북미의 전기자동차(EV)배터리 재료 시장 전망 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

North America Electric Vehicle Battery Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1636270

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

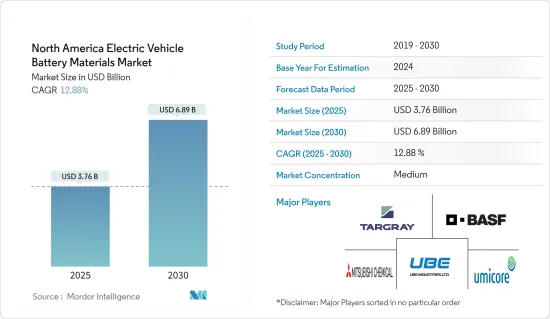

북미의 EV 배터리 재료 시장 규모는 2025년 37억 6,000만 달러로 추정되며, 예측기간(2025-2030년)의 연평균 성장율(CAGR)은 12.88%로, 2030년에는 68억 9,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

향후 수년간 북미의 EV 배터리 재료 시장은 전기차 판매의 급증과 정부 정책과 규제 강화에 의해 크게 주도될 전망입니다.

반대로 북미 전기 자동차 배터리 재료 시장은 국내 원자재 생산 부족으로 인한 수입 의존도가 높아 어려움에 직면해 있습니다.

그럼에도 불구하고 첨단 배터리 기술을 개발하기위한 노력은 계속되고 있습니다. 이 요인은 향후 시장에 몇 가지 기회를 만들 것으로 예상됩니다.

강력한 자동차 제조 및 판매 산업을 갖춘 미국은 예측 기간 동안 가장 높은 성장률을 기록하면서 성장 환경을 지배 할 것으로 예상됩니다.

북미의 EV 배터리 재료 시장 동향

리튬 이온 배터리가 시장을 독점

리튬 이온 배터리 부문은 북미 전기 자동차(EV) 배터리 재료 시장의 초석으로, 전기 자동차 기술의 성장과 발전에서 중추적인 역할을 하는 것이 특징입니다. 전기 자동차에 가장 널리 채택된 배터리 유형인 리튬 이온 배터리는 에너지 밀도, 효율성 및 수명이 유리하게 조합되어 있어 최신 전기차용에 없어서는 안 될 필수 요소입니다.

지난 10년간 배터리 기술과 제조 공정이 크게 발전하면서 전기 자동차 시장에서 리튬 이온 배터리의 채택이 가속화되었습니다. 이러한 발전은 비용을 절감했을 뿐만 아니라 성능과 신뢰성을 강화하여 리튬 이온 배터리를 제조업체와 소비자 모두에게 점점 더 매력적으로 만들었습니다.

최근 몇 년 동안 리튬 이온 배터리와 셀 팩의 가격이 하락세를 보이면서 최종 사용자 산업에서 리튬 이온 배터리의 매력은 더욱 커지고 있습니다. 2022년에 약간의 가격 인상을 경험한 배터리 가격은 2023년에 다시 한 번 하락세로 돌아섰습니다. 리튬 이온 배터리 팩의 가격은 14% 하락하여 사상 최저치인 139달러/kWh를 기록했습니다.

이 부문에는 배터리의 전반적인 성능과 기능에 기여하는 다양한 소재가 포함됩니다. 이러한 소재는 배터리의 에너지 밀도, 사이클 수명 및 열 안정성을 향상시켜 자동차 산업에서 요구하는 중요한 성능 매개변수를 해결하는 능력 때문에 선택됩니다. 예를 들어 니켈이 풍부한 양극재는 높은 에너지 용량으로 특히 선호되며, 이는 소비자 채택과 시장 경쟁력의 필수 요소인 전기 자동차의 주행 거리 연장으로 직결됩니다.

아시아 지역의 전기자동차에 대한 선호도가 높아지면서 리튬 이온 배터리에 대한 수요가 눈에 띄게 급증하고 있습니다. 이에 따라 배터리 제조업체와 조립업체들은 배터리 소재 생산 시설에 투자를 집중하고 있습니다. 이러한 전략적 움직임은 국내 및 국제적으로 증가하는 리튬 배터리에 대한 수요를 충족하기 위한 것입니다. 또한 배터리 기술의 발전은 이러한 수요를 더욱 촉진하고 있습니다. 전기 자동차 보급이 증가함에 따라 시장은 지속적으로 성장할 것으로 예상됩니다.

예를 들어, 2023년 10월, EV 배터리 재료의 중요한 선수인 유미코어는 CAM 공장과 pCAM 공장의 설립으로 캐나다 온타리오 주에서의 존재감을 확고히 하고 있습니다. 이 회사는 급성장하는 북미 전기자동차(EV) 시장에 대응하기 위해 온타리오주 로얄리스트에 35GWh의 배터리 재료 생산 시설을 적극적으로 건설하고 있습니다.

유미코어는 이 공장이 지역 전기자동차 공급망을 강화하고 전기자동차 배터리의 전반적인 상황을 강화하는 데 매우 중요한 역할을 한다는 것을 인식하고 캐나다 정부와 온타리오 주 정부 모두에서 엄청난 자금 지원을 확보하고 있습니다.

따라서 위에서 언급했듯이 예측 기간 동안 리튬 이온 배터리 분야가 시장을 독점할 것으로 예상됩니다.

상당한 성장을 이루는 미국

미국에서는 소비자 선호도, 환경 인식 및 온실 가스 배출을 줄이기위한 규제 압력의 조합으로 인해 전기 자동차에 대한 수요가 견고하게 증가하고 있습니다. 전기 자동차 구매에 대한 세금 공제 및 리베이트와 같은 연방 및 주 차원의 인센티브는 전기 자동차의 도입을 가속화하는 데 중요한 역할을 합니다.

2024년에는 최대 7,500달러의 세금 공제 혜택을 받을 수 있으며, 중고 전기 자동차 구매자는 최대 4,000달러를 받을 수 있는 재정적 인센티브를 받을 수 있습니다. 올해 주목할 만한 변화는 소비자가 이 세액공제를 적격 딜러에게 양도하여 차량 구매 시 즉시 할인을 받을 수 있다는 점입니다.

이러한 우대 조치는 소비자가 전기차를 더 저렴하게 구매할 수 있도록 할 뿐만 아니라 첨단 배터리 기술 및 소재에 대한 수요를 촉진합니다. 또한 2050년까지 탄소 배출량 제로를 달성하겠다는 미국 행정부의 의지와 전기자동차 충전 네트워크 및 청정에너지 노력에 대한 상당한 투자를 포함하는 인프라 법안은 전기자동차 시장을 더욱 활성화하고 결과적으로 배터리 소재에 대한 수요를 촉진할 것으로 예상됩니다.

이러한 우대조치는 국내 전기 자동차 보급에 박차를 가하고 있습니다. 특히, 국제에너지기구는 지난 10년간 전기 자동차 채택이 꾸준히 증가했다고 보고했습니다. 특히 2022년부터 2023년까지 배터리 전기 자동차 판매량은 37.5% 이상 급증했습니다. 지난 5년간의 연평균 성장률이 71.6%에 달했다는 점을 고려하면 이러한 성장세는 더욱 두드러집니다. 이러한 수치는 전기 자동차에 대한 관심이 높아지면서 국내 배터리 수요도 증가하고 있음을 보여줍니다.

국내 배터리 제조 역량에 대한 상당한 투자도 미국 부문의 특징입니다. 해외 공급망에 대한 의존도를 낮추는 것이 전략적으로 중요하다는 점을 인식한 민간 기업과 정부 기관 모두 현지 배터리 제조 시설 개발에 막대한 투자를 하고 있습니다. 테슬라, 제너럴 모터스, 현대, 포드 등 기업들은 리튬 이온 배터리를 대규모로 생산하는 기가팩토리를 설립하기 위한 노력의 선두에 서 있습니다.

예를 들어 2023년 4월, 두 개의 유명 자동차 제조업체가 미국에 전기 자동차(EV) 배터리 공장을 건설할 계획을 발표하면서 미국 내 전기 자동차 제조가 지속적으로 빠르게 성장하고 있음을 강조했습니다. 제너럴 모터스는 삼성SDI와 협력하여 미국 내 전기차 배터리 공장에 30억 달러를 공동 투자한다고 밝혔습니다. 이와 동시에 현대자동차는 한국의 배터리 제조업체 SK온과 파트너십을 맺고 조지아주에 배터리 공장을 설립하기 위해 50억 달러를 투자한다고 밝혔습니다.

이 시설은 첨단 제조 기술과 자동화를 활용하여 생산 효율성을 높이고 비용을 절감하며 국내 시장에 고품질 배터리를 안정적으로 공급하는 것을 목표로 합니다.

따라서 앞서 언급했듯이 미국은 예측 기간 동안 큰 성장을 이룰 것으로 예상됩니다.

북미의 EV 배터리 재료 산업 개요

북미의 EV 배터리 재료 시장은 적당히 세분화되어 있습니다. 이 시장의 주요 기업(특정한 순서 없음)은 Targray Technology International Inc., BASF SE, Mitsubishi Chemical Group Corporation, UBE Corporation, Umicore입니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

소개

2029년까지 시장 규모 및 수요 예측(단위 : 달러)

최근 동향과 개발

정부의 규제와 정책

시장 역학

성장 촉진요인

전기자동차 판매의 성장

정부의 지원 정책과 정책

억제요인

수입원재료 공급에 의존

공급망 분석

업계의 매력도 - Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협 제품 및 서비스

경쟁 기업간 경쟁 관계

투자 분석

제5장 시장 세분화

배터리 유형별

리튬 이온 배터리

납축 배터리

기타

재료별

음극

애노드

전해액

세퍼레이터

기타

지역별

미국

캐나다

기타 북미

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 프로파일

Targray Technology International Inc.

BASF SE

Mitsubishi Chemical Group Corporation

UBE Corporation

Umicore

Sumitomo Chemical Co., Ltd.

Nichia Corporation

ENTEK International LLC

Arkema SA

Kureha Corporation

기타 저명한 기업 리스트

시장 순위 및 점유율 분석

제7장 시장 기회와 앞으로의 동향

배터리 기술의 진보

HBR

영문 목차

영문목차

The North America Electric Vehicle Battery Materials Market size is estimated at USD 3.76 billion in 2025, and is expected to reach USD 6.89 billion by 2030, at a CAGR of 12.88% during the forecast period (2025-2030).

Key Highlights

In the coming years, the North America Electric Vehicle Battery Materials Market is poised to be significantly driven by surging electric vehicle sales and bolstering government policies and regulations.

Conversely, the North America Electric Vehicle Battery Materials Market faces challenges due to a heavy dependence on imports, stemming from insufficient domestic raw material production.

Nevertheless, continued efforts are being made to develop advanced battery technology. This factor is expected to create several opportunities for the market in the future.

With a robust vehicle manufacturing and sales industry, the United States is set to dominate the growth landscape, likely registering the highest expansion during the forecast period.

North America Electric Vehicle Battery Materials Market Trends

Lithium-ion Batteries to Dominate the Market

The lithium-ion battery segment is a cornerstone of the North American electric vehicle (EV) battery materials market, characterized by its pivotal role in the growth and advancement of electric vehicle technology. As the most widely adopted battery type for electric vehicles, lithium-ion batteries offer a favorable combination of energy density, efficiency, and longevity, making them indispensable for modern EV applications.

Significant advancements in battery technology and manufacturing processes over the last decade have propelled the adoption of lithium-ion batteries in the electric vehicle market. These strides have not only slashed costs but also bolstered performance and reliability, rendering lithium-ion batteries increasingly attractive to manufacturers and consumers alike.

In recent years, the price of lithium-ion batteries and cell packs has been on the decline, making them more attractive to end-user industries. After experiencing slight price hikes in 2022, battery prices were once again declining in 2023. The cost of lithium-ion battery packs has decreased by 14% to reach a historic low of USD 139/kWh.

This segment encompasses a diverse array of materials, each contributing to the overall performance and functionality of the batteries. These materials are chosen for their ability to enhance the battery's energy density, cycle life, and thermal stability, thereby addressing critical performance parameters required by the automotive industry. Nickel-rich cathode materials, for instance, are particularly favored for their high energy capacity, which directly translates to extended driving ranges for electric vehicles-an essential factor for consumer adoption and market competitiveness.

The region's increasing appetite for electric vehicles has propelled a notable surge in demand for lithium-ion batteries. Consequently, battery manufacturers and assemblers are now channeling investments into battery material production facilities. This strategic move aims to cater to the escalating need for lithium batteries, both on a domestic and international scale. Additionally, advancements in battery technology are further driving this demand. The market is expected to witness continued growth as electric vehicle adoption rises.

