보안 태세 관리(SPM) 시장 : 제공 제품별, 전개 모드별, 딜리버리 모델별, 조직 규모별, 용도별, 업계별, 지역별 - 예측(-2030년)

Security Posture Management Market by Solution, Service (Consulting, Managed ), Application, Vertical, Region - Global Forecast to 2030

상품코드:1861048

리서치사:MarketsandMarkets

발행일:2025년 09월

페이지 정보:영문 487 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

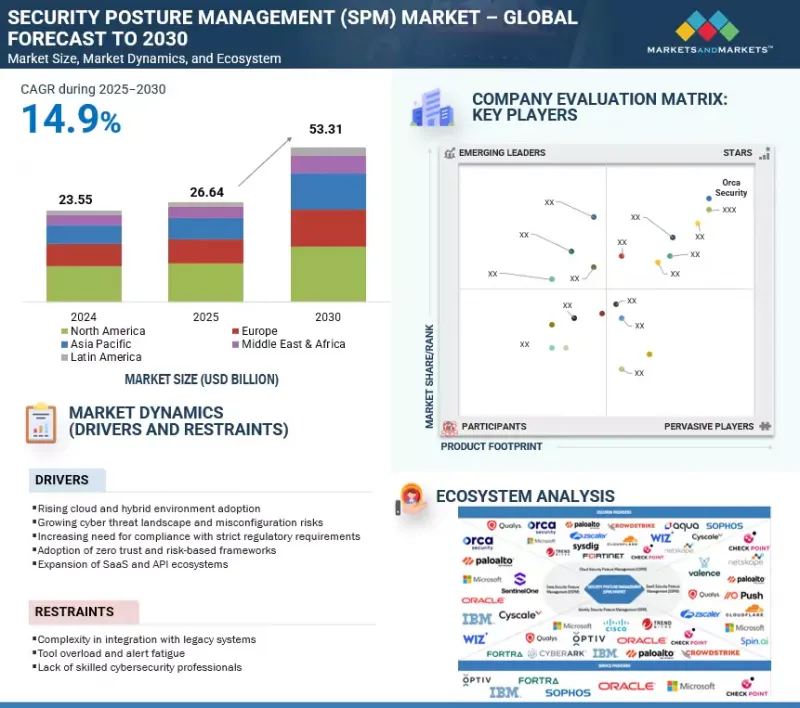

세계의 보안 태세 관리(SPM) 시장 규모는 2025년 266억 4,000만 달러에서 2030년에는 533억 1,000만 달러에 이르고, 예측 기간중 연평균 복합 성장률(CAGR) 14.9%로 확대될 것으로 예측됩니다.

SPM 시장은 지속적인 모니터링과 리스크 평가가 필요한 복잡하고 역동적인 디지털 환경을 만들어낸 SaaS와 API 생태계의 확장이 주도하고 있습니다.

조사 범위

조사 대상 연도

2019-2030년

기준 연도

2024년

예측 기간

2025-2030년

검토 단위

금액(100만 달러/10억 달러)

부문

제공 제품별, 전개 모드별, 딜리버리 모델별, 조직 규모별, 용도별, 업계별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카

조직이 여러 SaaS 용도를 도입하고, 통합 및 데이터 교환을 위해 API를 많이 사용하게 되면, 공격 대상 영역이 확대되어 사전 보안 대책이 필수적입니다. 동시에 엄격한 규제 요건을 준수해야 할 필요성이 높아짐에 따라 기업들은 첨단 자세 관리 도구를 도입하고 있습니다. 이러한 솔루션은 설정 오류, 데이터 유출, 진화하는 사이버 위협과 관련된 위험을 줄이면서 표준 준수를 유지하는 데 도움이 됩니다.

