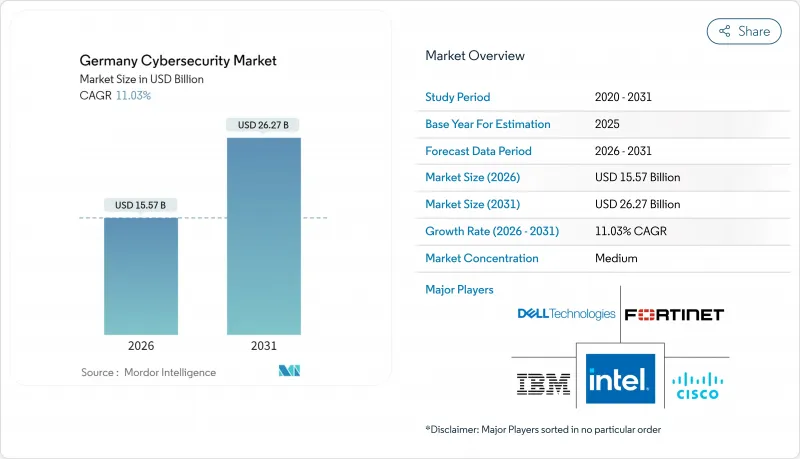

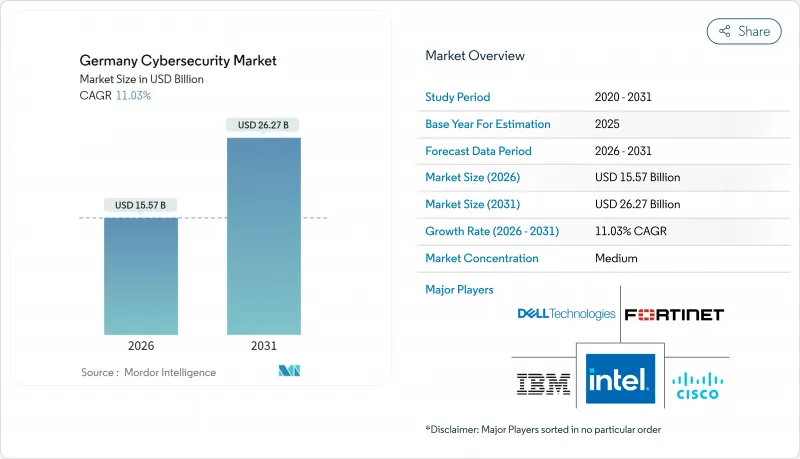

독일의 사이버 보안 시장 규모는 2026년 155억 7,000만 달러로 추정되고, 2025년 140억 2,000만 달러에서 성장할 전망이며, 2031년에는 262억 7,000만 달러에 이를 것으로 예측됩니다. 2026-2031년 연평균 성장률(CAGR)은 11.03%로 성장할 전망입니다.

2024년 내내 연방정보보안청(BSI)은 7만 2,000건의 사고보고서를 기록해 전년 대비 21% 증가했습니다. 한편, 동청의 Produkt-KOMPASS에서는 2만 4,531건의 공개 취약성이 등록되어 그 중 15%가 '중대'로 분류됐습니다. 2025-2027년 74억 유로의 의무적 지출이 발생할 전망입니다. 감독 체제도 동시에 강화되고 있으며, DAX 구성 기업의 68%가 2024년에 이사회 수준의 사이버 보안 위원회를 설치했습니다(2022년은 42%). 이러한 거버넌스 노력은 예산 승인을 조기화하고 독일 사이버 보안 시장 전체에서 핵심 IT 설비 투자에 보호 라인을 통합하도록 촉구하고 있습니다.

연방 통계국의 보고서에 따르면 클라우드 이용 기업은 2021년 54%에서 2024년 69%로 증가했습니다. 부처가 국내 데이터 보관 규칙을 강화한 결과, 공공기관의 소블린 클라우드 계약은 지난해 27% 확대되었습니다. 조직에서는 AI와 보호 예산을 단일 운영위원회에서 통합하는 움직임도 진행되어 이 통합이 독일 사이버 보안 시장 전체의 지출 확대를 뒷받침할 것으로 전망됩니다.

독일의 온라인 접근법은 2026년까지 575개의 연방 및 지자체 서비스를 디지털 방식으로 제공해야 합니다. 2024년 12월 현재 이러한 서비스의 41%가 이미 Open Telekom Cloud에서 실행 중이었습니다. 대학 병원에서는 이미지 데이터 세트를 아카이브하기 위해 하이브리드 클라우드 스토리지를 연간 94페타바이트로 확장했습니다. 모든 신규 워크로드는 BSI C5 보안 프레임워크를 준수해야 하며, 2024년 동안 인증 제공업체는 23개에서 34개로 증가했습니다. 인증 프로세스의 신속화는 조달상의 마찰을 줄이고 추가적인 전환을 촉진합니다. 이는 독일의 사이버 보안 시장 전반에서 라이선스 수요와 컨설팅 수요의 직접적인 증가로 이어집니다.

