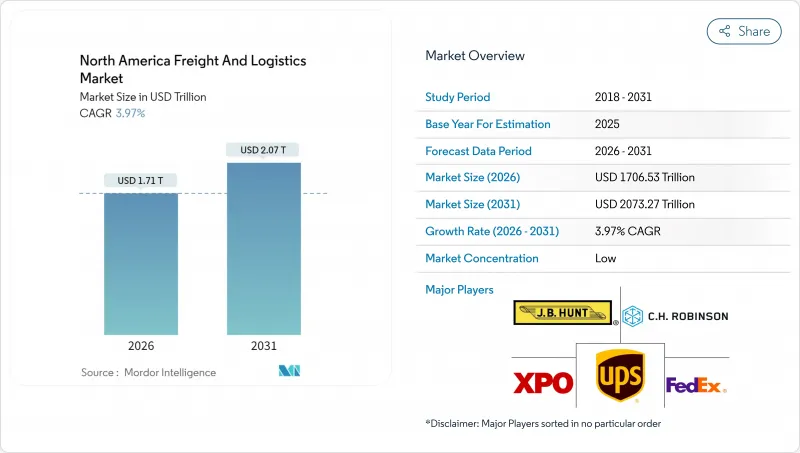

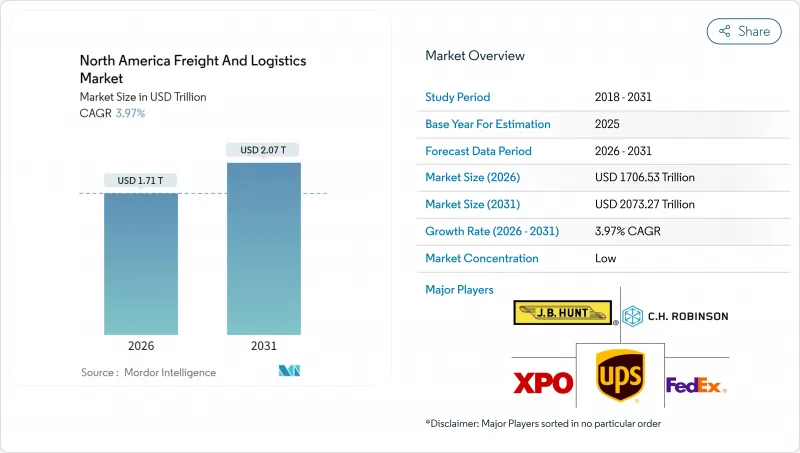

북미의 화물 및 물류 시장은 2025년에 1조 6,413억 7,000만 달러로 평가되었고, 2026년 1조 7,065억 3,000만 달러에서 2031년까지 2조 732억 7,000만 달러에 이를 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 3.97%로 예상됩니다.

미국-멕시코-캐나다 협정(USMCA)에 따른 강력한 무역 통합, 급증하는 전자상거래 물동량, 연방정부가 지원하는 인프라 현대화 프로젝트가 이 회랑의 전략적 중요성을 강화하고 투자 흐름을 뒷받침하고 있습니다. 2024년 국경 간 무역은 사상 최고치를 기록했고, 캐나다와 미국 간 무역액은 7,800억 달러, 멕시코와 미국 간 무역액은 8,078억 달러에 달할 것으로 예측됩니다. 멕시코로의 니어쇼어링 가속화와 1,100억 달러 규모의 미국 운송 자금이 결합되어 화물 운송 회랑의 재구축과 기술 중심의 효율화가 진행되고 있습니다. 한편, 인력 부족과 사이버 보안 위협은 운송 능력을 제약하고 자동화 도입을 촉진하는 동시에 강력한 네트워크의 필요성을 높이고 있습니다. 이러한 배경에서 북미 화물 및 물류 시장은 단기적인 운영상의 역풍이 있겠지만, 기술 혁신을 통해 꾸준한 성장이 예상됩니다.

2024년 2분기 전자상거래 보급률은 소매 매출의 15.6%에 이르렀으며, 연간 240억 개 이상의 소포를 발생시켜 기존 라스트마일 운송 능력을 넘어섰습니다. 이에 사업자는 도심지 마이크로 풀필먼트 허브 설치, 자율주행 배송 밴 시범 운영, 긱 이코노미 배송원 활용 등을 통해 연간 취급량의 40%를 차지하는 피크타임에 유연하게 대응할 수 있는 역량을 강화했습니다. 당일 및 익일 배송에 대한 기대는 120억 달러 규모의 도시 물류 부동산 시장을 창출하고 있으며, 아마존이 2024년 150개의 새로운 배송 스테이션을 개설한 것이 이를 증명하고 있습니다. 미국과 캐나다 규제 당국은 제한적인 드론 비행 통로를 승인하여 대체 운송 수단에 대한 제도적 지원을 보여주었습니다. 소포 밀도 증가(2022년 대비 35% 증가)로 인해 도로의 혼잡이 심해짐에 따라 운송업체들은 차량 체류시간과 배출가스를 줄이는 집약형 배송 모델을 시범 도입하고 있습니다.

