내방사선성 전자부품 시장 : 부품별, 제조 기술별, 제품 유형별, 용도별, 지역별 - 예측(-2030년)

Radiation Hardened Electronics Market by Component (Mixed Signal ICs, Processors & Controllers, Memory, Power Management), Manufacturing Technique (RHBD, RHBP), Product Type (COTS, Custom), Application and Region - Global Forecast to 2030

상품코드:1829989

리서치사:MarketsandMarkets

발행일:2025년 09월

페이지 정보:영문 286 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

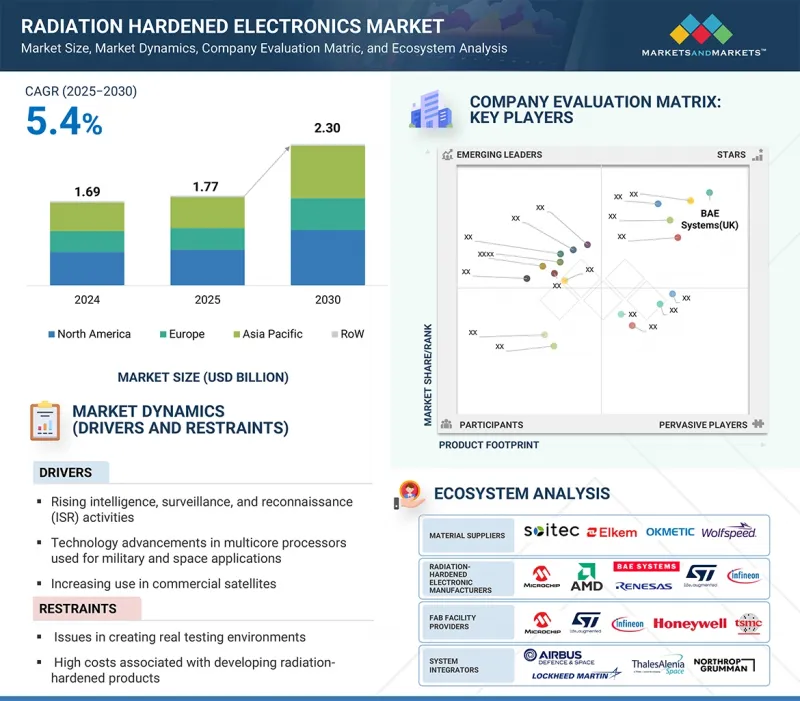

세계의 내방사선성 전자부품 시장 규모는 2025년 17억 7,000만 달러에서 2030년까지 23억 달러에 이를 것으로 예측되며, 예측 기간에 CAGR 5.4%의 성장이 전망됩니다.

인공위성, 무인항공기, 국방 시스템 등의 정보 수집, 감시 및 정찰(ISR) 플랫폼이 열악한 환경에서 미션 크리티컬한 성능을 보장하기 위해 방사선 내성 프로세서, 컨트롤러, 메모리 디바이스, 혼합 신호 IC에 대한 의존도가 높아짐에 따라 시장은 꾸준한 성장세를 보이고 있습니다.

조사 범위

조사 대상 연도

2021-2030년

기준 연도

2024년

예측 기간

2025-2030년

단위

10억 달러

부문

부품, 제조 기술, 제품 유형, 용도, 지역

대상 지역

북미, 유럽, 아시아태평양, 기타 지역

국방 및 우주 기관은 상황 인식 및 보안 통신을 강화하기 위해 ISR 기능에 많은 투자를 하고 있으며, 이에 따라 신뢰할 수 있는 내방사선 부품에 대한 수요가 증가하고 있습니다. 그러나 높은 개발 비용과 실제 테스트 환경 재현의 어려움은 여전히 산업의 주요 억제요인으로 작용하고 있습니다. 동시에, 전 세계 우주 비행 증가와 위성의 상용 상용 부품(COTS) 채택은 기회를 창출하는 한편, 고급 고객의 맞춤형 요구 사항과 같은 과제는 계속해서 경쟁 환경을 형성하고 있습니다.

