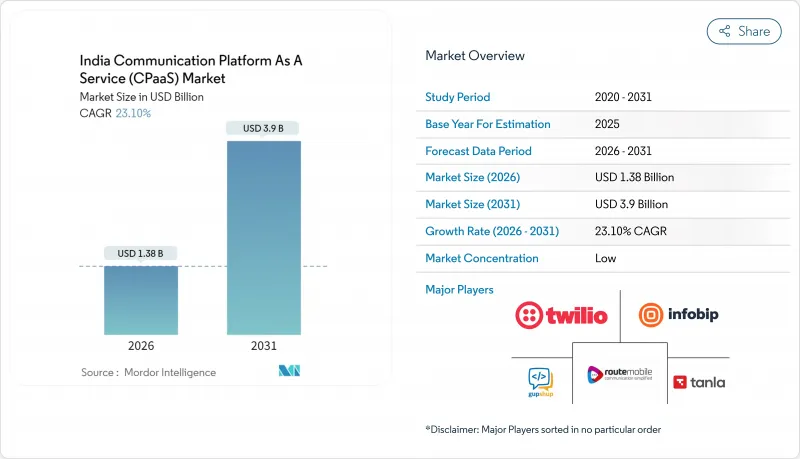

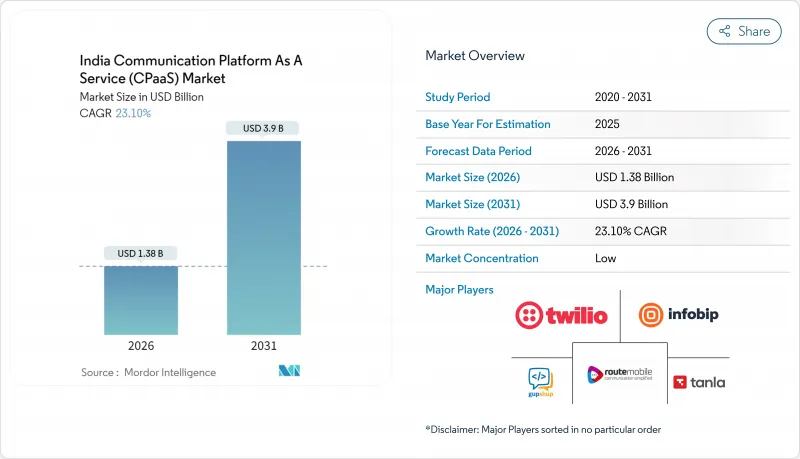

인도의 CPaaS(Communication Platform-as-a-Service) 시장은 2025년 11억 2,000만 달러로 평가되었고, 2026년에는 13억 8,000만 달러, 2026-2031년에 걸쳐 CAGR 23.1%로 성장할 것으로 예상됩니다.

실시간 결제, 소블린 클라우드 의무화, 5G 네트워크와 API의 연계가 함께, 프로그래머블 통신이 경영진 수준의 우선사항이 됨으로써 기업 도입이 급증했습니다. BFSI 부문에 있어서의 인증 및 부정 통지, WhatsApp나 RCS를 활용한 옴니 채널 대응, 로우 코드 개발 툴의 이용 사례가, 가장 강력한 성장 요인이 되고 있습니다. 하이브리드 클라우드 구축, 생성형 AI 기능 및 산업별 컴플라이언스 요구 사항이 경쟁 전략을 재구성합니다. 레거시 스택 전체의 도입 복잡성, 변동되는 A2P SMS 가격, 향상된 데이터 보안 모니터링이 여전히 주요 장벽이 되고 있습니다.

