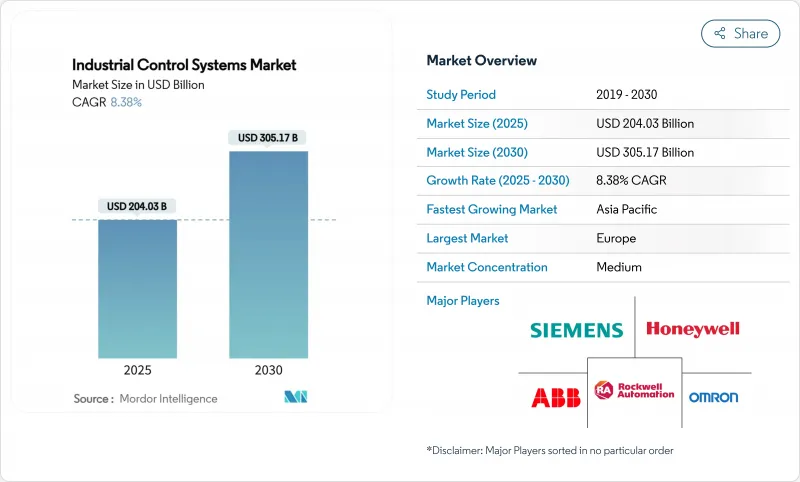

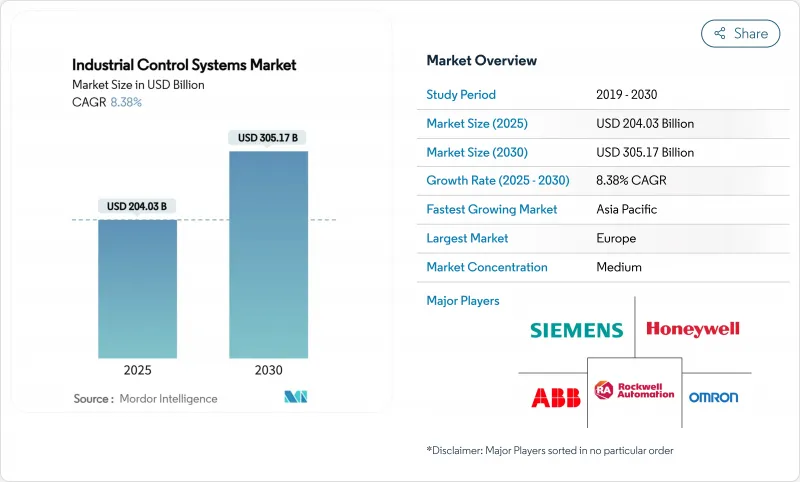

세계의 산업용 제어 시스템 시장 규모는 2025년 2,040억 3,000만 달러에 이르고, 2030년에는 3,051억 7,000만 달러에 이를 것으로 예측되며, CAGR은 8.38%로 추이할 것으로 보입니다.

Industry 4.0 하에서 가속화되는 디지털화, 사이버 보안 의무화, 개방적이고 공급업체 중립 아키텍처의 매력이 높아짐에 따라 자동화는 효율성을 위한 추가 기능이 아니라 운영의 핵심으로 강화되었습니다. 2024년 반도체 불황으로 공급망 리스크가 높아짐에 따라 전용 하드웨어에서 기능을 분리하는 소프트웨어 정의 제어 플랫폼의 가치가 부각되고, 한편 유럽과 북미에서는 정부의 우대 조치로 개수 프로젝트의 자본 풀이 확대되었습니다. 클라우드, 에지, On-Premise가 공존하게 된 이유는 제조업체가 낮은 대기 시간의 프로세스 제어를 포기하지 않고 규모의 큰 분석을 요구하게 되었기 때문입니다. 특히 전자공학과 생명과학 등의 고정밀 분야에서는 상호 운용 가능한 하드웨어에 AI 대응 소프트웨어와 통합 보안을 결합한 벤더가 경쟁적으로 유리하게 되고 있습니다.

제조업체는 자동화를 격리된 라인에서 운영, 엔지니어링 및 비즈니스 데이터를 통합하는 기업 규모의 네트워크로 확장합니다. Siemens SINUMERIK ONE과 같은 AI 지원 에지 노드는 현재 기계 플로어에서 직접 예측 유지 보수 및 적응 피드 속도 제어를 수행하여 의사 결정 대기 시간을 단축하고 있습니다. 보다 광범위한 연결성은 복합적인 가치를 창출하고 거시적인 역풍에도 불구하고 2025년에 OT 예산의 평균이 30% 증가한 이유를 설명하고 있습니다. 그 결과 상호 운용 가능한 제품이 독자적인 포인트 제품을 능가하고 시장 경쟁 역학을 재구성하고 있습니다.