USMCA로 인해 2024년 3국간 교역액은 1조 6,000억 달러에 달하고, 화물 운송량은 전년 대비 8.2% 증가할 것으로 예측됩니다. 라레도, 디트로이트 등 국경 검문소에서는 자동 통관 플랫폼으로 통관 시간이 최대 30% 단축되는 반면, 멕시코의 4,550억 달러 규모의 수출은 고부가가치 부품에 대한 복잡한 역물류 수요를 창출하고 있습니다. 2024년 캐나다 태평양 철도와 캔자스시티 레일웨이의 합병으로 캐나다 항구와 멕시코의 산업지대를 직접 연결하는 최초의 단일 노선 서비스가 구축되어 운송 시간을 단축하고 화물 수령 횟수를 최소화할 수 있게 되었습니다. 강화된 디지털 무역 규정으로 화물 추적이 실시간으로 이루어지고, 유통량이 많은 국경 지역에서의 체류 시간이 약 90분으로 단축되었습니다. 국경 양측의 콜드체인 및 자동차 물류 센터에 대한 투자는 북미 화물 및 물류 시장의 전략적 깊이를 강조하고 있습니다.

2024년 기준 북미 전역에서 8만 개 이상의 상용 운전직과 60만 개 이상의 창고 업무 일자리가 미충원된 상태이며, 남부 캘리포니아, 텍사스 트라이앵글 등 핫스팟에서는 이직률이 75%를 넘어선 것으로 나타났습니다. 운송업체들이 인력 확보 경쟁을 벌이는 가운데 임금 총액은 15-20% 상승했고, 노동력의 평균 연령은 47세를 넘어 장기적인 운송 능력에 대한 우려를 낳고 있습니다. 2024년 자동화 투자액은 48억 달러에 달할 것으로 예상되며, 기업들은 로봇 분류 시스템과 자율 주행 야드 트럭을 도입했습니다. 젊은 운전자의 주 간 화물 운송을 허용하는 연방 정부의 특례 조치가 시행되고 있지만, 2026년 이전에 인력 부족이 크게 완화될 가능성은 희박합니다.

제조업의 28.95%의 점유율은 적시성(Just In Time) 방식의 정착과 복잡한 반품 흐름을 보여줍니다. 반도체, 전기자동차, 의료기기 제조업체들은 통제된 환경과 안전한 운송에 대한 요구사항을 주도하고 있습니다. 니어쇼어링이 진행되면서 제조업체들은 생산 마일스톤과 화물 마일스톤을 통합하고 완충재고를 줄이는 엔드투엔드 가시성 툴을 원하고 있습니다.

옴니채널 대응의 추진으로 도매 및 소매업은 4.21%의 연평균 복합 성장률(CAGR)(2026-2031년)로 가장 빠르게 성장하고 있습니다. 소매업체들은 배송 시간을 단축하기 위해 재고를 분산시키고, 매장과 온라인 재고 풀을 통합하고 있습니다. 온도 관리형 식료품 물류에 대한 관심이 높아지면서 북미 화물 및 물류 시장에서 콜드체인에 대한 투자가 더욱 확대되고 있습니다. 역물류의 취급량이 증가함에 따라 반품 물품을 신속하게 선별하여 재판매 또는 재활용할 수 있는 운송업체가 점유율을 확대할 것입니다.

화물 운송은 2025년 매출의 62.58%를 차지하며 북미 화물 및 물류 시장에서 핵심적인 역할을 재확인했습니다. 이 기능은 도로 운송이 지배하고 있지만, 화주가 비용과 지속가능성을 우선시함에 따라 철도 컨테이너 운송의 점유율이 점차 증가하고 있습니다. 이 부문에서는 텔레매틱스를 활용한 예지보전을 통해 예기치 못한 다운타임을 줄이고 배송시간의 정확성을 높이고 있습니다. 자동화 시범사업은 장거리 플래토닝과 야드 내 작업용 로봇으로 확대되고 있으며, 향후 10년간 유인자산과 자율자산의 단계적 융합이 진행될 것임을 시사하고 있습니다.

CEP 서비스는 규모는 작지만 전자상거래의 성장으로 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 4.4%로 확대될 것으로 예측됩니다. 도시 고밀도 네트워크와 알고리즘에 의한 경로 최적화를 기반으로 미국 가구의 75%에서 당일 배송이 가능해졌습니다. 소규모 배송업체는 실시간 수요에 따라 운송 능력을 조정하는 동적 가격 책정 엔진을 시범 운영 중입니다. 이러한 추세는 퍼스트마일 및 라스트마일 배송의 혁신이 북미 화물 및 물류 시장 전반의 경쟁 우위를 결정짓는다는 것을 시사하고 있습니다.

