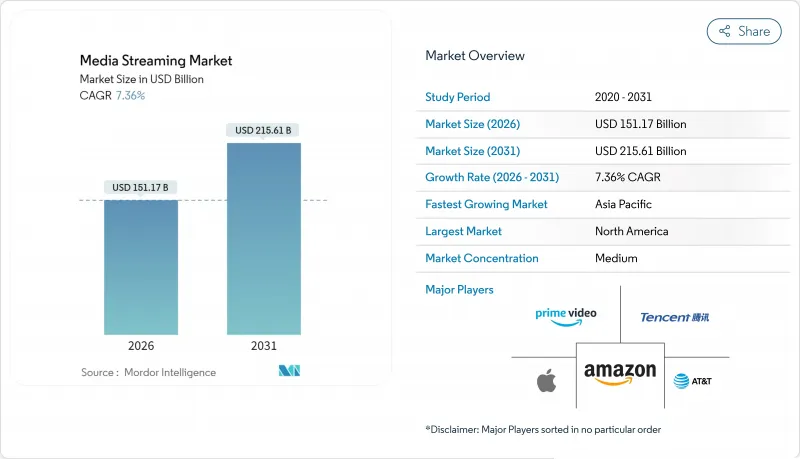

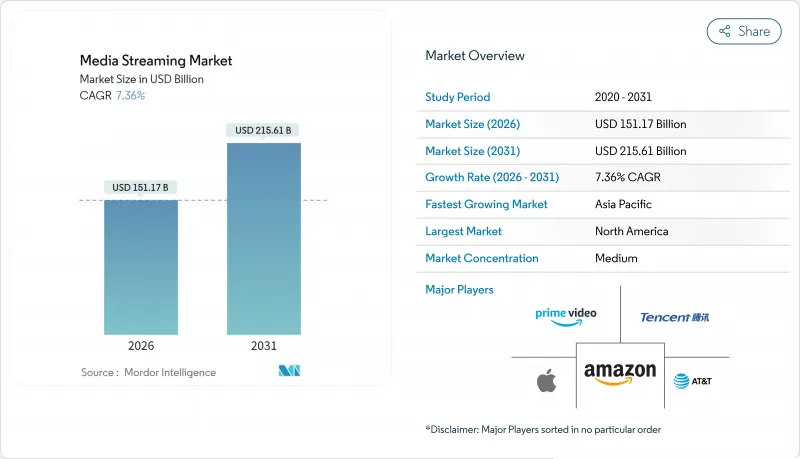

미디어 스트리밍 시장은 2025년 1,408억 달러로 평가되었으며, 2026년 1,511억 7,000만 달러에서 2031년까지 2,156억 1,000만 달러에 이를 것으로 예상됩니다. 예측 기간(2026-2031년)의 CAGR은 7.36%를 나타낼 것으로 전망됩니다.

이 견조한 전망은 구독 전용 제안에서 유료 플랜과 인벤토리를 결합한 하이브리드 수익 창출 모델로의 결정적인 전환에 도움이 됩니다. 이를 통해 플랫폼은 증가하는 고객 획득 비용을 상쇄하고 수익성을 향상시킬 수 있습니다. 경쟁 차별화는 광고 기술 스택 제어, 실시간 추천 엔진, 프리미엄 가격 설정을 가능하게 하는 독점적 컨텐츠 권리를 확보함으로써 점점 더 많이 만들어지고 있습니다. 네트워크 업그레이드, 특히 5G 배포는 높은 비트 전송률을 지원하고, 엣지 컴퓨팅의 도입은 지연을 줄이고, 4K 및 8K 스트림이 버퍼링 없이 모바일 사용자에게 도달할 수 있게 합니다. 스포츠 방영권의 분산으로 이벤트 주도의 가입자 급증과 CPM(노출 단가)의 상승이 촉진되는 한편, 지역 특화형 컨텐츠 라이브러리는 보급률이 낮은 지방 시장에서 신규 시청자를 획득합니다. 동시에 연간 180억 달러에 이르는 컨텐츠 예산에 따른 이익률 압박으로 인해 사업자는 오리지널 제작과 카탈로그 공유 계약의 균형을 잡고 있으며, 업계 전체에서 사용자 단가 최적화로의 전환이 가속화되고 있습니다.

