전기자동차 배터리 재료 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Electric Vehicle Battery Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1636235

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

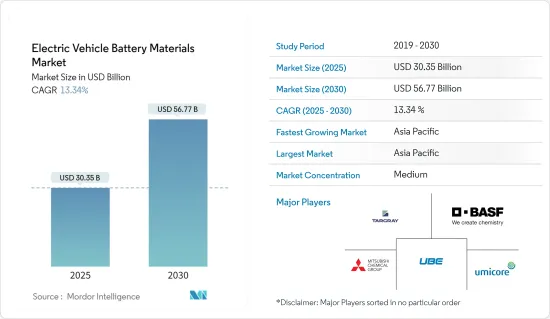

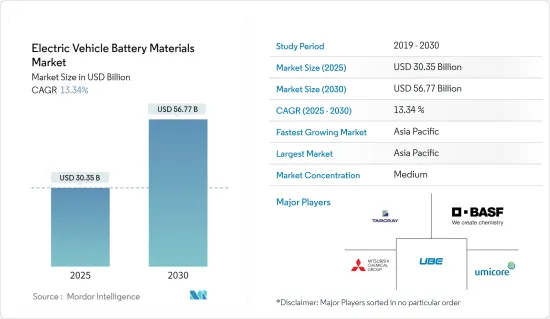

전기자동차 배터리 재료의 시장 규모는 2025년 303억 5,000만 달러로 예측되며, 예측 기간(2025-2030년) 동안 13.34%의 CAGR로 2030년에는 567억 7,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

중기적으로는 전기자동차의 보급 확대와 리튬이온 배터리의 저가화가 예측 기간 동안 시장을 견인할 것으로 보입니다.

한편, 일부 국가의 독점으로 인한 배터리 재료 공급망 격차가 향후 시장 성장을 억제할 것으로 예상됩니다.

그러나 보다 지속가능한 양극 및 음극과 효율적인 전해액을 위한 다양한 배터리 재료에 대한 연구와 발전은 시장 성장의 기회를 제공할 수 있습니다.

아시아태평양이 시장을 독점하고 있는 이유는 전기자동차 산업에서의 적용이 확대되고 있으며, 이는 배터리 재료에 대한 수요를 증가시키고 있기 때문입니다.

전기자동차 배터리 재료 시장 동향

리튬이온 배터리가 큰 비중을 차지할 것으로 예상

전기자동차에 사용되는 리튬이온 배터리 재료는 배터리 양극에 리튬 금속 산화물(Li(NixMnyCoz)O2, LiMn2O4, LiCoO2 등), 올리빈(LiFePO4 등), 바나듐 산화물, 이차 리튬 산화물 등을 포함합니다. 음극에 사용되는 재료에는 리튬 합금 재료, 흑연, 실리콘, 금속간 화합물 등이 있습니다.

리튬 배터리 재료에 대한 수요는 리튬이온 배터리 팩의 가격 하락과 높은 에너지 밀도, 상대적으로 긴 사이클 수명, 효율성 등 여러 가지 장점으로 인해 전기자동차에서 증가하고 있습니다.

2023년 리튬이온 배터리 팩의 가격은 전년 대비 약 13% 하락한 139달러/kWh가 될 것입니다. 이러한 장점에 더해, 전기자동차에 더 효과적이고 효율적인 리튬 배터리 재료를 생산하기 위한 연구 개발이 진행되고 있습니다.

예를 들어, 2024년 2월 인천대학교 과학자들은 리튬이온 배터리 분리막의 안정성과 특성을 향상시키는 방법을 고안했습니다. 이산화 규소 및 기타 기능성 분자의 층을 통합하여 이를 달성했습니다. 이러한 개발은 전기자동차 응용 분야에서 리튬 이온 분리막의 기능성을 향상시킬 수 있을 것으로 기대됩니다.