"메모리 부문은 2025-2030년 동안 가장 높은 CAGR로 성장할 것으로 예상했습니다. "

부품 부문의 메모리는 예측 기간 동안 가장 높은 CAGR로 성장할 것으로 예측됩니다. 메모리 장치는 데이터를 저장하고 통신 및 기능을 가능하게 하는 하드웨어 부품입니다. 우주선, 핵무기 등 중요한 용도에 사용되는 메모리 제품은 반도체 부품이 받는 총 이온화선량(TID)을 줄이기 위해 내방사선 강화가 필요합니다. 항공우주 및 우주 분야의 컴퓨팅 집약적인 용도는 다양한 프로세서 노드와 센서에서 발생하는 대량의 데이터를 처리하기 위해 고밀도, 고성능, 내방사선 메모리 솔루션이 점점 더 많이 요구되고 있습니다.

"2025년에는 우주 분야가 가장 큰 시장 점유율을 기록할 것으로 예측됩니다. "

내방사선 전자 부품은 다양한 우주 응용 분야에서 어려움을 극복하고 안정적인 작동을 보장하기 위해 특별히 설계되었습니다. 인공위성을 관리하는 온보드 컴퓨터의 핵심부터 로켓을 조종하는 유도 시스템까지, 이 견고한 부품들은 놀랍도록 다양한 작업에 전력을 공급합니다. 통신, 연료 효율, 과학적 데이터 수집, 먼 행성 표면에서의 복잡한 로봇 조종에 대응하고 있습니다. 또한, 우주선의 항법 시스템, 페이로드의 성능 모니터링, 우주 방사선에 노출된 상태에서의 비행 연속성 확보에도 필수적입니다. 위성 별자리, 유인 비행, 심우주 탐사 프로그램의 급속한 증가와 함께 방사선 내성 전자 부품은 민간 및 정부의 우주 활동에 필수적인 요소로 자리 잡았습니다.

"북미가 2030년 내방사선 전자제품 시장에서 가장 큰 점유율을 기록할 가능성이 높습니다. "

북미는 2030년 내방사선 전자제품 시장에서 가장 큰 점유율을 차지할 것입니다. 이 분야의 지속적인 기술 발전, 다양한 정부 우주 기관의 존재, 이 지역의 주요 시장 기업의 대다수 등이 이 지역의 내방사선 전자 부품의 성장 잠재력을 촉진하고 있습니다. 미국 정부는 내방사선 전자부품의 제조 능력을 지속적으로 향상시키기 위해 노력하고 있습니다. 또한, 활발한 국방 예산, 위성 별자리 투자 증가, NASA와 같은 정부 기관과 SpaceX, Northrop Grumman과 같은 비상장 항공우주 기업과의 협력 관계도 채용을 촉진하고 있습니다. 이 지역은 또한 잘 구축된 반도체 생태계, 광범위한 R&D 인프라, 차세대 ISR 및 미사일 방어 시스템에 대한 강력한 수요의 혜택을 누리고 있습니다.

세계의 내방사선 전자부품 시장에 대해 조사 분석했으며, 주요 성장 촉진요인과 억제요인, 경쟁 구도, 향후 동향 등의 정보를 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

내방사선성 전자부품 시장의 매력적인 기회

내방사선성 전자부품 시장 : 제품 유형별

내방사선성 전자부품 시장 : 제조 기술별

내방사선성 전자부품 시장 : 부품별

내방사선성 전자부품 시장 : 지역별

제5장 시장 개요

서론

시장 역학

성장 촉진요인

성장 억제요인

기회

과제

고객의 비즈니스에 영향을 미치는 동향/혼란

가격 결정 분석

주요 기업이 제공하는 파워 매니지먼트 제품 평균 판매 가격 : 부품 유형별(2024년)

A/D 및 D/A 컨버터 평균 판매 가격 : 주요 제조업체별(2024년)

프로세서 및 컨트롤러 평균 판매 가격 : 주요 기업별(2024년)

메모리 제품 평균 판매 가격 : 주요 기업별(2024년)

밸류체인 분석

생태계 분석

투자 및 자금조달 시나리오

기술 분석

주요 기술

보완 기술

인접 기술

Porter의 Five Forces 분석

주요 이해관계자와 구입 기준

사례 연구 분석

무역 분석

수입 시나리오(HS코드 8541)

수출 시나리오(HS코드 8541)