기업들이 중요한 비즈니스 운영에 있어 SaaS 플랫폼에 대한 의존도가 높아짐에 따라, SSPM 솔루션 부문은 SPM 시장에서 가장 빠르게 성장하고 있는 분야입니다. 오늘날 기업들은 수십, 수백 개의 SaaS 용도를 사용하고 있으며, 이는 보안 팀이 완벽한 가시성과 제어를 위해 고군분투하는 복잡한 환경을 만들어내고 있습니다. 2024년 보고서에 따르면, SaaS 용도의 65%는 중앙 집중식 IT 모니터링 없이 사용되고 있습니다. 2024년 보고서에 따르면, SaaS 용도의 65%는 IT의 중앙 집중식 모니터링 없이 활용되고 있습니다. 이러한 거버넌스 부족은 설정 오류, 무단 액세스, 컴플라이언스 위반 등의 위험에 노출될 수 있습니다. SSPM 솔루션은 SaaS 용도를 지속적으로 모니터링하고, 위험한 동작을 감지하고, 다양한 환경에서 정책 적용을 자동화함으로써 이러한 문제를 해결합니다. 규제 요건이 강화되고 SaaS 생태계가 확대되면서 기업들은 SSPM을 도입하여 내결함성을 강화하고 보안 표준을 철저히 준수하고 있습니다. SaaS 전용 보안에 대한 수요는 CSPM이나 IAM과 같은 기존 도구만으로는 SaaS 환경과 관련된 고유한 리스크를 보호할 수 없습니다는 인식이 확산되고 있음을 반영합니다. 따라서 SSPM 솔루션은 기업이 민첩성과 보안의 균형을 맞추는 데 중요한 역할을 하며, SPM의 전망에서 가장 역동적이고 필수적인 부분 중 하나가 되었습니다.

위험 가시화 및 노출 관리 분야는 복잡해지는 디지털 생태계의 보안 격차 및 취약점에 대해 기업이 더 깊은 통찰력을 원하고 있어 SPM 시장에서 가장 빠르게 성장하고 있습니다. 기업은 하이브리드 인프라, 멀티 클라우드 환경, SaaS 용도를 사용하고 있으며, 이러한 환경에서는 다양한 노출이 발생하기 때문에 실시간 가시성 확보가 보안 리더의 최우선 과제가 되고 있습니다. 2025년 3월에 발표된 설문조사에 따르면, CISO의 78% 가량이 자산과 ID에 대한 통합적인 가시성 부족을 가장 시급한 보안 문제로 꼽았다고 합니다. 위험 가시성 및 노출 관리 솔루션은 컨텍스트 기반 인텔리전스를 제공하고, 공격 경로를 매핑하고, 개별 경보가 아닌 비즈니스에 미치는 영향에 따라 복구 우선순위를 결정함으로써 이 문제를 해결합니다. 이러한 솔루션은 지속적으로 위험을 평가하고 공격자가 악용하기 전에 잠재적인 악용 시나리오를 식별함으로써 보안팀이 사후 방어에서 사전 예방적 방어 방식으로 전환할 수 있도록 지원합니다. 또한, 제로 트러스트 및 리스크 기반 프레임워크의 채택이 확대되고, 종합적인 가시성과 통제에 대한 지속적인 검증이 요구됨에 따라 수요도 가속화되고 있습니다. 사이버 공격이 증가하고, 설정 오류로 인한 침해가 여전히 주요 원인으로 작용함에 따라, 기업들은 의사결정을 강화하고, 단편적인 도구로 인한 노이즈를 줄이고, 진화하는 위협에 대한 내성을 강화하기 위해 이러한 솔루션에 주목하고 있습니다.

미국은 성숙한 디지털 생태계, 높은 클라우드 기술 채택률, 사이버 위협의 복잡성으로 인해 북미 SPM 시장에서 가장 큰 점유율을 차지할 것으로 예측됩니다. 은행, 의료, 정부 기관, 중요 인프라 등 각 산업 분야의 조직들은 탄력성을 강화하고 엄격한 컴플라이언스 요건을 충족하기 위해 첨단 보안 도구에 많은 투자를 하고 있습니다. IBM의 '2024년 7월 데이터 유출 비용 보고서'에 따르면, 헬스케어 분야는 13년 연속 평균 유출 비용이 1,093만 달러로 가장 높은 산업으로 꼽혔습니다. 이는 미국 시장에서 더 나은 가시성, 위험 평가 및 자동화된 태세 관리 솔루션에 대한 수요가 급증하고 있음을 보여줍니다. 미국은 또한 HIPAA, CCPA 및 분야별 사이버 보안 가이드라인과 같은 프레임워크를 통해 위험 기반 태세 관리 기법의 채택을 촉진하고, 규제 시행에 있어서도 선도적인 위치를 차지하고 있습니다. 2025년 3월 조사에 따르면, 미국 기업 보안팀의 절반 이상이 전체 환경에 대한 지속적인 가시성을 확보하지 못해 공격자가 악용할 수 있는 틈새를 만들고 있는 것으로 나타났습니다. 이러한 과제에 더해 급속한 디지털 전환, 고도로 규제된 환경, 대기업의 사업 규모가 결합되어 미국은 이 지역의 성장에 가장 큰 기여를 하는 지역으로 부상했습니다.

세계의 보안 위치 관리(Security Position Management) 시장에 대해 조사했으며, 제공 제품별, 배포 모드별, 제공 모델별, 조직 규모별, 용도별, 산업별, 지역별 동향, 시장 진출기업 프로파일 등의 정보를 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 프리미엄 인사이트

제5장 시장 개요와 업계 동향

도입

시장 역학

사례 연구 분석

밸류체인 분석

생태계 분석

생성형 AI가 보안 태세 관리(SPM) 시장에 미치는 영향

Porter의 Five Forces 분석

주요 이해관계자와 구입 기준

가격 분석

기술 분석

특허 분석

규제 상황

2025년 미국 관세의 영향 - 보안 태세 관리(SPM) 시장

고객의 비즈니스에 영향을 미치는 동향/혼란

보안 태세 관리(SPM) 시장 : 비즈니스 모델

2025년 주요 컨퍼런스 및 이벤트

투자 및 자금조달 시나리오

제6장 보안 태세 관리(SPM) 시장(제공 제품별)

서론

솔루션

서비스

제7장 보안 태세 관리(SPM) 시장(전개 모드별)

서론

On-Premise

클라우드

하이브리드

제8장 보안 태세 관리(SPM) 시장(딜리버리 모델별)

서론

에이전트리스 구독

에이전트 및 런타임 구독

데이터 볼륨 구독

기능별 구독

제9장 보안 태세 관리(SPM) 시장(조직 규모별)

서론

대기업

중소기업

제10장 보안 태세 관리(SPM) 시장(용도별)

서론

오설정 및 취약성 관리

컴플라이언스 및 거버넌스 보증

위험 가시성 및 노출 관리

사고 대비 및 대응 지원 체계 구축

제11장 보안 태세 관리(SPM) 시장(업계별)

서론

은행, 금융서비스 및 보험(BFSI)

헬스케어 및 생명과학

정부

IT 및 ITES

소매 및 전자상거래

통신

에너지 및 유틸리티

기타

제12장 보안 태세 관리(SPM) 시장(지역별)

