하이브리드 본딩 시장 : 패키징 아키텍처별, 장비 유형별, 집적 레벨별 - 예측(-2032년)

Hybrid Bonding Market by Packaging Architecture (Wafer-to-Wafer, Die-to-Wafer, Die-to-Die ), Equipment Type, Integration level - Global Forecast to 2032

상품코드:1889161

리서치사:MarketsandMarkets

발행일:2025년 12월

페이지 정보:영문 286 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

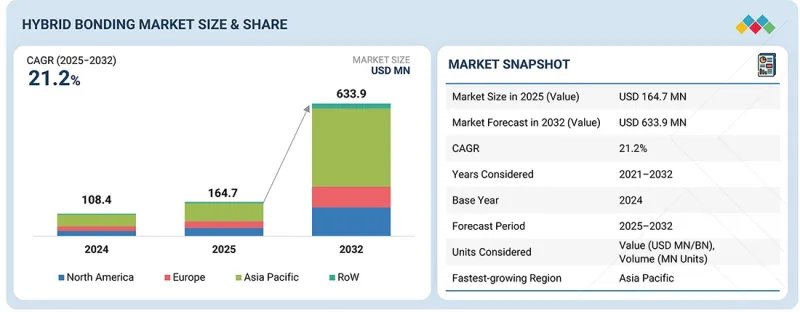

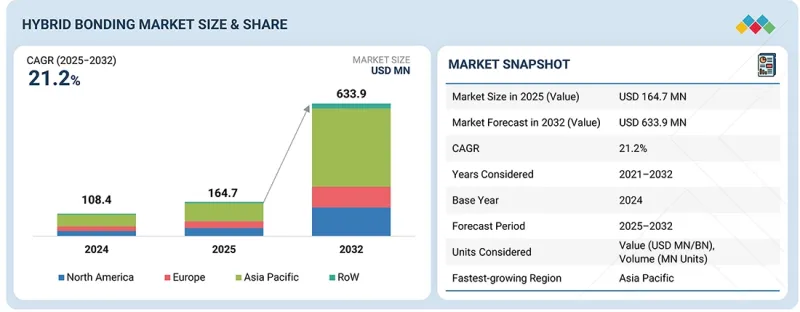

세계의 하이브리드 본딩 시장 규모는 2025년에 1억 6,470만 달러, 2032년까지 6억 3,390만 달러에 이를 것으로 예측되며, 2025년-2032년 CAGR 21.2%의 성장이 전망됩니다.

반도체 제조업체들이 스케일링의 한계를 극복하고 더 높은 대역폭, 더 낮은 지연, 더 높은 전력 효율을 달성하기 위해 3D 집적화로 전환하면서 전 세계적으로 하이브리드 본딩의 채택이 가속화되고 있습니다.

조사 범위

조사 대상 기간

2020-2032년

기준 연도

2024년

예측 기간

2025-2032년

단위

10억 달러

부문

패키징 아키텍처, 프로세스 플로우, 장비 유형, 지역

대상 지역

북미, 유럽, 아시아태평양, 기타 지역

AI, HPC, 첨단 로직 디바이스에서 칩렛 기반 아키텍처가 부상하면서 하이브리드 본딩이 구현하는 초미세 피치 상호 연결의 필요성이 더욱 커지고 있습니다. 주요 파운드리 및 IDM의 첨단 패키징 역량에 대한 지속적인 투자와 소형, 고성능 전자제품에 대한 수요 증가로 인해 전 세계적으로 시장 모멘텀이 강화되고 있습니다.

"W2W(Wafer to Wafer) 부문이 2024년 가장 큰 시장 점유율을 차지했습니다. "

2024년 W2W(Wafer to Wafer) 부문이 하이브리드 본딩 시장에서 가장 큰 점유율을 차지했습니다. 이는 공정 균일성, 정렬 정확도, 처리량에서 최고 수준을 제공하며, 대규모 생산 환경에 적합하기 때문입니다. 주요 메모리 제조업체와 파운드리는 3D NAND, DRAM 적층 및 CIS 제조에서 W2W 공정에 크게 의존하고 있으며, 높은 수율을 달성하기 위해서는 일관된 웨이퍼 레벨의 본딩이 필수적입니다. 또한, 다이 레벨 접근 방식에 비해 웨이퍼 전체에 걸쳐 초미세 피치 상호 연결을 지원할 수 있기 때문에 전체 제조 복잡성을 줄일 수 있습니다. 주요 반도체 팹이 3D 집적 능력을 계속 확장하고 있는 가운데, W2W는 여전히 대부분의 대량 하이브리드 본딩 배치의 기반이 되고 있습니다.

