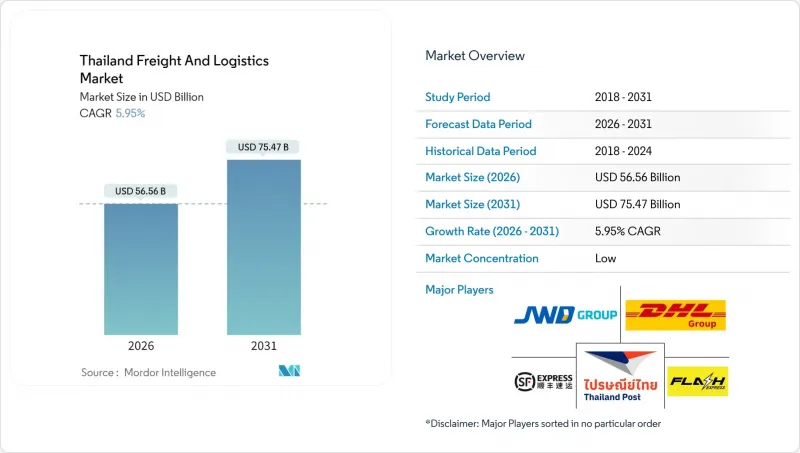

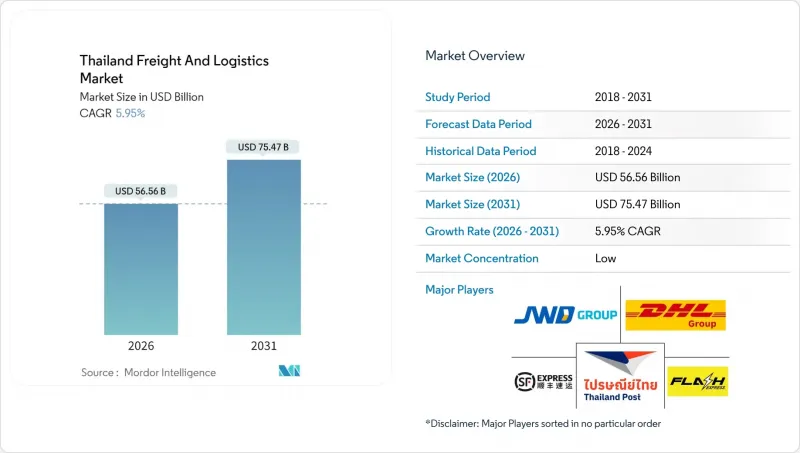

태국의 화물 및 물류 시장은 2025년 533억 8,000만 달러에서 2026년에는 565억 6,000만 달러로 성장하며, 2026-2031년에 CAGR 5.95%로 추이하며, 2031년에는 754억 7,000만 달러에 달할 것으로 예측됩니다.

태국의 아세안내 주요 복합운송 관문으로서의 지위, 지속적인 제조업 회귀, 정부 주도의 인프라 투자 등이 이러한 꾸준한 성장을 지원하고 있습니다. 정부의 대규모 프로젝트로 운송 시간이 단축되는 한편, 중국 외 지역으로의 투자 유입(China+1)이 유통 통로의 재구축을 촉진하고 통합형 창고에 대한 수요를 높이고 있습니다. E-Commerce의 확대로 인해 소포 처리량이 지속적으로 증가하고 있으며, 사업자들은 라스트마일 네트워크의 현대화와 데이터베이스 경로 최적화를 도입해야 합니다. 자동화 창고에서 실시간 IoT 추적에 이르기까지 디지털화는 결정적인 경쟁 우위가 되고 있으며, 지속가능성에 대한 요구는 철도와 전기 트럭으로의 모달 시프트를 가속화하고 있습니다.

도시 가구의 스마트폰 보급률이 90%를 넘어섰고, 온라인 소비가 기호품에서 생필품으로 옮겨가면서 소량화물의 물동량이 지속적으로 증가하고 있습니다. 네트워크 고도화를 통해 방콕의 경우 평균 배송 시간을 24시간 이내로 단축하고 전국적인 익일 배송망을 유지할 수 있게 되었습니다. 국내 CEP 사업자들은 가격 경쟁에서 수익성 관리로 전략을 전환하여 단위당 수익성을 개선하고, 자동화 투자를 위한 자금을 마련하고 있습니다. 지역 협력으로 국경 간 물동량 흐름이 확대되고, 태국 기업은 중국 플랫폼을 활용하여 CLMV 시장으로 원활한 배송을 실현하고 있습니다. 소비자의 실시간 가시성에 대한 기대가 높아지면서 AI를 활용한 동적 라우팅이 도입되어 연료비 절감과 탄소발자국 감소가 이루어지고 있습니다.

동부경제회랑(EEC)은 2024년 승인된 168억 달러의 투자를 주도하며 항만, 공항, 철도 연결의 새로운 업그레이드 물결을 가속화하고 있습니다. 2027년까지 400만 TEU의 처리 능력을 확장할 예정인 렘차방 터미널 F의 확장은 태국의 컨테이너 처리 능력을 40%까지 확대할 예정입니다. 우타파오 공항의 다단계 확장으로 인해 우타파오는 항공기에서 항구 정박지까지 6시간 이내에 고부가가치 화물을 운송할 수 있는 세 가지 운송 모드의 결절점으로 변모하고 있습니다. 이러한 자산들은 복합운송의 연결성을 높이고 도로의 병목현상을 완화하여 현재 GDP의 13-14%를 차지하는 물류비용 절감에 기여하고 있습니다.

태국의 물류 지출은 여전히 OECD 평균을 크게 상회하고 있으며, 그 주요 요인은 국내 화물의 80%가 여전히 도로 운송에 의존하고 있기 때문입니다. 분산된 트럭 운송 사업자는 연료 및 장비 조달에 있으며, 협상력이 부족하고, 사업자의 절반은 5 대 미만의 트럭으로 운영되고 있습니다. 항만 체류시간이 평균 62시간으로 길어 보관료와 체선료 부담이 증가하고 있습니다. 중소기업 운송회사는 상업은행들이 리스크가 낮은 부문을 우선시하므로 대출 조건이 까다로워지고 있습니다. 2024년 기업 대출이 1.9% 증가했음에도 불구하고 중소기업 대출 잔액은 감소했습니다. 경제특구의 10% 법인세율 등 정책적 인센티브는 비용 부담을 줄여줄 것이지만, 이전을 위한 전제조건이 도입을 억제하고 있습니다.

제조업은 2025년 매출의 32.21%를 차지할 것으로 예상되며, 동부 연안의 전자, 자동차, 석유화학 클러스터가 핵심을 형성합니다. 고정밀 부품의 유통은 온도 관리 환경과 신속한 통관이 요구되며, 전문 역량을 갖춘 사업자가 유리합니다. 도소매업은 옴니채널 소매업체들이 전국적인 풀필먼트 네트워크를 구축하면서 2026-2031년 연평균 복합 성장률(CAGR) 6.38%로 가장 높은 성장률을 나타낼 것으로 예측됩니다. 주문 마감 시간 연장 및 당일 배송 범위 확대에 따라 도시 지역 쇼핑객의 5km 이내 마이크로 풀필먼트 센터에 대한 수요가 증가하고 있습니다.

식품 가공업체와 농업 관련 기업은 지방의 농장과 방콕의 유통 거점을 연결하는 냉장 트럭 운송망에 계속 의존하고 있습니다. 건설물류는 지하철과 공항 프로젝트 등으로 견고한 흐름을 유지하고 있지만, 수요는 주기적으로 급등하는 모습을 보이고 있습니다. 전기자동차 조립으로의 전환에 따라 배터리 팩과 희토류 자석의 새로운 수입 흐름이 발생하여 특수 위험물 취급을 필요로 하는 태국의 화물 및 물류 시장 규모가 확대되고 있습니다.

2025년 기준, 화물 운송은 태국의 화물 및 물류 시장 점유율의 61.12%를 차지하고 있으며, 이는 산업단지에서 항만 및 국경 게이트에 대한 지속적인 대량 화물 흐름을 반영합니다. 동부 경제회랑과 렘차방항 사이의 탄탄한 인프라 연계가 이러한 이점을 지원하고 있습니다. 한편, 급성장하는 E-Commerce 수요가 CEP(도시 간 택배) 매출을 견인하고 있으며, 2026-2031년 연평균 복합 성장률(CAGR) 6.92%를 나타낼 것으로 예측됩니다. 기존 도로 화물 운송 기업은 실시간 텔레매틱스를 통합하고 철도 사업자와 제휴하여 운송 비용을 최대 12%까지 절감하는 준복합 운송 서비스를 제공합니다.

물류 사업자는 창고 관리 시스템을 도입하여 화주에게 화물의 가시성을 제공함으로써 예측에 기반한 보충을 가능하게 하고, 계절적 성수기 수요를 평준화할 수 있습니다. CEP 네트워크가 밀집된 가운데, 가전제품이나 전자제품을 위한 '두 사람' 2인 배송이 부가가치가 높은 틈새 서비스로 떠오르고 있습니다. 정부의 랜드브릿지 구상은 인도 태평양 횡단 컨테이너 화물을 남부 항구로 우회하는 것을 목표로 하고 있으며, 이로 인해 2020년대 중반까지 태국의 화물 운송 시장 규모가 더욱 확대될 가능성이 있습니다. 한편, 포워더는 CEP 사업자의 구역별 가격 책정 및 연료 할증료 제도 도입으로 CEP 분야에서의 이익률 향상이 예상됩니다.

The Thailand freight and logistics market is expected to grow from USD 53.38 billion in 2025 to USD 56.56 billion in 2026 and is forecast to reach USD 75.47 billion by 2031 at 5.95% CAGR over 2026-2031.

Thailand's position as ASEAN's principal multimodal gateway, combined with sustained manufacturing reshoring and state-led infrastructure investment, underpins this steady expansion. Government mega-projects are compressing transit times, while China+1 investment inflows are reshaping distribution corridors and spurring demand for integrated warehousing. E-commerce continues to lift parcel volumes, prompting operators to modernize last-mile networks and deploy data-driven route optimization. Digitalization-from automated depots to real-time IoT tracking-has become a decisive competitive lever, and sustainability mandates are accelerating modal shifts toward rail and electric truck fleets.

Parcel volumes continue to rise as smartphone penetration surpasses 90% of urban households and online spending migrates from discretionary goods to daily staples. Network densification enables operators to shorten average delivery times to under 24 hours in Bangkok while maintaining nationwide next-day reach. Domestic CEP players have pivoted from aggressive price wars toward yield management, raising unit profitability and freeing cash flow for automation investments. Regional partnerships are unlocking cross-border volumes, with Thai firms leveraging Chinese platforms for seamless fulfillment into CLMV markets. Consumer expectation of real-time visibility is encouraging the rollout of AI-enabled dynamic routing, which cuts fuel costs and shrinks carbon footprints.

The Eastern Economic Corridor anchors USD 16.8 billion of approved investment in 2024 and has catalyzed a new wave of port, airport, and rail link upgrades. The Laem Chabang Terminal F build-out, scheduled to add 4 million TEU capacity by 2027, expands Thailand's container handling headroom by 40%. U-Tapao airport's multi-phase expansion is transforming the province into a tri-modal junction capable of channeling high-value cargo from aircraft to seaport berth within six hours. These assets collectively reduce logistics costs-currently 13-14% of GDP-by lifting multimodal connectivity and alleviating road bottlenecks.

Thailand's logistics outlay remains materially higher than the OECD average, largely because 80% of domestic cargo still moves by road. Fragmented trucking fleets lack bargaining power for fuel and equipment, and the median operator runs under five trucks. Port dwell times average 62 hours, adding storage and demurrage expenses. SME carriers face tighter credit as commercial banks prioritize lower-risk segments; SME loan balances fell in 2024 even as corporate lending inched up 1.9%. Policy incentives such as a 10% corporate tax rate in Special Economic Zones should ease the cost burden, yet relocation prerequisites temper uptake.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Manufacturing accounted for 32.21% of 2025 revenue, anchored by electronics, automotive, and petrochemical clusters in the Eastern Seaboard. High-precision component flows require climate-controlled environments and expedited customs clearance, favoring operators with specialized capabilities. Wholesale and Retail Trade is projected to register the fastest 6.38% CAGR (2026-2031) as omnichannel retailers embrace nationwide fulfillment meshes. Extended cut-off times and same-day delivery windows are pushing demand for micro-fulfillment centers within 5 kilometers of urban shoppers.

Food processors and agribusinesses continue to rely on refrigerated truck lanes linking upcountry farms to Bangkok distribution hubs. Construction logistics remain buoyant thanks to metro rail and airport projects, though they exhibit cyclical demand spikes. The shift toward electric-vehicle assembly is spawning new inbound flows of battery packs and rare-earth magnets, bolstering the Thailand freight and logistics market size for specialized dangerous-goods handling.

Freight Transport contributed 61.12% of Thailand freight and logistics market share in 2025, reflecting sustained bulk cargo flows from industrial estates to ports and border gates. Strong infrastructure links between the Eastern Economic Corridor and Laem Chabang underpin this dominance. At the same time, burgeoning e-commerce demand is propelling CEP revenues, expected to post a 6.92% CAGR between 2026-2031. Traditional road freight firms are integrating real-time telematics and partnering with rail operators to offer quasi-intermodal services that cut transit costs by up to 12%.

Logistics providers are embedding warehouse management systems that feed shipment visibility to shippers, enabling predictive replenishment and smoothing seasonal peaks. As CEP networks densify, "white-glove" two-person deliveries for appliances and electronics are emerging as value-added niches. The government's Land Bridge concept aims to divert trans-Indo-Pacific container flows through southern seaports, which could further expand the Thailand freight and logistics market size for freight transport by mid-decade. In contrast, forwarders expect margin uplift in CEP as operators implement zone-based pricing and fuel surcharge mechanisms.

The Thailand Freight and Logistics Market Report is Segmented by End User Industry (Agriculture, Fishing, and Forestry, Construction, Manufacturing, Oil and Gas, Mining and Quarrying, Wholesale and Retail Trade, and Others) and by Logistics Function (Courier, Express, and Parcel (CEP), Freight Forwarding, Freight Transport, Warehousing and Storage, and Other Services). The Market Forecasts are Provided in Terms of Value (USD).