특허 분석

주요 컨퍼런스 및 이벤트(2025년-2026년)

규제 상황

규제기관, 정부기관 및 기타 조직

기준과 규제

내방사선성 전자부품 시장에 대한 AI의 영향

서론

주요 이용 사례와 시장 장래성

내방사선성 전자부품 시장에 대한 2025년 미국 관세의 영향

서론

주요 관세율

가격 영향 분석

국가/지역에 대한 영향

용도에 대한 영향

제6장 내방사선성 전자부품 재료와 포장 유형

서론

재료

실리콘

탄화규소(SiC)

질화갈륨(GaN)

갈륨비소(GaAs)

포장 유형

플립칩

세라믹 패키지

제7장 내방사선성 전자부품 시장 : 부품별

서론

혼합신호 ICS

프로세서 컨트롤러

메모리

전원 관리

기타 부품(정성)

제8장 내방사선성 전자부품 시장 : 제조 기술별

서론

RADIATION HARDENED BY DESIGN (RHBD)

RADIATION HARDENED BY PROCESS (RHBP)

RADIATION HARDENED BY SOFTWARE (RHBS) (QUALITATIVE)

제9장 내방사선성 전자부품 시장 : 제품 유형별

서론

COMMERCIAL-OFF-THE-SHELF

커스텀 메이드

제10장 내방사선성 전자부품 시장 : 용도별

서론

우주(위성)

항공우주 및 방위

원자력발전소

의료

기타 용도

제11장 내방사선성 전자부품 시장 : 지역별

서론

북미

북미의 거시경제 전망

미국

캐나다

멕시코

유럽

유럽의 거시경제 전망

영국

독일

프랑스

기타 유럽

아시아태평양

아시아태평양의 거시경제 전망

중국

인도

일본

한국

기타 아시아태평양

기타 지역

중동

남미

아프리카

제12장 경쟁 구도

개요

주요 시장 진출기업의 전략/강점(2019년-2025년)

매출 분석(2021년-2024년)

시장 점유율 분석(2024년)

기업 평가와 재무 지표

브랜드 비교

기업 평가 매트릭스 : 주요 기업(2024년)

기업 평가 매트릭스 : 스타트업/중소기업(2024년)

경쟁 시나리오

제13장 기업 개요

주요 기업

MICROCHIP TECHNOLOGY INC.

BAE SYSTEMS

RENESAS ELECTRONICS CORPORATION

INFINEON TECHNOLOGIES AG

STMICROELECTRONICS

ADVANCED MICRO DEVICES, INC.

TEXAS INSTRUMENTS INCORPORATED

HONEYWELL INTERNATIONAL INC.

TELEDYNE TECHNOLOGIES INCORPORATED

TTM TECHNOLOGIES INC.

기타 기업

THALES

ANALOG DEVICES, INC.

DATA DEVICE CORPORATION

3D PLUS

MERCURY SYSTEMS, INC.

PCB PIEZOTRONICS, INC.

VORAGO TECHNOLOGIES

GSI TECHNOLOGY, INC.

EVERSPIN TECHNOLOGIES INC

SEMICONDUCTOR COMPONENTS INDUSTRIES, LLC

AITECH

MICROELECTRONICS RESEARCH DEVELOPMENT CORPORATION

TRIAD SEMICONDUCTOR

ZERO ERROR SYSTEMS

RESILIENT COMPUTING

제14장 부록

LSH

영문 목차

영문목차

The global CST hardened electronics market is anticipated to grow from USD 1.77 billion in 2025 to USD 2.30 billion by 2030, at a CAGR of 5.4% during the forecast period. The market is experiencing steady growth as intelligence, surveillance, and reconnaissance (ISR) platforms, such as satellites, drones, and defense systems, increasingly rely on radiation-tolerant processors, controllers, memory devices, and mixed-signal ICs to ensure mission-critical performance in harsh environments.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Billion)

Segments

By Component, Manufacturing Technique, Product Type, Application, and Region

Regions covered

North America, Europe, APAC, RoW

Defense agencies and space organizations invest heavily in ISR capabilities to enhance situational awareness and secure communications, fueling the demand for reliable rad-hard components. However, high development costs and challenges in replicating real testing environments remain key restraints for the industry. At the same time, opportunities are emerging with the rise in global space missions and the adoption of commercial-off-the-shelf (COTS) components in satellites, while challenges such as customized requirements from high-end consumers continue to shape the competitive landscape.

