유럽의 전기자동차 배터리 재료 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Europe Electric Vehicle Battery Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1636274

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

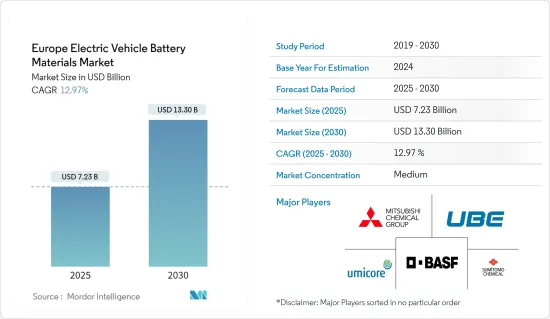

유럽의 전기자동차 배터리 재료 시장 규모는 2025년에 72억 3,000만 달러로 추정되며, 예측 기간(2025-2030년) 동안 12.97%의 CAGR로 2030년에는 133억 달러에 달할 것으로 예상됩니다.

주요 하이라이트

중기적으로는 전기자동차(EV) 판매 증가와 정부의 지원 정책 및 규제가 예측 기간 동안 전기자동차 배터리 재료의 수요를 촉진할 것으로 예상됩니다.

한편, 배터리 재료의 수입 의존도가 높아 공급망에 미치는 영향이 시장에 악영향을 미칠 가능성이 높습니다.

그러나 에너지 밀도 향상, 급속 충전, 안전성 향상, 수명 연장 등의 발전으로 배터리가 진화함에 따라 전기자동차 배터리 재료 시장에 진입하는 기업들에게 큰 기회가 될 것입니다.

전기자동차 도입 급증에 힘입어 독일은 유럽 전기자동차 배터리 재료 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다.

유럽의 전기자동차 배터리 재료 시장 동향

리튬이온 배터리 타입이 시장을 독점

전기자동차(EV)용 리튬이온 배터리 생산이 증가 추세에 있으며, 배터리 재료 시장에 큰 영향을 미치고 있습니다. 이러한 생산량의 급증은 리튬 수요를 증가시키고 있으며, 이 지역의 리튬 발견은 원료 비용에 큰 영향을 미치고 있습니다.

주요 시장 참여자들은 리튬이온 배터리 생산을 늘리고 배터리 원료의 수요 증가에 대응하기 위해 리튬 매장량 및 연구 개발에 투자하고 있습니다. 새로운 매장량이 발견됨에 따라 리튬이온 배터리의 가격은 장기적으로 하락하는 추세를 보이고 있습니다.

예를 들어, 2023년 전기자동차(EV) 및 배터리 에너지 저장 시스템(BESS)용 배터리 가격은 139달러/kWh까지 하락하여 13% 이상 하락했습니다. 지속적인 기술 혁신과 제조 개선으로 가격은 2025년까지 113달러/kWh까지 하락할 것으로 예상되며, 2030년에는 80달러/kWh까지 하락할 것으로 전망됩니다.

또한, 유럽 정부는 환경 문제에 대한 관심이 높아짐에 따라 EV용 리튬이온 배터리 생산을 적극적으로 추진하고 있습니다. 순 탄소 배출량 제로를 목표로 하는 이들 정부는 급증하는 전기자동차 수요에 대응하기 위해 리튬이온 배터리 생산을 촉진하는 여러 이니셔티브를 내놓고 있습니다.

예를 들어, 영국 정부는 2023년 11월 리튬이온 배터리를 포함한 배터리 공급망을 강화하기 위해 5,000만 파운드(6,300만 달러)를 투자한다고 발표했습니다. 배터리 전략은 무공해 차량과 그 공급망을 중점적으로 지원하며, 2030년까지 새로운 자본과 R&D 자금을 확대할 것을 약속했습니다. 이러한 이니셔티브는 청정에너지원으로서 리튬이온 배터리의 보급을 촉진하고 배터리 재료에 대한 수요를 증가시킬 것입니다.