서론

북미

북미 : 보안 태세 관리(SPM) 시장 성장 촉진요인

북미 : 거시경제 전망

미국

캐나다

유럽

유럽 : 보안 태세 관리(SPM) 시장 성장 촉진요인

유럽 : 거시경제 전망

영국

독일

프랑스

이탈리아

기타

아시아태평양

아시아태평양 : 보안 태세 관리(SPM) 시장 성장 촉진요인

아시아태평양 : 거시경제 전망

중국

일본

인도

기타

중동 및 아프리카

중동 및 아프리카 : 보안 태세 관리(SPM) 시장 성장 촉진요인

중동 및 아프리카 : 거시경제 전망

중동

GCC 국가

아프리카

라틴아메리카

라틴아메리카 : 보안 태세 관리(SPM) 시장 성장 촉진요인

라틴아메리카 : 거시경제 전망

브라질

멕시코

기타

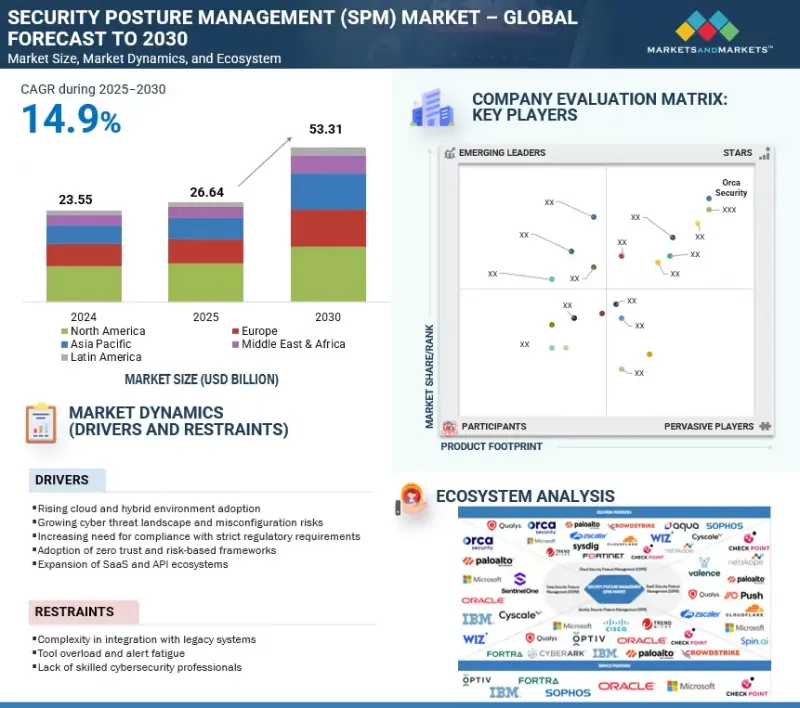

제13장 경쟁 구도

개요

주요 시장 진출기업의 전략/강점

매출 분석, 2019년-2024년

시장 점유율 분석

제품/브랜드 비교

기업 평가와 재무 지표

기업 평가 매트릭스, 주요 시장 진출기업, 2024년

경쟁 시나리오

제14장 기업 개요

주요 시장 진출기업

IBM

MICROSOFT

PALO ALTO NETWORKS

CROWDSTRIKE

CHECK POINT

ZSCALER

FORTRA

OPTIV SECURITY

ORCA SECURITY

AQUA SECURITY

SOPHOS

NETSKOPE

TREND MICRO

CLOUDFLARE

FORTINET

PERMISO SECURITY

WIPRO

QUALYS

SYSDIG

ORACLE

WIZ

TENABLE

SENTINELONE

CYSCALE

VALENCE SECURITY

PUSH SECURITY

LUMOS

SPIN.AI

FIREMON

APPOMNI

JUPITERONE

VEZA

GRIP SECURITY

PROOFPOINT

STRAC

CEQUENCE SECURITY

BEYONDTRUST

OKTA

AUTHMIND

FORCEPOINT

THALES

VARONIS

제15장 인접 시장과 관련 시장

제16장 부록

LSH

영문 목차

영문목차

The global security posture management (SPM) market size is projected to grow from USD 26.64 billion in 2025 to USD 53.31 billion by 2030 at a Compound Annual Growth Rate (CAGR) of 14.9% during the forecast period. The SPM market is driven by the expansion of SaaS and API ecosystems, which have created a complex and dynamic digital environment requiring continuous monitoring and risk assessment.

Scope of the Report

Years Considered for the Study

2019-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million/USD Billion)

Segments

Offering, Organization Size, Application, Vertical, and Region

Regions covered

North America, Europe, Asia Pacific, Middle East & Africa, Latin America

As organizations adopt multiple SaaS applications and rely heavily on APIs for integration and data exchange, the attack surface has expanded, making proactive security measures essential. At the same time, the increasing need for compliance with strict regulatory requirements is pushing enterprises to adopt advanced posture management tools. These solutions help maintain adherence to standards while reducing risks associated with misconfigurations, data exposure, and evolving cyber threats.

"By solution, the SaaS security posture management (SSPM) segment is expected to grow at the highest CAGR during the forecast period."

SSPM solutions segment is emerging as the fastest-growing within the SPM market as enterprises increase their reliance on SaaS platforms for critical business operations. Today, organizations use dozens or even hundreds of SaaS applications, creating complex environments where security teams struggle to gain complete visibility and control. A key challenge lies in the rise of shadow IT; according to a 2024 report, 65% of SaaS applications are being used without centralized IT oversight. This lack of governance exposes organizations to risks such as misconfigurations, unauthorized access, and compliance violations. SSPM solutions address these issues by continuously monitoring SaaS applications, detecting risky behaviors, and automating policy enforcement across diverse environments. As regulatory requirements tighten and SaaS ecosystems expand, enterprises adopt SSPM to strengthen resilience and ensure adherence to security standards. The demand for dedicated SaaS security reflects the growing awareness that traditional tools such as CSPM or IAM alone cannot safeguard the unique risks associated with SaaS environments. SSPM solutions, therefore, play a critical role in helping businesses balance agility with security, making them one of the most dynamic and essential segments in the SPM landscape.