"Memory segment is expected to grow at highest CAGR from 2025 to 2030"

Memory in the component segment is expected to grow at the fastest CAGR during the forecast period. A memory device is a hardware component that retains data, enabling communication or functionality. The memory products used for critical applications, such as spacecraft and nuclear weapons, need to be radiation-hardened to reduce the total ionizing dose (TID) received by the semiconductor components. Compute-intensive applications in the aerospace & space sector increasingly demand radiation-hardened memory solutions with high density and performance to handle large quantities of data obtained from various processor nodes and sensors.

"Space application is expected to record the largest market share in 2025"

Radiation-hardened electronics are specifically designed to weather the storm and ensure reliable operation across diverse space applications. From the beating heart of onboard computers managing satellites to the guidance systems steering rockets, these robust components power a remarkable range of tasks. They handle communication, fuel efficiency, scientific data collection, and complex robotic maneuvers on distant planetary surfaces. In addition, they are essential for navigation systems in spacecraft, monitoring payload performance, and ensuring mission continuity during exposure to cosmic radiation. With the rapid increase in satellite constellations, crewed missions, and deep-space exploration programs, radiation-hardened electronics are becoming indispensable for commercial and government space initiatives.

"North America is likely to register largest share of radiation hardened electronics market in 2030"

North America accounted for the largest share of the radiation hardened electronics market in 2030. Factors such as continuous technological advancements in this field, the presence of various government-owned space organizations, and a majority of the key market players in the region are driving the growth potential for radiation-hardened electronics in the region. The US government is continuously working on capabilities in manufacturing radiation hardened electronics. In addition, strong defense budgets, rising investments in satellite constellations, and collaborations between government agencies, such as NASA, and private aerospace companies, including SpaceX and Northrop Grumman, boost the adoption. The region also benefits from a well-established semiconductor ecosystem, extensive R&D infrastructure, and robust demand for next-generation ISR and missile defense systems.

Extensive primary interviews were conducted with key industry experts in the radiation hardened electronics market space to determine and verify the market size for various segments and subsegments gathered through secondary research. The breakdown of primary participants for the report is shown below.

The study contains insights from various industry experts, from component suppliers to Tier 1 companies and OEMs. The break-up of the primaries is as follows:

By Company Type: Tier 1 - 20%, Tier 2 - 25%, and Tier 3 - 55%

By Designation: C-level Executives - 30%, Directors - 30%, and Others - 40%

By Region: Asia Pacific - 30%, Europe - 20%, North America - 40%, and RoW - 10%

Note: Other designations include technology heads, media analysts, sales managers, marketing managers, and product managers.

The three tiers of companies are based on their total revenues as of 2024: Tier : >USD 1 billion, Tier 2: USD 500 million to 1 billion, and Tier 3: <USD 500 million.

The study includes an in-depth competitive analysis of these key players in the radiation hardened electronics market, with their company profiles, recent developments, and key market strategies.

Research Coverage:

The report describes detailed information regarding the key factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the radiation hardened electronics market. It also includes information like technology trends, trade data, and patent analysis. This research report categorizes the radiation hardened electronics market based on components, manufacturing techniques, product type, and region. A detailed analysis of the major industry players was carried out to provide insights into their business overviews, products offered, major strategies adopted that include new product launches, deals (acquisitions, partnerships, agreements, and contracts), and others (expansions), and AI/Gen AI impact on the radiation hardened electronics market.

Key Benefits of Buying the Report:

Analysis of key drivers (Increasing use of radiation-hardened electronics in space applications), restraints (Issues in creating real testing environment), opportunities (Favorable government initiatives and increasing space missions), and challenges (Customization required for high-end consumers)

Product development /Innovation: Detailed insights on growing technologies, research and development activities, and new product and service launches in the radiation hardened electronics market

Market Development: Comprehensive information about adjacent markets; the report analyses the radiation hardened electronics market across various geographies

Market Diversification: Exhaustive information about new products and services, untapped geographies, recent developments, and investments in the radiation hardened electronics market

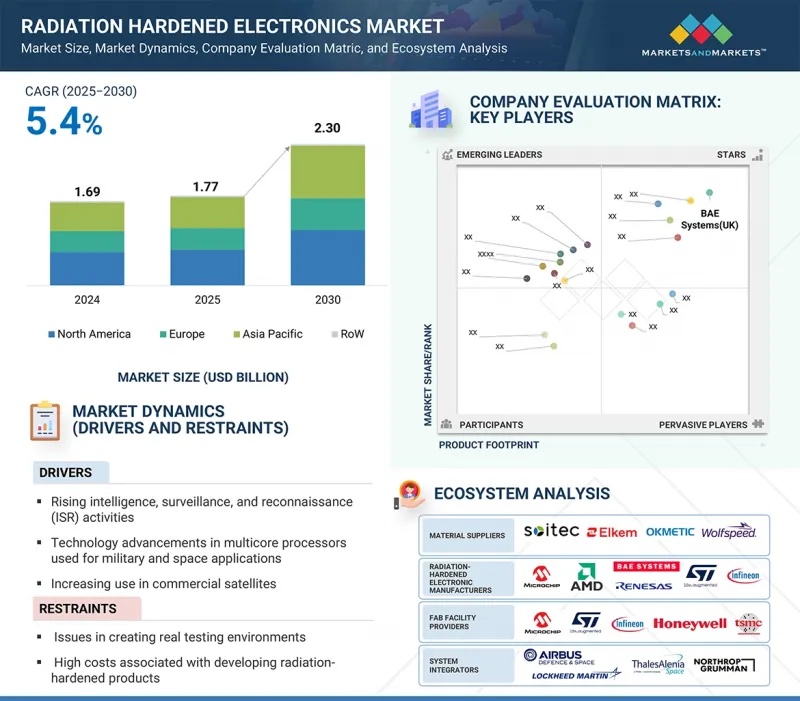

Competitive Assessment: In-depth assessment of market share, growth strategies, and services, offering of leading players, such as Microchip Technology Inc.(US), BAE Systems (UK), Renesas Electronics Corporation (Japan), Infineon Technologies AG (Germany), and STMicroelectronics (Switzerland), in the radiation hardened electronics market

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.2.1 MARKETS COVERED AND REGIONAL SCOPE

1.2.2 YEARS CONSIDERED

1.2.3 INCLUSIONS AND EXCLUSIONS

1.3 CURRENCY CONSIDERED

1.4 UNIT CONSIDERED

1.5 STAKEHOLDERS

1.6 LIMITATIONS

1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY AND PRIMARY RESEARCH

2.1.2 SECONDARY DATA

2.1.2.1 List of key secondary sources

2.1.2.2 Key data from secondary sources

2.1.3 PRIMARY DATA

2.1.3.1 List of primary interview participants

2.1.3.2 Key industry insights

2.1.3.3 Breakdown of primaries

2.1.3.4 Key data from primary sources

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.1.1 Approach to arrive at market size using bottom-up analysis (demand side)

2.2.2 TOP-DOWN APPROACH

2.2.2.1 Approach to arrive at market size using top-down analysis (supply side)

2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

2.4 RESEARCH ASSUMPTIONS

2.5 RESEARCH LIMITATIONS

2.6 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN RADIATION HARDENED ELECTRONICS MARKET

4.2 RADIATION HARDENED ELECTRONICS MARKET, BY PRODUCT TYPE

4.3 RADIATION HARDENED ELECTRONICS MARKET, BY MANUFACTURING TECHNIQUE

4.4 RADIATION HARDENED ELECTRONICS MARKET, BY COMPONENT

4.5 RADIATION HARDENED ELECTRONICS MARKET, BY GEOGRAPHY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Rising intelligence, surveillance, and reconnaissance (ISR) activities

