO) 컨스텔레이션 및 성층권 플랫폼을 위한 비용 최적화된 방사선 경화 장치로 이분됩니다. 지정학적 요인, 특히 NATO의 핵 근대화 계획, 아시아의 원자력 발전소 건설 재개, 소형 위성 발사의 활성화에 의해 제품의 로드맵과 자격 심사의 우선 순위가 재형성되고 있습니다. 상업 주조소는 방위 관련 프라임과 제휴하여 성숙한 실리콘 노드를 확장하는 한편 차세대 전력 시스템용으로 질화갈륨(GaN)과 탄화규소(SiC)를 통합하고 있습니다. 90nm 미만의 RHBP(Radiation-Hard-By-Process) 능력에서 공급망의 병목 현상은 진화하는 수출 규제와 함께 개발 사이클을 단축하고 비용을 절감하는 RHBD(Radiation-Hard-By-Design) 기법에 대한 병행적인 추진을 촉진하고 있습니다.

LEO 메가 컨스텔레이션 성능 목표의 새로운 계층화를 추진하고 있습니다. 대량 생산 위성을 위한 30-50 krad(Si) 내성 부품과 정지 위성 및 심우주 위성을 위한 100 krad(Si) 내성 부품입니다. 디바이스 벤더는 현재 고집적화와 저실드 질량을 양립시킨 소형화 GaN 파워 스테이지 등의 제품 라인을 병행하여 운영하고 있습니다. 동시에 내 방사선 FPGA를 사용하여 궤도에서 재구성하면 운영자가 물리적 액세스 없이 미션 소프트웨어를 업데이트 할 수 있으며 컨스텔레이션 수명주기가 연장됩니다. 달 보급 위성과 화성 중계 위성의 수주 잔여는 견조하고, 심우주 수요는 더욱 높아지고 있습니다.

미국과 유럽의 방위부는 고도의 전자기 펄스 시나리오로부터 중요한 시스템을 보호하기 위해 신뢰할 수 있는 국산 마이크로 일렉트로닉스에 자금을 투입하고 있습니다. 2025년도 미국 국방부 예산에서는 방사선에 강한 RF 및 광전자의 프로토타입을 가속화하기 위해 2,488만 4,000달러가 할당되었습니다. 시험 인프라도 이에 준하고 있습니다. 해군 수상전 센터 크레인의 단펄스 감마선 시설은 1억 달러를 투입하여 근대화를 추진하고 핵 근대화 프로그램의 동시 진행을 가능하게 하고 있습니다.

방사선 경화 ASIC의 개발에는 시판의 동등품에 비해 5-10배의 비용이 듭니다. 전략적 방사성 전자 협의회(Strategic Radiation-Hardened Electronics Council)는 2025년까지 연간 6,000시간까지 SEE 테스트 빔이 과도하게 신청될 것으로 예상하고 있으며, 이 격차가 인증 대기행렬을 늘리고 있습니다. 따라서 우주사업자는 COTS 기반 선정과정을 간소화하여 리드타임을 단축하고 궤도의 라이프 리스크와 발사시기의 균형을 맞추려고 합니다.

우주 부문은 2024년 방사선 경화 일렉트로닉스 시장의 46.3%를 차지했으며 총 이온화 선량과 단일 사건 영향 내성의 사양 기준선을 지원합니다. 맞춤형 GEO 우주선에서 급증하는 LEO 컨스텔레이션으로 전환하는 운영자는 현재 저비용 및 신속한 새로 고침을 위해 탄력성의 일부를 교환하고 낮은 차폐 질량으로 30krad(Si) 설계 목표에 맞는 하이브리드 제품 라인을 촉매하고 있습니다. NASA의 Artemis 달 프로그램과 상업적인 태양계 물류는 심우주 방사선 대역을 견디는 100krad(Si) 이상의 장치에 대한 안정적인 수요를 지원합니다.

고고도 UAV/HAPS 플랫폼은 2030년까지 4.2%의 성장이 예측되어 항공우주 일렉트로닉스를 준우주 방사선 스펙트럼으로 확장합니다. 설계자는 RHBD FPGA를 적응형 페이로드에 활용하여 와이드 밴드갭의 파워 스테이지를 사용하여 엄격한 에너지 예산에 대응합니다. 이 하위 부문의 방사선 경화 일렉트로닉스 시장 규모는 6G 네트워크 백홀 테스트가 프로토타입에서 운영 플릿으로 이동함에 따라 확대될 것으로 예측됩니다.

