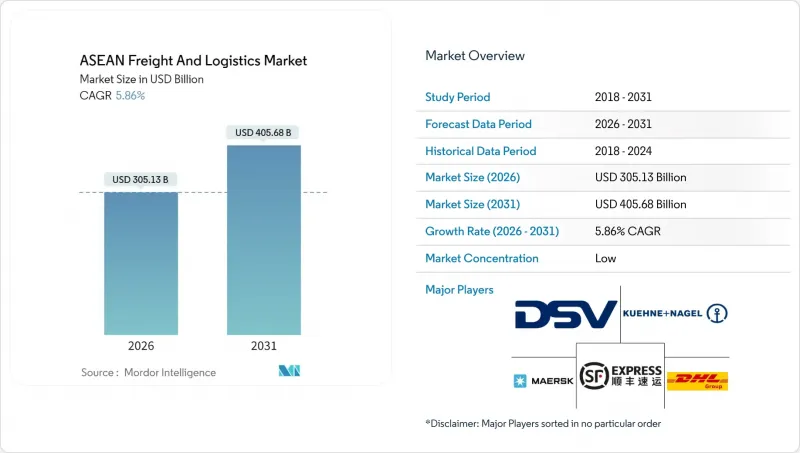

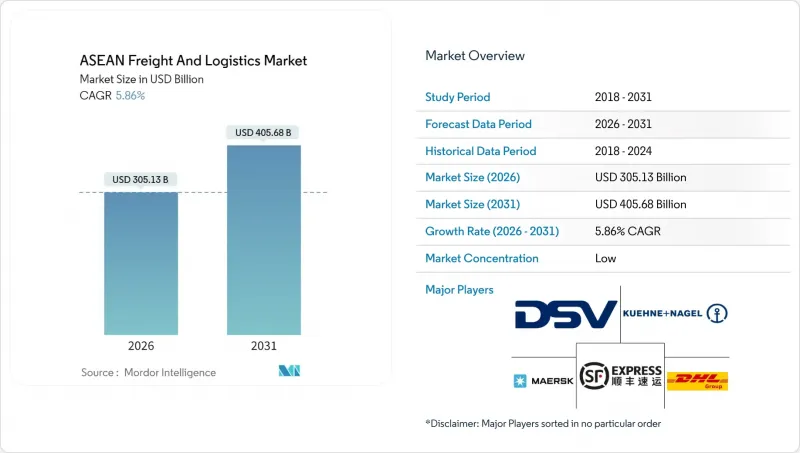

아세안의 화물 및 물류 시장은 2025년 2,882억 4,000만 달러에서 2026년에는 3,051억 3,000만 달러로 성장하고, 2026-2031년 CAGR 5.86%로 성장을 지속하여 2031년까지 4,056억 8,000만 달러에 이를 것으로 예측됩니다.

탄탄한 전자상거래 보급, 제조 공급망 재배치, 관세 인하 무역 협정, 대규모 공공 인프라 계획이 결합되어 10개 회원국 전체가 성장 모멘텀을 유지하고 있습니다. 아세안의 화물 및 물류 시장은 2025년 6월 발효된 필리핀의 RCEP(역내종합적경제동반자협정(RCEP) 가입으로 혜택을 받고 있으며, 이로 인해 무역품의 90% 관세가 철폐되고 통관 절차가 신속히 처리될 예정입니다. 경쟁의 격화로 인해 촘촘한 지역 네트워크 구축을 위한 인수합병이 촉진되는 한편, 전기차 배터리 물류, 의약품 콜드체인 등 새로운 서비스 분야가 수익원 다변화를 가져다 줄 것입니다. 그러나 신흥 시장의 높은 GDP 대비 물류비 비율, 내항 제한, 설비 불균형 등의 문제가 비용 부담으로 작용하고 있으며, 사업자들은 기술 혁신과 운송 모드의 최적화를 통해 이를 상쇄해야 합니다.