VDMA의 보고서에 따르면 스마트 센서의 도입률은 2024년 생산 라인의 71%에 달했습니다. IW 쾰른 연구소의 계산에 따르면 자동차 공장의 평균 가동 중지 시간 비용은 시간당 EUR 290,000에 이릅니다. 자산 발견 플랫폼은 현재 국내에서 230만 점의 중요한 산업 기기를 맵핑하고 있으며 수동 모니터링의 도입 기반을 구축하고 있습니다. 종합 설비 효율(OEE) 산출에 사이버 보호 대책을 통합함으로써, 제조자는 재량적인 IT 예산에서 필수 운영 보호로 자금을 옮겨 독일의 사이버 보안 시장 내에서 산업 등급 솔루션에 대한 수익 경사를 촉진하고 있습니다.

독일에서는 2025년 시점에서 9만 6,300건의 IT 보안직이 미충족으로 전년대비 25% 증가하고 있습니다. 뮌헨의 수석 SOC 분석가들의 평균 연봉은 96,000유로로 2019년 대비 57% 상승했습니다. 28개 대학이 전문 학위를 수여하고 있으며, 연간 3,400명의 졸업생만이 노동 시장에 참가하여, 수요의 7%만 채웠습니다. 이 인력 부족으로 기업 예산에는 고수준의 임금 하한이 통합되어 지출은 자동화, SOC-as-a-service, 매니지드 감지 서비스로 향하고 있습니다. 이로 인해 이익률이 억제되지만 독일 사이버 보안 시장에서 서비스 제공 업체의 수익을 지원합니다.

2025년 독일 사이버 보안 시장 점유율에서 솔루션 분야는 66.05%(92억 6,000만 달러)를 차지했습니다. 한편, 매니지드 보안 서비스는 37억 1,000만 달러의 수익을 낳고, 18.12%의 성장 곡선을 묘사하고 있습니다. 기업은 또한 16만 4,000대의 BSI 인증 차세대 방화벽을 구입했으며 출하량은 14% 증가했습니다. 서비스 수익은 점점 더 사용량 기반으로 전환하고 있으며 독일 텔레콤에 따르면 2024년 보안 계약의 42%가 고정 요금이 아닌 종량제였습니다. 공급자의 인센티브를 실제 위협 상황에 연동시킴으로써 독일의 사이버 보안 시장 전반에 걸쳐 지속적인 최적화 및 장기적인 고객 정착이 보장됩니다.

MSS(Managed Security Services) 수요는 중앙정부가 2024년 6억 8,000만 유로의 SOC 프레임워크 발주를 통해 더욱 가속화되어 벤더의 규모 확대로 이어지고 있습니다. 소프트웨어 정의 경계(SDP)와 제로 트러스트의 파일럿 도입에 대한 의존도가 높아지는 가운데, 대부분의 사내 팀에서는 대응이 곤란한 24시간 365일의 정책 조정이 필요해, 외부 위탁 SOC 능력에 대한 수요가 가속하고 있습니다.

2025년 현재 온프레미스 및 프라이빗 클라우드 환경은 독일 사이버 보안 시장 규모의 52.85%(74억 1,000만 달러)를 차지했습니다. 한편, 퍼블릭 클라우드 보안은 16.52%의 연평균 복합 성장률(CAGR)을 나타냅니다. 유로스타트 조사에 따르면 독일 기업의 46%가 퍼블릭 클라우드에 어떠한 데이터를 저장하고 있는 것, 핵심적인 재무 기록을 맡고 있는 기업은 불과 11%에 머물고 있습니다. 캡 제미니 설문조사에서는 현지 호스팅 서비스에는 18%의 프리미엄이 설정되어 있지만, 도입 기업의 58%가 가격 상승을 받아들이고 있습니다.

Eco eV의 추정에 따르면 72%의 기업이 전환 단계에서 두 개의 SIEM 플랫폼을 운영하고 있습니다. 온프레미스 및 클라우드 텔레메트리를 통합하는 공급업체는 2024년 41%의 새로운 ARR 성장을 기록했습니다. 이 듀얼 스택의 현실은 복잡성을 고정화하고 단일 제품보다 확장 가능한 플랫폼을 우월하게 함과 동시에 독일 사이버 보안 시장을 이끄는 '주권 우선'의 철학을 강화하고 있습니다.

독일의 사이버 보안 시장 보고서는 제공 형태별(솔루션, 서비스), 전개 모드별(클라우드, 온프레미스), 최종 사용자 산업별(은행, 금융서비스 및 보험(BFSI), 의료, IT 및 통신, 산업 및 방위, 제조, 소매 및 전자상거래, 에너지 및 유틸리티 등), 최종 사용자 기업 규모별(중소기업(SME), 대기업)로 업계를 세분화하고 있습니다.