산업계 규제는 안전성의 무결성(IEC 61508/61511)과 사이버 보안의 탄력성(IEC 62443)이라는 이중 의무에 집약되고 있습니다. Siemens의 SIBERprotect와 같은 도구는 안전 루프를 온전히 유지하면서 위험한 자산을 밀리초 단위로 격리하므로 인증된 안전 PLC와 안전한 통신 프로토콜이 필수적입니다. CISA는 2024년 OT 취약성에 대한 24가지 권고를 발표했으며, 구매자는 현재 사이버 안전 자격을 자본 계획에 통합하고 있으며 산업용 제어 시스템 시장은 기본적으로 통합된 기능을 제공하는 공급업체로 안내되고 있습니다.

Deloitte는 2033년까지 미국 제조업에서 190만명이 미취직이 될 수 있으며, 그 중 상당수가 IT와 OT의 하이브리드 기술을 필요로할 것으로 예측했습니다. 따라서 벤더는 매니지드 서비스와 로우 코드 설정을 번들로 도입 시 마찰을 완화하려고 합니다.

SCADA 플랫폼은 2024년 산업용 제어 시스템 시장의 28.7%를 차지했으며, 중앙 집중식 접근법은 에지 대응 PLC와 경쟁하고 있으며, 2030년까지의 CAGR은 11.46%로 예상됩니다. 마이크로 AI 칩의 유입은 PLC가 상태 모니터링 및 품질 검사 워크로드를 로컬로 처리할 수 있게 하여 데이터 백홀과 네트워크 혼잡을 완화합니다. 석유 및 가스 및 화학 산업에서 분산 제어 시스템은 여전히 연속 공정을 관리하고 있지만, 고객은 자산의 수명을 연장하기 위해 기존 DCS에 예측 알고리즘을 중첩하려고 합니다. 휴먼 머신 인터페이스는 현장 문제 해결을 위해 AR 오버레이를 통합한 의사결정 지원 콘솔로 진화하고 있습니다. 지능형 전자 장치는 그리드 운영자가 보다 신속한 고장 분리를 추구하는 중 유틸리티 기업에서 지지를 모으고 있습니다. 이러한 이용 사례에서 개방형 API를 통합한 공급업체는 산업용 제어 시스템 시장에서 높은 평가를 받으며 플랜트 관리자는 공급업체에 묶이지 않고 최상의 블리드 구성 요소를 결합할 수 있습니다.

SCADA가 2025년 산업용 제어 시스템 시장 규모에 여전히 585억 달러를 기여했기 때문에 업그레이드 사이클의 핵심은 애널리틱스를 주입하면서 모니터링 레이어를 그대로 유지하는 컨테이너 기반 마이크로서비스입니다. 반면에 이산 제조업의 파일럿 프로그램에서 Edge PLC 클러스터는 예기치 않은 다운타임을 최대 20% 줄이고 투자 회수를 가속화하고 있습니다. 중앙 집중식 아키텍처와 분산 아키텍처 모두에서 라이프사이클 서비스를 조화시킬 수 있는 공급업체는 불균형한 점유율을 획득할 것으로 예측됩니다.

자산 성능 관리는 플랜트가 설비 전체의 유효성과 스케줄 불필요한 유지보수를 추구하는 가운데 2024년 매출의 23.6%를 창출했습니다. 향후 사이버 보안 제품군은 OT 자산을 목표로 하는 랜섬웨어 증가에 대한 반동으로 인해 CAGR 12.75%로 다른 모든 카테고리를 상회할 것으로 전망됩니다. 취약성 스캔, 제로 트러스트 세분화, 안전 PLC의 하드닝을 융합시킨 통합형 제품은 제약회사 등의 위험을 싫어하는 부문에 지지되고 있습니다. 생산 실행 시스템은 현재 품질 분석 및 전자 배치 기록을 번들로 제공하고 있으며 제품 수명주기 관리 도구는 디지털 트윈과 연계하여 설계 및 제조를 다루고 있습니다. ERP 공급업체는 REST API를 통해 OT 데이터 모델을 공개하고 수요 중심의 계획 알고리즘에 공급합니다. 따라서 산업용 제어 시스템 시장은 별도의 모듈이 아닌 교차 도메인 데이터를 오케스트레이션하는 플랫폼에 기울어지고 있습니다.

2030년까지 산업용 제어 시스템 시장 규모가 140억 달러 이상에 달할 것으로 예상되는 산업용 사이버 플랫폼은 벤처 자금을 모아 기존 벤더에게 틈새 전문가의 인수를 촉구하고 있습니다. APM, MES, 사이버 레이어를 동기화하는 데 뛰어난 공급업체는 디지털 변환의 로드맵을 한 번에 일관되게 실현하는 파트너로서 자리잡고 있습니다.

유럽은 2024년 매출의 28.5%를 차지했으며, 엄격한 기능 안전 규제와 지속가능성 의무화로 고효율 자동화가 평가되고 있습니다. Manufacturing-X와 같은 자금 조달 체계는 데이터 주권을 중시하는 프로젝트에 1억 5,000만 유로(1억 6,100만 달러)를 분배해 국내 벤더에게 조기 진입의 우위를 부여하고 있습니다. 자본 프로젝트는 EU의 녹색 거래 보고서에 따라 탄소발자국 대시 보드를 번들로 늘어나고 있습니다. 동유럽의 클러스터는 서양 OEM의 니어 쇼어 용량으로 기능하여 중위 제어 기기에 대한 수요 증가를 자극하고 있습니다.

아시아태평양은 CAGR 10.24%로 성장해 전자, EV용 배터리, 재생 가능 부품의 대규모 생산 능력 확대로부터 혜택을 받습니다. 중국의 인구동태 역풍과 임금 인플레이션이 공장 자동화를 가속화하고 동남아시아 국가는 세제 우대 조치를 활용하여 리쇼어링 프로젝트를 유치합니다. 국내 PLC와 로봇 공급업체가 점유율을 늘리고 있지만, 하이엔드 안전성과 모션 솔루션은 다국적의 기존 기업이 우위를 유지하고 있습니다. 중국의 중요 정보 인프라 법을 필두로 하는 정부의 사이버 규제는 구매자를 검증 가능한 보안 계통의 제품으로 향하게 하여 조달 후보 리스트를 형성하고 있습니다.

북미는 리쇼어링 이니셔티브와 CHIPS법의 2억 달러의 디지털 트윈 프로그램을 통해 기세를 유지합니다. 미국 멕시코 걸프의 에너지 전환에 대한 지출은 LNG, 수소 및 CCS 시설을 개조하기 위한 개방형 공정 자동화에 대한 수요를 창출하고 있습니다. 캐나다 NGen의 3,500만 달러의 지속 가능한 제조 과제는 모듈형 제어 키트의 중소기업 채택을 추진하고 있습니다. CISA에 의한 사이버 지침의 강화는 조달 사양을 향상시키고 IEC 62443 인증을 가진 공급업체가 유리합니다. 이러한 동향을 종합하면 산업용 제어 시스템 시장은 지역적으로 다양한 성장을 계속하고 있습니다.

The industrial control systems market size stood at USD 204.03 billion in 2025 and is projected to reach USD 305.17 billion by 2030, advancing at an 8.38% CAGR.

Accelerated digitalization under Industry 4.0, mounting cybersecurity obligations, and the growing appeal of open, vendor-neutral architectures are reinforcing automation as an operational cornerstone rather than an efficiency add-on. Heightened supply-chain risk during the 2024 semiconductor squeeze underscored the value of software-defined control platforms that detach functionality from dedicated hardware, while government incentives in Europe and North America widened the capital pool for retrofit projects. Cloud, edge, and on-premise deployments now coexist as manufacturers seek analytics at scale without surrendering low-latency process control. Competitive positioning increasingly favors vendors that combine interoperable hardware with AI-enabled software and integrated security, especially in high-precision sectors such as electronics and life sciences.

Manufacturers are extending automation from isolated lines to enterprise-wide networks that merge operational, engineering, and business data. AI-ready edge nodes such as Siemens SINUMERIK ONE now execute predictive maintenance and adaptive feed-rate control directly on the machine floor, shrinking decision latency. Broader connectivity generates compound value, which explains why average OT budgets grew 30% in 2025 despite macro headwinds. As a result, interoperable offerings are edging out proprietary point products, reshaping competitive dynamics across the industrial control systems market.

Industrial regulations are converging around dual mandates of safety integrity (IEC 61508/61511) and cybersecurity resilience (IEC 62443). Tools such as Siemens SIBERprotect isolate compromised assets within milliseconds while keeping safety loops intact, making certified safety PLCs and secure communication protocols indispensable. With CISA releasing 24 advisories on OT vulnerabilities in 2024, buyers now factor cyber-safety credentials into capital planning, nudging the industrial control systems market toward vendors that offer natively integrated capabilities.