2024년 방사선 경화 일렉트로닉스 시장 점유율은 집적 회로가 31.5%를 차지했으며 혼합 신호 ASIC이 여러 아날로그 프론트엔드와 전원 관리 기능을 하나의 다이로 집계하여 보드 레벨 질량을 줄였습니다. SEE에 대응하는 빔타임에 관한 공급 리스크는 칩 하우스가 동일한 IP 블록을 2개의 주조 플로우로 동시에 인정하도록 촉구하여 계속계획을 강화하고 있습니다.

필드 프로그래머블 게이트 어레이는 위성 운영자가 궤도에서 재구성을 강조하는 동안 CAGR로 가장 빠른 4.6%를 보일 것으로 예상됩니다. 최신 Kintex UltraScale XQRKU060 클래스는 200만 개의 로직 셀과 구성 메모리 업셋을 완화하는 온칩 스크럽 컨트롤러를 결합합니다. 방사선 경화 일렉트로닉스 시장에서 FPGA는 고정 기능 실리콘과 소프트웨어만의 결함 완화 갭을 채우고 디스크리트 로직으로부터 점유율을 빼앗고 있습니다.

북미는 2024년 매출의 39.8%를 차지했으며 지속적인 방어 예산과 NASA의 탐사 이니셔티브에 의해 지원되었습니다. 신뢰할 수 있는 국내 파운드리와 NSWC Crane 등의 전용 빔라인 설비가 인증 루프를 단축하고 많은 공급 계약 공급망을 지원합니다. 달 통신과 소행성 탐사 임무로의 우주상거래 다양화는 이 지역 수요를 더욱 지원할 것입니다.

아시아태평양은 중국, 인도, 한국이 로켓 함대 규모를 확대하고 신조 원자로 시운전을 하기 때문에 2030년까지 연평균 복합 성장률(CAGR)이 가장 빨리 4.1%를 기록합니다. 정부 우주 기관은 수입 부품에 대한 의존도를 줄이기 위해 현지 대학과 공동으로 RHBD 설계 센터에 투자하고 있습니다. 신흥 상업 출시 업체도 민첩한 위성 비즈니스 모델을 지원하기 위해 내 방사선 FPGA를 채택하고 있습니다.

유럽에서는 ESA의 대규모 미션 파이프라인과 강력한 원자력 발전소 개조 일정이 결합되어 있습니다. NEUROSPACE 이니셔티브와 같은 뉴로모픽 온보드 프로세싱 프로그램은 이 지역의 초저전력 컴퓨팅에 축발을 부각하고 있습니다. 아랍에미리트(UAE)과 사우디아라비아에 위치한 중동 우주 사무소는 화성 탐사기와 지구 관측 클러스터를 추구하고 현지에서 조립 및 시험의 틈새 기회를 열고 있습니다. 남미는 아직 개발 도상이지만, 자국제의 어비오닉스를 요구하는 브라질과 아르헨티나의 소형 위성 프로젝트로부터 혜택을 받고 있습니다.

The radiation hardened electronics market size stands at USD 1.88 billion in 2025 and is forecast to climb to USD 2.27 billion by 2030, reflecting a 3.84% CAGR.

Demand continues to bifurcate between ultra-high-reliability parts for deep-space and strategic defense missions and cost-optimized, radiation-tolerant devices for proliferated low-Earth-orbit (LEO) constellations and stratospheric platforms. Geopolitical drivers-most notably NATO nuclear-modernization programs, renewed nuclear-power construction in Asia, and the ramp-up of small-satellite launches-are reshaping product road maps and qualification priorities. Commercial foundries are partnering with defense primes to stretch mature silicon nodes while integrating gallium nitride (GaN) and silicon carbide (SiC) for next-generation power systems. Supply-chain bottlenecks in <=90 nm radiation-hard-by-process (RHBP) capacity, together with evolving export-control regimes, spur a parallel push toward radiation-hard-by-design (RHBD) methodologies that shorten development cycles and lower cost.