인도 기업은 고정 통신 설비 투자보다 변동적인 운영 비용을 선호하기 때문에 종량 과금 제도가 조달 형태를 재정의합니다. 이익률이 낮은 중소기업은 클라우드 이용을 보조하고 도입을 효율화하는 '디지털 인디아' 시책을 활용하여 몇 주간에 CPaaS를 도입하고 있습니다. 이 모델은 비용 가시성을 향상시키고, 핵심 업무에 대한 자금을 해방하고, 계약 재협상 없이 계절적인 트래픽 급증에 대응합니다. 대기업은 지출과 캠페인 실적을 연관시키는 상세한 분석 기능을 평가하고 있으며 소매업과 물류산업에서 인도의 CPaaS(Communication Platform-as-a-Service) 시장의 채택을 가속화하고 있습니다. 벤더는 투명성이 있는 요금표의 공개나 무료 개발자 크레딧의 번들 제공으로 대응해, 진입 장벽을 한층 더 저감하고 있습니다.

WhatsApp Business API의 4억 8,700만 명의 인도 사용자 기반은 2024년 고객 서비스와 상거래에 필수적인 존재가 되었습니다. 그러나 2025년 7월에 실시된 수수료 개정으로 총소유비용이 상승했기 때문에 브랜드 각사는 거래 흐름을 위한 RCS의 통합을 추진하고 있습니다. RCS는 Android에서 기본적으로 읽은 알림, 인증된 발신자 ID, 리치 카드를 제공하여 독점적인 잠금 기능 없이 OTT 앱과 동등한 기능을 제공합니다. 대기업 EC 기업에 의한 초기 파일럿에서는 SMS 대비 30% 높은 클릭률을 확인했으며, 인도의 CPaaS(Communication Platform-as-a-Service) 시장은 멀티채널 연계로 이행하고 있습니다. CPaaS 플랫폼은 현재 비용 전달율 사용자 선호에 따른 채널 선택을 최적화하는 라우팅 로직을 통합하여 채널 장애 시 지속성을 보장합니다.

대기업에서는 메인프레임 시대의 ERP, 커스텀 CRM, 독자 미들웨어를 병용하는 경우가 많으며, 이들은 현대적인 REST나 gRPC 엔드포인트를 네이티브로 소비할 수 없습니다. 따라서 CPaaS 배포에는 어댑터, 대기열 계층 및 데이터 매핑이 필요하며 프로젝트 예산을 늘릴 수 있습니다. 이해관계자들은 모놀리식 코드 베이스에 내장된 하드코딩된 SMS 게이트웨이와 같은 숨겨진 기술적 부채를 발견할 수 있으며, 이로 인해 타임라인은 원래의 비즈니스 사례의 가정을 넘어 연장됩니다. 데이터 보호법에 따른 컴플라이언스 감사는 모든 데이터 홉의 추적성을 의무화하고 추가 엔지니어링 오버헤드를 추가합니다. 디스커버리 워크숍에서 시스템 오브 레코드의 제약이 밝혀지면, CPaaS가 플러그 앤 플레이라는 인식이 희미해져, 변경 관리가 성공의 중요한 요소가 됩니다.

중소기업은 2031년까지 24.1%의 연평균 복합 성장률(CAGR)로 성장할 전망이지만 대기업은 2025년에 67.12%의 수익 점유율을 유지했습니다. 비용에 부합하는 종량 과금 계약, 번들 템플릿 및 정부 기반 스타트업 인큐베이터가 진입 장벽을 제거하여 중소기업이 통신 설비 투자 없이 엔터프라이즈급 경험을 제공할 수 있도록 합니다. 여행과 소매업 등 계절성 사업은 축제 기간 동안 이용이 급증하고 인도의 CPaaS(Communication Platform-as-a-Service) 시장을 특징으로 하는 탄력적인 과금 모델을 실증하고 있습니다. 병행하여 대기업은 수백 부문에 걸친 옴니채널 플랫폼을 확장하고 AI 구동형 개인화 엔진을 CRM과 통합하여 업셀 전환율을 향상시키고 있습니다. 대규모 트래픽은 볼륨 할인 계약을 가져오고 공급업체 수익의 기반이 되지만 다층적 거버넌스 및 데이터 거주 요구 사항으로 인해 구현은 여전히 복잡합니다.

