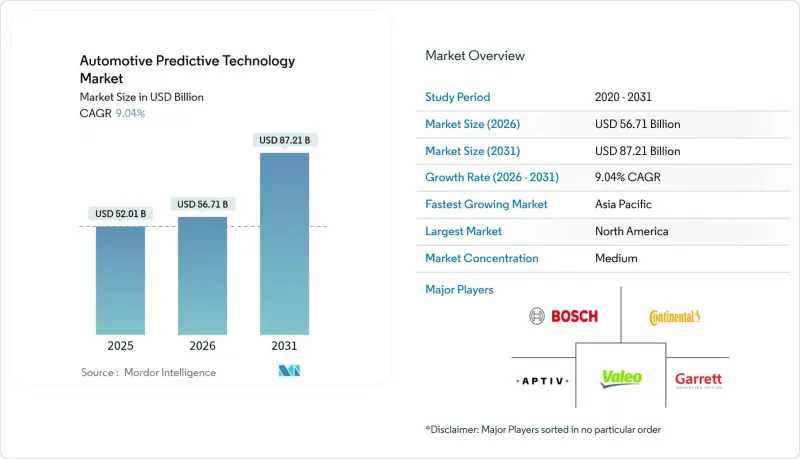

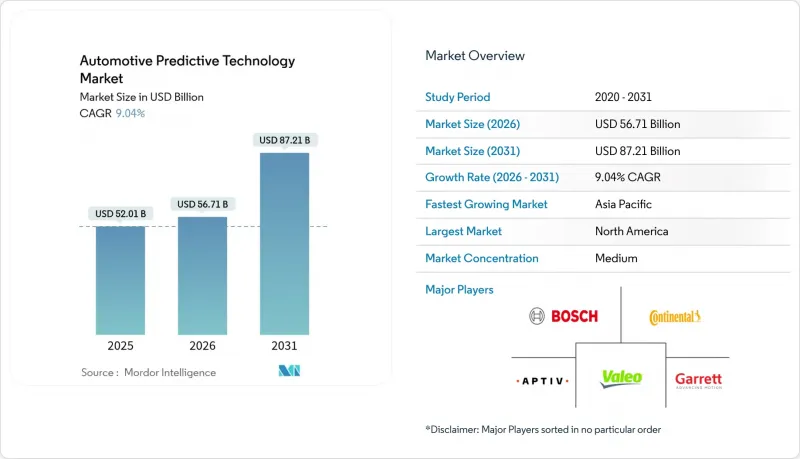

2026년 자동차 예측 기술 시장 규모는 567억 1,000만 달러로 추정되며, 2025년 520억 1,000만 달러에서 성장이 전망됩니다.

2031년까지 872억 1,000만 달러에 달할 것으로 예상되며, 2026년부터 2031년까지 CAGR 9.04%로 확대될 것으로 전망됩니다.

이러한 급속한 확장은 업계가 사후 대응형 유지보수에서 차량 아키텍처 내부에서 직접 실시간 인사이트를 제공하는 임베디드 인텔리전스로의 전환을 추진하고 있기 때문입니다. 엣지 컴퓨팅은 클라우드 분석을 보완하고, 안전에 중요한 기능에서 밀리초 단위의 의사결정을 가능하게 합니다. 상용차 관리자들은 예측 툴과 5G 텔레매틱스를 통합하여 계획되지 않은 유지보수가 눈에 띄게 감소했음을 입증했으며, 사용량 기반 분석을 채택한 보험사들은 보험금 청구 빈도가 감소했다고 보고하고 있습니다. 안전 및 배출가스 관련 규제 요건은 지속적으로 수요를 증가시키고 있으며, 센서 비용의 하락은 도입 장벽을 완화하고 있습니다. 이와 동시에 NVIDIA, Qualcomm, Microsoft 등의 기술 공급업체들이 자동차 등급 AI 칩셋과 확장 가능한 클라우드 플랫폼을 가치사슬에 투입하여 경쟁을 심화시키고 있습니다.

