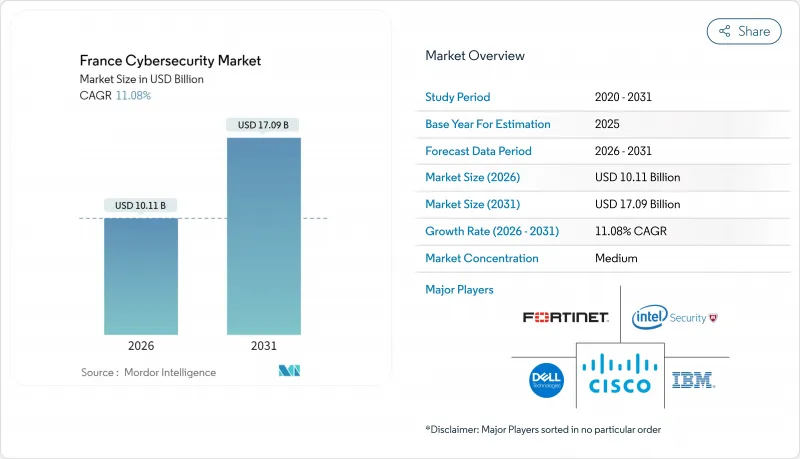

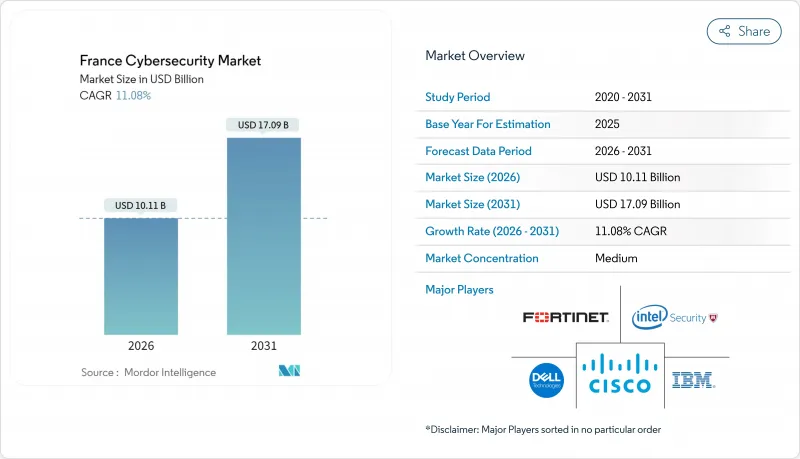

프랑스의 사이버 보안 시장은 2025년 91억 달러로 평가되었으며, 2026년 101억 1,000만 달러에서 2031년까지 170억 9,000만 달러에 이를 것으로 예상됩니다. 예측 기간(2026-2031년)에 있어서 CAGR은 11.08%를 나타낼 것으로 전망되고 있습니다.

NIS2에 근거한 규제의 급속한 확대, 공공 부문의 자금 투입 증가, 클라우드 마이그레이션의 급격한 증가가 함께 공급업체에게 잠재적인 기회가 확대되고 있습니다. 기업은 보안 스택의 통합을 지속하고 컴플라이언스 및 인력 부족 부담을 줄이는 통합 플랫폼에 대한 지출을 확대하고 있습니다. 숙련된 기술자의 만성 부족을 보완하기 위해 관리 보안 서비스에 대한 수요가 급증하는 반면, AI 구동 분석은 프랑스의 보안 운영 센터(SOC)에서 표준화가 진행되고 있습니다. 올림픽 기간 동안 사이버 활동의 활성화는 국내 위협 인식을 영구적으로 재조정하고 의료, 에너지, 운송 등 중요한 분야에서 위협 감시 인프라에 장기 투자를 촉진하고 있습니다.

NIS2에 의해 규제 대상이 500에서 약 1만 5,000의 프랑스 기업으로 확대되어 규제 대상 섹터수가 3배로 증가했습니다. 거버넌스 리스크 컴플라이언스(GRC) 도구에 대한 수요가 급증하고 있습니다. 프랑스 정부는 '프랑스 2030' 계획에서 사이버 보안 관련 17 프로젝트에 3,900만 유로(4,200만 달러)를 계상해 국가 능력 개발을 추진하고 있습니다. ANSSI(프랑스 국가 정보 보안청)의 단계적 도입 방침은 제재보다 능력 강화를 중시하고 있으며, 기업이 취약성 해소를 서두르는 가운데 컨설팅 서비스 수요를 환기하고 있습니다. 정부가 아토스의 사이버 보안 자산을 7억 유로(7억 4,800만 달러)로 취득할 의향을 보인 것은 국내 지적 재산의 전략적 가치를 더욱 강조하는 것입니다. 이러한 움직임이 결합되어 자본이 주입되고 고객 기반이 확대되고 프랑스의 사이버 보안 시장이 유럽의 컴플라이언스 거점으로서의 지위를 강화하고 있습니다.

