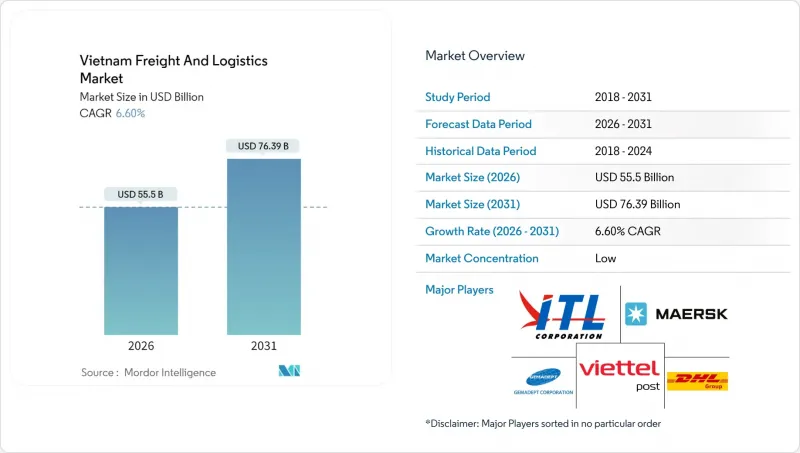

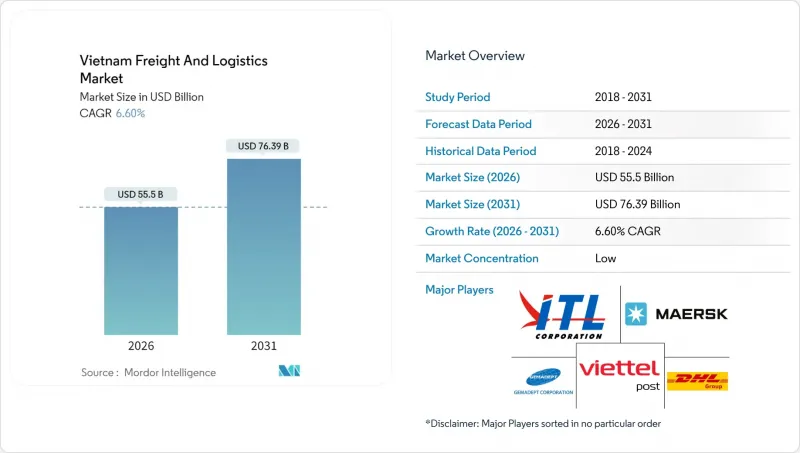

베트남의 화물 및 물류 시장은 2025년 520억 6,000만 달러에서 2026년에는 555억 달러로 성장하며, 2026-2031년에 CAGR 6.6%로 추이하며, 2031년까지 763억 9,000만 달러에 달할 것으로 예측됩니다.

이러한 성장 궤적은 제조업의 지속적인 유입, E-Commerce 소포 증가, 도로, 항만, 공항에 대한 150억 달러 규모의 공공 투자를 반영하고 있습니다. 구조적 호재로는 중국발 니어쇼어링, 아세안 단일창구 통관 디지털화, 온도관리 배송 수요 증가 등을 꼽을 수 있으며, 이로 인해 육해공 운송루트 전체에서 물동량이 증가하고 있습니다. 국제적인 통합 기업이 현지 사업 기반을 강화하는 한편, 국내 사업자들이 콜드체인과 라스트마일 투자를 통해 규모를 확대하면서 경쟁은 더욱 치열해지고 있습니다. 따라서 베트남의 화물 및 물류 시장은 인프라 구축, 무역 자유화, 디지털 혁신이라는 선순환의 혜택을 누리고 있으며, 이로 인해 체류 시간이 단축되고 새로운 서비스 분야가 개발되고 있습니다.

