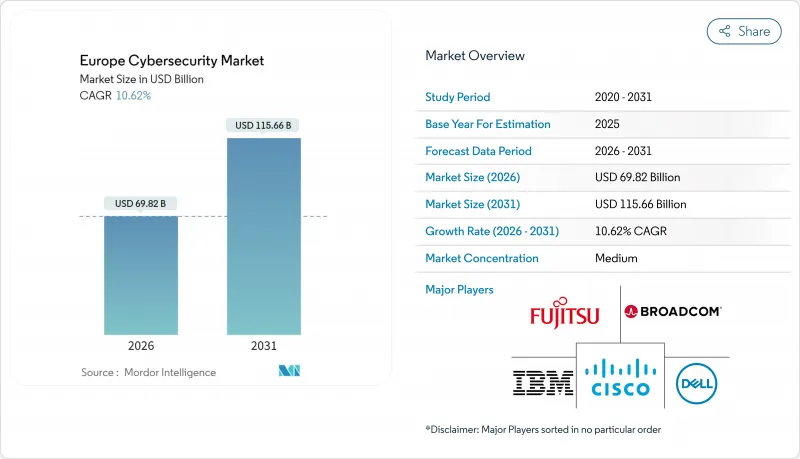

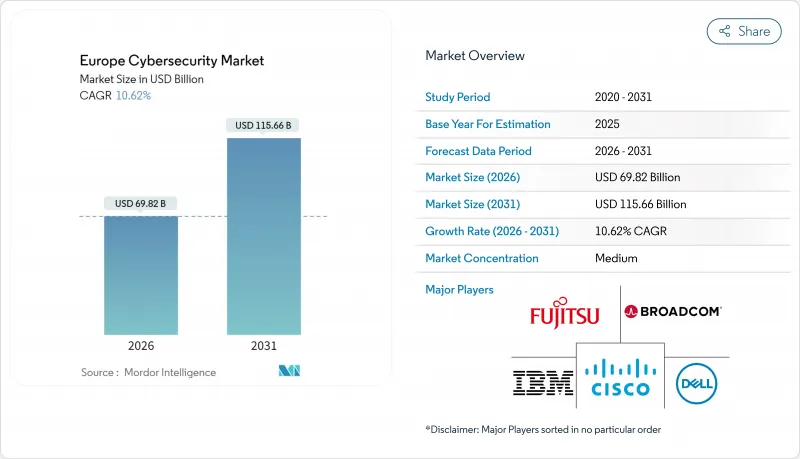

유럽의 사이버 보안 시장 규모는 2026년 698억 2,000만 달러로 추정되고 있습니다. 이는 2025년 631억 2,000만 달러에서 성장했으며, 2031년에는 1,156억 6,000만 달러에 이를 것으로 예측됩니다. 2026-2031년 CAGR 10.62%로 확대가 전망되고 있습니다.

의무적 규제, 증가하는 지정학적 위험, 그리고 소블린 클라우드 플랫폼으로의 전환 가속화로 인해 사이버 보안은 지역 전반에 걸쳐 모든 지출에서 핵심 운영 경비로 상승하고 있습니다. 네트워크 및 정보 보안 지령 2(NIS2) 및 디지털 운영 탄력성 법(DORA) 시행이 지출 계획의 기반을 굳히는 한편, 러시아와 우크라이나 분쟁은 랜섬웨어 피해를 30% 증가시켜 이사회 수준의 리스크 인식을 높이고 있습니다. 클라우드 퍼스트 전략은 계속되는 한편, 기업이 주권과 규모의 균형을 맞추고 있는 가운데 하이브리드 전개가 기세를 늘리고 있습니다. 공급업체 통합은 컴플라이언스 수요에 대응하기 때문에 공급업체가 사고 대응 및 관리 서비스 능력을 획득함에 따라 치열해지고 있습니다. 그러나 29만 9,000명 규모의 전문가 부족으로 경쟁의 격화는 완화되고 있으며, 이는 내부 보안팀의 부담을 증대시키는 동시에 관리 서비스의 채용을 뒷받침하고 있습니다.

NIS2는 적용대상을 유럽 16만 이상의 사업체로 확대하여 최대 1,000만 유로 또는 세계 매출의 2%에 해당하는 벌칙을 도입했습니다. 이로 인해 사이버 보안 예산이 임의 지출에서 의무 지출로 전환됩니다. DORA는 금융기관에 병행하는 ICT 리스크 관리 의무를 부과하고, 벨피우스 은행 등 은행 업계는 탄력성 강화를 위해 벤더 포트폴리오의 재구축을 강요받고 있습니다. 법적 요건에 따라 평균 보안 지출은 IT 예산의 9%에 이르렀으며 89%의 기업이 신규 채용의 필요성을 보고했습니다. 통합 지원 플랫폼 및 관리형 서비스는 여러 관할 구역에 대한 보고를 효율화하고, 컴플라이언스를 유지하며, 처벌 위험을 줄이기 위해 가장 혜택을 받고 있습니다.