또한, 리튬이온 배터리 가격이 하락하고 수요가 급증함에 따라 새로운 생산 공장의 설립은 배터리 원료의 필요성을 더욱 높이고 있습니다. 최근 몇 년 동안 리튬이온 배터리 생산 증대를 위한 투자가 크게 증가하고 있습니다.

예를 들어, 프랑스는 2024년 2월 민관합동으로 100억 유로(108억 4,000만 달러)를 투자하여 향후 몇 년 동안 전국에 리튬이온 배터리를 포함한 전기자동차 배터리 기가팩토리 4곳을 설립할 것이라고 발표했습니다. 이러한 전략적 투자로 프랑스 내 배터리 생산이 확대되고 이에 따라 리튬이온 배터리 재료에 대한 수요도 증가할 것으로 예상됩니다.

이러한 선진적인 노력으로 예측 기간 동안 리튬이온 배터리 생산이 크게 증가하여 EV용 배터리 재료에 대한 수요가 급증할 것으로 예상됩니다.

괄목할 만한 성장을 이룬 독일

독일은 자동차 산업과 지속가능한 모빌리티에 대한 노력으로 전기자동차(EV) 배터리 재료 부문에서 중요한 역할을 하고 있습니다. 지난 몇 년 동안 독일은 지역 전체에서 최고의 전기자동차 생산국이 되었습니다.

국제에너지기구(IEA)에 따르면 독일의 전기자동차(EV) 판매량은 2023년에 70만 대에 달할 것으로 예상되며, 이는 2022년의 수치와 동일하지만 2019년 대비 5.5배 증가한 수치입니다. 최근 유럽 정부가 내놓은 수많은 프로젝트와 이니셔티브로 인해 EV 판매는 향후 몇 년 동안 크게 성장할 태세를 갖추고 있습니다.

독일은 유럽에서 경쟁력 있는 지속가능한 배터리 셀 제조 가치사슬을 구축하고자 하는 유럽 배터리 얼라이언스에서 매우 중요한 역할을 담당하고 있습니다. 독일 정부는 주요 전기자동차 기업들과 긴밀히 협력하면서 국내 배터리 셀 생산 시설에 많은 투자를 하고 있습니다.

2024년 1월, 스웨덴의 리튬이온 배터리 제조업체인 노스볼트(Northvolt)는 9억 2천만 유로(9억 8,643만 달러)에 달하는 대규모 국가 지원책에 대한 유럽연합의 승인을 받았습니다. 이 자금은 독일 하이데(Heide)에 전기자동차 및 하이브리드 차량용 배터리 생산 공장을 설립하기 위한 것입니다. 이러한 움직임은 이 지역의 배터리 생산을 촉진하고 EV용 배터리 재료에 대한 수요를 증가시킬 것입니다.

독일은 첨단 배터리 및 재활용 기술을 선도하고 있습니다. 기업 및 연구기관 모두 폐배터리에서 리튬, 코발트, 니켈 등 귀중한 물질을 효율적으로 추출하는 방법을 혁신하고 있습니다.

2024년 5월, 폴란드의 ESM(Elemental Strategic Metals)은 미국의 스타트업 파트너인 Ascend Elements와 공동으로 리튬이온 배터리 재활용 공장 계획을 발표했습니다. 연간 2만 5,000톤의 생산능력으로 2024년 가을 건설, 2026년 가동을 목표로 하고 있습니다. 이 같은 벤처는 원료 생산을 촉진하고 EV용 배터리 재료의 생산량을 더욱 높일 수 있을 것으로 보입니다.

이러한 발전을 감안할 때, 예측 기간 동안 EV용 배터리 생산량이 증가하고 EV용 배터리 재료의 수요가 눈에 띄게 급증하는 궤도를 보일 것으로 예상됩니다.