TikTok, Shopee, Lazada와 같은 전자상거래 플랫폼은 아세안 주요 도시에서 전통적인 화물 물동량을 넘어선 소포 취급량을 견인하고 있습니다. 플랫폼이 주도하는 운송업체 배분은 네트워크 밀도와 제3자 사업자에 대한 협상력을 높이고, 사업자들은 하루에 수백만 개의 소포를 처리하는 자동 분류 허브에 투자하도록 장려하고 있습니다. 유니콘 기업인 플래시 익스프레스는 1,300개 매장으로 확장하여 현재 6개국에서 하루 최대 200만 개의 소포를 처리하고 있으며, 빠른 배송에 필요한 업무의 집약도를 보여주고 있습니다. 분산형 풀필먼트, 도시 집중 허브, 마이크로모빌리티 차량군은 라스트 마일 효율성을 향상시키지만, 전기 자전거와 세발자전거에 대한 지역별 규제로 인해 통일된 배포가 지연되고 있습니다. 실시간 추적 및 예측 배송 시간은 고객의 표준적인 기대치가 되어 CEP 사업자들의 디지털화 추진을 촉진하고 있습니다.

동북아시아에서 아세안으로 생산기지를 이전하는 외국계 기업들로 인해 국경 간 화물 운송, 부품 셔틀 서비스, 전문 창고에 대한 지속적인 수요가 발생하고 있습니다. 전자 및 전기 제품이 자본 유입을 주도했으며, 말레이시아는 2024년 9월 341억 링깃(72억 달러) 상당의 집적회로를 수출했습니다. 베트남의 산업단지는 개선된 심해 항만 및 복선 철도 회랑과 직접 연결되어 내륙과 원활하게 연결되고 있습니다. 적시 생산 방식은 납기 신뢰성과 통관 효율성의 중요성을 높이고, 엔드-투-엔드 물류 통합업체의 가치 제안을 강화하고 있습니다. RCEP(역내종합적경제동반자협정)의 원산지 규정은 역내 조달을 촉진하여 공급망의 지역화를 더욱 촉진하고, 아세안 역내 화물 운송량을 촉진하고 있습니다.

도로 품질 부족, 내륙 수로의 제한, 전력 부족은 특히 내륙 국가와 도서 국가 하위 지역에서 운송 시간을 연장하고 처리 비용을 증가시킵니다. 국제에너지기구(IEA)에 따르면, 2000년부터 2024년까지 동남아시아의 화물 운송에 의한 석유 수요는 130만 배럴/일에서 280만 배럴/일로 증가하여 교통 체증과 배출량이 확대될 것으로 예상하고 있습니다. 전력망의 불안정성과 디젤 발전기의 고비용은 콜드체인의 보급을 저해하고, 의약품과 신선식품의 물류에 제약을 주고 있습니다. 인프라 자금 조달이 가속화되지 않으면 신흥 회원국은 서비스 품질이 저하되고 고부가가치 가치사슬에 참여할 기회를 놓칠 위험이 있습니다.

제조업은 2025년 매출의 31.74%를 차지할 것으로 예상되며, 이는 이 지역이 세계 전자, 자동차, 섬유 공급망에서 중요한 역할을 담당하고 있음을 보여줍니다. 유연한 창고 배치와 시간 지정 화물 서비스를 통해 베트남, 태국, 말레이시아에 집적된 공장에 저스트 인 시퀀싱 배송이 가능합니다. 아세안의 도매 및 소매업 화물 및 물류 시장 점유율은 현대식 식료품, 패션 및 일반 상품 부문이 옴니채널 유통망을 확대함에 따라 2026년부터 2031년까지 연평균 6.31%의 빠른 성장세를 보일 것으로 예측됩니다. 농림업은 벌크화물과 냉장화물을 통해 여전히 상당한 물동량을 차지하고 있으며, 건설업은 공공 인프라 건설에 따른 중량물 운송을 주도하고 있습니다.