BFSI(은행, 금융 및 보험)와 의료 부문에 있어서의 컴플라이언스 대책의 강화에 의해 규제 대상 데이터를 주권 영역 경유로 라우팅하면서, 피크 부하 분산에 퍼블릭 클라우드를 활용하는 하이브리드 아키텍쳐에의 이행이 진행되고 있습니다. 콜센터 담당자용 생성형 AI 코파일럿의 파일럿 프로젝트에서는 평균 처리 시간이 2자리수 개선되어 CPaaS 시장 점유율 확대가 시사되고 있습니다. 한편, 중소기업은 로우코드 빌더를 활용해, WhatsApp 스토어 프론트나 자동 청구 봇을 구축, 개발주기를 몇 달에서 몇 주로 단축했습니다. 이 프로그래머블 통신의 민주화로 인도의 CPaaS(Communication Platform-as-a-Service) 시장의 퍼널은 대도시권에서 제2층의 기업이 클러스터로 확대되고 있습니다.

BFSI(은행 및 금융 및 보험) 부문은 2025년 수익의 28.22%를 차지했고 OTP(원타임 패스워드), 전자 위임장 경보, 부정 통지 등에 대한 규제 요건이 초신뢰성 높은 전달을 요구하고 있습니다. 은행은 실시간 고객 커뮤니케이션을 규정하는 인도 준비 은행의 통달에 대응하기 위해 멀티 채널 리던던시(SMS, 푸시 알림, 인앱 알림)를 도입하고 있습니다. AI 강화형 챗봇은 일상적인 문의를 처리하고 복잡한 경우에만 인간 사업자를 할당함으로써 지원 비용 절감과 고객 만족도 향상을 실현하고 있습니다. 데이터 현지화 법률을 충족하는 소블린 클라우드 플랫폼은 필수 요구 사항으로, 공급업체 선택을 좁히는 동시에 서비스 품질에 대한 기대를 높이고 있습니다.

물류 부문은 EC 성장과 국가 물류 시책의 디지털화 목표에 힘입어 24.6%라는 최대 CAGR을 기록했습니다. 실시간 화물 시각화, 드라이버 조정 및 예외 처리는 SMS, RCS 및 음성 채널에서 업데이트 정보를 스트리밍하는 이벤트 중심 API에 의존합니다. 통합 물류 인터페이스 플랫폼의 표준화는 상호 운용성을 촉진하고 API 중심 프레임 워크 수요를 강화하고 있습니다. 창고 운영자는 CPaaS 경보 연동 IoT 센서를 도입하고 자동 보충 메시지를 생성하여 공급망 루프를 강화합니다. 의료 소매 부문은 원격 의료 및 옴니 채널 마케팅의 성숙과 함께 꾸준한 확장을 유지하지만, 성장률은 물류 부문의 하이퍼 수직 통합의 기세에 미치지 못합니다.

The India CPaaS market is expected to grow from USD 1.12 billion in 2025 to USD 1.38 billion in 2026 and is forecast to reach USD 3.9 billion by 2031 at 23.1% CAGR over 2026-2031.

Enterprise adoption surged as real-time payments, sovereign-cloud mandates, and 5G network-API exposure converged to make programmable communication a board-level priority. BFSI use cases for authentication and fraud alerts, omnichannel engagement on WhatsApp and RCS, and low-code development tooling are among the strongest growth catalysts. Hybrid-cloud deployments, generative-AI features, and industry-specific compliance requirements are reshaping competitive strategies. Implementation complexity across legacy stacks, volatile A2P SMS pricing, and heightened data-security scrutiny remain the chief obstacles.

Consumption-based pricing is redefining procurement as Indian organizations prefer variable opex over fixed telecom capex commitments. SMEs with thin margins implement CPaaS in weeks, riding Digital India incentives that subsidize cloud usage and streamline onboarding. The model improves cost visibility, releases cash for core operations, and supports seasonal traffic spikes without renegotiating contracts. Enterprises also value granular analytics that correlate spend with campaign performance, accelerating adoption of the India CPaaS market across retail and logistics sectors. Vendors are responding by publishing transparent rate cards and bundling free developer credits, lowering the entry barrier even further.