또한, 리튬 이온 전기자동차의 수요 증가에 따라 여러 기업들이 리튬 이온 전기자동차 배터리 생산에 투자하고 있어 리튬이온 배터리 재료에 대한 수요 증가가 예상됩니다. 예를 들어, 캔자스주 데소토에 위치한 파나소닉의 차량용 배터리 공장은 2025년까지 전기자동차용 2170개의 리튬이온 배터리를 증산할 것으로 예상됩니다. 이러한 목표는 향후 리튬 배터리 재료에 긍정적인 환경이 조성될 것임을 시사합니다.

이와 같이, 리튬이온 배터리 가격 하락과 기술 개발 등의 요인으로 인해 리튬이온 배터리 재료의 수요는 예측 기간 동안 증가할 것으로 예상됩니다.

아시아태평양이 시장을 독점할 것으로 예상

아시아태평양은 특히 중국에서 배터리 수요와 생산의 대부분을 차지하고 있기 때문에 전기자동차 배터리 재료 시장을 독점할 것으로 예상됩니다. 중국의 배터리 생산은 전기자동차 배터리 수요의 대부분을 충족시키고 있습니다.

국제에너지기구(IEA)에 따르면 2023년 중국의 전기자동차 배터리 수요는 417GWh로 지난해 314GWh보다 증가했습니다. 유럽은 185GWh, 미국은 99GWh입니다. 이처럼 전기자동차 배터리 수요 증가가 중국의 생산량 증가로 이어지고 있으며, 예측 기간 동안 전기자동차 배터리 재료의 수요가 증가할 것으로 예상됩니다.

또한, 중국은 세계 최대의 전기자동차 배터리 수출국이며, 2023년에는 전기자동차 배터리의 약 12%를 수출할 예정입니다. 중국은 배터리 재료의 대부분을 국내에서 생산하고 있어 전기자동차 배터리 제조를 위한 공급망이 보다 통합적이고 지속가능합니다.

또한, 2023년 기준 중국은 전 세계 양극활물질 생산능력의 거의 90%, 음극활물질 생산능력의 97% 이상을 차지할 것으로 예상됩니다. 한국은 주목할 만한 9%의 점유율을 차지하며, 일본이 3%로 그 뒤를 이어 양극 활물질 부문에서 중국 외의 유일한 중요한 진입자가 될 것입니다.

이 지역은 투자와 정부 지원의 증가로 인해 전기자동차 배터리 재료 시장에서 크게 성장할 것으로 예상됩니다. 예를 들어, 중국은 2024년 5월 전기자동차에 전력을 공급하는 차세대 배터리 기술 개발에 8억 4,500만 달러를 투자할 것이라고 발표했습니다. 이러한 투자는 예측 기간 동안 전기자동차 배터리 재료에 대한 수요를 증가시킬 것으로 예상됩니다.

따라서 위와 같은 발전으로 아시아태평양이 시장을 독점할 것으로 예상됩니다.

전기자동차 배터리 재료 산업 개요

전기자동차 배터리 재료 시장은 반분할되어 있습니다. 이 시장의 주요 기업으로는 Targray Technology International Inc., BASF SE, Mitsubishi Chemical Group Corporation, UBE Corporation, Umicore 등이 있습니다.

기타 혜택

엑셀 형식의 시장 예측(ME) 시트

3개월간 애널리스트 지원

목차

제1장 소개

조사 범위

시장 정의

조사 가정

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

소개

2029년까지 시장 규모와 수요 예측(단위 : 달러)

최근 동향과 개발

정부 정책 및 규정

시장 역학

성장 촉진요인

전기자동차 보급 확대

리튬이온 배터리 가격 하락

성장 억제요인

공급망 격차

공급망 분석

산업의 매력 - Porter's Five Forces 분석

공급 기업의 교섭력

소비자의 협상력

신규 참여업체의 위협

대체품의 위협 제품·서비스

경쟁 기업 간의 경쟁 관계

투자 분석

제5장 시장 세분화

배터리 유형

리튬이온

납축배터리

기타

재료

음극

양극

분리막

전해액

기타

2029년까지 시장 규모·수요 예측(지역별)