유럽의 전기자동차 배터리 재료 산업 개요

유럽의 전기자동차 배터리 재료 시장은 상당히 세분화되어 있습니다. 주요 참여 기업(순서는 무관)으로는 BASF SE, Mitsubishi Chemical Group Corporation, UBE Corporation, Umicore, Sumitomo Chemical 등이 있습니다.

기타 혜택

엑셀 형식의 시장 예측(ME) 시트

3개월간 애널리스트 지원

목차

제1장 소개

조사 범위

시장 정의

조사 가정

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

소개

2029년까지 시장 규모와 수요 예측(단위 : 10억 달러)

최근 동향과 개발

정부 정책 및 규정

시장 역학

성장 촉진요인

전기자동차 판매 성장

정부 지원 정책 및 규정

성장 억제요인

수입 원료 공급에 대한 의존

공급망 분석

산업의 매력 - Porter's Five Forces 분석

공급 기업의 교섭력

소비자의 협상력

신규 참여업체의 위협

대체품의 위협 제품·서비스

경쟁 기업 간의 경쟁 관계

투자 분석

제5장 시장 세분화

배터리 유형

리튬이온 배터리

납축배터리

기타

재료

양극

음극

전해액

분리막

기타

지역

독일

프랑스

영국

이탈리아

스페인

러시아

터키

북유럽

기타 유럽

제6장 경쟁 구도

M&A, 합작투자, 제휴, 협정

주요 기업의 전략

기업 개요

Sumitomo Chemical Co., Ltd.

BASF SE

Mitsubishi Chemical Group Corporation

UBE Corporation

Umicore SA

Contemporary Amperex Technology Co. Limited

Johnson Matthey

ENTEK International LLC

Northvolt

SGL Carbon

기타 저명한 기업 리스트

시장 순위/점유율 분석

제7장 시장 기회와 향후 동향

배터리 기술의 진보

ksm

영문 목차

영문목차

The Europe Electric Vehicle Battery Materials Market size is estimated at USD 7.23 billion in 2025, and is expected to reach USD 13.30 billion by 2030, at a CAGR of 12.97% during the forecast period (2025-2030).

Key Highlights

Over the medium term, growing electric vehicle (EV) sales and supportive government policies and regulations are expected to drive the demand for electric vehicle battery materials during the forecast period.

On the other hand, the high import dependency on battery materials and the impact on the supply chain are likely to negatively impact the market.

However, as batteries evolve with advancements like enhanced energy density, quicker charging, heightened safety, and extended lifespans, significant opportunities emerge for players in the electric vehicle battery materials market.

Driven by a surge in electric vehicle adoption, Germany is poised to lead as the fastest-growing region in Europe's electric vehicle battery materials market.

Europe Electric Vehicle Battery Materials Market Trends

Lithium-Ion Battery Type Dominate the Market

The production of lithium-ion batteries for electric vehicles (EVs) is on the rise, significantly influencing the battery materials market. This surge in production has driven up the demand for lithium, and discoveries of lithium in the region are notably affecting raw material costs.

Key market players are channeling investments into lithium reserves and R&D, aiming to boost lithium-ion battery production and meet the growing demand for battery raw materials. As new reserves are discovered, the prices of lithium-ion batteries have seen a downward trend over time.

For instance, in 2023, battery prices for electric vehicles (EVs) and battery energy storage systems (BESS) dropped to USD 139/kWh, marking a decline of over 13%. With ongoing technological innovations and manufacturing improvements, projections suggest prices will further dip to USD 113/kWh by 2025 and reach USD 80/kWh by 2030.

Moreover, European governments are actively promoting lithium-ion battery production for EVs, driven by mounting environmental concerns. With a keen focus on achieving net-zero carbon emissions, these governments have launched multiple initiatives to boost lithium-ion battery production, aiming to meet the surging EV demand.