"컴퓨팅 로직 부문은 2025-2032년 하이브리드 본딩 시장에서 가장 높은 CAGR을 나타낼 것으로 예측됩니다. "

고성능 AI 가속기, HPC 프로세서, 데이터센터 워크로드, 첨단 엣지 컴퓨팅 시스템에 대한 수요로 인해 컴퓨팅 로직 용도는 예측 기간 동안 가장 빠르게 성장할 것으로 예측됩니다. 하이브리드 본딩 기술은 이러한 디바이스가 요구하는 초 고밀도 수직 상호연결을 실현하고, 더 높은 대역폭, 우수한 에너지 효율, 로직과 메모리의 긴밀한 통합을 가능하게 합니다. 업계가 칩렛 기반 설계로 빠르게 전환하고 있는 가운데, 하이브리드 본딩은 레티클 크기 제한을 극복하고 확장성을 향상시키므로 채택이 더욱 가속화될 것으로 보입니다. 차세대 로직 아키텍처와 멀티 다이 패키징에 대한 지속적인 투자로 컴퓨팅 로직 부문은 가장 강력한 성장세를 보이고 있습니다.

"아시아태평양 하이브리드 본딩 시장에서 인도는 2025-2032년 가장 높은 CAGR을 나타낼 것으로 예측됩니다. "

인도는 강력한 정부 인센티브와 정책 프레임워크에 힘입어 반도체 제조의 급속한 확대와 첨단 패키징 이니셔티브에 힘입어 예측 기간 동안 아시아태평양에서 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 국가 반도체 미션에 기반한 대규모 투자로 3D 집적 및 하이브리드 본딩 관련 기술에 특화된 새로운 팹, OSAT 시설, 연구센터의 개발이 가속화되고 있습니다. 또한, 통신, 자동차, 데이터센터 부문의 고성능 전자기기 수요 증가도 첨단 패키징 기술에 대한 수요를 촉진하고 있습니다. 세계 장비 공급업체 및 기술 파트너와의 협력 강화로 인해, 이 지역에서 하이브리드 본딩 채택이 가장 빠르게 확대될 것으로 예측됩니다.

세계의 하이브리드 본딩(Hybrid Bonding) 시장에 대해 조사 분석했으며, 주요 촉진요인과 저해요인, 경쟁 구도, 향후 동향 등의 정보를 전해드립니다.

목차

제1장 서론

제2장 주요 요약

제3장 중요 지견

하이브리드 본딩 시장 기업에 있어서 매력적인 기회

하이브리드 본딩 시장 : 패키징 아키텍처별

하이브리드 본딩 시장 : 프로세스 플로우별

하이브리드 본딩 시장 : 용도별

하이브리드 본딩 시장 : 업계별

하이브리드 본딩 시장 : 지역별

제4장 시장 개요

시장 역학

성장 촉진요인

성장 억제요인

기회

과제

미충족 요구와 화이트 스페이스

연결된 시장과 부문간 기회

Tier 1/2/3 기업의 전략적 움직임

제5장 업계 동향

Porter의 Five Forces 분석

거시경제 전망

GDP 동향과 예측

세계의 반도체 제조 장비 업계 동향

세계의 반도체 검사 및 계측 업계 동향

공급망 분석

생태계 분석

가격 결정 분석

웨하본다 평균 판매 가격 : 주요 제조업체별(2024년)

웨하본다 평균 판매 가격 : 지역별(2024년)

무역 분석

수입 시나리오(HS코드 848620)

수출 시나리오(HS코드 848620)

주요 컨퍼런스 및 이벤트(2025년-2026년)

고객의 비즈니스에 영향을 미치는 동향/혼란

투자 및 자금조달 시나리오

사례 연구 분석

2025년 미국 관세의 영향 - 하이브리드 본딩 시장

주요 관세율

가격 영향 분석

국가/지역에 대한 영향

업계에 대한 영향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 향후 용도

주요 신기술

SUB-MICRON & DIRECT CU-TO-CU HYBRID BONDING

저온 하이브리드 본딩(200оC미만)

보완 기술

기술/제품 로드맵

특허 분석

하이브리드 본딩 시장에 대한 AI/생성형 AI의 영향

주요 이용 사례와 시장 장래성

하이브리드 본딩 시장 OEM 베스트 프랙티스

하이브리드 본딩 시장 AI 도입에 관한 사례 연구

상호 접속된 에코시스템과 시장 기업에 대한 영향

AI 통합 하이브리드 본딩 솔루션 채택에 대한 고객 준비 상황

제7장 규제 상황과 지속가능성에 관한 대처

지역 규제와 컴플라이언스

규제기관, 정부기관 및 기타 조직

업계표준

지속가능성 이니셔티브

지속가능성 이니셔티브에 대한 규제 정책의 영향

인증, 라벨 및 환경기준

제8장 고객 상황과 구매 행동

의사결정 프로세스

구매 프로세스에 관여하는 주요 이해관계자와 평가 기준

구매 프로세스 주요 이해관계자

구입 기준

채택 장벽과 내부 과제

다양한 업계의 미충족 요구

제9장 하이브리드 본딩 용재료

접착 재료 (산화층, 구리 및 금속화 적층 구조)

접착제 및 임시 접착 재료

세정 및 표면 처리 재료

제10장 하이브리드 본딩 시장 : 본딩 유형별

COPPER-TO-COPPER (CU-CU)

COPPER-TO-PAD/METAL-TO-PAD

기타 본딩 유형

제11장 하이브리드 본딩 시장 : 패키징 아키텍처별

W2W(Wafer to Wafer)

D2W(Die to Wafer)

D2D(Die to Die)

제12장 하이브리드 본딩 시장 : 통합 레벨별

2.5D 패키징

3D 적층 IC

이종 집적

제13장 하이브리드 본딩 시장 : 프로세스 플로우별

백엔드

프론트엔드

제14장 하이브리드 본딩 시장 : 장비 유형별

WAFER BONDERS

SURFACE PREPARATION TOOLS

INSPECTION & METROLOGY TOOLS

CLEANING & CMP SYSTEMS

제15장 하이브리드 본딩 시장 : 용도별

컴퓨팅 및 로직

메모리 및 스토리지

센싱 인터페이스

접속성 및 통신

기타 용도

제16장 하이브리드 본딩 시장 : 업계별

IT 및 통신

소비자 일렉트로닉스

자동차

항공우주 및 방위

의료

산업 자동화

기타 업계

제17장 하이브리드 본딩 시장 : 지역별

아시아태평양

중국

일본

인도

한국

대만

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

프랑스

영국

이탈리아

스페인

폴란드

북유럽

기타 유럽

기타 지역

중동

아프리카

남미

제18장 경쟁 구도

개요

주요 시장 진출기업의 전략/강점(2021년-2025년)

시장 점유율 분석(2024년)

매출 분석(2020년-2024년)

기업 평가와 재무 지표

제품 비교

APPLIED MATERIALS, INC.

SUSS MICROTEC SE

BESI

KULICKE AND SOFFA INDUSTRIES, INC.

EV GROUP(EVG)

기업 평가 매트릭스 : 주요 기업(2024년)

기업 평가 매트릭스 : 스타트업/중소기업(2024년)

경쟁 시나리오

제19장 기업 개요

주요 기업

APPLIED MATERIALS, INC.

SUSS MICROTEC SE

BESI

EV GROUP(EVG)

KULICKE AND SOFFA INDUSTRIES, INC.

TOKYO ELECTRON LIMITED

LAM RESEARCH CORPORATION

SHIBAURA MECHATRONICS CORPORATION

ASMPT

HANMI SEMICONDUCTOR

기타 기업

ONTO INNOVATION

DISCO CORPORATION

TORAY ENGINEERING CO., LTD.

KLA CORPORATION

BEIJING U-PRECISION TECH CO., LTD

최종사용자

TAIWAN SEMICONDUCTOR MANUFACTURING COMPANY LIMITED

SAMSUNG

SMIC

UNITED MICROELECTRONICS CORPORATION

GLOBALFOUNDRIES

INTEL CORPORATION

SK HYNIX INC.

MICRON TECHNOLOGY, INC.

TEXAS INSTRUMENTS INCORPORATED

AMKOR TECHNOLOGY

ASE TECHNOLOGY HOLDING CO., LTD.

JSCJ

SILICONWARE PRECISION INDUSTRIES CO., LTD.

POWERTECH TECHNOLOGY INC.

SONY SEMICONDUCTOR SOLUTIONS CORPORATION

제20장 조사 방법

제21장 부록

LSH

영문 목차

영문목차

The global hybrid bonding market is expected to reach USD 164.7 million in 2025 and USD 633.9 million by 2032, recording a CAGR of 21.2% from 2025 to 2032. Global hybrid bonding adoption is accelerating as semiconductor manufacturers transition to 3D integration to overcome scaling limitations and achieve higher bandwidth, lower latency, and improved power efficiency.

Scope of the Report

Years Considered for the Study

2020-2032

Base Year

2024

Forecast Period

2025-2032

Units Considered

Value (USD Billion)

Segments

By Packaging Architecture, Process Flow, Equipment Type and region

Regions covered

North America, Europe, APAC, RoW

The rise of chiplet-based architectures in AI, HPC, and advanced logic devices further strengthens the need for ultra-fine-pitch interconnects that hybrid bonding enables. Continued investments in advanced packaging capacity by leading foundries and IDMs, combined with increasing requirements for compact, high-performance electronics, are reinforcing strong market momentum worldwide.