5.2.1.2 Mounting demand for bandwidth, data processing, and memory components

5.2.1.3 Growing emphasis on affordable satellite communication

5.2.1.4 Increasing power generation from nuclear energy

5.2.2 RESTRAINTS

5.2.2.1 Issues in creating testing environments

5.2.2.2 High costs associated with developing radiation-hardened products

5.2.3 OPPORTUNITIES

5.2.3.1 Increasing global space missions

5.2.3.2 Rising demand for reconfigurable radiation-hardened electronics

5.2.3.3 Increasing use of commercial-off-the-shelf components in space satellites

5.2.4 CHALLENGES

5.2.4.1 Customization requirements from high-end consumers

5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.4 PRICING ANALYSIS

5.4.1 AVERAGE SELLING PRICE OF POWER MANAGEMENT PRODUCTS OFFERED BY KEY PLAYERS, BY COMPONENT TYPE, 2024

5.4.2 AVERAGE SELLING PRICE OF A/D & D/A CONVERTERS, BY KEY PLAYER, 2024

5.4.3 AVERAGE SELLING PRICE OF PROCESSORS & CONTROLLERS, BY KEY PLAYER, 2024

5.4.4 AVERAGE SELLING PRICE OF MEMORY PRODUCTS, BY KEY PLAYER, 2024

5.5 VALUE CHAIN ANALYSIS

5.6 ECOSYSTEM ANALYSIS

5.7 INVESTMENT AND FUNDING SCENARIO

5.8 TECHNOLOGY ANALYSIS

5.8.1 KEY TECHNOLOGIES

5.8.1.1 Radiation-hardened semiconductors

5.8.1.2 Rad-hard design techniques

5.8.1.3 Rad-hard packaging

5.8.2 COMPLEMENTARY TECHNOLOGIES

5.8.2.1 Radiation testing and simulation tools

5.8.2.2 Thermal management solutions

5.8.3 ADJACENT TECHNOLOGIES

5.8.3.1 Satellite and space systems

5.8.3.2 Defense electronics and avionics

5.8.3.3 Quantum and cryogenic electronics

5.9 PORTER'S FIVE FORCES ANALYSIS

5.9.1 INTENSITY OF COMPETITIVE RIVALRY

5.9.2 BARGAINING POWER OF SUPPLIERS

5.9.3 BARGAINING POWER OF BUYERS

5.9.4 THREAT OF SUBSTITUTES

5.9.5 THREAT OF NEW ENTRANTS

5.10 KEY STAKEHOLDERS AND BUYING CRITERIA

5.10.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.10.2 BUYING CRITERIA

5.11 CASE STUDY ANALYSIS

5.11.1 US DOD INVESTS IN SKYWATER TECHNOLOGY TO ADVANCE RADIATION-HARDENED TECHNOLOGY TO 90 MM PROCESS HARDENING TECHNIQUE

5.11.2 AAC MICROTEC AND TOHOKU UNIVERSITY INTEGRATE 4MBIT MRAM DEVICE FOR SATELLITES

5.11.3 ARMY CONTRACTING COMMAND INVESTS IN BAE SYSTEMS TO EXPEDITE DEVELOPMENT OF RHBD MICROELECTRONICS

5.11.4 NASA AND AIR FORCE RESEARCH LABORATORY CHOSE VORAGO TO PARTICIPATE IN RADIATION-HARDENED ELECTRONIC MEMORY EXPERIMENT

5.11.5 MERCURY SYSTEMS, INC. DEVELOPS 3U TRRUST-STOR VPX RT FOR TWO PROMINENT SUPPLIERS OF LOW EARTH ORBIT SATELLITES

5.12 TRADE ANALYSIS

5.12.1 IMPORT SCENARIO (HS CODE 8541)

5.12.2 EXPORT SCENARIO (HS CODE 8541)

5.13 PATENT ANALYSIS

5.14 KEY CONFERENCES AND EVENTS, 2025-2026

5.15 REGULATORY LANDSCAPE

5.15.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.15.2 STANDARDS AND REGULATIONS