"By application, the risk visibility & exposure management segment is expected to grow at the highest CAGR during the forecast period."

The risk visibility and exposure management segment is witnessing the fastest growth in the SPM market as enterprises seek more profound insights into their security gaps and vulnerabilities across increasingly complex digital ecosystems. Organizations deal with hybrid infrastructures, multi-cloud environments, and SaaS applications that introduce a wide range of exposures, making real-time visibility a top priority for security leaders. According to a survey published in March 2025, nearly 78% of CISOs highlighted the lack of unified visibility across assets and identities as their most pressing security challenge. Risk visibility and exposure management solutions address this by providing contextual intelligence, mapping attack paths, and prioritizing remediation based on business impact rather than isolated alerts. They help security teams shift from reactive to proactive defense by continuously assessing risks and identifying potential exploitation scenarios before attackers can take advantage. The growing adoption of zero trust and risk-based frameworks is also accelerating demand, as these approaches require comprehensive visibility and continuous validation of controls. With the volume of cyberattacks increasing and misconfigurations remaining a leading cause of breaches, enterprises are turning to these solutions to enhance decision-making, reduce noise from fragmented tools, and ensure stronger resilience against evolving threats.

The US is expected to hold the largest market size in the North American region during the forecast period.

The US is expected to hold the largest share in the North American SPM market due to its mature digital ecosystem, high adoption of cloud technologies, and the increasing complexity of its cyber threat landscape. Organizations across industries such as banking, healthcare, government, and critical infrastructure invest heavily in advanced security tools to strengthen resilience and meet stringent compliance mandates. The healthcare sector continues to face significant challenges, with IBM's July 2024 Cost of a Data Breach Report identifying it as the industry with the highest average breach cost of 10.93 million dollars for the thirteenth consecutive year. This highlights the urgent demand for better visibility, risk assessment, and automated posture management solutions in the US market. The country also leads in regulatory enforcement, with frameworks such as HIPAA, CCPA, and sector-specific cybersecurity guidelines driving the adoption of risk-based posture management practices. In March 2025, a survey revealed that over half of security teams in US enterprises lack continuous visibility across their environments, creating gaps that attackers can exploit. These challenges, combined with rapid digital transformation, a highly regulated environment, and the scale of operations across large enterprises, position the US as the strongest contributor to regional growth.

Breakdown of primaries

The study contains insights from various industry experts, from component suppliers to Tier 1 companies and OEMs. The break-up of the primaries is as follows:

By Company Type: Tier 1 - 35%, Tier 2 - 45%, and Tier 3 - 20%

By Designation: Managerial and Other Levels- 60%, C-Level - 40%

By Region: North America - 35%, Europe - 20%, Asia Pacific - 20%, Middle East & Africa - 20%, Latin America - 5%

Major vendors in the global SPM market include IBM (US), Microsoft (US), Check Point (Israel), Zscaler (US), Fortra (US), Optiv Security (US), Orca Security (US), Aqua Security (US), Sophos (UK), Palo Alto Networks (US), CrowdStrike (US), Netskope (US), Trend Micro (Japan), Cloudflare (US), Fortinet (US), Wipro (India), Qualys (US), Sysdig (US), Oracle (US), Wiz.io (US), Tenable (US), SentinelOne (US), Cyscale (UK), Valence Security (US), Push Security (UK), Lumos (US), Spin.AI (US), Permiso Security (US), FireMon (US), AppOmni (US), JupiterOne (US), Veza (US), Grip Security (Israel), Proofpoint (US), Strac.io (US), Cequence Security (US), BeyondTrust (US), Okta (US), AuthMind (US), Forcepoint (US), Thales (France), and Varonis (US).

The study includes an in-depth competitive analysis of the key players in the SPM market, their company profiles, recent developments, and key market strategies.

Research Coverage

The report segments the SPM market and forecasts its size offering (solutions/platforms (CSPM, SSPM, ISPM, DSPM, ASPM) and services), organization size (large enterprises and SMEs), application (misconfiguration & vulnerability management, compliance & governance assurance, risk visibility & exposure management, incident preparedness & response enablement), and vertical (banking, financial services, and insurance, healthcare & life sciences, government, IT & ITeS, retail & e-commerce, telecommunications, energy & utilities, and other verticals (media & entertainment and education)).

The study also includes an in-depth competitive analysis of the market's key players, their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report

The report will help market leaders and new entrants with information on the closest approximations of the revenue numbers for the overall SPM market and the subsegments. It will also help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

Analysis of key drivers (Rising cloud and hybrid environment adoption, growing cyber threat landscape and misconfiguration risks, Increasing need for compliance with strict regulatory requirements, adoption of zero trust and risk-based frameworks, expansion of SaaS and API ecosystems), restraints (Complexity in integration with legacy systems, tool overload and alert fatigue, lack of skilled cybersecurity professionals), opportunities (Convergence of security platforms such as CNAPP, CSPM, DSPM, SSPM, integration of AI and ML, emergence of identity and data-centric SPM), and challenges (Lack of unified posture visibility across environments, rapid expansion of shadow IT and unauthorized SaaS use, and difficulty in prioritizing and remediating risks)

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product & service launches in the SPM market

Market Development: Comprehensive information about lucrative markets - the report analyzes the SPM market across varied regions

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the SPM market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players in the SPM market, including Microsoft (US), Palo Alto Networks (US), Check Point (Israel), CrowdStrike (US), and Zscaler (US)

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.4 YEARS CONSIDERED

1.5 CURRENCY CONSIDERED

1.6 UNITS CONSIDERED

1.7 STAKEHOLDERS

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.2 PRIMARY DATA

2.1.2.1 Breakup of primary interviews

2.1.2.2 Key insights from industry experts

2.2 MARKET SIZE ESTIMATION

2.2.1 TOP-DOWN APPROACH

2.2.2 BOTTOM-UP APPROACH

2.3 DATA TRIANGULATION

2.4 MARKET FORECAST

2.5 RESEARCH ASSUMPTIONS

2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN SECURITY POSTURE MANAGEMENT MARKET

4.2 SECURITY POSTURE MANAGEMENT MARKET, BY OFFERING

4.3 SECURITY POSTURE MANAGEMENT MARKET, BY SOLUTION

4.4 SECURITY POSTURE MANAGEMENT MARKET, BY SERVICE

4.5 SECURITY POSTURE MANAGEMENT MARKET, BY PROFESSIONAL SERVICE

4.6 SECURITY POSTURE MANAGEMENT MARKET, BY DEPLOYMENT MODE

4.7 SECURITY POSTURE MANAGEMENT MARKET, BY DELIVERY MODEL

4.8 SECURITY POSTURE MANAGEMENT MARKET, BY ORGANIZATION SIZE

4.9 SECURITY POSTURE MANAGEMENT MARKET, BY APPLICATION

4.10 SECURITY POSTURE MANAGEMENT MARKET, BY VERTICAL

4.11 MARKET INVESTMENT SCENARIO

5 MARKET OVERVIEW AND INDUSTRY TRENDS

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Rising cloud and hybrid environment adoption

5.2.1.2 Growing cyber threat landscape and misconfiguration risks

5.2.1.3 Increasing need for compliance with strict regulatory requirements

5.2.1.4 Adoption of zero trust and risk-based frameworks

5.2.1.5 Expansion of Software-as-a-Service and Application Programming Interface ecosystems

5.2.2 RESTRAINTS

5.2.2.1 Complexity in integration with existing IT infrastructure

5.2.2.2 Tool overload and alert fatigue

5.2.2.3 Lack of skilled cybersecurity professionals

5.2.3 OPPORTUNITIES

5.2.3.1 Convergence of security platforms

5.2.3.2 Emergence of identity and data-centric security posture management

5.2.3.3 Optimizing security posture management for regulatory compliance in healthcare and finance

5.2.4 CHALLENGES

5.2.4.1 Lack of unified posture visibility across environments

5.2.4.2 Rapid expansion of shadow IT and unauthorized SaaS use

5.2.4.3 Difficulty in prioritizing and remediating risks

5.3 CASE STUDY ANALYSIS

5.3.1 MOVATE STRENGTHENS SECURITY POSTURE MANAGEMENT WITH PALO ALTO NETWORKS NEXT-GENERATION FIREWALLS AND ADVANCED ANALYTICS