For instance, in October 2023, Umicore, a significant player in electric vehicle battery materials, is solidifying its presence in Ontario, Canada, with the establishment of the CAM and pCAM plants. The company is actively building a 35 GWh battery materials production facility in Loyalist, ON, specifically tailored to cater to the burgeoning North American electric vehicle (EV) market.

Recognizing the pivotal role this plant will play in bolstering the regional electric vehicle supply chain and enhancing the overall electric vehicle battery landscape, Umicore has secured significant financial backing from both the Canadian and Ontario governments.

Therefore, as per the points mentioned above, the lithium-ion battery segment is expected to dominate the market during the forecasted period.

United States to Witness Significant Growth

The United States segment has a robust and growing demand for electric vehicles, driven by a combination of consumer preferences, environmental awareness, and regulatory pressures to reduce greenhouse gas emissions. Federal and state-level incentives, such as tax credits and rebates for Electric Vehicle purchases, play a crucial role in accelerating the adoption of electric vehicles.

In 2024, the available financial incentives include a tax credit of up to USD 7,500, while buyers of used electric cars might be eligible for up to USD 4,000. A notable change this year is that consumers can now choose to transfer this credit to a qualifying dealer, securing an instant discount on their vehicle purchase.

These incentives not only make Electric Vehicles more affordable for consumers but also stimulate demand for advanced battery technologies and materials. Furthermore, the United States administration's commitment to achieving net-zero emissions by 2050 and the proposed infrastructure bill, which includes substantial investments in Electric Vehicle charging networks and clean energy initiatives, are expected to bolster the Electric Vehicle market further and, consequently, the demand for battery materials.

These incentives have spurred a swift adoption of electric vehicles in the country. Notably, the International Energy Agency reports a steady rise in electric vehicle adoption over the past decade. Specifically, from 2022 to 2023, battery electric vehicle sales surged by over 37.5%. This growth is even more pronounced when considering the annual average rate over the past five years, which stood at an impressive 71.6%. Such figures underscore the escalating interest in electric vehicles, consequently boosting the demand for batteries in the nation.

Significant investments in domestic battery manufacturing capabilities also characterize the United States segment. Recognizing the strategic importance of reducing dependence on foreign supply chains, both private sector players and government entities are investing heavily in the development of local battery manufacturing facilities. Companies like Tesla, General Motors, Hyundai, and Ford are spearheading efforts to establish gigafactories that produce lithium-ion batteries at scale.

For instance, in April 2023, Two prominent automakers unveiled plans to construct electric vehicle (EV) battery plants in the United States, underscoring the continued rapid growth of electric vehicle manufacturing in the nation. General Motors, in collaboration with Samsung SDI, disclosed a joint investment of USD 3 billion for an electric vehicle battery plant in the United States. Concurrently, Hyundai revealed its partnership with South Korean battery manufacturer SK On, committing a substantial USD 5 billion to establish a battery factory in Georgia.

These facilities aim to leverage advanced manufacturing technologies and automation to enhance production efficiency, reduce costs, and ensure a stable supply of high-quality batteries for the domestic market.

Therefore, as mentioned above, the United States is expected to witness significant growth during the forecast period.

North America Electric Vehicle Battery Materials Industry Overview

The North America Electric Vehicle Battery Materials Market is moderately fragmented. Some of the key players in this market (in no particular order) are Targray Technology International Inc., BASF SE, Mitsubishi Chemical Group Corporation, UBE Corporation, and Umicore

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Growing Electric Vehicle Sales

4.5.1.2 Supportive Government Policies and Regulations

4.5.2 Restraints

4.5.2.1 Dependence on Imported Raw Material Supply

4.6 Supply Chain Analysis

4.7 Industry Attractiveness - Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

4.8 Investment Analysis

5 MARKET SEGMENTATION

5.1 Battery Type

5.1.1 Lithium-ion Battery

5.1.2 Lead-Acid Battery

5.1.3 Others

5.2 Material

5.2.1 Cathode

5.2.2 Anode

5.2.3 Electrolyte

5.2.4 Separator

5.2.5 Others

5.3 Geography

5.3.1 United States

5.3.2 Canada

5.3.3 Rest of North America

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements