할랄 인증 단백질 가수분해물 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)

Halal-Certified Protein Hydrolysates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1876653

리서치사:Global Market Insights Inc.

발행일:2025년 11월

페이지 정보:영문 210 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

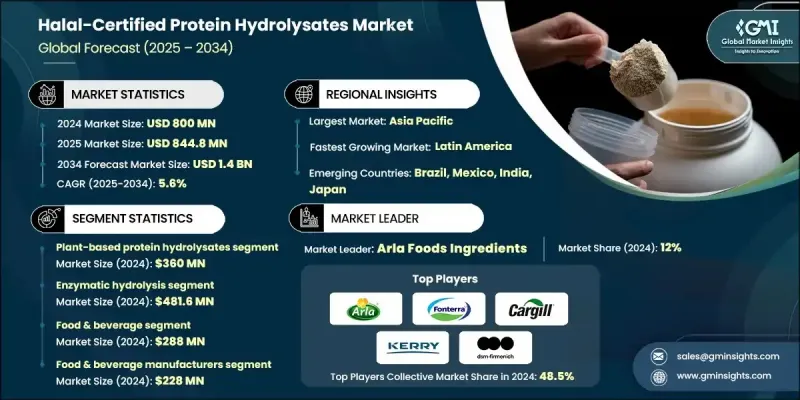

세계의 할랄 인증 단백질 가수분해물 시장은 2024년에 8억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 5.6%로 성장할 전망이며, 14억 달러에 이를 것으로 예측되고 있습니다.

건강 의식이 높아지고 깨끗한 라벨과 기능성 원료에 대한 수요 증가로 시장은 확대 경향이 있습니다. 소비자가 단백질의 소화성, 근육 회복, 장내 환경에 대한 관심을 강화하고 있는 것은 스포츠 영양, 영양 보조 식품, 임상 영양 분야에서의 성장을 가속하고 있습니다. 효소 가수분해 기술의 발전은 공정 효율 및 제품 품질 향상을 통해 시장 구조를 변화시키고 있습니다. 현대의 효소 기반 시스템은 펩티드 분해를 제어할 수 있어 생체이용률이 높고 오프플레이버가 적은 가수분해물을 생성합니다. 세계의 식품 원료 제조업체는 할랄 대응을 실현하고 정밀 영양학과 깨끗한 생산을 가능하게 하기 위해 효소 가수분해 공정을 적응시키고 있습니다. 영아 영양 및 임상 영양 분야에서 할랄 인증 가수분해물의 이용 확대도 시장의 채용을 촉진하고 있으며, 이들은 알레르겐성을 감소시켜 영양소 흡수를 개선합니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 시 가치

8억 달러

예측 금액

14억 달러

CAGR

5.6%

식물 유래 단백질 가수분해물은 지속가능하고 윤리적이며 알레르겐이 없는 단백질원에 대한 소비자의 선호도 증가로 인해 2024년에는 3억 6,000만 달러를 차지했습니다. 유당 불내증, 비가니즘, 환경 의식이 증가함에 따라 제조업체는 동물성 단백질을 대두, 완두콩 및 쌀 유래의 가수분해물로 대체하도록 촉구되고 있습니다. 할랄 인증의 용이성, 원료 가용성, 단순화된 제조 공정으로 식물성 가수분해물은 음료, 기능성 식품, 스포츠 영양 용도 분야에 이상적입니다.

효소 가수분해 부문은 2024년에 4억 8,160만 달러에 달했습니다. 이는 특이성과 영양적 완전성을 손상시키지 않고 고품질의 생물학적 활성 단백질 가수분해물을 생산할 수 있는 능력 때문입니다. 이 방법을 통해 제조업체는 펩티드 사슬의 길이와 조성을 조절할 수 있으며, 영양 보충제, 임상 식품 및 스포츠 영양 식품의 소화성 및 기능성을 향상시킬 수 있습니다. 또한, 효소 가수분해는 화학 촉매를 사용하지 않기 때문에 할랄 기준에 적합하며 할랄 인증 생산 라인에서 사용하기에 적합합니다.

북미의 할랄 인증 단백질 가수분해물 시장은 2024년 1억 2,000만 달러(15% 점유율)를 기록했습니다. 미국은 성숙한 식품가공 산업, 기능성 및 클린 라벨 원료에 대한 높은 소비자 수요, 증가하는 무슬림 인구에 의해 1억 80만 달러를 공헌하고 있습니다. 피트니스 지향 소비자층에서 할랄 인증 영양 보조 식품에 대한 인지도 향상도 이 지역 시장 성장을 견인하고 있습니다.

세계의 할랄 인증 단백질 가수분해물 시장의 주요 기업으로는 Arla Foods Ingredients, ADM(Archer Daniels Midland), Cargill Incorporated, Actus Nutrition, Fonterra Co-operative Group, Glanbia PLC, Friesland Campina, Abbott Laboratories, Roquette Freres, DSM-Firmenich, Kerry Group, Agropur Cooperative 등이 있습니다. 할랄 인증 단백질 가수분해물 부문의 기업들은 그 존재감을 강화하기 위해 효소 가수분해 효율, 펩티드의 생체이용률 및 클린 라벨의 배합을 개선하기 위한 연구개발에 주력하고 있습니다. 식품 제조업체, 영양 브랜드, 임상 영양 공급자와의 전략적 제휴는 유통 네트워크의 확대에 기여하고 있습니다. 또한 기업은 컴플라이언스 및 확장성을 보장하기 위해 할랄 인증 프로세스, 지역 생산 시설 및 원재료 조달에 투자하고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

높아지는 건강 의식 및 클린 라벨에 대한 수요

효소 가수분해에 있어서 기술적 진보

영아 영양 및 임상 영양 분야에 있어서 용도 확대

업계의 잠재적 위험 및 과제

생산 비용 상승 및 가격 프리미엄

할랄 인증 원료의 한정된 이용가능성

시장 기회

식물성 단백질 가수분해물의 성장 가능성

디지털 추적 가능성 및 블록체인 통합

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

가격 동향

지역별

제품

장래 시장 동향

기술 및 혁신 동향

현재의 기술 동향

신흥 기술

특허 상황

무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

주요 수입국

주요 수출국

지속가능성 및 환경면

지속가능한 대처

폐기물 감축 전략

생산에 있어서 에너지 효율

환경에 배려한 대처

탄소발자국에 관한 고려 사항

제4장 경쟁 구도

서문

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병 및 인수

제휴 및 협업

신제품 발매

사업 확대 계획

제5장 시장 추계 및 예측 : 원료 유형별(2021-2034년)

주요 동향

식물성 단백질 가수분해물

완두콩 단백질 가수분해물

콩 단백질 가수분해물

쌀 단백질 가수분해물

헬프 단백질 가수분해물

기타 식물성 원료

동물성 단백질 가수분해물

유청 단백질 가수분해물

카제인 가수분해물

소 유래 단백질 가수분해물

가금 단백질 가수분해물

해양성 단백질 가수분해물

물고기 단백질 가수분해물

새우 및 갑각류 가수분해물

기타 해양 유래 원료

미생물 유래 단백질 가수분해물

제6장 시장 추계 및 예측 : 가공 기술별(2021-2034년)

주요 동향

효소 가수분해

미생물 효소 시스템

식물 유래 효소계

고정화 효소 기술

산 가수분해

알칼리 가수분해

기타

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

주요 동향

유아용 영양 식품

고도 가수분해 조제분유

부분 가수분해 조제분유

저 알레르기성 제품

스포츠 영양

프리워크아웃 보충제

트레이닝 후의 회복 제품

단백질 파우더 및 셰이크

임상 및 의료영양학

경장 영양 제품

의료용 식품

전문적인 식사 관리

영양보조식품 및 뉴트라슈티컬

캡슐 및 정제

분말보충제

기능성 식품

식음료 원료

풍미 증강제

단백질 강화

유화제 및 안정제

화장품 및 퍼스널케어

안티에이징 제품

헤어 케어 제품

스킨 케어 용도

제8장 시장 추계 및 예측 : 최종 이용 산업별(2021-2034년)

주요 동향

식음료 제조업체

의약품

영양 보조 식품 및 보충제 제조업체

화장품 및 퍼스널케어

사료 및 반려동물 식품

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제10장 기업 프로파일

Arla Foods Ingredients

Fonterra Co-operative Group

Cargill Incorporated

Kerry Group

DSM-Firmenich

ADM(Archer Daniels Midland)

Actus Nutrition

FrieslandCampina

Agropur Cooperative

Roquette Freres

Abbott Laboratories

Glanbia PLC

AJY

영문 목차

영문목차

The Global Halal-Certified Protein Hydrolysates Market was valued at USD 800 million in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 1.4 billion by 2034.

The market is witnessing expansion due to rising health awareness and the increasing demand for clean-label, functional ingredients. Consumers are becoming more conscious of protein digestibility, muscle recovery, and gut health, which is fueling growth across sports nutrition, dietary supplements, and clinical nutrition sectors. Advances in enzymatic hydrolysis are reshaping the market by enhancing process efficiency and product quality. Modern enzyme-based systems allow controlled peptide breakdown, producing hydrolysates with higher bioavailability and reduced off-flavors. Global food ingredient manufacturers are adapting their enzymatic hydrolysis processes to meet halal compliance, enabling precision nutrition and cleaner production. The growing use of halal-certified hydrolysates in infant and clinical nutrition, where they reduce allergenicity and improve nutrient absorption, is also driving market adoption.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$800 Million

Forecast Value

$1.4 Billion

CAGR

5.6%

The plant-based protein hydrolysates accounted for USD 360 million in 2024, owing to rising consumer preference for sustainable, ethical, and allergen-free protein sources. Lactose intolerance, veganism, and environmental awareness have encouraged manufacturers to replace animal-derived proteins with soy, pea, and rice hydrolysates. Their ease of halal certification, availability of raw materials, and simplified production processes make plant-based hydrolysates ideal for beverages, functional foods, and sports nutrition applications.