북미

미국

캐나다

기타 북미

유럽

독일

프랑스

영국

이탈리아

스페인

북유럽

러시아

터키

기타 유럽

아시아태평양

중국

인도

호주

일본

한국

말레이시아

태국

인도네시아

베트남

기타 아시아태평양

중동 및 아프리카

사우디아라비아

아랍에미리트

나이지리아

이집트

카타르

남아프리카공화국

기타 중동 및 아프리카

남미

브라질

아르헨티나

콜롬비아

기타 남미

제6장 경쟁 구도

M&A, 합작투자, 제휴, 협정

주요 기업의 전략

기업 개요

Targray Technology International Inc.

BASF SE

Mitsubishi Chemical Group Corporation

UBE Corporation

Umicore

Sumitomo Chemical Co. Ltd

Nichia Corporation

ENTEK International LLC

Arkema SA

Kureha Corporation

기타 저명한 기업 리스트

시장 순위 분석

제7장 시장 기회와 향후 동향

기타 배터리 재료 연구개발 증가

ksm

영문 목차

영문목차

The Electric Vehicle Battery Materials Market size is estimated at USD 30.35 billion in 2025, and is expected to reach USD 56.77 billion by 2030, at a CAGR of 13.34% during the forecast period (2025-2030).

Key Highlights

Over the medium period, the growing adoption of electric vehicles and the decreasing price of lithium-ion batteries are expected to drive the market during the forecast period.

On the other hand, the supply chain gap in battery materials created by the monopoly of some countries is expected to restrain market growth in the future.

However, the ongoing research and advancement in different battery materials for more sustainable cathode and anode, as well as efficient electrolytes, may offer opportunities for market growth.

Asia-Pacific dominates the market, owing to the growing application in the electric vehicle industry, which augments the demand for battery material.

Electric Vehicle Battery Materials Market Trends

Lithium-ion Battery is Expected to Have a Major Share

Lithium-ion battery materials used in electric vehicles include batteries cathode include lithium-metal oxides (such as Li(NixMnyCoz)O2, LiMn2O4, and LiCoO2), olivines (such as LiFePO4), vanadium oxides, and rechargeable lithium oxides. The materials used in anodes include lithium-alloying materials, graphite, silicon, or intermetallics.

The demand for lithium battery materials is increasing in electric vehicles owing to the decreasing price of lithium-ion battery packs and several advantages such as high energy density, relatively long cycle life, and efficiency.

In 2023, the price of lithium-ion battery packs decreased by around 13% compared to the previous year to USD 139/kWh. In addition to these advantages, research and development are being conducted to manufacture more effective and efficient lithium battery materials for electric vehicles.

For instance, in February 2024, scientists at the Incheon National University devised a method to enhance the stability and characteristics of lithium-ion battery separators. They achieved this by incorporating a layer of silicon dioxide and other functional molecules. Such developments will improve the functionality of lithium-ion separators in electric vehicle applications.

Further, with the increasing demand for lithium-ion electric vehicles, several companies are investing in manufacturing lithium-ion electric vehicle batteries, and the demand for lithium-ion battery materials is expected to increase. For instance, Panasonic's automotive battery plant in De Soto, Kansas, is expected to increase production of the 2170 cylindrical lithium-ion batteries for electric vehicles by 2025. Such an aim depicts a positive environment for lithium battery materials in the future.

Thus, owing to the factors mentioned above, such as the decreasing price of lithium-ion batteries and technological developments, the demand for lithium-ion battery materials is expected to be significant during the forecast period.

Asia-Pacific is Expected to Dominate the Market

Asia-Pacific is expected to dominate the electric vehicle battery materials market for electric vehicles, as the region accounts for the majority of battery demand and production, especially in China. China's battery production fulfills the majority of the demand for electric vehicle batteries.