유럽 조직에 대한 랜섬웨어 공격은 위협 행위자가 지정학적 긴장을 악용한 결과 2024년 30% 증가했습니다. 제조업에서는 2025년 1분기에 공격 건수가 84% 증가했고, 침해 비용은 556만 달러를 넘어 과거의 위기 시 손실을 웃돌았습니다. 의료 분야의 사고는 2023년에 309건에 달했고, 절반이 랜섬웨어 관련이었기 때문에 EU는 추가적인 사고 대응 자원을 할당하는 행동 계획을 수립했습니다. LockBit과 같은 지속적인 그룹은 적발 전에 1,700건의 공격을 수행했으며, 행동 기반 감지와 다층 대응 서비스의 필요성이 부각되었습니다.

유럽에서는 29만 9,000명 이상의 유자격 사이버 보안 전문가가 부족하고 현직 직원의 76%가 정식 자격을 보유하고 있지 않습니다. 독일에서는 지출이 2자리 증가를 보임에도 불구하고 구인을 채우는 데 어려움을 겪고 있으며, 프랑스에서는 급여가 9만 8,100달러에 다가오고 있음에도 불구하고 1만 5,000건의 구인 범위가 예상됩니다. 기술 부족으로 인해 특히 클라우드 보안 및 OT 보호 분야에서의 프로젝트 전개가 늦어지고, 기업은 사내 능력의 대안으로서 매니지드 검지 및 대응 서비스로의 이행을 강요받고 있습니다.

2025년 유럽 사이버 보안 시장 점유율의 67.25%를 솔루션이 차지하였고, 클라우드 ID 네트워크 제어를 통합 콘솔에 집약하는 통합 플랫폼이 이를 지원하고 있습니다. 매니지드 검지 및 대응을 포함한 서비스 분야의 유럽 사이버 보안 시장 규모는 기업이 일상 업무를 외부 위탁함으로써 인력 부족을 보완하는 움직임에서 2031년까지 연평균 복합 성장률(CAGR) 13.56%로 확대될 것으로 예측되고 있습니다. 고성장 요인은 NIS2의 적용 범위에 새롭게 포함된 중견 기업이며, 여러 공급업체의 툴킷보다 단일 구독 서비스 번들을 선호하는 경향이 있습니다.

Managed Service Provider는 EU의 다양한 규제 시스템에 걸친 증거 수집을 자동화하는 컴플라이언스 대시보드를 사용자 정의합니다. 동시에 대형 은행 및 제조업체가 제로 트러스트 참조 모델과 포스트 양자암호 로드맵을 구축하는 동안 전문 서비스 수요는 견조합니다. 워크플로우 자동화 및 네이티브 보고 기능을 통합한 통합 솔루션 공급업체는 크로스셀 이점을 누리지만, 틈새 단일 제품 공급업체는 통합 압력에 직면합니다.

클라우드 도입은 기업이 탄력성과 상시 갱신을 중시한 결과 2025년 수익의 56.90%를 차지했습니다. 하이브리드 모델은 현재 15.03%라는 가장 빠른 CAGR을 기록하고 있습니다. 이는 주권 규칙에 따라 기업이 기밀 데이터를 EU 영역 내에 유지하면서 세계의 하이퍼스케일러 분석 기능을 지속적으로 활용해야 하기 때문입니다. 금융기관이 양자 내성 메트로네트워크의 시험 운영을 진행하는 가운데 하이브리드 아키텍처의 유럽 사이버 보안 시장 규모는 확대되고 있습니다. 이 네트워크는 온프레미스에 키를 유지하면서 원격 측정 데이터를 주권 클라우드의 분석 엔진으로 라우팅합니다.

하드웨어의 완전한 제어가 필요한 방위 및 공공 부문 워크로드에서는 온프레미스 설치가 여전히 주류입니다. 그러나 이러한 환경에서도 클라우드 기반 위협 인텔리전스 피드가 통합되어 복합 토폴로지를 형성합니다. 이를 통해 공급업체는 SaaS와 어플라이언스 모두에서 동일한 정책 엔진을 제공하여 관리자가 워크로드 위치에 관계없이 통합 제어를 적용할 수 있습니다.