"Wafer-to-wafer (W2W) segment accounted for the largest market share in 2024."

The wafer-to-wafer (W2W) segment held the largest share of the hybrid bonding market in 2024 as it provides the highest level of process uniformity, alignment accuracy, and throughput, making it ideal for large-scale production environments. Major memory manufacturers and foundries rely heavily on W2W processes for 3D NAND, DRAM stacking, and CIS manufacturing, where consistent wafer-level bonding is essential to achieving high yields. Its capability to support extremely fine-pitch interconnects across full wafers also reduces overall manufacturing complexity compared to die-level approaches. As leading semiconductor fabs continue expanding 3D integration capacity, W2W remains the foundation of most high-volume hybrid bonding deployments.

"Computing & logic segment is projected to witness the highest CAGR in the hybrid bonding market from 2025 to 2032."

Computing & logic applications are expected to grow the fastest during the forecast period due to the demand for high-performance AI accelerators, HPC processors, data-center workloads, and advanced edge computing systems. Hybrid bonding enables the ultra-dense vertical interconnects these devices require to achieve higher bandwidth, improved energy efficiency, and tighter logic-to-memory integration. The rapid industry shift toward chiplet-based designs further boosts adoption, as hybrid bonding helps overcome reticle-size limits and enhances scalability. With continuous investments in next-generation logic architectures and multi-die packaging, the computing and logic segment is positioned for the strongest growth trajectory.

"India is expected to record the highest CAGR in the Asia Pacific hybrid bonding market from 2025 to 2032."

India is expected to exhibit the highest CAGR in Asia Pacific during the forecast period due to its rapid expansion of semiconductor manufacturing and advanced packaging initiatives supported by strong government incentives and policy frameworks. Large-scale investments under national semiconductor missions accelerate the development of new fabs, OSAT facilities, and research centers focused on 3D integration and hybrid bonding-related capabilities. The country also witnesses the rising demand for high-performance electronics across telecom, automotive, and data-center sectors, which drives the need for advanced packaging technologies. Combined with increasing collaboration with global equipment suppliers and technology partners, the country is positioned for the fastest growth in hybrid bonding adoption in the region.

Extensive primary interviews were conducted with key industry experts in the hybrid bonding market space to determine and verify the market size for various segments and subsegments gathered through secondary research. The breakdown of primary participants for the report is shown below:

The study contains insights from various industry experts, from component suppliers to Tier 1 companies and OEMs. The break-up of the primaries is as follows:

By Company Type: Tier 1 - 35%, Tier 2 - 45%, and Tier 3 - 20%

By Designation: C-level Executives - 40%, Managers - 30%, and Others - 30%

By Region: North America - 40%, Europe - 30%, Asia Pacific - 20%, and RoW - 10%

Daifuku Co., Ltd. (Japan), MURATA MACHINERY, LTD. (Japan), Exyte Group (Germany), DuPont (US), and Thermo Fisher Scientific Inc. (US) are some key players in the hybrid bonding market.

Research Coverage:

This research report categorizes the hybrid bonding market based on Packaging Architecture [Wafer-to-Wafer (W2W), Die-to-Wafer (D2W), and Die-to-Die (D2D)], Process Flow (Front-end and Back-end), Equipment Type (Wafer Bonders, Cleaning & CMP Systems, Surface Prep Tools, and Inspection & Metrology Tools), Bonding Type [Copper-to-copper (Cu-Cu), Copper-to-pad/metal-to-pad, and Other Bonding Types], Integration Level (2.5D Packaging with Hybrid Bonding, 3D Stacked ICs, and Heterogeneous Integration), Application (Computing & Logic, Memory & Storage, Sensing & Interface, Connectivity & Communications, and Other Applications) Vertical (IT & Telecommunications, Consumer Electronics, Automotive, Aerospace & Defense, Healthcare & Medical, Industrial Automation, and Other Verticals), and Region (North America, Europe, Asia Pacific, and RoW). The report describes the major drivers, restraints, challenges, and opportunities pertaining to the hybrid bonding market and forecasts the same till 2030. Apart from this, the report also consists of leadership mapping and analysis of all the companies included in the hybrid bonding ecosystem.

Key Benefits of Buying the Report

The report will help the market leaders/new entrants in this market by providing information on the closest approximations of the revenue numbers for the overall hybrid bonding market and the subsegments. This report will help stakeholders to understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

Analysis of key drivers (Rising demand for high-bandwidth, low-latency interconnects in AI, HPC, and logic-memory systems, Increasing reliance on advanced hybrid bonding to power >200-layer 3D memory, Shift toward chiplet-based architectures to overcome reticle limits and reduce system power, Growing need for low-temperature bonding to support fragile materials, advanced BEOL stacks, and next-gen devices), restraints (Substantial upfront capital investment and Stringent environment and surface quality requirements), opportunities (Rising need for ultra-dense logic-to-memory connectivity in AI/ML accelerators and Deployment of hybrid bonding in CIS and AR/VR sensors to improve SNR and pixel density), and challenges (Issues in maintaining ultra-low defectivity across wafers and Lack of standardization in die formats, pad structures, and surface pre-treatment flows) influencing the growth of the hybrid bonding market

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the hybrid bonding market

Market Development: Comprehensive information about lucrative markets-the report analyzes the hybrid bonding market across varied regions

Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the hybrid bonding market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players, including EV Group (EVG) (Austria), Applied Materials, Inc. (US), SUSS MicroTec SE (Germany), Besi (Netherlands), Kulicke & Soffa Industries, Inc. (Singapore), Tokyo Electron (TEL) (Japan), ASMPT (Singapore), Lam Research Corporation (US), and SHIBAURA MECHATRONICS CORPORATION (Japan), in the hybrid bonding market

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 UNIT CONSIDERED

1.6 LIMITATIONS

1.7 STAKEHOLDERS

2 EXECUTIVE SUMMARY

2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

2.3 DISRUPTIVE TRENDS IN HYBRID BONDING MARKET

2.4 HIGH-GROWTH SEGMENTS

2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN HYBRID BONDING MARKET

3.2 HYBRID BONDING MARKET, BY PACKAGING ARCHITECTURE

3.3 HYBRID BONDING MARKET, BY PROCESS FLOW

3.4 HYBRID BONDING MARKET, BY APPLICATION

3.5 HYBRID BONDING MARKET, BY VERTICAL

3.6 HYBRID BONDING MARKET, BY REGION

4 MARKET OVERVIEW

4.1 INTRODUCTION

4.2 MARKET DYNAMICS

4.2.1 DRIVERS

4.2.1.1 Rising demand for high-bandwidth, low-latency interconnects in AI, HPC, and logic-memory systems

4.2.1.2 Increasing reliance on advanced hybrid bonding to power >200-layer 3D memory

4.2.1.3 Shift toward chiplet-based architectures to overcome reticle limits and reduce system power

4.2.1.4 Growing need for low-temperature bonding to support fragile materials, advanced BEOL stacks, and next-gen devices

4.2.2 RESTRAINTS

4.2.2.1 Substantial upfront capital investment

4.2.2.2 Stringent environment and surface quality requirements

4.2.3 OPPORTUNITIES

4.2.3.1 Rising need for ultra-dense logic-to-memory connectivity in AI/ML accelerators

4.2.3.2 Deployment of hybrid bonding in CIS and AR/VR sensors to improve SNR and pixel density

4.2.4 CHALLENGES

4.2.4.1 Issues in maintaining ultra-low defectivity across wafers

4.2.4.2 Lack of standardization in die formats, pad structures, and surface pre-treatment flows

4.3 UNMET NEEDS AND WHITE SPACES

4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

5.1 PORTER'S FIVE FORCES ANALYSIS

5.1.1 INTENSITY OF COMPETITIVE RIVALRY

5.1.2 BARGAINING POWER OF SUPPLIERS

5.1.3 BARGAINING POWER OF BUYERS

5.1.4 THREAT OF SUBSTITUTES

5.1.5 THREAT OF NEW ENTRANTS

5.2 MACROECONOMIC OUTLOOK

5.2.1 INTRODUCTION

5.2.2 GDP TRENDS AND FORECAST

5.2.3 TRENDS IN GLOBAL SEMICONDUCTOR MANUFACTURING EQUIPMENT INDUSTRY

5.2.4 TRENDS IN GLOBAL SEMICONDUCTOR INSPECTION AND METROLOGY INDUSTRY

5.3 SUPPLY CHAIN ANALYSIS

5.4 ECOSYSTEM ANALYSIS

5.5 PRICING ANALYSIS

5.5.1 AVERAGE SELLING PRICE OF WAFER BONDERS, BY KEY PLAYER, 2024

5.5.2 AVERAGE SELLING PRICE OF WAFER BONDERS, BY REGION, 2024

5.6 TRADE ANALYSIS

5.6.1 IMPORT SCENARIO (HS CODE 848620)

5.6.2 EXPORT SCENARIO (HS CODE 848620)

5.7 KEY CONFERENCES AND EVENTS, 2025-2026

5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.9 INVESTMENT AND FUNDING SCENARIO

5.10 CASE STUDY ANALYSIS

5.10.1 IMEC PARTNERS WITH EV GROUP TO DEVELOP ADVANCED PROCESS FLOWS TO ACHIEVE FINE-PITCH INTERCONNECTS

5.10.2 SUSS MICROTEC INTRODUCES XBC300 GEN2 TO ENABLE WAFER-TO-WAFER AND DIE-TO-WAFER BONDING IN INNOVATION CENTERS AND SEMICONDUCTOR PILOT LINES

5.10.3 APPLIED MATERIALS AND BESI DELIVER INTEGRATED D2W HYBRID BONDING TO SUPPORT HIGH-VOLUME MANUFACTURING

5.11 IMPACT OF 2025 US TARIFF - HYBRID BONDING MARKET

5.11.1 INTRODUCTION

5.11.2 KEY TARIFF RATES

5.11.3 PRICE IMPACT ANALYSIS

5.11.4 IMPACT ON COUNTRIES/REGIONS

5.11.4.1 US

5.11.4.2 Europe

5.11.4.3 Asia Pacific

5.11.5 IMPACT ON VERTICALS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACTS, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

6.1 KEY EMERGING TECHNOLOGIES

6.1.1 SUB-MICRON AND DIRECT CU-TO-CU HYBRID BONDING

6.1.2 LOW-TEMPERATURE HYBRID BONDING (<200°C)

6.2 COMPLEMENTARY TECHNOLOGIES

6.2.1 ADVANCED CMP

6.3 TECHNOLOGY/PRODUCT ROADMAP

6.4 PATENT ANALYSIS

6.5 IMPACT OF AI/GEN AI ON HYBRID BONDING MARKET

6.5.1 TOP USE CASES AND MARKET POTENTIAL

6.5.2 BEST PRACTICES FOLLOWED BY OEMS IN HYBRID BONDING MARKET

6.5.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN HYBRID BONDING MARKET

6.5.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

6.5.5 CLIENTS' READINESS TO ADOPT AI-INTEGRATED HYBRID BONDING SOLUTIONS

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

7.1 REGIONAL REGULATIONS AND COMPLIANCE

7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

7.1.2 INDUSTRY STANDARDS

7.2 SUSTAINABILITY INITIATIVES

7.3 IMPACT OF REGULATORY POLICIES ON SUSTAINABILITY INITIATIVES

7.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

8.1 DECISION-MAKING PROCESS

8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

8.2.2 BUYING CRITERIA

8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

8.4 UNMET NEEDS OF VARIOUS VERTICALS

9 MATERIALS FOR HYBRID BONDING

9.1 INTRODUCTION

9.2 BONDING MATERIALS (OXIDE LAYERS, COPPER, AND METALLIZATION STACKS)

9.3 ADHESIVES AND TEMPORARY BONDING MATERIALS

9.4 CLEANING AND SURFACE PREPARATION MATERIALS

10 HYBRID BONDING MARKET, BY BONDING TYPE

10.1 INTRODUCTION

10.2 COPPER-TO-COPPER (CU-CU)

10.2.1 DEMAND FOR HIGH-PERFORMANCE INTERCONNECTS AT FINE PITCHES TO DRIVE MARKET

10.3 COPPER-TO-PAD/METAL-TO-PAD

10.3.1 NEED FOR PROCESS FLEXIBILITY AND COMPATIBILITY WITH DIVERSE METALLIZATION SCHEMES TO FUEL SEGMENTAL GROWTH

10.4 OTHER BONDING TYPES

11 HYBRID BONDING MARKET, BY PACKAGING ARCHITECTURE

11.1 INTRODUCTION

11.2 WAFER-TO-WAFER (W2W)

11.2.1 HIGH THROUGHPUT, PITCH SCALABILITY, AND COST EFFICIENCY FOR HOMOGENEOUS HIGH-VOLUME STACKS TO SPUR DEMAND

11.3 DIE-TO-WAFER (D2W)

11.3.1 YIELD OPTIMIZATION AND HETEROGENEOUS COMPONENT INTEGRATION TO BOLSTER SEGMENTAL GROWTH

11.4 DIE-TO-DIE (D2D)

11.4.1 FOCUS ON MODULARITY, LATENCY REDUCTION, AND POWER EFFICIENCY OF COMPUTE ARCHITECTURES TO BOOST SEGMENTAL GROWTH

12 HYBRID BONDING MARKET, BY INTEGRATION LEVEL

12.1 INTRODUCTION

12.2 2.5D PACKAGING

12.2.1 NEED FOR HIGH-BANDWIDTH INTERCONNECTS AND IMPROVED SIGNAL INTEGRITY IN LATERAL DIE CONFIGURATIONS TO DRIVE MARKET

12.3 3D STACKED ICS

12.3.1 RISING ADOPTION OF STACKED COMPUTE TILES IN HPC AND DATA CENTER PROCESSORS TO FOSTER SEGMENTAL GROWTH

12.4 HETEROGENEOUS INTEGRATION

12.4.1 SUPPORT FOR ADVANCED SURFACE ACTIVATION, HIGH-ACCURACY DIE PLACEMENT, WARPAGE CONTROL, AND LOW-TEMPERATURE BONDING TO SPUR DEMAND

13 HYBRID BONDING MARKET, BY PROCESS FLOW

13.1 INTRODUCTION

13.2 BACK-END

13.2.1 FOCUS ON CREATING DENSE, LOW-LATENCY INTERCONNECTS AT PACKAGING LEVEL TO ACCELERATE SEGMENTAL GROWTH

13.3 FRONT-END

13.3.1 NEED FOR HIGH INTERCONNECT PERFORMANCE AND INTEGRATION PRECISION TO AUGMENT SEGMENTAL GROWTH

14 HYBRID BONDING MARKET, BY EQUIPMENT TYPE

14.1 INTRODUCTION

14.2 WAFER BONDERS

14.2.1 NEED FOR SUB-MICRON ALIGNMENT, ULTRA-FLAT SURFACES, AND LOW-TEMPERATURE CU-CU DIFFUSION BONDING TO FUEL SEGMENTAL GROWTH

14.3 SURFACE PREPARATION TOOLS

14.3.1 ABILITY TO SUPPORT PLASMA ACTIVATION, ION-BEAM CLEANING, AND CHEMICAL SURFACE CONDITIONING TO CONTRIBUTE TO SEGMENTAL GROWTH

14.4 INSPECTION & METROLOGY TOOLS

14.4.1 SUB-MICRON OVERLAY MEASUREMENT, VOID DETECTION, AND POST-BOND VERIFICATION ATTRIBUTES TO FOSTER SEGMENTAL GROWTH

14.5 CLEANING & CMP SYSTEMS

14.5.1 ABILITY TO PROVIDE PLANARIZED COPPER/DIELECTRIC LAYERS AND CONTAMINANT-FREE SURFACES TO BOLSTER SEGMENTAL GROWTH

15 HYBRID BONDING MARKET, BY APPLICATION

15.1 INTRODUCTION

15.2 COMPUTING & LOGIC

15.2.1 HIGH-PERFORMANCE COMPUTING (HPC) & AI ACCELERATORS

15.2.1.1 Requirement for massive bandwidth scaling, fine-grained parallelism, and data locality optimization to drive market

15.2.2 HETEROGENEOUS SOCS & CHIPLET INTEGRATION

15.2.2.1 Extremely dense, short-reach links of chip architectures to contribute to segmental growth

15.3 MEMORY & STORAGE

15.3.1 HIGH-BANDWIDTH MEMORY (HBM)

15.3.1.1 Increasing demand for multi-terabit bandwidth between GPUs/AI accelerators and memory stacks to boost segmental growth

15.3.2 3D NAND & STACKED DRAM

15.3.2.1 Rising need for ultra-large vertical stacking and reduced interconnect delay in dense memory arrays to drive market

15.4 SENSING & INTERFACE

15.4.1 CMOS IMAGE SENSORS (CIS)

15.4.1.1 Requirement for higher frame rates and lower latency to accelerate segmental growth

15.4.2 MICRO-LED DISPLAYS

15.4.2.1 Ability to support fine-pitch interconnects for mass transfer, reduced defect density, and high optical efficiency to spur demand

15.4.3 MEMS & OTHER SENSORS

15.4.3.1 Requirement for low-profile, multi-functional sensing stacks to augment segmental growth

15.5 CONNECTIVITY & COMMUNICATIONS

15.5.1 RF FRONT-END MODULES (FEM)

15.5.1.1 Reliance on hybrid bonding to shorten RF signal paths and reduce insertion loss to contribute to segmental growth

15.5.2 PHOTONICS & OPTICAL INTERCONNECTS

15.5.2.1 Focus on reducing optical power requirements and improving signal fidelity to augment segmental growth

15.5.3 5G DEVICES

15.5.3.1 Support for compact integration of RF front-end modules, antenna arrays, and baseband processors at fine pitches to spur demand

15.6 OTHER APPLICATIONS

16 HYBRID BONDING MARKET, BY VERTICAL

16.1 INTRODUCTION

16.2 IT & TELECOMMUNICATIONS

16.2.1 EXPANSION OF CLOUD-NATIVE INFRASTRUCTURE AND HYPERSCALE INFRASTRUCTURE TO DRIVE MARKET

16.2.2 DATA CENTER

16.2.3 CLOUD COMPUTING

16.3 CONSUMER ELECTRONICS

16.3.1 PREFERENCE FOR COMPACT, POWER-EFFICIENT, AND FEATURE-DENSE DEVICES TO ACCELERATE SEGMENTAL GROWTH

16.3.2 SMARTPHONES

16.3.3 WEARABLES

16.4 AUTOMOTIVE

16.4.1 DEMAND FOR RELIABLE ELECTRONIC ARCHITECTURES TO SUPPORT AUTONOMOUS AND SOFTWARE-DEFINED VEHICLES TO FUEL SEGMENTAL GROWTH

16.4.2 ADVANCED DRIVER ASSISTANCE SYSTEMS (ADAS)

16.4.3 INFOTAINMENT

16.5 AEROSPACE & DEFENSE

16.5.1 NEED FOR ROBUST, MINIATURIZED, AND HIGH-PERFORMANCE ELECTRONIC ARCHITECTURES TO BOLSTER SEGMENTAL GROWTH

16.6 HEALTHCARE & MEDICAL

16.6.1 FOCUS ON MINIATURIZATION, PRECISION, AND DATA THROUGHPUT TO AUGMENT SEGMENTAL GROWTH

16.7 INDUSTRIAL AUTOMATION

16.7.1 ADOPTION OF ADVANCED CONTROL SYSTEMS, REAL-TIME ANALYTICS, ROBOTICS, AND EDGE AI TO FOSTER SEGMENTAL GROWTH

16.8 OTHER VERTICALS

17 HYBRID BONDING MARKET, BY REGION

17.1 INTRODUCTION

17.2 ASIA PACIFIC

17.2.1 CHINA

17.2.1.1 High emphasis on advanced packaging capabilities to accelerate market growth

17.2.2 JAPAN

17.2.2.1 Strong focus on 3D integration and expertise in ultra-precision manufacturing to fuel market growth

17.2.3 INDIA

17.2.3.1 Increasing investment in semiconductor manufacturing and advanced packaging ecosystem to boost market growth

17.2.4 SOUTH KOREA

17.2.4.1 High commitment to expand memory manufacturing and hybrid bonding equipment supply to contribute to market growth

17.2.5 TAIWAN

17.2.5.1 Rise in foundries and advanced packaging facilities to expedite market growth

17.2.6 REST OF ASIA PACIFIC

17.3 NORTH AMERICA

17.3.1 US

17.3.1.1 Leadership in chiplet architectures, AI compute, and advanced packaging R&D to augment market growth

17.3.2 CANADA

17.3.2.1 Presence of specialized research institutions and photonic integration labs to contribute to market growth

17.3.3 MEXICO

17.3.3.1 Rising deployment of hybrid-bonded semiconductor components to bolster market growth

17.4 EUROPE

17.4.1 GERMANY

17.4.1.1 Transition toward autonomous driving and software-defined platforms to drive market

17.4.2 FRANCE

17.4.2.1 Presence of laboratories and advanced packaging pilot lines to foster market growth

17.4.3 UK

17.4.3.1 Demand for advanced packaging from aerospace, defense, and HPC research to fuel market growth

17.4.4 ITALY

17.4.4.1 Preference for fine interconnect pitches in electronic packages to accelerate market growth

17.4.5 SPAIN

17.4.5.1 Strong focus on IoT and smart infrastructure deployment to expedite market growth

17.4.6 POLAND

17.4.6.1 Expanding electronics manufacturing clusters and government-backed semiconductor initiatives to drive market

17.4.7 NORDICS

17.4.7.1 Emphasis on deep-tech research to accelerate market growth

17.4.8 REST OF EUROPE

17.5 ROW

17.5.1 MIDDLE EAST

17.5.1.1 Growing emphasis on high-tech R&D and defense electronics modernization to fuel market growth

17.5.2 AFRICA

17.5.2.1 Development of academic research programs and electronics testing laboratories to facilitate market growth

17.5.3 SOUTH AMERICA

17.5.3.1 Growing demand for high-end electronics, industrial IoT, and research-led semiconductor development to drive market

18 COMPETITIVE LANDSCAPE

18.1 OVERVIEW

18.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

18.3 MARKET SHARE ANALYSIS, 2024

18.4 REVENUE ANALYSIS, 2020-2024

18.5 COMPANY VALUATION AND FINANCIAL METRICS

18.6 PRODUCT COMPARISON

18.6.1 APPLIED MATERIALS, INC.

18.6.2 SUSS MICROTEC SE

18.6.3 BESI

18.6.4 KULICKE AND SOFFA INDUSTRIES, INC.

18.6.5 EV GROUP (EVG)

18.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

18.7.1 STARS

18.7.2 EMERGING LEADERS

18.7.3 PERVASIVE PLAYERS

18.7.4 PARTICIPANTS

18.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

18.7.5.1 Company footprint

18.7.5.2 Region footprint

18.7.5.3 Application footprint

18.7.5.4 Packaging architecture footprint

18.7.5.5 Equipment type footprint

18.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024