5.16 IMPACT OF AI ON RADIATION HARDENED ELECTRONICS MARKET

5.16.1 INTRODUCTION

5.16.2 TOP USE CASES AND MARKET POTENTIAL

5.17 IMPACT OF 2025 US TARIFF ON RADIATION HARDENED ELECTRONICS MARKET

5.17.1 INTRODUCTION

5.17.2 KEY TARIFF RATES

5.17.3 PRICE IMPACT ANALYSIS

5.17.4 IMPACT ON COUNTRIES/REGIONS

5.17.4.1 US

5.17.4.2 Europe

5.17.4.3 Asia Pacific

5.17.5 IMPACT ON APPLICATIONS

6 RADIATION HARDENED ELECTRONIC MATERIALS AND PACKAGING TYPES

6.1 INTRODUCTION

6.2 MATERIALS

6.2.1 SILICON

6.2.2 SILICON CARBIDE (SIC)

6.2.3 GALLIUM NITRIDE (GAN)

6.2.4 GALLIUM ARSENIDE (GAAS)

6.3 PACKAGING TYPES

6.3.1 FLIP-CHIP

6.3.2 CERAMIC PACKAGES

7 RADIATION HARDENED ELECTRONICS MARKET, BY COMPONENT

7.1 INTRODUCTION

7.2 MIXED-SIGNAL ICS

7.2.1 A/D & D/A CONVERTERS

7.2.1.1 Increasing usage in space applications to bolster segmental growth

7.2.2 MULTIPLEXERS & RESISTORS

7.2.2.1 Rising need for data acquisition systems in space flights to augment segmental growth

7.3 PROCESSORS & CONTROLLERS

7.3.1 MPU

7.3.1.1 Mounting development of multicore processors for space & defense applications to fuel segmental growth

7.3.2 MCU

7.3.2.1 Widespread use in spacecraft subsystems to accelerate segmental growth

7.3.3 ASIC

7.3.3.1 Ability to address highly customized design requirements to contribute to segmental growth

7.3.4 FPGA

7.3.4.1 Use to eliminate costs related to electronic re-designing or manual updating to boost segmental growth

7.4 MEMORY

7.4.1 VOLATILE

7.4.1.1 DRAM

7.4.1.1.1 Low retention time and increased bandwidth to augment segmental growth

7.4.1.2 SRAM

7.4.1.2.1 High adoption in image processing applications in satellites to fuel segmental growth

7.4.2 NON-VOLATILE

7.4.2.1 MRAM

7.4.2.1.1 Ability to withstand effects of radiation and ionizing radiation in space to bolster segmental growth

7.4.2.2 Flash

7.4.2.2.1 Use to withstand extreme radiation to contribute to segmental growth

7.4.2.3 Other memory components

7.5 POWER MANAGEMENT

7.5.1 MOSFETS

7.5.1.1 Increasing adoption in outer space applications to foster segmental growth

7.5.2 DIODES

7.5.2.1 High voltage and improved electrical radiation performance to fuel segmental growth

7.5.3 THYRISTORS

7.5.3.1 Adoption in electronic converters for aerospace power systems to drive market

7.5.4 IGBTS

7.5.4.1 High current density and low power dissipation attributes to accelerate segmental growth

7.6 OTHER COMPONENTS (QUALITATIVE)

8 RADIATION HARDENED ELECTRONICS MARKET, BY MANUFACTURING TECHNIQUE

8.1 INTRODUCTION

8.2 RADIATION HARDENED BY DESIGN (RHBD)

8.2.1 ABILITY TO IMPROVE RELIABILITY OF ELECTRONIC COMPONENTS IN EXTREME ENVIRONMENTS TO FOSTER SEGMENTAL GROWTH

8.2.2 TOTAL IONIZING DOSE (TID)

8.2.3 SINGLE EVENT EFFECT (SEE)

8.3 RADIATION HARDENED BY PROCESS (RHBP)

8.3.1 LESS SENSITIVITY TO DEGRADING EFFECTS CAUSED BY RADIATION TO BOOST SEGMENTAL GROWTH

8.3.2 SILICON ON INSULATOR (SOI)

8.3.3 SILICON ON SAPPHIRE (SOS)

8.4 RADIATION HARDENED BY SOFTWARE (RHBS) (QUALITATIVE)

9 RADIATION HARDENED ELECTRONICS MARKET, BY PRODUCT TYPE

9.1 INTRODUCTION

9.2 COMMERCIAL-OFF-THE-SHELF

9.2.1 INCREASING ADOPTION IN COMMERCIAL AND MILITARY SATELLITES DUE TO LOW-COST BENEFITS TO DRIVE MARKET

9.3 CUSTOM-MADE

9.3.1 HIGH PREFERENCE IN DEFENSE MISSION-CRITICAL APPLICATIONS TO EXPEDITE SEGMENTAL GROWTH

10 RADIATION HARDENED ELECTRONICS MARKET, BY APPLICATION

10.1 INTRODUCTION

10.2 SPACE (SATELLITES)

10.2.1 COMMERCIAL