유럽의 사이버 보안 시장 보고서는 제공 형태별(솔루션, 서비스), 전개 모드별(온프레미스, 클라우드), 최종 사용자 산업별(은행, 금융서비스 및 보험(BFSI), 의료, IT 및 통신, 산업 및 방위, 제조, 소매 및 전자상거래, 에너지 및 유틸리티 등), 최종 사용자 기업 규모(중소기업(SME), 대기업)에 의해 업계를 세분화하고 있습니다. 또한 국가별로 분류하고 있습니다.

Europe cybersecurity market size in 2026 is estimated at USD 69.82 billion, growing from 2025 value of USD 63.12 billion with 2031 projections showing USD 115.66 billion, growing at 10.62% CAGR over 2026-2031.

Mandatory regulation, rising geopolitical risk, and an accelerating shift to sovereign cloud platforms elevate cybersecurity from optional spend to core operational outlay across the region. Enforcement of the Network and Information Security Directive 2 (NIS2) and the Digital Operational Resilience Act (DORA) anchors spending plans, while the Russia-Ukraine conflict fuels a 30% rise in ransomware incidents that heightens board-level risk awareness. Cloud-first strategies persist, yet hybrid deployments gain traction as enterprises balance sovereignty with scale. Vendor consolidation intensifies as suppliers acquire incident-response and managed-services capabilities to meet compliance demand. Heightened competition, however, is tempered by a 299,000-professional skills deficit that stretches internal security teams and bolsters managed service uptake.

NIS2 expands coverage to more than 160,000 European entities and introduces penalties of up to EUR 10 million or 2% of global turnover, which is shifting cybersecurity budgets from discretionary to compulsory . DORA imposes parallel ICT-risk mandates on financial entities, forcing banks such as Belfius to restructure vendor portfolios for resilience. The legal scope drives average security spending to 9% of IT budgets, while 89% of firms report new hiring needs. Integration-ready platforms and managed services benefit most because they streamline multi-jurisdiction reporting, sustain compliance, and reduce penalty exposure.

Ransomware attacks on European organizations climbed 30% in 2024 as threat actors weaponized geopolitical tensions. Manufacturing bore 84% growth in strike volume during Q1 2025 with breach costs topping USD 5.56 million, eclipsing previous crisis-era losses. Healthcare incidents reached 309 in 2023, half involving ransomware, prompting an EU action plan that allocates additional incident-response resources. Persistent groups such as LockBit executed 1,700 attacks before takedown efforts, underlining the need for behavior-based detection and layered response services.

Europe lacks more than 299,000 qualified cybersecurity professionals, and 76% of existing staff possess no formal credentials. Germany posts double-digit growth in spending yet struggles to fill vacancies, while France expects 15,000 open roles despite salaries approaching USD 98,100. Skills scarcity slows project rollouts, particularly in cloud security and OT protection, compelling enterprises to shift toward managed detection and response as a substitute for in-house capability.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solutions accounted for 67.25% of the Europe cybersecurity market share in 2025, underpinned by integrated platforms that bundle cloud, identity, and network controls into unified consoles. The Europe cybersecurity market size for services, including managed detection and response, is projected to expand at a 13.56% CAGR to 2031 as enterprises offset workforce shortages by outsourcing daily operations. High-growth comes from mid-market firms newly covered under NIS2 that prefer single-subscription service bundles over multi-vendor toolkits.

Managed services providers tailor compliance dashboards that automate evidence collection across the EU's heterogeneous regulatory regimes. Concurrently, professional-services demand remains steady as large banks and manufacturers architect zero-trust reference models and post-quantum roadmaps. Integrated solution vendors that embed workflow automation and native reporting enjoy cross-sell advantage, while niche point-product suppliers face consolidation pressure.

Cloud deployments represented 56.90% of 2025 revenue as enterprises embraced elasticity and evergreen updates. Hybrid models now register the swiftest 15.03% CAGR because sovereignty rules compel companies to retain sensitive data inside EU borders while still tapping global hyperscaler analytics. The Europe cybersecurity market size for hybrid architectures grows as financial institutions pilot quantum-secure metro networks that keep keys on premises yet route telemetry to analytics engines in sovereign clouds.

On-premise installations persist in defense and public-sector workloads that require full control of hardware. Yet even these environments integrate cloud-based threat intelligence feeds, creating blended topologies. Vendors therefore package identical policy engines across SaaS and appliance form factors so administrators can enforce uniform controls regardless of workload location.

The Europe Cybersecurity Market Report Segments the Industry Into by Offering (Solutions, and Services), Deployment Mode (On-Premise, and Cloud), End-User Vertical (BFSI, Healthcare, IT and Telecom, Industrial and Defense, Manufacturing, Retail and E-Commerce, Energy and Utilities, Manufacturing, and Others), and End-User Enterprise Size (Small and Medium Enterprises (SMEs), and Large Enterprises). And Country.