온라인 마켓플레이스의 확대와 소셜커머스의 지역적 제약 완화로 2024년 국내 택배 취급량은 45% 증가할 것으로 예측됩니다. 베트남 화물 및 물류 시장에서 택배 네트워크는 자동 분류기 및 AI 경로 엔진을 도입하여 평균 배송 시간을 48시간에서 24시간으로 단축하고 있습니다. 그러나 라스트마일 네트워크의 분절화로 인해 소포당 배송비용이 태국보다 28% 더 비싸고, 사업자들은 마이크로 허브 공유와 크라우드 소싱형 드라이버 활용을 통해 지방으로의 서비스 확대를 추진하고 있습니다. 규제 측면에서도 순풍이 불고 있습니다. 200달러 미만 소포에 대한 통관 절차가 간소화되어 통관 체류일수가 5일에서 1일로 단축되었습니다. 수요에 따라 자본이 따라가고, ViettelPost는 15개의 로봇 분류 센터를 개설하고, Giao Hang Nhanh는 2025년까지 마을 단위의 커버리지를 달성할 것이라고 밝혔습니다. 이러한 움직임은 디지털 기반을 강화하여 향후 취급량 확대를 가속화하고, CEP(택배)를 베트남 화물 및 물류 시장에서 가장 빠르게 성장하는 분야로 확고히 자리매김하고 있습니다.

중국으로부터의 전자 및 의류 산업의 이전으로 2024년 제조 물류 수요는 28% 증가했습니다. 이는 세계 브랜드들이 지정학적 리스크와 비용 리스크를 헤지한 결과입니다. 북부 클러스터에서는 고부가가치 전자제품의 유통이 항공 운송을 우선시하고 있으며, 노이바이 공항의 부품 취급량은 전년 대비 35% 증가함. 이로 인해 용량 증설과 슬롯의 우선순위를 재조정해야 하는 상황입니다. 삼성의 확장만으로도월2,400TEU의 운송이 필요하며, 폭스콘과 룩쉐어는 각각 수출 게이트웨이로 연결되는 폐쇄형 루프 회랑을 운영하고 있습니다. 의류 제조업체는 육로와 해상 복합운송을 활용하여 기존 중국 노선보다 40% 단축된 리드타임을 실현하고 있습니다. 키트 조립, 반품 처리, 품질관리 창고를 제공하는 사업자들은 현재 프리미엄 마진을 얻고 있으며, 베트남 화물 및 물류 시장에서 순수 운송에서 통합 계약 물류로의 전환을 보여주고 있습니다.

수출 대 수입 비율이 3:1이기 때문에 빈 컨테이너가 내륙에 머물러 평균 재배치 비용이 20피트 컨테이너의 경우 85달러, 40피트 컨테이너의 경우 170달러로 상승했습니다. 2024년 커피와 섬유제품의 성수기에 컨테이너 가동률이 70% 이하로 떨어지면서 컨테이너 불균형 요금이 25% 상승했습니다. 포워더는 추적용 IoT 태그와 공유 풀을 활용하여 가동률 향상과 개별 운송 비용의 15-20% 절감을 꾀하고 있지만, 구조적인 무역 불균형으로 인해 헤드홀 추가 요금의 조기 완화는 쉽지 않을 것으로 보입니다. 이로 인해 베트남의 화물 및 물류 시장은 변동에 직면하여 중소 화주들의 이익률을 압박하고 있습니다.

2025년 제조업은 베트남 화물 및 물류 시장 점유율의 35.12%를 차지했습니다. 이는 해외 바이어와의 정확한 재고 동기화를 필요로 하는 전자제품 및 의류 허브가 주도하고 있습니다. 엄격한 사이클 타임으로 인해 RFID 대응 부품 키트화 및 지연 창고 관리가 촉진되고, 제3자 물류(3PL)의 침투가 진행되고 있습니다. 도매 및 소매업은 현대식 식료품점, D2C 브랜드, 크로스보더 마켓플레이스의 SKU 및 배송 거점 확대에 따라 2026-2031년 연평균 복합 성장률(CAGR) 6.98%로 증가할 것으로 예측됩니다. 해산물, 과일, 백신 분야에서는 운송 실패 비용이 물류 프리미엄을 크게 상회하므로 GDP 인증 파트너의 채택이 정당화되어 콜드체인 프로토콜이 확대되고 있습니다. 의약품 이력추적에 대한 규제 강화는 진입장벽을 높이고, 검증된 프로세스를 가진 사업자에 대한 수요를 집중시키며, 베트남 화물 및 물류 시장내 통합 추세를 강화시키고 있습니다.