For instance, in November 2023, the United Kingdom government unveiled a GBP 50 million (USD 63 million) investment to fortify its battery supply chain, including lithium-ion batteries, aligning with the nation's future EV production goals. The Battery Strategy promises focused support for zero-emission vehicles and their supply chains, with new capital and R&D funding extending to 2030. Such initiatives are poised to bolster the adoption of lithium-ion batteries as a clean energy source, subsequently driving up the demand for battery materials.

Additionally, as lithium-ion battery prices decline and demand surges, the establishment of new production plants further fuels the need for battery raw materials. Recent years have witnessed a significant uptick in investments aimed at boosting lithium-ion battery production.

For instance, in February 2024, France unveiled a EUR 10 billion (USD 10.84 billion) investment, sourced from both public and private entities, to establish four gigafactories for electric vehicle batteries, including lithium-ion variants, across the nation in the upcoming years. Such strategic investments are set to amplify battery production in France, subsequently heightening the demand for lithium-ion battery materials.

Given these advancements and initiatives, a marked increase in lithium-ion battery production and a surge in demand for EV battery materials are anticipated during the forecast period.

Germany to Witness Significant Growth

Germany plays a significant role in the electric vehicle (EV) battery materials sector, driven by its automotive industry and commitment to sustainable mobility. In the past few years, the country has become one of the leading EV producers across the region.

According to the International Energy Agency (IEA), Electric vehicle (EV) sales in Germany reached 0.7 million units in 2023, consistent with 2022 figures but marking a 5.5-fold increase since 2019. With numerous projects and initiatives recently launched by the European government, EV sales are poised for significant growth in the coming years.

Germany plays a pivotal role in the European Battery Alliance, which aims to establish a competitive and sustainable battery cell manufacturing value chain in Europe. Collaborating closely with leading EV companies, the German government is making substantial investments in domestic battery cell production facilities.

In January 2024, Northvolt, a Swedish lithium-ion battery manufacturer, secured European Union approval for a significant EUR 902 million (USD 986.43 million) state aid package. This funding is earmarked for establishing an EV and hybrid vehicle battery production plant in Heide, Germany. Such moves are set to boost battery production in the region, driving up demand for EV battery materials.

Germany is leading the charge in advanced battery recycling technologies. Both companies and research institutions are innovating efficient methods to extract valuable materials, such as lithium, cobalt, and nickel, from used batteries.

In May 2024, Elemental Strategic Metals (ESM), a Polish firm, in collaboration with its US start-up partner Ascend Elements, unveiled plans for a lithium-ion battery recycling plant. With a capacity of 25,000 tonnes per year, construction is slated for autumn 2024, aiming for operational status by 2026. Such ventures are set to boost raw material production, further elevating the output of EV battery materials.

Given these developments, the trajectory points towards heightened battery production for EVs and a marked surge in demand for EV battery materials in the forecast period.

Europe Electric Vehicle Battery Materials Industry Overview

Europe's electric vehicle battery materials market is moderately fragmented. Some key players (not in particular order) are BASF SE, Mitsubishi Chemical Group Corporation, UBE Corporation, Umicore, Sumitomo Chemical Co., Ltd., among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD billion, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Growing Electric Vehicle Sales

4.5.1.2 Supportive Government Policies and Regulations

4.5.2 Restraints

4.5.2.1 Dependency on Imported Raw Material Supply

4.6 Supply Chain Analysis

4.7 Industry Attractiveness - Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

4.8 Investment Analysis

5 MARKET SEGMENTATION

5.1 Battery Type

5.1.1 Lithium-ion Battery

5.1.2 Lead-Acid Battery

5.1.3 Others

5.2 Material

5.2.1 Cathode

5.2.2 Anode

5.2.3 Electrolyte

5.2.4 Separator

5.2.5 Others

5.3 Geography

5.3.1 Germany

5.3.2 France

5.3.3 United Kingdom

5.3.4 Italy

5.3.5 Spain

5.3.6 Russia

5.3.7 Turkey

5.3.8 NORDIC

5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements