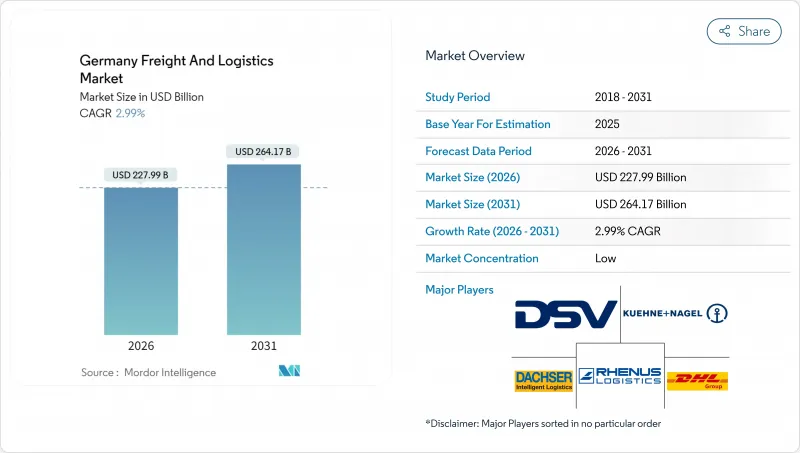

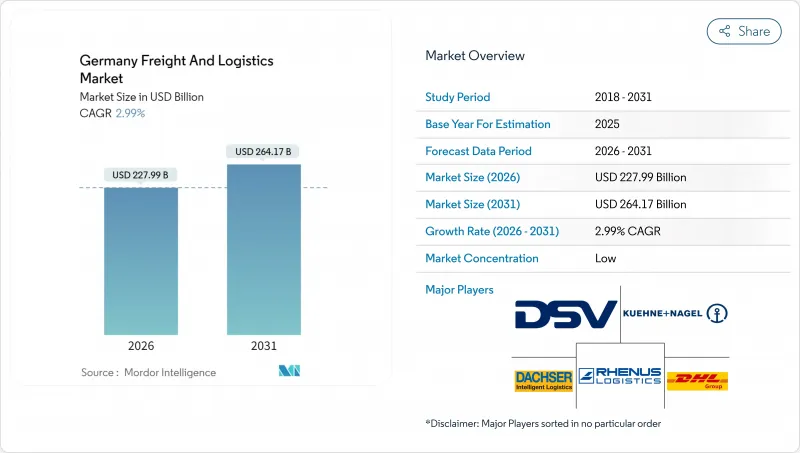

독일의 화물 및 물류 시장은 2025년 2,213억 7,000만 달러에서 2026년에는 2,279억 9,000만 달러로 성장할 것으로 보입니다. 2026-2031년에 걸쳐 CAGR 2.99%로 성장할 것으로 예상되며, 2031년까지 2,644억 달러에 달할 전망입니다.

이 완만한 성장 속도는 이미 성숙한 생태계가 전자상거래 물류, 수출 중심 제조 회랑, 그리고 도로 운송에 대한 탄소 비용을 인상하는 유럽 그린딜 규정을 중심으로 재편되고 있음을 반영합니다. 2030년까지 총 17억 유로(19억 달러) 규모의 철도 인센티브 패키지와 톤당 55유로(60.7달러)로 꾸준히 상승하는 탄소 가격은 화주들이 유연하고 단거리 운송에는 여전히 도로를 이용하면서도 복합 운송 솔루션으로 전환하도록 유도하고 있습니다. 동시에 택배·특송·소포(CEP) 시장은 소비자 온라인 쇼핑 침투율 87%에 힘입어 성장세를 가속화하며, 소포 밀도가 1인당 54개 이상으로 증가하고 도시 물류센터의 자동화 투자도 확대되고 있습니다. 운전자 부족 현상(2025년 기준 7만 개 공석)이 심화되면서 트럭 운송 능력은 축소되고 임금은 상승해, 운송사들은 경로 최적화 소프트웨어 도입과 자율주행 야드 트랙터 시험 운행을 추진하고 있습니다. 이러한 구조적 변화 속에서 독일의 화물 및 물류 시장은 중앙 유럽의 지리적 위치, 41,000km에 달하는 고속도로망, 세계적 수준의 항구를 활용하여 유럽 대륙의 무역 흐름을 계속해서 주도하고 있습니다.

독일의 전자상거래 보급률은 2024년에 87%에 도달하여 연간 45억 개의 소포를 처리하고, 현재 주민 1인당 평균 54회의 배송을 처리하는 밀집된 라스트 마일 네트워크를 구축하고 있습니다. 아마존 프레시와 레베의 당일 배송 서비스 확대로 식료품 플랫폼은 전년 대비 23% 성장했으며, 이에 대응해 운영사들은 프랑크푸르트에서 트램 기반 배송 시범 운영을, 베를린·함부르크·뮌헨에서는 주차장 내 마이크로 물류센터를 도입했습니다. 택배 통합업체들은 시간당 3만 개 처리 가능한 고속 분류기를 설치하고 저공해 구역 규정을 준수하기 위해 전기 배송 밴을 추가했습니다. 싱글스데이와 크리스마스 같은 계절적 성수기는 도시 도로를 과부하시켜 지방자치단체의 도시 물류 통합 계획 수립을 최우선 과제로 만들었다. 소형 소포의 지속적인 유입은 CEP 네트워크에 로봇공학, AI 기반 수요 예측, 유연한 교대 근무 스케줄링의 전략적 가치를 강화합니다.

독일의 공장들은 글로벌 변동성 속에서도 2024년 1조 5,600억 유로(1조 7,200억 달러) 상당의 상품을 수출했습니다. 이는 다각화된 수출 시장과 핵심 원자재의 근거리 조달 덕분입니다. 자동차 제조사들은 바이에른주와 바덴뷔르템베르크주의 최종 조립 공장 반경 500km 내에 1차 공급업체를 집적시켜 운송 리드타임을 단축하고 순차적 공급 흐름을 안정화했습니다. 기계 및 화학 수출업체들은 함부르크-뮌헨 및 라인-루르 회랑에서 장기 철도 운송 계약을 체결해 화차 회전율을 15% 개선하고 디젤 가격 급등으로부터 마진을 보호했습니다. 예측 가능한 화물 회랑 덕분에 물류 업체들은 대용량 셔틀을 운영하고 터미널 운영사와 물량 기반 할인을 협상할 수 있습니다. 수출 안정성은 독일 화물 및 물류 시장의 기반을 계속해서 뒷받침하며, 온도 조절 컨테이너, 특수 프로젝트 화물 장비, 관세 준수 서비스에 대한 수요를 유지하고 있습니다.

2025년 기준 공석은 70,000명에 달하며, 면허 소지 트럭 운전자의 39%가 55세 이상으로 차량 가동률이 저하되고 성수기에는 트랙터의 7-10%를 주차해야 하는 상황입니다. 운전학교는 연간 18,000명의 신규 운전자를 배출하는 반면, 은퇴로 인한 이탈은 25,000명을 초과해 기술 격차가 확대되고 있습니다. 운송사들은 임금을 10% 인상하고 입사 보너스를 제공했지만, 야간 근무, 장기간 집을 떠나야 하는 생활 방식, 복잡한 규제 등 생활 방식상의 장벽이 인력 유입을 제한하고 있습니다. 임시 방편으로 화주들은 배송 시간을 분산하고, 철도 블록을 전세 내며, 창고 부지 내에서 자율주행 셔틀을 시험 운영하여 인간 운전자가 도로 구간 운전에 집중할 수 있도록 하고 있습니다. 이 부족 현상은 자동화나 이민 해결책이 등장할 때까지 독일 화물 및 물류 시장의 성장 잠재력을 제약할 것입니다.

2025년 시점에서 제조업은 독일의 화물 및 물류 시장 점유율의 28.37%를 차지하며 물류 지출액으로 환산하면 628억 1,000만 달러에 이를 전망입니다. 이 부문의 견고성은 순차적 JIT(적시 생산) 흐름에 의존하는 자동차, 기계 및 공정 산업 분야에서 독일의 깊은 전문성에서 비롯됩니다. 과도한 재고 가치와 공장 가동 시간 요구사항은 라인사이드 배송, 반환 가능 포장재, 하위 조립품에 대한 장기 다중 서비스 계약을 촉진합니다. 반면 도매 및 소매 무역은 현재 규모는 작지만, 옴니채널 모델이 매장, 다크 스토어, 소비자 직거래 채널 간 신속한 재고 보충을 요구함에 따라 2026-2031년 연평균 복합 성장률(CAGR) 3.18%를 기록할 전망입니다.

건설 물류는 중량물 운송 트럭과 프리팹 모듈의 현장 순차적 조립에 의존하여 성장 속도는 느리지만 꾸준한 활동 영역을 형성합니다. 농업·어업·임업 분야는 수확 성수기 동안 콜드 체인 역량과 시간 민감형 창구가 필요하여 냉장 트레일러 수요와 도시 시장으로의 복합운송 신선식품 운송로를 강화합니다. 석유, 가스, 광업 및 채석업은 독일의 에너지 전환 정책으로 풍력 및 태양광 설비 부품으로 물동량이 이동하면서 점유율이 소폭 하락했습니다. 의료 기술부터 수소 연료전지 부품에 이르는 신흥 분야는 복잡성과 온도 제어 마이크로 물류를 추가하여 전문 3PL 업체에 유리하게 작용합니다.

화물 운송은 2025년 59.29% 점유율로 여전히 핵심 분야였으나, 택배·특송 부문은 전자상거래 습관과 연계된 주거지 배송 물량 증가에 힘입어 2026-2031년 연평균 3.44% 성장률로 가장 빠른 확장을 보일 전망입니다. 기업들이 공급자 충격에 대비해 안전 재고를 확보함에 따라 창고 및 보관 부문도 성장세를 보일 전망입니다. 화물 운송 대행사는 디지털 예약 포털과 다중 모드 가시성 도구를 결합해 소규모 수출업체들이 운송 자산을 보유하지 않고도 프리미엄 항공 및 철도 서비스를 이용할 수 있도록 지원하며 변화에 대응하고 있습니다.

독일의 화물 및 물류 시장에서는 부가가치 서비스(키트 조립, 간이 조립, 반품 처리 등)가 '기타' 카테고리에서 계속 중시되고 있으며, 이들은 제조업의 린 생산 방식을 보완하는 것입니다. 독일의 밀집된 소비자 기반 덕분에 국내 CEP(특송) 시장 점유율은 66.56%를 기록했으나, 유럽 단일 시장 내 폴란드, 프랑스, 북유럽 쇼핑객을 공략하는 상인들의 영향으로 국경 간 CEP 노선의 성장세가 더 강합니다. 화물 운송 하위 부문별 운명은 엇갈린다. 대량 트럭 운송은 탄소세 부담을 직격받는 반면, 특화 자동차 정기 배송은 안정적인 계약 수익을 창출합니다. DSV의 DB 쉔커 인수를 대표로 하는 3PL 간 기회주의적 통합은 소포 통합업체 및 항만 터미널에 대한 협상력을 증폭시킨다.

The Germany freight and logistics market is expected to grow from USD 221.37 billion in 2025 to USD 227.99 billion in 2026 and is forecast to reach USD 264.17 billion by 2031 at 2.99% CAGR over 2026-2031.

The moderate growth pace reflects an already-mature ecosystem that is repositioning around e-commerce fulfillment, export-oriented manufacturing corridors, and European Green Deal rules that raise carbon costs for road haulage. Rail incentive packages worth EUR 1.7 billion (USD 1.9 billion) through 2030, coupled with steadily climbing carbon prices of EUR 55 (USD 60.7) per tonne, are steering shippers toward intermodal solutions while still relying on road for flexible, short-haul moves. At the same time, the courier, express, and parcel (CEP) wave gains momentum from 87% consumer online-shopping penetration, pushing parcel density past 54 items per capita and accelerating automation investments in urban depots. Rising driver vacancies-70,000 open positions in 2025-tighten trucking capacity and elevate wages, motivating carriers to adopt route-optimization software and test autonomous yard tractors. Amid these structural shifts, the Germany freight and logistics market continues to leverage its central European location, 41,000 km highway grid, and world-class ports to anchor continental trade flows.

Germany's e-commerce penetration hit 87% in 2024, translating into 4.5 billion annual parcels and driving a dense last-mile network that now averages 54 deliveries per resident. Grocery platforms grew 23% year over year as Amazon Fresh and Rewe expanded same-day services, prompting operators to pilot tram-based drop-offs in Frankfurt and micro-depots in parking structures across Berlin, Hamburg, and Munich. Parcel integrators responded by installing high-speed sorters capable of 30,000 items per hour and by adding electric delivery vans to comply with low-emission-zone rules. Seasonal peaks such as Singles' Day and Christmas overloaded city streets, making urban consolidation schemes a priority for municipalities. The sustained flow of small parcels reinforces the strategic value of robotics, AI-driven demand forecasting, and flexible shift scheduling for CEP networks.