Deloitte estimates 1.9 million US manufacturing roles may go unfilled by 2033, many requiring hybrid IT-OT skills. Scarcity inflates labor costs and prolongs commissioning cycles, prompting vendors to bundle managed services and low-code configuration to soften onboarding friction.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

SCADA platforms retained a 28.7% slice of the industrial control systems market in 2024, yet their centralized approach is being contested by edge-enabled PLCs that are posting 11.46% CAGR through 2030. The influx of micro-AI chips allows PLCs to process condition-monitoring and quality-inspection workloads locally, reducing data backhaul and network congestion. In oil & gas and chemicals, Distributed Control Systems still govern continuous processes, but customers are layering predictive algorithms over legacy DCS to extend asset life. Human-Machine Interfaces have evolved into decision-support consoles incorporating AR overlays for on-the-spot troubleshooting. Intelligent Electronic Devices are gaining traction in utilities as grid operators pursue faster fault isolation. Across these use cases, the industrial control systems market rewards suppliers that embed open APIs, enabling plant managers to mix best-of-breed components without vendor lock-in.

With SCADA still contributing USD 58.5 billion to industrial control systems market size in 2025, upgrade cycles center on container-based micro-services that keep supervisory layers intact while injecting analytics. Meanwhile, pilot programs in discrete manufacturing show edge PLC clusters trimming unplanned downtime by up to 20%, accelerating payback. Vendors able to harmonize lifecycle services for both centralized and distributed architectures are expected to capture disproportionate share.

Asset Performance Management generated 23.6% of 2024 revenue as plants chase overall equipment effectiveness and schedule-free maintenance. Looking ahead, cybersecurity suites are set to outpace all other categories at 12.75% CAGR, a reaction to increased ransomware targeting OT assets. Integrated offerings that fuse vulnerability scanning, zero-trust segmentation, and safety-PLC hardening resonate with risk-averse sectors such as pharmaceuticals. Manufacturing Execution Systems now bundle quality analytics and electronic batch records, while Product Lifecycle Management tools couple with digital twins to bridge design and production. ERP vendors are exposing OT data models via REST APIs, feeding demand-driven planning algorithms. The industrial control systems market is therefore tilting toward platforms that orchestrate cross-domain data rather than discrete modules.

Industrial cyber platforms, forecast to exceed USD 14 billion in industrial control systems market size by 2030, are attracting venture funding and prompting established vendors to buy niche specialists. Suppliers competent in synchronizing APM, MES, and cyber layers position themselves as single-throat-to-choke partners for digital transformation roadmaps.

The Global Industrial Control Systems Market Report is Segmented by Operational Technology (SCADA, DCS, PLC, and More), Software (APM, PLM, MES, ERP, and More), Deployment Mode (On-Premise, Cloud-Based, Edge/Hybrid), End-User Industry (Oil and Gas, Chemical and Petrochemical, Power and Utilities, Food and Beverages, Automotive and Transportation, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe steers 28.5% of 2024 revenue, driven by rigorous functional-safety statutes and sustainability mandates that reward high-efficiency automation. Funding schemes such as Manufacturing-X distribute EUR 150 million (USD 161 million) to projects that emphasize data sovereignty, giving domestic vendors an early-mover edge. Capital projects increasingly bundle carbon-footprint dashboards, aligning with the EU's Green Deal reporting. Eastern European clusters act as near-shore capacity for Western OEMs, stimulating incremental demand for mid-tier control gear.

Asia-Pacific, advancing at 10.24% CAGR, benefits from large-scale capacity expansions in electronics, EV batteries, and renewable components. China's demographic headwinds and wage inflation accelerate factory automation, while Southeast Asian nations leverage tax incentives to lure reshoring projects. Domestic PLC and robot suppliers are gaining share, but multinational incumbents retain dominance in high-end safety and motion solutions. Government cyber rules, notably China's Critical Information Infrastructure law, push buyers toward products with verifiable security lineage, shaping procurement shortlists.

North America sustains momentum through reshoring initiatives and the CHIPS Act's USD 200 million digital-twin program. Energy transition spending in the US Gulf Coast is spawning demand for open-process automation to retrofit LNG, hydrogen, and CCS facilities. Canada's NGen USD 35 million sustainable manufacturing challenge propels SME adoption of modular control kits. Heightened cyber directives from CISA elevate procurement specifications, giving advantage to suppliers with IEC 62443 certifications. Collectively, these trends keep the industrial control systems market on a diversified regional growth footing.