The North America freight and logistics market was valued at USD 1641.37 billion in 2025 and estimated to grow from USD 1706.53 billion in 2026 to reach USD 2073.27 billion by 2031, at a CAGR of 3.97% during the forecast period (2026-2031).

Robust USMCA-driven trade integration, surging e-commerce parcel volumes, and federally funded infrastructure modernization projects are reinforcing the strategic importance of the corridor and underpinning investment flows. Cross-border trade reached record levels in 2024, with Canada-U.S. commerce hitting USD 780 billion and Mexico-U.S. flows touching USD 807.8 billion. Accelerated near-shoring to Mexico, complemented by USD 110 billion in U.S. transportation funding, is reshaping freight corridors and injecting technology-led efficiencies. At the same time, labor shortages and cybersecurity threats are constraining capacity, spurring automation adoption, and heightening the need for resilient networks. Against this backdrop, the North America freight and logistics market is poised for steady, technology-enabled growth despite short-term operational headwinds.

E-commerce penetration reached 15.6% of retail sales in Q2 2024, generating more than 24 billion parcels annually and outstripping legacy last-mile capacity. Operators responded by deploying micro-fulfillment hubs within city limits, piloting autonomous delivery vans and tapping gig-economy couriers to flex capacity during peak periods that now account for 40% of yearly throughput. Same-day and next-day expectations have unlocked a USD 12 billion urban logistics real-estate opportunity, evidenced by the 150 new delivery stations Amazon opened in 2024. Regulators in both the United States and Canada have cleared limited drone corridors, signaling institutional backing for alternative modes. Higher parcel density-up 35% since 2022-has intensified curbside congestion, prompting carriers to test consolidated drop-off models that lower vehicle dwell times and emissions.

USMCA enabled USD 1.6 trillion in trilateral trade during 2024, with freight flows rising 8.2% year over year. Automated customs platforms now trim clearance times by up to 30% at crossings such as Laredo and Detroit, while Mexican exports of USD 455 billion are generating complex reverse-logistics needs for high-value components. The 2024 Canadian Pacific Kansas City rail merger established the first single-line service that links Canadian ports directly to Mexican industrial zones, compressing transit times and minimizing handoffs. Enhanced digital trade provisions support real-time cargo tracking, further reducing border dwell times to roughly 90 minutes at high-volume lanes. Investments in cold-chain and automotive logistics centers on both sides of the border highlight the strategic depth of the North America freight and logistics market.

More than 80,000 commercial driving positions and 600,000 warehouse roles remained unfilled across North America in 2024, with churn surpassing 75% in hot spots such as Southern California and the Texas Triangle. Wage bills climbed 15-20% as carriers competed for talent, yet the workforce median age crept past 47 years, threatening long-term capacity. Automation spend reached USD 4.8 billion in 2024 as firms implemented robotic sortation and autonomous yard trucks. Federal waivers allowing younger drivers to haul interstate freight are in place, but meaningful labor relief is unlikely before 2026.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Manufacturing's 28.95% share signals entrenched just-in-time practices and complex returns flows. Semiconductor, electric-vehicle and medical-device producers are driving requirements for controlled environments and secured transport. Even amid near-shoring, manufacturers are demanding end-to-end visibility tools that integrate production milestones with freight milestones, shrinking buffer inventories.

Wholesale and retail trade, propelled by omnichannel fulfillment, is the fastest mover at a 4.21% CAGR (2026-2031). Retailers are decentralizing inventory into micro-fulfillment sites to cut delivery times while blending store and online stock pools. Temperature-controlled grocery logistics are seeing heightened interest, supporting further cold-chain investment in the North America freight and logistics market. As reverse-logistics volumes rise, carriers that can quickly triage returns for resale or recycling will gain share.

Freight Transport controlled 62.58% of revenue in 2025, reaffirming its backbone role within the North America freight and logistics market. Road haulage dominates this function, yet rail intermodal share is creeping upward as shippers prioritize cost and sustainability. The segment is leveraging telematics for predictive maintenance, trimming unplanned downtime, and tightening delivery windows. Automation pilots now span long-haul platooning and yard-hostler robotics, pointing to a gradual blend of manned and autonomous assets through the decade.

CEP services, while smaller, are expanding at a 4.4% CAGR (2026-2031) thanks to e-commerce. Same-day coverage is now feasible for 75% of U.S. households, underpinned by dense urban networks and algorithmic route optimization. Parcel carriers are experimenting with dynamic pricing engines that match capacity to real-time demand. Combined, these dynamics reinforce that innovation in first- and last-mile delivery will shape competitive positioning across the broader North America freight and logistics market.

The North America Freight and Logistics Market Report is Segmented by Logistics Function (Courier, Express, and Parcel, Freight Forwarding, Freight Transport, Warehousing and Storage, and Other Services), End User Industry (Agriculture, Fishing, and Forestry, Construction, Manufacturing, Wholesale and Retail Trade, and More), and Geography (United States, Canada, and More). The Market Forecasts are Provided in Terms of Value (USD).