5G 텔레매틱스가 탑재된 상용차는 예측 알고리즘이 고해상도 센서 데이터를 20밀리초 미만의 지연으로 스트리밍하기 때문에 예기치 못한 서비스 발생이 크게 감소하고 있습니다. 4G를 훨씬 능가하는 네트워크 처리량으로 유지보수 시스템은 진동, 온도, 유체역학을 지속적으로 분석할 수 있습니다. 차량 운영자는 이러한 정보를 동적 서비스 스케줄로 변환하여 고정 간격 모델 대비 다운타임을 줄일 수 있습니다. 승용차도 마찬가지로 혜택을 누릴 수 있으며, 운전자는 차량 상태를 최상의 상태로 유지하기 위한 컴퓨팅 워크로드를 인지하지 못한 채 부품 수명을 최적화하는 예측 소프트웨어의 무선 업데이트(OTA)를 받을 수 있습니다.

자동차 제조사들은 차량 중앙제어장치에 신경망을 내장하고 있습니다. BMW의 iDrive 업그레이드는 여러 매개변수를 동시에 평가하고 개별화된 건강 진단을 생성하여 보증 청구를 줄입니다. OEM의 익명화된 차량 데이터 관리를 통해 알고리즘이 수백만 시간의 집합적인 주행 데이터로 재학습하기 때문에 신형 모델은 기존 모델보다 더 높은 수준의 지능을 갖출 수 있습니다. 이러한 지속적인 학습 프로세스는 제품 차별화를 재정의하고, 고장이 발생하기 전에 예측 가능한 브랜드에 소유자의 선택이 집중되도록 합니다. 이를 통해 부품 수명이 연장되고 잔존가치가 향상됩니다.

GDPR은 텔레매틱스 데이터를 익명화되어 있더라도 개인 식별 정보로 분류하고, 도입을 지연시키는 동의 획득 장벽을 마련하고 있습니다. 2024년에는 커넥티드카에 대한 사이버 공격이 증가하여 분산형 예측 아키텍처의 취약점이 부각될 것으로 예상됩니다. 자동차 제조사들은 암호화에 많은 투자를 하고 있지만, 소비자들은 여전히 프라이버시 우려를 구매를 망설이는 주요 이유로 꼽고 있습니다. 인증 체계가 성숙하기 전까지는 상시 연결 차량을 기피하는 구매자도 존재할 것입니다.

2025년 기준, 예측 유지보수는 자동차 예측 기술 시장의 48.62%를 차지했습니다. 정기점검에서 상태기반 수리로 전환한 차량에서 운영사업자는 유지보수 비용 절감 효과를 입증하고 있습니다. 운전자들이 실시간 알림을 중시하는 추세에 따라 사전 알림은 11.12%의 CAGR로 확대될 것으로 예상됩니다. 안전 및 보안 분석은 규제 당국의 첨단 운전 지원 시스템 의무화에 따라 더욱 탄력을 받고 있습니다. 한편, 교통 최적화는 예측 데이터와 스마트 시티 인프라를 융합하고 있습니다. 상업적 시나리오에서는 운전 행동 모니터링이 보험료 할인을 제공하는 보험 프로그램과 연계되어 도입을 더욱 가속화하고 있습니다.

이러한 사용 사례들이 융합되기 시작했습니다. 단일 소프트웨어 스택이 유지보수 알고리즘, 도로 위험 예측, 운전자 안내 대시보드를 동시에 공급할 수 있게 되어 향후 플랫폼 통합을 암시하고 있습니다. 유지보수 분석과 실시간 안전 경보를 결합한 벤더는 프리미엄 구독 및 데이터 수익화 기회를 주도할 수 있는 최적의 위치에 있습니다.

2025년 기준 승용차가 매출의 60.73%를 차지하는 반면, 중대형 상용차는 CAGR 9.86%로 가장 높은 성장세를 보이고 있습니다. 대형 트럭은 가동 중단 1시간마다 배송 기회 손실이 발생하기 때문에 예측 가동률 향상은 물류 사업자에게 즉각적인 투자 효과를 가져다 줍니다.