The enzymatic hydrolysis segment reached USD 481.6 million in 2024, attributed to its specificity and ability to produce high-quality, bioactive protein hydrolysates without compromising nutritional integrity. This method allows manufacturers to control peptide chain length and composition, improving digestibility and functionality for dietary supplements, clinical foods, and sports nutrition. Additionally, enzymatic hydrolysis aligns with halal standards since it avoids chemical catalysts, making it suitable for halal-certified production lines.

North America Halal-Certified Protein Hydrolysates Market captured USD 120 million in 2024, representing 15% share. The U.S. contributed USD 100.8 million due to its mature food processing industry, high consumer demand for functional and clean-label ingredients, and growing Muslim population. Increasing awareness of halal-certified nutritional supplements among fitness-focused consumers is also driving market growth in the region.

Key players in the Global Halal-Certified Protein Hydrolysates Market include Arla Foods Ingredients, ADM (Archer Daniels Midland), Cargill Incorporated, Actus Nutrition, Fonterra Co-operative Group, Glanbia PLC, FrieslandCampina, Abbott Laboratories, Roquette Freres, DSM-Firmenich, Kerry Group, and Agropur Cooperative. To strengthen their presence, companies in the halal-certified protein hydrolysates sector are focusing on research and development to improve enzymatic hydrolysis efficiency, peptide bioavailability, and clean-label formulations. Strategic collaborations with food manufacturers, nutrition brands, and clinical nutrition providers help expand distribution networks. Firms are also investing in halal certification processes, regional production facilities, and raw material sourcing to ensure compliance and scalability.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Source type

2.2.3 Processing Technology

2.2.4 Application

2.2.5 End Use Industry

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier Landscape

3.1.2 Profit Margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising health consciousness & clean label demand

3.2.1.2 Technological advancements in enzymatic hydrolysis

3.2.1.3 Expanding applications in infant & clinical nutrition

3.2.2 Industry pitfalls and challenges

3.2.2.1 Higher production costs & price premiums

3.2.2.2 Limited availability of halal-certified raw materials

3.2.3 Market opportunities

3.2.3.1 Plant-based protein hydrolysates growth potential

3.2.3.2 Digital traceability & blockchain integration

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Price trends

3.7.1 By region

3.7.2 Product

3.8 Future market trends

3.9 Technology and Innovation Landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent Landscape

3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and environmental aspects

3.12.1 Sustainable practices

3.12.2 Waste reduction strategies

3.12.3 Energy efficiency in production

3.12.4 Eco-friendly initiatives

3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Source Type, 2021 - 2034 (USD Million) (Kilo Tons)

5.1 Key trends

5.2 Plant-based protein hydrolysates

5.2.1 Pea protein hydrolysates

5.2.2 Soy protein hydrolysates

5.2.3 Rice protein hydrolysates

5.2.4 Hemp protein hydrolysates

5.2.5 Other plant sources

5.3 Animal-based protein hydrolysates

5.3.1 Whey protein hydrolysates

5.3.2 Casein hydrolysates

5.3.3 Bovine protein hydrolysates

5.3.4 Poultry protein hydrolysates

5.4 Marine protein hydrolysates

5.4.1 Fish protein hydrolysates

5.4.2 Shrimp & crustacean hydrolysates

5.4.3 Other marine sources

5.5 Microbial protein hydrolysates

Chapter 6 Market Estimates and Forecast, By Processing Technology, 2021 - 2034 (USD Million) (Kilo Tons)

6.1 Key trends

6.2 Enzymatic hydrolysis

6.2.1 Microbial enzyme systems

6.2.2 Plant-derived enzyme systems

6.2.3 Immobilized enzyme technology

6.3 Acid hydrolysis

6.4 Alkaline hydrolysis

6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

7.1 Key trends

7.2 Infant nutrition

7.2.1 Extensively hydrolyzed formulas

7.2.2 Partially hydrolyzed formulas

7.2.3 Hypoallergenic products

7.3 Sports nutrition

7.3.1 Pre-workout supplements

7.3.2 Post-workout recovery products

7.3.3 Protein powders & shakes

7.4 Clinical/medical nutrition

7.4.1 Enteral nutrition products

7.4.2 Medical foods

7.4.3 Specialized dietary management

7.5 Dietary supplements & nutraceuticals

7.5.1 Capsules & tablets

7.5.2 Powder supplements

7.5.3 Functional foods

7.6 Food & beverage ingredients

7.6.1 Flavor enhancers

7.6.2 Protein fortification

7.6.3 Emulsifiers & stabilizers

7.7 Cosmetics & personal care

7.7.1 Anti-aging products

7.7.2 Hair care products

7.7.3 Skin care applications

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Million) (Kilo Tons)

8.1 Key trends

8.2 Food & beverage manufacturers

8.3 Pharmaceuticals

8.4 Nutraceuticals & Dietary supplement producers

8.5 Cosmetics & personal care

8.6 Animal feed & pet food

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD million) (Kilo Tons)