German factories shipped EUR 1.56 trillion (USD 1.72 trillion) worth of goods in 2024 despite global volatility, thanks to diversified destination markets and near-shoring of critical inputs. Automakers clustered tier-1 suppliers within 500 km of final-assembly plants in Bavaria and Baden-Wurttemberg, trimming transport lead times and stabilizing just-in-sequence flows. Machinery and chemical exporters locked in long-term rail contracts on the Hamburg-Munich and Rhine-Ruhr corridors, improving wagon-turnaround rates by 15% and shielding margins from diesel price spikes. The predictable freight corridors enable logistics providers to run high-capacity shuttles and negotiate volume-based discounts with terminal operators. Export reliability continues to underpin the Germany freight and logistics market, sustaining demand for temperature-controlled containers, specialized project cargo gear, and customs compliance services.

Vacancies hit 70,000 in 2025, with 39% of licensed truckers older than 55, eroding fleet utilization and forcing companies to park 7-10% of tractors during peak weeks. Training schools graduate only 18,000 new drivers annually, against retirement outflows above 25,000, widening the skills gap. Carriers raised wages 10% and offered sign-on bonuses, but lifestyle deterrents-night work, days away from home, dense regulation-limit attraction. As a stop-gap, shippers stagger delivery windows, charter rail blocks, and trial autonomous shuttles inside warehouse yards to free humans for open-road segments. The shortage constrains the Germany freight and logistics market's growth potential until automation or immigration solutions emerge.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Manufacturing accounted for 28.37% of Germany freight and logistics market share in 2025, translating into USD 62.81 billion in logistics spend. The segment's robustness derives from Germany's deep specialization in autos, machinery, and process industries that rely on sequenced just-in-time flows. Outsized inventory values and plant uptime requirements foster long-term, multi-service contracts for line-side delivery, returnable packaging, and sub-assembly. In contrast, wholesale and retail trade, while smaller at present, registers a 3.18% CAGR (2026-2031) as omnichannel models force rapid replenishment between stores, dark stores, and direct-to-consumer channels.

Construction logistics hinges on heavy-lift trucking and on-site sequencing for prefabricated modules, creating a steady if slower-growing slice of activity. Agriculture, Fishing & Forestry calls for cold chain capacity and time-critical windows during harvest peaks, bolstering reefer trailer demand and multimodal fresh-produce corridors to urban markets. Oil, Gas, Mining & Quarrying edges downward as Germany's Energiewende moves tonnage toward components for wind and solar installations. Emerging verticals, from medical technology to hydrogen fuel-cell components, add complexity and temperature-controlled micro-flows that favor specialized 3PLs.

Freight Transport remained the cornerstone at 59.29% share in 2025; however, the Courier, Express, and Parcel arm is forecast to post the quickest expansion at 3.44% CAGR between 2026-2031, propelled by residential delivery volumes tied to the e-commerce habit. Growth also favors Warehousing & Storage, which absorbs safety stocks as firms hedge against supplier shocks. Freight Forwarding adapts by bundling digital booking portals with multimodal visibility tools, enabling smaller exporters to tap premium air and rail services without owning transportation assets.

The Germany freight and logistics market continues to prioritize value-added services such as kitting, light assembly, and returns processing under the Others banner, all of which complement manufacturers' lean-production mandates. Domestic CEP registered a 66.56% share thanks to Germany's dense consumer base, yet cross-border CEP lanes inside the European single market post stronger growth as merchants court Polish, French, and Nordic shoppers. Freight Transport sub-segments show diverging fortunes: bulk trucking feels the brunt of carbon taxes, while specialized automotive milk-runs deliver stable contract revenue. Opportunistic consolidation among 3PLs, exemplified by DSV's purchase of DB Schenker, amplifies bargaining power over parcel integrators and port terminals.

The Germany Freight and Logistics Market Report is Segmented by End User Industry (Agriculture, Fishing, and Forestry, Construction, Manufacturing, Oil and Gas, Mining and Quarrying, Wholesale and Retail Trade, and Others) and by Logistics Function (Courier, Express, and Parcel (CEP), Freight Forwarding, Freight Transport, Warehousing and Storage, and Other Services). The Market Forecasts are Provided in Terms of Value (USD).