농업, 건설 등 전통적 부문은 기간 수송량을 유지하지만, 교통수단의 대체가 진행되고 있습니다. 메콩강 삼각주에서 바지선과 철도의 시범 운영으로 부피가 큰 쌀과 모래 수송이 혼잡한 간선도로에서 벗어나고 있습니다. 석유-가스-광업 물류는 전문성이 유지되고, 높은 안전 기준과 복잡한 용선 계약이 틈새 포워더에게 유리하게 작용하고 있습니다.

2025년 기준, 수출 제조업이 벌크 화물 흐름을 주도한 결과, 화물 운송은 베트남 화물 및 물류 시장 규모의 64.12%를 차지했습니다. 그러나 소셜 커머스와 크로스보더 쇼핑의 확대로 택배, 익스프레스 배송, 소포 부문의 매출은 2026-2031년 연평균 복합 성장률(CAGR) 7.52%로 증가하며 점유율을 계속 확대할 것으로 보입니다. CEP(택배)의 급격한 성장으로 사업자들은 허브의 자동화와 세관 API 통합을 추진하여 마감에서 배송까지의 주기를 절반으로 단축하고 있습니다. 창고업도 디지털화 추세에 따라 양식업과 백신 공급망을 지원하기 위해 온도 관리 자산은 2026-2031년 연평균 7.89%의 성장률을 보일 것으로 예측됩니다. 블록체인 선하증권과 IoT 센서 네트워크가 표준화되면서 서비스의 경계가 모호해지고 있습니다. 베트남의 화물 및 물류 시장에서 화물 운송업체들은 실시간 가시성과 부가가치 포장을 결합하여 상품화에 대한 마진을 확보하기 위해 노력하고 있습니다.

화물 운송의 우위가 지속되는 가운데, 운송 모드 간 전환이 진행되고 있습니다. 2031년까지 도로 운송은 규모를 유지하지만, 속도가 비용을 능가하는 선택적 운송 분야에서는 항공화물과 익스프레스 배송이 점유율을 차지할 것입니다. 디지털 화물 플랫폼은 현물화물을 통합하고, 트럭 가동률을 12% 향상시켜 빈 반송 및 수작업으로 인한 서류 처리 등의 문제를 해결합니다. 통합 계획으로 도로, 해상, 철도를 결합한 멀티모달 운송 루트를 실현하여 CO2 배출량을 줄이고 ESG를 의식하는 수출업체에 어필할 수 있습니다.

The Vietnam freight and logistics market is expected to grow from USD 52.06 billion in 2025 to USD 55.5 billion in 2026 and is forecast to reach USD 76.39 billion by 2031 at 6.6% CAGR over 2026-2031.

This trajectory reflects sustained manufacturing inflows, e-commerce parcel growth, and public spending of USD 15 billion on roads, ports, and airports. Structural tailwinds include near-shoring from China, ASEAN single-window customs digitalization, and rising demand for temperature-controlled distribution that together lift volumes across road, sea, and air corridors. Competitive intensity is sharpening as international integrators deepen local footprints while domestic operators scale through cold-chain and last-mile investments. The Vietnam freight and logistics market, therefore, benefits from a virtuous cycle of infrastructure, trade liberalization, and digital transformation that reduces dwell times and unlocks new service niches.

Domestic parcel volumes jumped 45% in 2024 as online marketplaces proliferated and social-commerce blunted geographic constraints. The Vietnam freight and logistics market has seen courier networks deploy automated sorters and AI route engines that shrink average delivery windows from 48 to 24 hours. Yet fragmented last-mile networks mean per-parcel delivery costs remain 28% above Thailand, spurring providers to pool micro-hubs and leverage crowdsourced drivers to widen rural reach. Regulatory momentum adds tailwind: simplified clearance for parcels under USD 200 now cuts customs dwell from five days to one. Capital follows demand, with ViettelPost opening 15 robotic sort centers and Giao Hang Nhanh pledging commune-level coverage by 2025. These moves embed digital density that accelerates future volume scaling and entrenches CEP as the fastest-growing slice of the Vietnam freight and logistics market.