According to the International Energy Agency, in 2023, the demand for electric vehicle batteries in China accounted for 417 GWh, up from 314 GWh last year. Europe produced 185 GWh, and the United States produced 99 GWh in 2023. Thus, the increasing demand for electric vehicle batteries is leading China to produce more, and the demand for electric vehicle battery materials is expected to rise during the forecast period.

Further, China is the world's largest exporter of electric vehicle batteries, with around 12% of its electric vehicle batteries exported in 2023. The country has a more integrated and sustainable supply chain for manufacturing electric vehicle batteries due to the majority of battery materials being produced domestically.

Moreover, as of 2023, China accounted for almost 90% of the world's cathode-active material manufacturing capacity and over 97% of anode-active material production. Korea holds a notable 9% share, with Japan following at 3%, making them the only significant players outside China in the cathode active material segment.

The region is expected to grow significantly in the electric vehicle battery materials market due to the increasing investments and government support. For instance, in May 2024, China announced it would invest USD 845 million in developing next-generation battery technology that powers electric vehicles. Such investments will boost the demand for electric vehicle battery material during the forecast period.

Thus, owing to the above-mentioned developments, Asia-Pacific is expected to dominate the market.

Electric Vehicle Battery Materials Industry Overview

The electric vehicle battery materials market is semi-fragmented. Some of the major players in the market (in no particular order) include Targray Technology International Inc., BASF SE, Mitsubishi Chemical Group Corporation, UBE Corporation, and Umicore.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 The Growing Adoption of Electric Vehicles

4.5.1.2 Decreasing Price of Lithium-ion Batteries

4.5.2 Restraints

4.5.2.1 The Supply Chain Gap

4.6 Supply Chain Analysis

4.7 Industry Attractiveness - Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

4.8 Investment Analysis

5 MARKET SEGMENTATION

5.1 Battery Type

5.1.1 Lithium-ion

5.1.2 Lead-acid

5.1.3 Other Battery Types

5.2 Material

5.2.1 Anode

5.2.2 Cathode

5.2.3 Separator

5.2.4 Electrolyte

5.2.5 Other Materials

5.3 Geography [Market Size and Demand Forecast till 2029 (for regions only)]

5.3.1 North America

5.3.1.1 United States

5.3.1.2 Canada

5.3.1.3 Rest of North America

5.3.2 Europe

5.3.2.1 Germany

5.3.2.2 France

5.3.2.3 United Kingdom

5.3.2.4 Italy

5.3.2.5 Spain

5.3.2.6 NORDIC

5.3.2.7 Russia

5.3.2.8 Turkey

5.3.2.9 Rest of Europe

5.3.3 Asia-Pacific

5.3.3.1 China

5.3.3.2 India

5.3.3.3 Australia

5.3.3.4 Japan

5.3.3.5 South Korea

5.3.3.6 Malaysia

5.3.3.7 Thailand

5.3.3.8 Indonesia

5.3.3.9 Vietnam

5.3.3.10 Rest of Asia-Pacific

5.3.4 Middle East and Africa

5.3.4.1 Saudi Arabia

5.3.4.2 United Arab Emirates

5.3.4.3 Nigeria

5.3.4.4 Egypt

5.3.4.5 Qatar

5.3.4.6 South Africa

5.3.4.7 Rest of Middle East and Africa

5.3.5 South America

5.3.5.1 Brazil

5.3.5.2 Argentina

5.3.5.3 Colombia

5.3.5.4 Rest of South America

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 Targray Technology International Inc.

6.3.2 BASF SE

6.3.3 Mitsubishi Chemical Group Corporation

6.3.4 UBE Corporation

6.3.5 Umicore

6.3.6 Sumitomo Chemical Co. Ltd

6.3.7 Nichia Corporation

6.3.8 ENTEK International LLC

6.3.9 Arkema SA

6.3.10 Kureha Corporation

6.4 List of Other Prominent Companies

6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 The Increasing Research and Development of Other Battery Materials