합리적인 가격의 5G 네트워크 배포는 모바일 연결에서 중단 없는 HD 및 4K 스트리밍을 가능하게 하고 소비 패턴을 변화시켰습니다. 사업자는 데이터 패키지를 지원합니다. 왜냐하면 증가한 동영상 트래픽이 프리미엄 네트워크 투자의 수익화로 이어지기 때문에 인프라 정비와 컨텐츠 참여를 모두 촉진하는 선순환이 발생하기 때문입니다. 시청자에 가까운 위치에 위치한 에지 노드는 지연을 더욱 줄여 개인화된 추천을 실시간으로 업데이트할 수 있습니다. 그 결과 가격에 민감한 신흥 경제국의 미디어 스트리밍 시장은 지속적인 성장을 이루고 있습니다.

주요 대도시 지역의 포화 상태에 따라 주요 서비스는 광섬유 배포와 지방 광대역 개선으로 인해 배달 비용이 낮아진 지방 도시를 새로운 목표로 삼고 있습니다. 지역제작의 예산은 세계적 히트작에 비해 겸손하면서 문화에 맞는 시리즈는 서비스가 미치지 못하는 시청자층의 충성도 향상에 공헌하고 있습니다. 지역 방언과 시청 시간대를 고려한 고급 추천 알고리즘은 컨텐츠 지출을 늘리지 않고 참여를 유지하고 미디어 스트리밍 시장에 증분 수익을 제공합니다.

Netflix가 2025년에 180억 달러를 지출한 사실은 규모의 리더 기업조차도 수익성을 압박하는 인플레이션 나선형을 돋보이게 합니다. 프리미엄 컨텐츠 라이브러리를 둘러싼 치열한 입찰 경쟁은 경쟁 서비스가 비용의 일부만 가입자에게 전가할 수 있기 때문에 차별화를 손상시킵니다. 공유 계약은 당분간의 자금 유출을 억제하지만, 가입자 획득의 기반이 되는 독점적 우위성을 둔화시켜 미디어 스트리밍 시장 전체의 경제성에 과제를 가져오고 있습니다.

2025년에도 동영상 컨텐츠는 수익의 77.35%를 차지하는 압도적인 점유율을 유지했습니다. 이는 정착한 시청 습관과 사용자 정착을 지원하는 독점 시리즈에 대한 많은 투자를 반영합니다. 한편, 음악 서비스는 8.82%의 연평균 복합 성장률(CAGR)로 계속 확대되고 있으며, 제한된 네트워크 환경에서도 안정적이고 스트리밍 가능한 컴팩트한 파일 크기가 기여하고 있습니다. AI 구동형 재생목록이 매일 청취 빈도를 높이고 광고 인벤토리를 확대함으로써 오디오 분야의 미디어 스트리밍 시장 규모는 계속 확대되고 있습니다.

제작 비용이 낮고 국경을 초월한 소구력으로 음악 플랫폼은 세계 시청자를 신속하게 수익화할 수 있는 반면 동영상 플랫폼은 장편 컨텐츠의 예산 증가를 부담하고 있습니다. 이 비용 격차는 교차 형식 번들링을 촉진하고 시장 점유율을 보호하기 위해 음성 및 동영상 제안이 단일 앱 내에서 융합되는 미래를 시사합니다.

온디맨드 라이브러리는 2025년 수익의 86.76%를 차지했지만 라이브 스트리밍의 9.44%라는 CAGR은 실시간 경험에 대한 수요 증가를 보여주고 있습니다. 스포츠 중계나 대형 리얼리티 프로그램은 광고주가 중시하는 「예약 시청」을 낳아, 온 디맨드 평균을 웃도는 스트림 단가를 실현하고 있습니다.

기술적 복잡성은 경쟁 우위를 강화합니다. 엣지 컴퓨팅과 커스텀 프로토콜이 트래픽 급증을 관리하고 2초의 심리적 임계값 아래로 떨어지는 지연을 보장합니다. 이러한 기능을 습득한 플랫폼은 세계 대형 이벤트 개최 시 미디어 스트리밍 시장 점유율 확대를 포착하는 태세를 갖추고 있습니다.

북미는 2025년 수익의 34.48%를 차지하는 성숙기에 들어가 사업자는 사용자 획득에서 평생가치 향상으로 전략전환을 진행했습니다. Verizon의 융합 전략에서 알 수 있듯이 광선 및 모바일 계약과의 번들로 인해 대규모 마케팅 비용을 들이지 않고 가구의 둘러싸기와 ARPU 확대를 실현. 스포츠 방영권 경쟁에서 프로그램 제작비는 상승하는 한편, 확립된 광고 시장이 하이브리드층의 수익성을 지원하고 있습니다.

아시아태평양은 정부에 의한 로컬 컨텐츠 제작의 장려와 5G 보급의 가속에 힘입어 8.97%의 연평균 복합 성장률(CAGR)로 확대가 전망됩니다. Netflix는 문화를 배려한 오리지널 작품 공개 후 지역 시청률이 20% 급증하고 로컬 이야기가 압도적인 참여를 낳는 것을 실증했습니다. 정부는 크리에이터 지원 기금(인도의 10억 달러 규모의 대처가 상징적)을 제공하여 신규 컨텐츠 공급과 미디어 스트리밍 시장의 활성화를 촉진하고 있습니다. 그러나 다양한 데이터 현지화 규제에 의해 병행 인프라 구축이 의무화되어 중소 브랜드의 진입 장벽이 높아지고 있습니다. 유럽에서는 GDPR(EU 개인정보보호규정) 대응과 언어 시장의 세분화가 운영 비용을 밀어 올리고 성장에 편차가 보입니다. Netflix와 TF1의 제휴와 같은 배포 계약은 규제 당국과 시청자 모두를 수용하기 위해 스트리밍 사업자와 기존 방송국이 협력하는 하이브리드 모델을 보여줍니다. 라틴아메리카에서는 브라질 77.2%, 칠레 70.9%라는 광섬유 보급률이 고해상도 스트리밍의 보급으로 이어지기 시작하여 새로운 수익 기회를 창출하고 있습니다. 아프리카는 여전히 모바일 우선이며 잠재적인 수요를 유발하기 위해서는 낮은 대역폭 최적화와 다운로드 가능한 컨텐츠 옵션이 필수적입니다.

The media streaming market was valued at USD 140.80 billion in 2025 and estimated to grow from USD 151.17 billion in 2026 to reach USD 215.61 billion by 2031, at a CAGR of 7.36% during the forecast period (2026-2031).

This strong outlook rests on a decisive pivot from subscription-only propositions toward hybrid monetization that combines paid tiers with advertising inventory, enabling platforms to offset rising customer-acquisition costs and improve profitability. Competitive differentiation increasingly stems from control of advertising technology stacks, real-time recommendation engines, and exclusive content rights that secure premium pricing. Network upgrades-in particular 5G rollouts-support higher-bitrate delivery, while edge compute adoption cuts latency, allowing 4K and 8K streams to reach mobile users without buffering. Sports rights fragmentation drives event-led subscriber spikes and higher CPMs, whereas localized content libraries draw new viewers in under-penetrated rural markets. At the same time, margin pressure from USD 18 billion annual content budgets forces operators to balance original production with catalog sharing pacts, accelerating a sector-wide shift toward revenue-per-user optimization.

Deployment of affordable 5G networks has reshaped consumption patterns by supporting uninterrupted HD and 4K streams on mobile connections. Operators subsidize data packages because elevated video traffic monetizes premium network investments, creating a feedback loop that spurs both infrastructure build-out and content engagement. Edge nodes positioned close to viewers further trim latency, enabling personalized recommendations to refresh in real time. The result is sustained growth for the media streaming market in price-sensitive emerging economies.

Having saturated major metropolitan areas, leading services are targeting secondary cities where fiber rollout and improved rural broadband have lowered delivery cost. Localized production budgets are modest relative to global tent-pole titles, yet culturally tailored series drive higher loyalty among underserved audiences. Sophisticated recommendation algorithms that account for regional dialects and viewing times maintain engagement without raising content outlays, adding incremental revenue to the media streaming market.

Netflix's USD 18 billion outlay in 2025 underscores an inflationary spiral that squeezes profitability even for scale leaders. Fierce bidding for premium libraries diminishes differentiation because rival services can only pass a portion of costs to subscribers. Sharing agreements reduce immediate cash burn but blunt exclusivity advantages that underpin subscriber acquisition, challenging overall economics of the media streaming market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Video maintained a commanding 77.35% revenue slice in 2025, reflecting entrenched viewing habits and heavy investment in exclusive series that anchor user retention. Music services, however, are expanding at an 8.82% CAGR aided by compact file sizes that stream reliably on constrained networks. The media streaming market size for audio is swelling as AI-driven playlists raise daily listening frequency and enlarge ad inventory.

Lower production costs and borderless appeal allow music platforms to monetize global audiences rapidly, while video players shoulder rising budgets for long-form content. This cost asymmetry encourages cross-format bundling, signalling a future where audio and video propositions converge within a single app to protect market share.

On-demand libraries accounted for 86.76% of 2025 revenue, yet live streaming's 9.44% CAGR illustrates growing appetite for real-time experiences. Sporting fixtures and tent-pole reality shows create appointment viewing that advertisers value, lifting revenue per stream above on-demand averages.

Technical complexity strengthens competitive moats: edge compute and custom protocols manage traffic spikes, ensuring latency below the two-second psychological threshold. Platforms mastering these capabilities are positioned to capture incremental media streaming market share during peak global events.

The Media Streaming Market Report is Segmented by Content Type (Video Streaming, Music Streaming), Service Type (Live Streaming, On-Demand Streaming), Revenue Model (Subscription, Advertising), Streaming Quality (SD, HD, 4K/UHD, 8K), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America generated 34.48% of 2025 revenue but is maturing, prompting operators to pivot from user acquisition toward higher lifetime value. Bundling with fiber and mobile contracts, as demonstrated by Verizon's convergence strategy, locks in households and widens ARPU without heavy marketing spend. Sports-rights competition inflates programming costs, yet the presence of established ad markets sustains hybrid-tier profitability.

Asia-Pacific is projected to expand at a 8.97% CAGR, buoyed by governmental encouragement of local content creation and accelerating 5G coverage. Netflix recorded a 20% regional viewing surge after debuting culturally tailored originals, confirming that local narratives unlock outsized engagement. Governments are offering creator funds-India's USD 1 billion initiative is emblematic-that feed fresh catalogs and stimulate the media streaming market. Nonetheless, diverse data-localization rules compel parallel infrastructure builds, raising entry barriers for smaller brands. Europe shows uneven growth as GDPR compliance and fragmented language markets inflate operational overheads. Carriage agreements such as Netflix's tie-up with TF1 illustrate a hybrid model where streaming and traditional broadcasters collaborate to satisfy regulators and audiences. Latin America's fiber penetration-77.2% in Brazil and 70.9% in Chile-has started translating into higher-resolution streaming uptake, creating fresh addressable revenue. Africa remains mobile-first; low-bandwidth optimizations and downloadable content options are crucial to unlock latent demand.