Electronics and apparel relocations from China lifted manufacturing logistics demand 28% in 2024 as global brands hedged geopolitical and cost risk. Northern clusters host high-value electronics flows that prefer airfreight; component uplift at Noi Bai Airport climbed 35% year-over-year, forcing capacity additions and slot reprioritization. Samsung's expansion alone requires 2,400 TEU moves monthly, while Foxconn and Luxshare each operate closed-loop corridors to export gateways. Apparel producers leverage road-sea combinations, redirecting lead times 40% shorter than legacy China lanes. Providers offering kitting, return-handling, and quality-control warehousing now command premium margins, signaling a shift from pure transport to integrated contract logistics within the Vietnam freight and logistics market.

An export-to-import ratio of 3:1 strands empties inland, raising average repositioning outlay to USD 85 per 20-foot box and USD 170 for 40-foot units. Container imbalance charges rose 25% in 2024 as availability dipped below 70% during peak coffee and textile seasons. Forwarders deploy tracking IoT tags and shared pools to lift utilization and shave 15-20% from separate carrier costs, yet structural trade asymmetry means headhaul surcharges are unlikely to abate quickly. The Vietnam freight and logistics market thus endures volatility that squeezes margins for SME shippers.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Manufacturing drove 35.12% of Vietnam freight and logistics market share in 2025, anchored by electronics and garment hubs that mandate precise inventory sync with overseas buyers. Tight cycle times spur RFID-enabled component kitting and postponement warehousing, raising third-party logistics penetration. Wholesale and retail trade is catching up, projected to rise 6.98% CAGR (2026-2031) as modern grocery, direct-to-consumer brands, and cross-border marketplaces widen SKUs and delivery nodes. Cold-chain protocols expand with seafood, fruit, and vaccines, where shipment failure costs far exceed logistics premiums and justify GDP-certified partners. Regulatory pushes for pharmaceutical traceability raise barriers, funneling demand toward players with validated processes, reinforcing consolidation trends inside the Vietnam freight and logistics market.

Traditional sectors such as agriculture and construction keep baseline tonnage but face modal substitution; barge and rail pilots in the Mekong Delta shift bulky rice and sand away from congested highways. Oil, gas, and mining logistics remain specialist, with higher safety compliance and charter-party complexity that reward niche forwarders.

Freight transport generated 64.12% of the Vietnam freight and logistics market size in 2025 as export manufacturing dictated bulk cargo flows. Yet courier, express, and parcel revenue is on course for a 7.52% CAGR (2026-2031), commandeering incremental share as social-commerce and cross-border shopping proliferate. The CEP surge pushes operators to automate hubs and integrate customs APIs, compressing cut-off-to-delivery cycles by half. Warehousing follows digital cues; temperature-controlled assets are set to grow at 7.89% CAGR (2026-2031), supported by aquaculture and vaccine supply chains. As blockchain bills of lading and IoT sensor networks become standard, service boundaries blur; freight transporters bundle real-time visibility and value-added packaging to secure margin against commoditization in the Vietnam freight and logistics market.

Continued freight-transport primacy masks intra-modal shifts. Road retains scale through 2031, but airfreight and express haulage capture discretionary shipments where velocity trumps cost. Digital freight platforms aggregate spot loads that raise truck utilization by 12%, attacking pain points of empty backhauls and manual paperwork. Integrated planning unlocks multimodal itineraries that blend road, sea, and rail, trimming CO2 and appealing to ESG-minded exporters.

The Vietnam Freight and Logistics Market Report is Segmented by End User Industry (Agriculture, Fishing, and Forestry, Construction, Manufacturing, Oil and Gas, Mining and Quarrying, Wholesale and Retail Trade, and Others) and by Logistics Function (Courier, Express, and Parcel (CEP), Freight Forwarding, Freight Transport, Warehousing and Storage, and Other Services). The Market Forecasts are Provided in Terms of Value (USD).