소매 공급망에서는 변동이 심한 온라인 수요에 대응하기 위해 재고 관리의 자동화가 진행됩니다. 도시 밀집 지역에서는 다크 스토어와 마이크로 풀필먼트 거점이 증가하여 배송 약속 시간을 2시간 이내로 단축합니다. 한편, 제조업체는 지정학적 리스크를 헤지하기 위해 공장 거점을 분산시키고, 서비스 제공업체는 보세 트럭 운송 경로와 부품 흐름을 동기화할 수 있는 지역 물류 센터를 확보해야 하는 상황입니다. 온도관리 창고는 식품 및 의약품 분야에서 보급이 확대되고 있으며, 말레이시아 타스코의 냉장창고 네트워크 가동률은 2024년 평균 85-90%를 나타낼 것으로 예측됩니다.

화물 운송 부문은 2025년 매출의 60.12%를 차지할 것으로 예상되며, 이는 벌크 상품 및 컨테이너 운송의 핵심적인 역할을 반영합니다. 한편, CEP(도시지역 배송)는 도시지역 EC 수요 증가(고빈도 소포 배송 및 투명한 추적)를 배경으로 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 6.78%로 가장 빠르게 성장할 것으로 예측됩니다. 아세안 지역의 CEP 사업자를 위한 화물 및 물류 시장 규모는 방콕과 자카르타의 하루 300만 개 처리 용량의 분류기 등 자동화 투자를 통해 확대되고 있습니다. 화물운송업은 확대되는 역내 무역을 위해 통관 업무와 다구간 운송을 조정하여 수익 안정성을 유지하고 있습니다. 창고업은 재고의 현지화, 특히 성장하는 온라인 식료품 유통을 지원하기 위한 냉장 보관소 설치의 혜택을 누리고 있습니다. 소규모이지만 수익성이 높은 전문 서비스(프로젝트 화물, 역물류, 애프터마켓 부품)는 사업 포트폴리오를 보완하고 경기 순환의 영향으로부터 사업자를 보호합니다.

디지털 전환은 더 이상 선택의 여지가 없습니다. 주요 CEP 기업들은 경로 최적화 알고리즘과 핸드헬드 스캐너를 통합하여 판매자와 구매자에게 실시간 상태 업데이트를 제공합니다. 대도시 지역의 온라인 약국 및 밀키트 서비스 확대에 따라 온도 관리형 CEP 화물에 대한 수요가 증가하고 있습니다. 지역 기반 사업자는 국경 간 소포를 통합하고 아세안 단일 창구를 활용하여 사이클 타임을 단축하고 고객과의 관계를 더욱 공고히 할 수 있습니다. 지역마다 전기 배달 오토바이에 대한 규제가 다르기 때문에 각 도시에서 규정 준수 차량을 시범 운영하여 이러한 운영상의 불확실성을 해결하고 있습니다.

The ASEAN freight and logistics market is expected to grow from USD 288.24 billion in 2025 to USD 305.13 billion in 2026 and is forecast to reach USD 405.68 billion by 2031 at 5.86% CAGR over 2026-2031.

Robust e-commerce uptake, the relocation of manufacturing supply chains, tariff-cutting trade pacts, and large-scale public infrastructure programs collectively sustain growth momentum across all ten member states. The ASEAN freight and logistics market benefits from the June 2025 entry into force of the Philippines' RCEP accession, which removes duties on 90% of traded goods and accelerates customs clearances. Intensifying competition prompts mergers and acquisitions that aim to build dense regional networks, while new service niches such as EV-battery logistics and pharmaceutical cold chains diversify revenue streams. Nonetheless, high logistics-to-GDP ratios in emerging markets, cabotage restrictions, and equipment imbalances add cost pressures that operators must offset through technology and modal optimization.

E-commerce platforms such as TikTok, Shopee, and Lazada have driven parcel counts that outpace traditional freight volumes across major ASEAN cities. Platform-controlled carrier allocation increases network density and bargaining power over third-party providers, prompting operators to invest in automated sortation hubs that handle millions of parcels daily. Unicorn Flash Express scaled to 1,300 branches and now processes up to 2 million parcels per day across six countries, illustrating the operational intensity required for rapid deliveries. Distributed fulfillment, urban consolidation hubs, and micro-mobility fleets improve last-mile efficiency, although inconsistent local regulations on electric bikes and trikes slow uniform deployment. Real-time tracking and predictive delivery windows become standard customer expectations, reinforcing the digitization push among CEP players.