WhatsApp Business API's audience of 487 million Indian users made it indispensable for customer service and commerce in 2024. Pricing revisions enacted in July 2025, however, raised the total cost of ownership, nudging brands to integrate RCS for transactional flows. RCS offers read receipts, verified sender IDs, and rich cards natively on Android, delivering parity with over-the-top apps minus proprietary lock-in. Early pilots by large e-commerce firms show 30% higher click-through than SMS, pushing the India CPaaS market toward multi-channel orchestration. CPaaS platforms now embed routing logic that optimizes channel selection by cost, deliverability, and user preference, ensuring continuity if one path fails.

Large enterprises often juggle mainframe-era ERPs, custom CRMs, and proprietary middleware that cannot natively consume modern REST or gRPC endpoints. CPaaS rollouts, therefore, require adapters, queuing layers, and data-mapping that inflate project budgets. Stakeholders may discover hidden technical debt, such as hard-coded SMS gateways embedded in monolithic codebases, extending timelines beyond initial business-case assumptions. Compliance audits under the Data Protection Act mandate traceability of every data hop, adding further engineering overhead. The perception that CPaaS is plug-and-play fades once discovery workshops reveal system-of-record constraints, making change management a critical success factor.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

SMEs added momentum by posting a 24.1% CAGR through 2031 while large enterprises retained 67.12% revenue share in 2025. Cost-aligned pay-per-use contracts, bundled templates, and government start-up incubators remove entry barriers, allowing small firms to offer enterprise-grade experiences without telecom capex. Seasonal businesses in travel and retail spike usage during festival periods, showcasing the elastic billing models that define the India CPaaS market. In parallel, large enterprises scale omnichannel platforms across hundreds of departments, integrating AI-driven personalization engines with CRMs to enhance upsell conversions. Their sizeable traffic yields volume-discounted contracts that anchor vendor revenues, even as implementation remains complex due to multilayer governance and data residency requirements.

Heightened compliance defenses in BFSI and healthcare push many corporates toward hybrid architectures that route regulated data through sovereign zones while leveraging public cloud for peak offload. Pilot projects with generative-AI copilots for call-center agents exhibit double-digit improvements in average handling time, signaling further wallet-share gains for CPaaS. SMEs, meanwhile, tap low-code builders to craft WhatsApp storefronts and automated invoicing bots, shrinking development cycles from months to weeks. This democratization of programmable communications enlarges the India CPaaS market funnel beyond metro hubs into Tier-2 entrepreneurship clusters.

BFSI accounted for 28.22% of 2025 revenue as regulatory mandates for OTP, e-mandate alerts, and fraud notifications demand ultra-reliable delivery. Banks deploy multi-channel redundancy, SMS, push, and in-app to meet Reserve Bank circulars stipulating real-time customer communication. AI-enriched chatbots now triage routine queries, reserving human agents for complex cases, trimming support costs, and bolstering customer satisfaction. Sovereign-cloud platforms that satisfy data-localization statutes are prerequisites, narrowing vendor selection and heightening service-quality expectations.

Logistics recorded the fastest 24.6% CAGR, propelled by e-commerce growth and the National Logistics Policy's digitization targets. Real-time shipment visibility, driver coordination, and exception handling rely on event-driven APIs that stream updates across SMS, RCS, and voice channels. Unified Logistics Interface Platform standards spur interoperability, reinforcing demand for API-centric frameworks. Warehouse operators explore IoT sensors tied to CPaaS alerts, generating automated replenishment messages that tighten supply-chain loops. Healthcare and retail maintain steady expansion as telemedicine and omnichannel marketing mature, yet their growth trails the hyper-vertical momentum seen in logistics.

The India Communication Platform As A Service (CPaaS) Market is Segmented by Organization Size (Small and Medium Enterprises and Large Enterprises), End-User Industry (IT and Telecom, BFSI, and More), Communication Channel (SMS, Voice, and More), Deployment Model (Public Cloud, Hybrid Cloud, and On-Premise), Cpaas Function (Messaging API, Voice API, and More), and Region. The Market Forecasts are Provided in Terms of Value (USD).