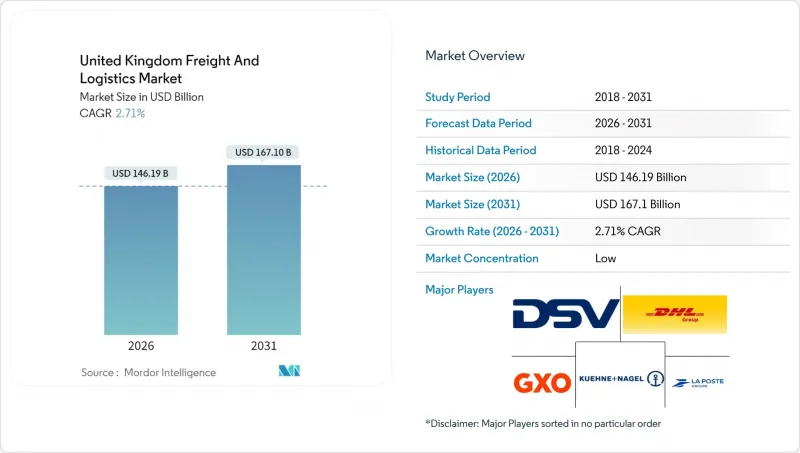

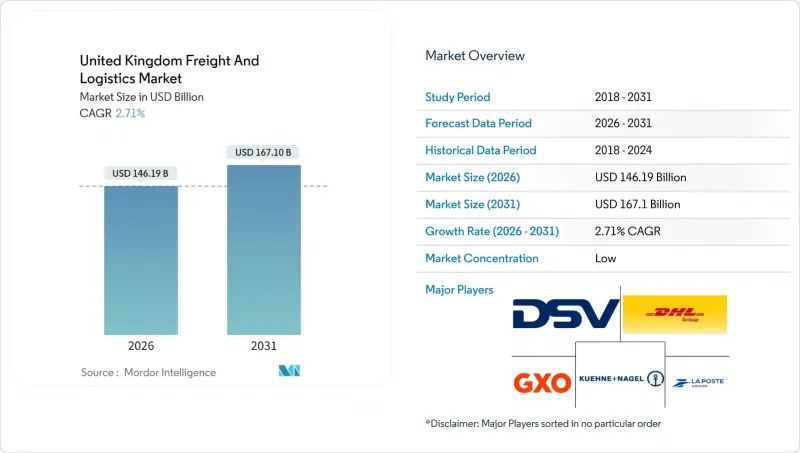

영국의 화물 및 물류 시장은 2025년 1,423억 3,000만 달러에서 2026년에는 1,461억 9,000만 달러로 성장하며, 2026-2031년에 CAGR 2.71%로 추이하며, 2031년까지 1,671억 달러에 달할 것으로 예측됩니다.

이러한 꾸준한 성장 궤적은 성숙하면서도 적응력이 뛰어난 이 분야가 E-Commerce 이동, 제조 니어쇼어링, 디지털 통관을 중심으로 스스로를 재구성하고 있음을 반영하고 있습니다. 도시 지역의 소포 밀도 증가, 브로커 업무 흐름의 자동화, 심해항구의 인프라 구축 노력은 물동량 모멘텀을 강화하는 반면, 운전자 층의 고령화와 지정학적 해운 충격은 성장 곡선을 억제하고 있습니다. 도로, 철도, 해상, 항공 등 다양한 운송수단의 균형으로 영국 화물 및 물류 시장은 견고한 성장세를 유지하고 있습니다. 그러나 홍해를 통한 우회 운송으로 인한 수입 비용 상승과 리튬 배터리의 보험 요건은 프리미엄 항공화물의 흐름을 복잡하게 만드는 요인으로 작용하고 있습니다. 경쟁의 강도는 여전히 중간 정도이며, 최근 대형 인수합병은 규모 확대, 기술 심화, 환경 규제 대응력 등 우위로의 전환을 시사하고 있습니다.

2025년 영국 온라인 소매 지출의 견고한 증가는 경로당 소포 배송 건수를 증가시켜 배송 단가를 낮추고 당일 배송 서비스의 경제성을 향상시키고 있습니다. 아마존이 오프라인 식료품 사업에서 철수하고 택배 서비스에 다시 집중하고 있는 것은 디지털 퍼스트(Digital First)를 강조하고 있습니다. Co-op과 같은 퀵커머스 사업자는 현재 83%의 가구에 서비스를 제공하고 있으며, Gopuff와 Morrisons의 제휴를 통해 낮 시간대 매장 용량을 다크 스토어 운영에 재사용하고 있습니다. 런던 대도시권 및 맨체스터의 고밀도 발착지 클러스터에서는 마이크로 풀필먼트 처리 용량이 평방피트당 40-50% 증가하여 도시 지역 분류 로봇에 대한 추가 투자를 촉진하고 있습니다. 이러한 밀도 증가는 노동력과 연료의 인플레이션을 상쇄하고 대체 연료 차량의 규모 기반을 구축함으로써 영국의 화물 및 물류 시장을 지원하고 있습니다.