LEO mega-constellations are driving a new stratification of performance targets: 30-50 krad(Si) tolerant parts for mass-manufactured satellites versus >=100 krad(Si) parts for geostationary and deep-space assets. Device vendors now run parallel product lines, such as miniaturized GaN power stages that blend higher integration with lower shielding mass.Smaller spacecraft footprints intensify the need for size-, weight-, and power-optimized (SWaP) solutions while preserving single-event-effect immunity. Concurrently, on-orbit reconfigurability via radiation-tolerant FPGAs allows operators to refresh mission software without physical access, extending constellation life cycles. Strong backlog for lunar logistics and Mars relay satellites further cements deep-space demand.

The United States and European defense ministries are channeling funds into trusted domestic microelectronics to shield critical systems from high-altitude electromagnetic pulse scenarios. The FY 2025 United States DoD budget allocates USD 24.884 million to accelerate radiation-hardened RF and opto-electronic prototypes. Test infrastructure follows suit: Naval Surface Warfare Center Crane's Short Pulse Gamma facility underpins a USD 100 million modernization drive, enabling concurrent nuclear-modernization programs.

Developing radiation-hardened ASICs costs 5-10 times more than commercial equivalents. The Strategic Radiation-Hardened Electronics Council forecasts SEE test-beam oversubscription of up to 6,000 hours annually by 2025, a gap that stretches qualification queues. Space operators therefore pilot streamlined COTS-based selection processes to cut lead times, balancing life-orbit risk against launch cadence.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The space segment accounted for 46.3% of the radiation hardened electronics market in 2024, anchoring specification baselines for total-ionizing-dose and single-event-effect immunity. Operators moving from bespoke GEO spacecraft to proliferated LEO constellations now trade some resilience for lower cost and rapid refresh, catalyzing hybrid product lines that mate 30 krad(Si) design targets with lower shielding mass. NASA's Artemis lunar program and commercial cislunar logistics underpin steady demand for >=100 krad(Si) devices that survive deep-space radiation belts.

High-Altitude UAV/HAPS platforms, forecast to grow at 4.2% to 2030, extend aerospace electronics into a quasi-space radiation spectrum. Designers leverage RHBD FPGAs for adaptive payloads and use wide-band-gap power stages to meet tight energy budgets. The radiation hardened electronics market size for this sub-segment is projected to broaden as 6G network backhaul trials migrate from prototypes to operational fleets.

Integrated circuits held 31.5% radiation hardened electronics market share in 2024, with mixed-signal ASICs consolidating multiple analog front ends and power-management functions onto a single die to trim board-level mass. Supply risks around SEE-capable beam time are prompting chip houses to qualify identical IP blocks simultaneously on two foundry flows, bolstering continuity plans.

Field-programmable gate arrays represent the fastest 4.6% CAGR as satellite operators prize in-orbit reconfiguration. The latest Kintex UltraScale XQRKU060 class blends 2 million logic cells with on-chip scrub controllers that mitigate configuration memory upsets. The radiation hardened electronics market sees FPGAs bridging the gap between fixed-function silicon and software-only fault mitigation, carving share from discrete logic.

The Radiation Hardened Electronics Market Report is Segmented by End-User (Space, and More), Component (Discrete Semiconductors, and More), Product Type (Analog and Mixed-Signal, Digital Logic, and More), Manufacturing Technique (Rad-Hard-By-Design (RHBD), and More), Semiconductor Material (Silicon, and More), Radiation Type (Total Ionizing Dose (TID), and More), Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America generated 39.8% of 2024 sales, buoyed by sustained defense budgets and NASA exploration initiatives. Trusted domestic foundries, plus dedicated beam-line capacity at facilities such as NSWC Crane, shorten certification loops and anchor many prime-contractor supply chains. Space commerce diversification into lunar communications and asteroid-prospecting missions should further support regional demand.

Asia Pacific posts the quickest 4.1% CAGR to 2030 as China, India, and South Korea scale rocket fleets and commission new-build nuclear reactors. Government space agencies co-invest with local universities in RHBD design centers to decrease reliance on imported parts. Emerging commercial launch providers likewise adopt radiation-tolerant FPGAs to meet agile-satellite business models.

Europe combines ESA's large mission pipeline with strong nuclear-plant refurbishment schedules. Neuromorphic on-board processing programs such as the NEUROSPACE initiative underscore the region's pivot toward ultra-low-power compute. Middle-East space offices in the UAE and Saudi Arabia pursue Mars probes and Earth-observation clusters, opening niche opportunities for localized assembly and test. South America remains nascent but benefits from Brazilian and Argentine small-satellite projects seeking home-grown avionics.