Foreign investors relocating production from Northeast Asia to ASEAN spur sustained demand for cross-border freight, component shuttle services, and specialized warehousing. Electronics and electrical goods dominate capital inflows, with Malaysia exporting integrated circuits worth MYR 34.1 billion (USD 7.2 billion) in September 2024. Vietnam's industrial parks link directly to upgraded deep-sea ports and double-track rail corridors, enabling seamless hinterland connectivity. Just-in-time manufacturing raises the premium on schedule reliability and customs efficiency, reinforcing the value proposition of end-to-end logistics integrators. Rules of origin under RCEP further localize supply chains by incentivizing regional content, stimulating intra-ASEAN freight volumes.

Road quality deficits, limited inland waterways, and power shortages prolong transit times and inflate handling expenses, particularly in landlocked and archipelagic sub-regions. The International Energy Agency notes that oil demand from Southeast Asian freight transport rose from 1.3 million to 2.8 million barrels per day between 2000 and 2024, magnifying congestion and emissions. Cold-chain rollout is hampered by grid unreliability and high diesel generator costs, constraining pharmaceutical and fresh-produce logistics. Without accelerated infrastructure finance, emerging members risk lower service quality and missed participation in high-value supply chains.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Manufacturing generated 31.74% of 2025 revenue, underscoring the region's vital role in global electronics, automotive, and textile supply chains. Flexible warehousing footprints and time-definite freight services enable just-in-sequence deliveries to factories clustered in Vietnam, Thailand, and Malaysia. The ASEAN freight and logistics market share for wholesale and retail trade will rise quickly on a 6.31% CAGR (2026-2031) as modern grocery, fashion, and general merchandise segments expand omnichannel distribution networks. Agriculture and forestry continue to contribute sizable tonnage via bulk and reefer cargoes, while construction drives heavy-lift activity linked to public infrastructure builds.

Retail supply chains embrace automation to align inventory with volatile online demand. Dark stores and micro-fulfillment sites multiply in dense urban pockets, shrinking delivery promises to sub-two-hour windows. Manufacturers, meanwhile, diversify plant footprints to hedge geopolitical risk, prompting service providers to secure bonded trucking corridors and regional distribution centers that synchronize component flows. Temperature-controlled warehousing gains traction across food and pharma verticals, and capacity utilization in Malaysia's Tasco cold storage network averaged 85-90% in 2024.

The freight transport segment supplied 60.12% of 2025 revenue, reflecting its core role in bulk commodity and container movements. CEP, however, grows fastest at 6.78% CAGR (2026-2031), fueled by urban e-commerce that demands high-frequency parcel drops and transparent tracking. The ASEAN freight and logistics market size for CEP operators improves through automation investments such as 3-million-parcel-per-day sorters in Bangkok and Jakarta. Freight forwarding maintains revenue stability by orchestrating customs brokerage and multi-leg shipping for expanding intra-regional trade. Warehousing benefits from inventory localization, including chilled storage nodes that support growing online grocery traffic. Small but lucrative specialized services-project cargo, reverse logistics, and aftermarket parts-round out the portfolio and insulate operators from cyclicality.

Digital transformation is no longer optional. Leading CEP firms integrate route-optimization algorithms and handheld scanners that push real-time status updates to merchants and buyers. Temperature-controlled CEP consignments escalate as online pharmacies and meal-kit services scale in metro areas. Operators with regional footprints can consolidate cross-border parcels and leverage the ASEAN Single Window to shorten cycle times, creating stickier customer relationships. Fragmented regulations on electric delivery bikes present an operational wildcard that companies navigate by piloting compliant fleets city by city.

The ASEAN Freight and Logistics Market Report is Segmented by End User Industry (Agriculture, Fishing, and Forestry, Construction, Manufacturing, and More), by Logistics Function (Courier, Express, and Parcel (CEP), Freight Forwarding, Freight Transport, Warehousing and Storage, and Other Services), and by Country (Indonesia, Malaysia, Thailand, Vietnam, and Rest of ASEAN). The Market Forecasts are Provided in Terms of Value (USD).