10.2.1.1 Widespread use of global positioning systems and navigation systems to contribute to segmental growth

10.2.1.2 Small satellites

10.2.1.3 New space

10.2.1.4 Nanosatellites

10.2.2 MILITARY

10.2.2.1 Requirement for high-quality components that withstand high levels of radiation to foster segmental growth

10.3 AEROSPACE & DEFENSE

10.3.1 WEAPONS & MISSILES

10.3.1.1 Deployment of reliable electronic components in defense applications to accelerate segmental growth

10.3.2 VEHICLES/AVIONICS

10.3.2.1 Focus on withstanding extreme radiation and temperature to contribute to segmental growth

10.4 NUCLEAR POWER PLANTS

10.4.1 EMPHASIS ON INCREASING POWER GENERATION TO AUGMENT SEGMENTAL GROWTH

10.5 MEDICAL

10.5.1 IMPLANTABLE MEDICAL DEVICES

10.5.1.1 Rapid technological advances to accelerate segmental growth

10.5.2 RADIOLOGY

10.5.2.1 Reliance of imaging techniques on ionizing radiation to fuel segmental growth

10.6 OTHER APPLICATIONS

11 RADIATION HARDENED ELECTRONICS MARKET, BY REGION

11.1 INTRODUCTION

11.2 NORTH AMERICA

11.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

11.2.2 US

11.2.2.1 Increasing space missions supported by government and private agencies to drive market

11.2.3 CANADA

11.2.3.1 Government initiatives related to space exploration to foster market growth

11.2.4 MEXICO

11.2.4.1 Expanding economy and commercial space satellite business to augment segmental growth

11.3 EUROPE

11.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

11.3.2 UK

11.3.2.1 Increasing government initiatives to support space sector to fuel market growth

11.3.3 GERMANY

11.3.3.1 Proliferation of national space programs to boost demand for radiation-hardened electronics

11.3.4 FRANCE

11.3.4.1 Rising partnerships in space industry to contribute to market growth

11.3.5 REST OF EUROPE

11.4 ASIA PACIFIC

11.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

11.4.2 CHINA

11.4.2.1 Increasing investment in military operations and technologies to accelerate market growth

11.4.3 INDIA

11.4.3.1 Growing focus on Earth observation, communication, and navigation satellites to drive market

11.4.4 JAPAN

11.4.4.1 Rise in funding for space programs to contribute to market growth

11.4.5 SOUTH KOREA

11.4.5.1 Increasing production of rockets to augment market growth

11.4.6 REST OF ASIA PACIFIC

11.5 ROW

11.5.1 MIDDLE EAST

11.5.1.1 Saudi Arabia

11.5.1.1.1 Ambitious space and defense initiatives to contribute to market growth

11.5.1.2 UAE

11.5.1.2.1 Expanding space program and strong focus on defense modernization to drive market

11.5.1.3 Rest of Middle East

11.5.2 SOUTH AMERICA

11.5.2.1 Growing support from foreign space agencies to fuel market growth

11.5.3 AFRICA

11.5.3.1 Increasing investment in satellite programs to accelerate market growth

12 COMPETITIVE LANDSCAPE

12.1 OVERVIEW

12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2019-2025

12.3 REVENUE ANALYSIS, 2021-2024

12.4 MARKET SHARE ANALYSIS, 2024

12.5 COMPANY VALUATION AND FINANCIAL METRICS

12.6 BRAND COMPARISON

12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

12.7.1 STARS

12.7.2 EMERGING LEADERS

12.7.3 PERVASIVE PLAYERS

12.7.4 PARTICIPANTS

12.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

12.7.5.1 Company footprint

12.7.5.2 Region footprint

12.7.5.3 Component footprint

12.7.5.4 Manufacturing technique footprint

12.7.5.5 Product type footprint

12.7.5.6 Application footprint

12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024