5.3.2 MARICO IMPROVES SECURITY POSTURE MANAGEMENT AND USER EXPERIENCE WITH ZSCALER ZERO TRUST EXCHANGE

5.3.3 TEMPLE COLLEGE EVOLVES FROM FIREWALLS TO COMPREHENSIVE SECURITY POSTURE MANAGEMENT WITH FORTINET SECURITY FABRIC

5.3.4 D2IQ STRENGTHENS SECURITY POSTURE MANAGEMENT WITH CLOUDFLARE EMAIL SECURITY

5.3.5 SCHRODINGER INCREASES SECURITY POSTURE BY 300% IN ONLY 4 MONTHS WITH CROWDSTRIKE FALCON SHIELD

5.4 VALUE CHAIN ANALYSIS

5.4.1 COMPONENT PROVIDERS

5.4.2 PLANNING AND DESIGNING

5.4.3 INFRASTRUCTURE DEPLOYMENT

5.4.4 SYSTEM INTEGRATION

5.4.5 END-USER GROUPS

5.5 ECOSYSTEM ANALYSIS

5.6 IMPACT OF GENERATIVE AI ON SECURITY POSTURE MANAGEMENT MARKET

5.6.1 GENERATIVE AI

5.6.2 TOP USE CASES AND MARKET POTENTIAL IN SECURITY POSTURE MANAGEMENT MARKET

5.6.3 IMPACT OF GENERATIVE AI ON INTERCONNECTED AND ADJACENT ECOSYSTEMS

5.6.3.1 DevSecOps/Application Security

5.6.3.2 EDR/MDR

5.6.3.3 Cloud Security

5.6.3.4 AI/ML Analytics

5.6.3.5 IAM

5.7 PORTER'S FIVE FORCES ANALYSIS

5.7.1 THREAT OF NEW ENTRANTS

5.7.2 THREAT OF SUBSTITUTES

5.7.3 BARGAINING POWER OF SUPPLIERS

5.7.4 BARGAINING POWER OF BUYERS

5.7.5 INTENSITY OF COMPETITIVE RIVALRY

5.8 KEY STAKEHOLDERS AND BUYING CRITERIA

5.8.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.8.2 BUYING CRITERIA

5.9 PRICING ANALYSIS

5.9.1 AVERAGE SELLING PRICE OF SECURITY POSTURE MANAGEMENT OFFERINGS, BY KEY PLAYER, 2024

5.9.2 PRICING RANGE, BY KEY PLAYER, 2024

5.10 TECHNOLOGY ANALYSIS

5.10.1 KEY TECHNOLOGIES

5.10.1.1 Vulnerability Exposure Management

5.10.1.2 Configuration Assessment Engines

5.10.1.3 Risk-based Prioritization Algorithms

5.10.1.4 Security Misconfiguration Detection

5.10.1.5 Automation & Remediation Engines

5.10.2 COMPLEMENTARY TECHNOLOGIES

5.10.2.1 SIEM

5.10.2.2 SOAR

5.10.2.3 XDR

5.10.2.4 CIEM

5.10.2.5 DevSecOps/Shift-left Tools

5.10.2.6 Threat Intelligence Feeds

5.10.2.7 Policy-as-Code Engines

5.10.3 ADJACENT TECHNOLOGIES

5.10.3.1 Zero Trust Network Access

5.10.3.2 CASB

5.10.3.3 GRC

5.10.3.4 PAM

5.10.3.5 Business Continuity/Resilience Tools

5.11 PATENT ANALYSIS

5.12 REGULATORY LANDSCAPE

5.12.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.12.2 KEY REGULATIONS

5.12.2.1 PIPEDA

5.12.2.2 GDPR

5.12.2.3 PCI-DSS

5.12.2.4 CCPA

5.12.2.5 GLBA

5.12.2.6 FISMA

5.12.2.7 ISO - Standard 27001

5.12.2.8 SOC 2 Type II Compliance

5.12.2.9 SOC 2 Type II Compliance

5.13 IMPACT OF 2025 US TARIFFS-SECURITY POSTURE MANAGEMENT MARKET

5.13.1 INTRODUCTION

5.13.2 KEY TARIFF RATES

5.13.3 PRICE IMPACT ANALYSIS

5.13.4 IMPACT ON COUNTRY/REGION

5.13.4.1 North America

5.13.4.2 Europe

5.13.4.3 Asia Pacific

5.13.5 IMPACT ON END-USE INDUSTRIES

5.14 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.15 SECURITY POSTURE MANAGEMENT MARKET: BUSINESS MODELS