방산 조달, 의약품, 정밀 엔지니어링 분야에서 공급업체들의 거점이 유럽 대륙에서 영국으로 단계적으로 회귀하는 움직임이 가속화되고 있습니다. 북서부 및 웨스트미들랜드 지역 클러스터의 생산량은 2033년까지 12% 증가할 것으로 예상되며, 산업단지와 수출 기지 간의 중간 하역 화물 수요를 창출할 것입니다. 셰필드에 신설된 BAE시스템즈의 96,000평방피트(약 8,900평방미터) 규모의 새로운 시설은 이러한 변화를 상징하며, 제조업체의 69%가 국내 조달 비율을 심화할 계획을 가지고 있습니다. 안정적인 수주 흐름은 간선 노선의 가동률을 평준화하여 영국 화물 및 물류 시장 전체에서 운송업체와 철도화물 사업자의 운송 용량 투자를 지원하고 있습니다.

대형 화물차 운전자의 평균 연령은 55세를 넘어섰고, 견습생 등록자 수는 충원 인원보다 약 40%가량 적습니다. 15-20%의 임금 인상과 엄격한 자격 취득 기간으로 인해 운송업체들은 자율주행차량의 시험 운행과 유연한 교대제 운영으로 전환하고 있습니다. 특히 온도관리형 및 위험물 운송 분야의 부족이 두드러져 영국 화물 및 물류 시장 전체의 운영 리스크를 높이고 있습니다.

제조업은 2025년 매출의 36.85%를 차지할 것으로 예상되며, 북서부 및 남서부 지역의 제약 및 항공우주 산업 클러스터의 수혜를 받을 것으로 예측됩니다. 국내 조달 동향(생산자의 69%가 영국 공급업체를 추가할 계획)이 중거리 운송량의 안정성을 지원하고 있습니다. 도소매업은 2026-2031년 연평균 복합 성장률(CAGR) 2.97%로 확대될 것이며, 식료품 EC의 보급과 옴니채널 대응이 반영된 것으로 분석됩니다.

퀵커머스 네트워크가 런던 외곽으로 확장됨에 따라 2031년까지 영국의 도매 및 소매업 화물 및 물류 시장 점유율은 2포인트 상승할 것으로 예측됩니다. 건설물류는 공공 부문의 인프라 사업에 힘입어, 석유-가스-광업-채석업은 해상풍력발전과 수소 파이프라인으로 전환하고 있습니다. '기타' 카테고리에는 재생에너지 장비 물류와 같은 신흥 분야가 포함되어 영국 화물 및 물류 시장 전반 수요 다변화를 촉진하고 있습니다.

2025년 영국 화물 및 물류 시장 매출의 63.02%는 화물 운송이 차지할 것으로 예상되며, 항만, 공항, 미들랜드 지역 물류 거점 간의 원활한 연결성을 활용하고 있습니다. 택배, 익스프레스 배송, 소포 서비스는 소포 밀도 증가와 자율 분류 시스템 도입을 배경으로 2026-2031년 연평균 복합 성장률(CAGR) 3.12%를 나타낼 것으로 예측됩니다. 적극적인 통합으로 전통적 분야의 경계가 모호해지고, 여러 서비스 프로바이더가 운송, 창고, 중개 업무를 결합하여 엔드 투 엔드 계약을 체결하고 있습니다.

영국의 택배, 익스프레스 배송, 소포 부문의 화물 및 물류 시장 규모는 24시간 배송에 대한 기대감으로 인해 2031년까지 241억 8,000만 달러에 달할 것으로 예측됩니다. 창고 및 보관 서비스는 재고 완충 전략의 혜택을 받고, 화물 운송은 통관 자동화를 통한 경제 효과를 중심으로 전개됩니다. 프로젝트 화물 운송 및 역물류와 같은 전문적인 '기타 서비스'는 재생에너지 사이클과 순환형 공급망을 수익화하여 거시경제의 변동에 대한 저항력을 보여주고 있습니다.

The United Kingdom freight and logistics market is expected to grow from USD 142.33 billion in 2025 to USD 146.19 billion in 2026 and is forecast to reach USD 167.1 billion by 2031 at 2.71% CAGR over 2026-2031.

This steady trajectory reflects a mature yet adaptive sector that is reshaping itself around e-commerce fulfillment, manufacturing near-shoring, and digital customs processing. Parcel density gains in urban areas, automation of broker workflows, and infrastructure commitments at deep-sea ports are reinforcing throughput momentum, while an aging driver pool and geopolitical shipping shocks temper the growth curve. Balance across road, rail, sea, and air modes keeps the United Kingdom freight and logistics market resilient, even as Red Sea re-routing inflates inbound costs and lithium-battery insurance requirements complicate premium air cargo flows. Competitive intensity remains moderate, with recent blockbuster acquisitions indicating a shift toward scale, technology depth, and environmental compliance advantages.

Robust U.K. online retail spending in 2025 is lifting parcel stops per route, which lowers per-delivery cost and improves same-day service economics. Amazon's exit from brick-and-mortar grocery and renewed focus on home delivery underline a digital-first mindset. Quick-commerce operators such as Co-op now reach 83% of households, while Gopuff's partnership with Morrisons repurposes daytime store capacity to dark-store operations. Dense origin-destination clusters in Greater London and Manchester have seen micro-fulfillment throughput rise 40-50% per square foot, encouraging further investment in urban sortation robotics. These density gains sustain the United Kingdom freight and logistics market by offsetting labor and fuel inflation and by anchoring scale for alternative-fuel fleets.

Defense procurement, pharmaceuticals, and precision engineering are fueling a gradual relocation of supplier footprints from continental Europe back to the United Kingdom. Output from regional clusters in the North West and West Midlands is projected to rise 12% by 2033, adding mid-haul freight demand between industrial parks and export gateways. BAE Systems' new 96,000-square-foot facility in Sheffield exemplifies the shift, while 69% of manufacturers plan to deepen domestic sourcing. Consistent order flows smooth utilization on trunk routes, underpinning capacity investments by hauliers and rail-freight operators across the United Kingdom freight and logistics market.

The median age of heavy-goods-vehicle operators has climbed past 55, while apprenticeship enrollments lag replacements by roughly 40%. Rising wage bills of 15-20% and tight certification windows push carriers toward autonomous-vehicle pilots and flexible shift scheduling. Scarcity is most pronounced in temperature-controlled and hazardous-materials niches, elevating operating risk across the United Kingdom freight and logistics market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Manufacturing generated 36.85% of turnover in 2025, benefitting from pharmaceutical and aerospace clusters in the North West and South West. Domestic sourcing trends, with 69% of producers planning to add U.K. suppliers, anchor steady mid-haul volumes. Wholesale and Retail Trade, expanding at a 2.97% CAGR (2026-2031), reflects grocery e-commerce diffusion and omnichannel fulfillment.

The United Kingdom freight and logistics market share for Wholesale and Retail Trade is set to climb by 2 percentage points by 2031 as quick-commerce networks extend beyond London. Construction logistics ride public-sector infrastructure programs, while Oil, Gas, Mining, and Quarrying pivot to offshore wind and hydrogen pipelines. The "Others" bucket covers nascent verticals such as renewable-equipment logistics, reinforcing demand diversification across the United Kingdom freight and logistics market.

Freight Transport owned 63.02% of 2025 revenue in the United Kingdom freight and logistics market, leveraging seamless connectivity between ports, airports, and Midlands distribution hubs. Courier, Express, and Parcel services enjoy a 3.12% CAGR (2026-2031) on the back of higher parcel density and autonomous sortation rollouts. Active consolidation blurs traditional silos, with multi-service providers bundling transport, warehousing, and brokerage to win end-to-end contracts.

The United Kingdom freight and logistics market size for the Courier, Express, and Parcel segment is projected to reach USD 24.18 billion by 2031, supported by 24-hour delivery expectations. Warehousing and Storage gains from inventory-buffer strategies, while Freight Forwarding pivots on customs-automation economies. Specialized "Other Services", such as project cargo and reverse logistics, monetise the renewable-energy cycle and circular supply chains, showing resilience against macro-volatility.

The United Kingdom Freight and Logistics Market Report is Segmented by End User Industry (Agriculture, Fishing, and Forestry, Construction, Manufacturing, Oil and Gas, Mining and Quarrying, Wholesale and Retail Trade, and Others) and by Logistics Function (Courier, Express, and Parcel, Freight Forwarding, Freight Transport, Warehousing and Storage, and Other Services). The Market Forecasts are Provided in Terms of Value (USD).