전기화는 이해관계를 더욱 확대할 것입니다: 배터리 예지보전은 현재 경로 계획, 충전 타이밍 최적화, 재판매 가격 설정에 정보를 제공하고 있습니다. 소형 상용차는 택배 배송 피크에 맞춰 정비를 동기화하는 예측 모듈을 채택한 EC Fleet를 통해 또 다른 성장 층을 추가하고 있습니다. 개인용 차량이 가장 큰 차량 기반을 유지하는 반면, 상업용 부문의 운영 압력은 향후 10년간의 제품 로드맵을 형성할 것입니다.

북미는 2025년 44.05%의 점유율을 차지했습니다. 이는 5G의 광범위한 커버리지, 주요 간선 도로망의 정비, 텔레매틱스 도입을 장려하는 연방 안전 정책의 배경에 기인합니다. 대형 트럭 사업자는 전자 검사 보고를 의무화하는 연방 자동차 운송 안전국(FMCSA)의 규제에 직면하는 경우가 많으며, 이는 차량이 예측 대시보드 도입을 더욱 촉진할 수 있습니다. 기술 제휴도 확대되고 있으며, 제너럴 모터스는 OnStar 텔레매틱스를 Microsoft Azure와 연계하여 기업 고객을 위한 분석 서비스 패키지를 제공하고 있습니다.

아시아태평양은 10.11%의 CAGR로 성장하고 있으며, 중국이 2030년까지 신에너지차(NEV) 판매 비중 40%를 목표로 하고 있는 것이 그 원동력입니다. 따라서 배터리 기술의 전망은 지역 우선순위로 자리매김하고 있습니다. 덴소 등 일본 업체들은 차세대 전자제어장치에 엣지 AI 칩을 탑재하고, 한국은 삼성의 반도체 기술을 활용해 하드웨어 분야에서 지역적 우위를 공고히 하고 있습니다. 인도와 싱가포르에서는 정부 주도의 스마트 교통 시범사업이 예측 차량 서브시스템과 도시 분석 통합을 가속화하고 있습니다. 이는 개별 차량을 넘어 도시 수준의 모빌리티 조정을 위한 광범위한 생태계 추진을 반영합니다.

유럽은 복잡한 프라이버시 규제에도 불구하고 꾸준한 진전을 보이고 있습니다. 독일 제조업체는 GDPR을 준수하면서 세계 모델을 훈련하는 크로스벤더 데이터 공유 트러스트를 시범 운영하고 있으며, EU의 국경 간 배출권 거래제도는 차량 전체에 대한 예측 모니터링을 촉진하고 있습니다. 지멘스 모빌리티와 BMW의 공동 디지털 트윈 프로그램은 산업용 IoT 스택이 자동차 분석에 상호 긍정적인 영향을 미치는 실례를 보여주고 있으며, 유럽의 성장은 단일 OEM 사일로를 넘어선 다자간 데이터 협력에 의존하고 있음을 시사하고 있습니다.

Automotive predictive technology market size in 2026 is estimated at USD 56.71 billion, growing from 2025 value of USD 52.01 billion with 2031 projections showing USD 87.21 billion, growing at 9.04% CAGR over 2026-2031.

This rapid expansion stems from the industry's migration from reactive maintenance to embedded intelligence that delivers real-time insights directly inside the vehicle architecture. Edge computing now complements cloud analytics, enabling sub-millisecond decision-making for safety-critical functions. Commercial fleet managers have documented notable drops in unplanned maintenance when predictive tools are integrated with 5G telematics, while insurers that adopt usage-based analytics report lower claim frequencies. Regulatory mandates for safety and emissions continually pull demand upward, and falling sensor costs ease adoption barriers. In parallel, technology suppliers such as NVIDIA, Qualcomm, and Microsoft intensify competition by bringing automotive-grade AI chipsets and scalable cloud platforms into the value chain.

Commercial vehicles equipped with 5G telematics exhibit significantly fewer unscheduled service events because predictive algorithms stream high-resolution sensor data with latency below 20 milliseconds. Network throughput that is significantly greater than 4G lets maintenance systems analyze vibration, temperature, and fluid dynamics continuously. Fleet operators translate these insights into dynamic service schedules, cutting downtime over fixed-interval models. Passenger cars benefit as well, receiving over-the-air predictive software updates that optimize component life while drivers remain unaware of the computing workloads that keep the vehicle in peak condition.

Automakers are embedding neural networks in central vehicle controllers; BMW's iDrive upgrade evaluates several parameters at once to generate personalized health diagnostics, trimming warranty claims. OEM control of anonymized fleet data makes every new model release smarter than the last because algorithms retrain on millions of collective driving hours. This continuum of learning redefines product differentiation; owners gravitate toward brands that can predict faults before they surface, thereby extending component life and boosting residual value.

GDPR classifies telematics data as personally identifiable even when anonymized, forcing consent hurdles that slow deployments. Cyberattacks on connected vehicles rose in 2024, highlighting vulnerabilities in distributed predictive architectures. Automakers spend heavily on encryption, yet consumers still cite privacy worries among top purchase hesitations. Until certification schemes mature, some buyers will avoid always-connected vehicles.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Predictive maintenance held a 48.62% share of the automotive predictive technology market in 2025. Operators documented maintenance savings once vehicles switched from scheduled service to condition-based repairs. Proactive alerts are on track for an 11.12% CAGR because drivers value real-time notifications that prevent roadside failures. Safety and security analytics gain momentum as regulators mandate advanced driver assistance upgrades, while traffic optimization marries predictive data with smart-city infrastructure. In commercial scenarios, driver-behavior monitoring dovetails with insurance programs that offer premium discounts, further accelerating adoption.

These use cases are starting to converge. A single software stack can now feed maintenance algorithms, road-hazard predictions, and driver coaching dashboards simultaneously, pointing to future platform consolidation. Vendors that combine maintenance insights with real-time safety warnings are best positioned to command premium subscriptions and data monetization opportunities.

Passenger cars contributed 60.73% revenue in 2025, yet medium and heavy commercial vehicles carry the highest forward momentum at a 9.86% CAGR. Every hour of downtime costs a heavy-duty truck in lost deliveries, which makes predictive uptime an immediate payback for logistics operators.

Electrification amplifies the stakes: battery prognostics now inform route planning, charge-window optimization, and resale pricing. Light commercial vans add another layer of growth with e-commerce fleets adopting predictive modules that sync servicing around parcel-delivery peaks. Although personal vehicles remain the largest unit base, the commercial segment's operational pressures will shape product roadmaps for the next decade.

The Automotive Predictive Technology Market Report is Segmented by Application (Predictive Maintenance, Proactive Alerts, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Deployment (On-Premise, Cloud-Based), Hardware (ADAS Components, Telematics Control Units, and More), End User (OEM, Aftermarket), Technology, and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America captured a 44.05% share in 2025 on the back of 5G coverage, a major portion of major highway miles, and federal safety policies that reward telematics adoption. Heavy truck operators often face Federal Motor Carrier Safety Administration mandates requiring electronic inspection reporting, further nudging fleets toward predictive dashboards. Technology alliances proliferate; General Motors links its OnStar telematics with Microsoft Azure to push analytics-as-a-service packages to corporate customers.

Asia-Pacific is expanding at a 10.11% CAGR, catalyzed by China's New Energy Vehicle target of 40% EV sales by 2030 . Battery prognosis, therefore, ranks high on local priority lists. Japanese suppliers such as Denso bundle edge-AI chips inside next-generation electronic control units, and South Korea leverages semiconductor muscle from Samsung to cement regional leadership in hardware. Government-funded smart-transport pilots in India and Singapore accelerate urban analytics integration with predictive vehicle subsystems, reflecting a broader ecosystem push beyond individual vehicles toward city-level mobility orchestration.

Europe posts steady gains despite thorny privacy rules. German manufacturers pilot cross-vendor data-sharing trusts that satisfy GDPR while still training global models, and the EU's cross-border emissions-trading schemes encourage fleetwide predictive monitoring. Siemens Mobility's Digital Twin program in collaboration with BMW, shows how industrial IoT stacks cross-fertilize automotive analytics, indicating that European growth will hinge on multiparty data alliances that transcend single OEM silos.