ANSSI가 기록한 2024년 보안 인시던트는 4,386건(전년 대비 15% 증가)으로 의료 분야가 랜섬웨어 피해 보고의 10%를 차지했습니다. 알만티에르 및 코르베유-에손느의 병원에서는 긴급 정지를 강요 받고, 엔드포인트 검지와 사고 대응의 정액 계약 서비스의 필요성이 급무가 되었습니다. 루브르 미술관이나 그랑 팔레 등 문화 시설도 피해를 입어 어떠한 분야도 무연하지 않다는 것을 증명하고 있습니다. 지출은 XDR 플랫폼과 위기 관리 컨설팅으로 전환하고 있으며 프랑스의 사이버 보안 시장이 신속한 서비스 제공의 장으로 강화되고 있음을 보여줍니다.

2020년 이후 사이버 보안 인력이 89% 증가했음에도 불구하고 전국에서 약 1만 5,000건의 구인 부족이 지속되고 있습니다. 고위 분석가의 급여는 9만 유로(9만 6,300달러)에 이르며 공급자의 이익률을 압박함과 동시에 자동화를 촉진하고 있습니다. 탈레스는 GenAI4SOC를 도입하여 케이스 트리어지 효율을 40% 향상시켰습니다. 이러한 노력은 인재 부족을 완화하지만, 해소하는 것이 아니라 프랑스 사이버 보안 시장의 완전한 확대를 방해하는 요인이 되고 있습니다.

솔루션 분야는 2025년 수익의 52.10%를 차지하고 통합 위협 관리 제품군과 XDR이 기업의 도구 난립 해소에 따라 보급을 가속화했습니다. 관리 서비스 분야는 인력 부족을 보완하기 위해 24시간 감시를 외부 위탁하는 고객이 증가하고 CAGR 12.85%로 확대 중입니다. ID 액세스 관리 도구, 특히 특권 액세스 관리는 제로 트러스트 배포의 기초입니다. 예를 들어 Wallix사는 ANSSI(프랑스 국가 정보 보안청)의 인증을 활용하여 규제 대상 클라이언트를 획득하고 있습니다. 전문 서비스는 소프트웨어 지출을 보완하고 NIS2(네트워크 정보 보안 지침)의 목표 달성을 위한 평가 및 복구 프로젝트를 제공합니다. 하드웨어 어플라이언스는 기반 역할을 유지하면서 AI 구동형 분석 기능과의 통합이 진행되고 있어 프랑스의 사이버 보안 시장을 특징짓는 융합 경향을 나타내고 있습니다.

이 통합 동향은 하이브리드 소비 모델을 촉진합니다. 구매자는 핵심 플랫폼을 라이선싱하고 사고 대응을 위해 지속적인 서비스를 추가합니다. 이 접근법은 공급업체의 라이프타임 가치를 확장하는 동시에 엄격한 예산 사이클에서 유연성을 제공합니다. 랜섬웨어 공격이 격화되고 있는 가운데, 사고 대응의 지속적인 서비스는 BFSI(은행 및 금융 및 보험) 및 의료 분야에서 기본 요건이 되어, 프랑스의 사이버 보안 서비스 시장 규모를 꾸준히 밀어 올리고 있습니다.

클라우드 도입은 2025년 지출의 59.78%를 차지하며 SaaS에 대한 광범위한 선호와 중소기업의 급속한 진입을 반영했습니다. 클라우드 솔루션과 관련된 프랑스의 사이버 보안 시장 규모는 중요한 워크로드의 하이브리드 환경 전환으로 On-Premise 기반을 뛰어넘는 14.25%의 연평균 복합 성장률(CAGR)을 나타낼 것으로 예측됩니다. SecNumCloud 인증은 국내 호스팅에 대한 신뢰를 가속화하고 OVHcloud 및 Outscale과 같은 사업자에게 이익을 제공합니다.

On-Premise 모델은 데이터 거주지 및 지연 요구사항이 확장성을 능가하는 방위 및 엄격한 규제가 적용되는 유틸리티 분야에서 계속되고 있습니다. 그러나 이러한 분야에서도 기존의 제어 기능을 강화하기 위해 클라우드 기반 분석 기술이 채택되었습니다. 여러 공급업체 간에 정책을 표준화하는 멀티클라우드 오케스트레이션 플랫폼이 널리 보급되고 있으며, 단일 하이퍼스케일러를 넘어 배포하는 기업공급업체 잠금 위험을 줄일 수 있습니다. 그 결과, 프랑스의 사이버 보안 시장에서는 기존의 도입 형태의 경계가 더욱 모호해지고, 제어 플레인 중심의 아키텍처로 이행이 진행되고 있습니다.