The German Cybersecurity market size in 2026 is estimated at USD 15.57 billion, growing from 2025 value of USD 14.02 billion with 2031 projections showing USD 26.27 billion, growing at 11.03% CAGR over 2026-2031.

Across 2024, the Federal Office for Information Security (BSI) logged 72,000 incident reports, a 21% jump on the prior year, while its Produkt-KOMPASS registered 24,531 published vulnerabilities, 15% of which were labelled critical . Fresh statutes-most notably the NIS2 Implementation and Cyber Security Strengthening Act, the Digital Operational Resilience Act and BaFin's updated IT requirements-unlock EUR 7.4 billion of compulsory outlays between 2025 and 2027. Oversight is tightening in parallel; 68% of DAX constituents created a board-level cybersecurity committee in 2024, up from 42% in 2022. These governance moves encourage earlier budget sign-off and embed protection lines within core IT capex across the German Cybersecurity market.

The Federal Statistical Office reported cloud use by 69% of companies in 2024, compared with 54% in 2021. Sovereign-cloud contracts inside public agencies expanded 27% last year as ministries tightened domestic-data-residency rules. Organizations also fuse AI and protection budgets under single steering committees, and that integration is expected to reinforce spending momentum across the German Cybersecurity market.

Germany's Online Access Act mandates digital delivery of 575 federal and municipal services by 2026. By December 2024, 41% of those services already ran on Open Telekom Cloud. University hospitals raised hybrid-cloud storage to 94 petabytes over the year to archive imaging datasets. All new workloads must conform to the BSI C5 security framework, whose list of certified providers grew from 23 to 34 during 2024. Faster certification lowers procurement friction and fuels additional migrations, translating directly into higher license and consulting demand across the German Cybersecurity market.

The VDMA reported that smart-sensor adoption reached 71% of production lines in 2024. IW Cologne pegged average downtime costs at EUR 290,000 per hour in automotive plants. Asset-discovery platforms now map 2.3 million critical industrial components nationwide, underpinning passive-monitoring adoption. By integrating cyber safeguards in overall-equipment-effectiveness calculations, manufacturers shift budgets from discretionary IT to mandatory operational protection, tilting revenue towards industrial-grade solutions inside the German Cybersecurity market.

Germany entered 2025 with 96,300 open IT-security positions, 25% higher than a year earlier. Senior SOC analysts in Munich command average pay of EUR 96,000, 57% above 2019 levels. Although 28 universities award specialist degrees, only 3,400 graduates enter the workforce annually, covering 7% of demand. Scarcity hardwires elevated wage floors into corporate budgets and directs spending towards automation, SOC-as-a-service and managed detection, which tempers margins yet supports service-provider revenues in the German Cybersecurity market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solutions accounted for 66.05% of 2025 German Cybersecurity market share, equal to USD 9.26 billion, while managed security services produced USD 3.71 billion and are pacing an 18.12% expansion curve. Companies also bought 164,000 BSI-certified next-generation firewalls, a 14% shipment gain. Service revenue is increasingly usage-based; Deutsche Telekom said that 42% of 2024 security bookings were metered rather than fixed-fee. Aligning provider incentives with live threat conditions ensures continuous optimisation and long-term stickiness across the German Cybersecurity market.

MSS engagement is further fuelled by central government placing EUR 680 million of SOC framework orders in 2024, which broadens vendor scale. The growing reliance on software-defined perimeters and zero-trust pilots requires 24/7 policy tuning unavailable in most internal teams, accelerating demand for outsourced SOC capacity.

On-premise and private-cloud instances retained 52.85% of the German Cybersecurity market size in 2025, or USD 7.41 billion, even as public-cloud security exhibits a 16.52% CAGR. Eurostat shows 46% of German firms storing some data in the public cloud, yet only 11% entrust core financial records. Capgemini measured an 18% premium for locally hosted services, but 58% of adopters accept the higher price.

Eco e.V. estimates that 72% of enterprises operate two SIEM platforms during transition phases. Vendors that unify on-premise and cloud telemetry registered 41% new ARR growth in 2024. This dual-stack reality entrenches complexity, favouring extensible platforms over point products and reinforcing the sovereign-first ethos guiding the German Cybersecurity market.

The Germany Cyber Security Market Report Segments the Industry Into by Offering (Solutions, and Services), Deployment Mode (Cloud, and On-Premise), End-User Vertical (BFSI, Healthcare, IT and Telecom, Industrial and Defense, Manufacturing, Retail and E-Commerce, Energy and Utilities, and Others), and End-User Enterprise Size (Small and Medium Enterprises (SMEs), and Large Enterprises).