프랑스의 사이버 보안 시장 보고서는 제공 형태(솔루션, 서비스), 도입 모드(On-Premise, 클라우드), 최종 사용자 업종(은행, 금융서비스 및 보험(BFSI), 의료, IT 및 통신, 산업 및 방위, 제조, 소매·E커머스, 에너지 및 유틸리티, 기타), 최종 사용자 기업 규모(중소기업(SME), 대기업)에 의해 업계를 세분화하고 있습니다.

The France cybersecurity market was valued at USD 9.10 billion in 2025 and estimated to grow from USD 10.11 billion in 2026 to reach USD 17.09 billion by 2031, at a CAGR of 11.08% during the forecast period (2026-2031).

Rapid regulatory expansion under NIS2, heavier public-sector funding, and a sharp rise in cloud migration are synchronizing to widen the addressable opportunity for vendors. Enterprises continue to consolidate security stacks, channeling spending toward integrated platforms that ease compliance and talent pressures. Managed security services are surging as buyers offset a persistent shortage of skilled practitioners, while AI-driven analytics are becoming standard in French security operations centers. Heightened Olympic-period cyber activity has permanently recalibrated domestic threat awareness, prompting long-term investment in threat-monitoring infrastructure across critical sectors such as healthcare, energy, and transportation.

NIS2 widens the compliance net from 500 to roughly 15,000 French entities, tripling the number of regulated sectors and intensifying demand for governance, risk, and compliance tooling. France 2030 earmarked EUR 39 million (USD 42 million) for 17 cybersecurity projects, anchoring sovereign capability development. ANSSI's phased roll-out stresses enablement over sanction, spurring advisory services as firms race to close gaps. Government interest in acquiring Atos' cybersecurity assets for EUR 700 million (USD 748 million) further underlines the strategic value of domestic IP. Together these moves inject capital, enlarge the client base, and reinforce the France cybersecurity market as a continental compliance hub.

ANSSI logged 4,386 security incidents in 2024, up 15% year on year, with healthcare representing 10% of ransomware filings. Hospitals at Armentieres and Corbeil-Essonnes endured emergency shutdowns, driving urgency around endpoint detection and incident-response retainer services. Cultural landmarks such as the Louvre and Grand Palais also faced disruptions, proving no sector is immune. Spending is pivoting toward XDR platforms and crisis-management consulting, reinforcing the France cybersecurity market as a responsive services arena.

Roughly 15,000 cybersecurity vacancies persist nationwide, despite an 89% workforce expansion since 2020. Salary inflation reaches EUR 90,000 (USD 96,300) for senior analysts, squeezing provider margins and stimulating automation. Thales responded with GenAI4SOC to improve case triage efficiency by 40%. Such initiatives temper, but do not erase, the talent gap that restrains the France cybersecurity market's ability to scale fully.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solutions generated 52.10% of 2025 revenue, with unified threat-management suites and XDR gaining traction as enterprises rationalize tool sprawl. The managed-services slice is growing at 12.85% CAGR as clients contract out 24/7 monitoring to compensate for staffing gaps. Identity-and-access tools, especially privileged-access management, underpin Zero-Trust rollouts. Wallix, for example, leverages its ANSSI qualification to court regulated clients. Professional services complement software spend, delivering assessment and remediation projects tied to NIS2 milestones. Hardware appliances remain foundational but are increasingly bundled with AI-driven analytics, illustrating the convergence that defines the France cybersecurity market.

The integration trend is fostering hybrid consumption models in which buyers license core platforms and overlay retained services for incident response. This approach expands lifetime value for vendors while providing flexibility in tight budget cycles. As ransomware campaigns intensify, incident-response retainers are now a baseline requirement across BFSI and healthcare, pushing the France cybersecurity market size for services steadily upward.

Cloud deployments accounted for 59.78% of 2025 spending, reflecting widespread SaaS preference and rapid SME onboarding. The France cybersecurity market size attached to cloud solutions is forecast to rise at a 14.25% CAGR, outpacing the on-premise base as more critical workloads move to hybrid environments. SecNumCloud certification accelerates trust in domestic hosting, benefiting players such as OVHcloud and Outscale.

On-premise models persist in defense and heavily regulated utilities where data residency and latency demands outweigh elasticity. Yet even these sectors adopt cloud-based analytics to augment legacy controls. Multi-cloud orchestration platforms that normalize policy across providers are gaining lift, mitigating vendor lock-in risks for enterprises expanding beyond a single hyperscaler. As a result, the France cybersecurity market continues to blur traditional deployment lines, pivoting toward control-plane-centric architectures.

The France Cybersecurity Market Report Segments the Industry Into by Offering (Solutions, and Services), Deployment Mode (On-Premise, and Cloud), End-User Vertical (BFSI, Healthcare, IT and Telecom, Industrial and Defense, Manufacturing, Retail and E-Commerce, Energy and Utilities, Manufacturing, and Others), and End-User Enterprise Size (Small and Medium Enterprises (SMEs), and Large Enterprises)