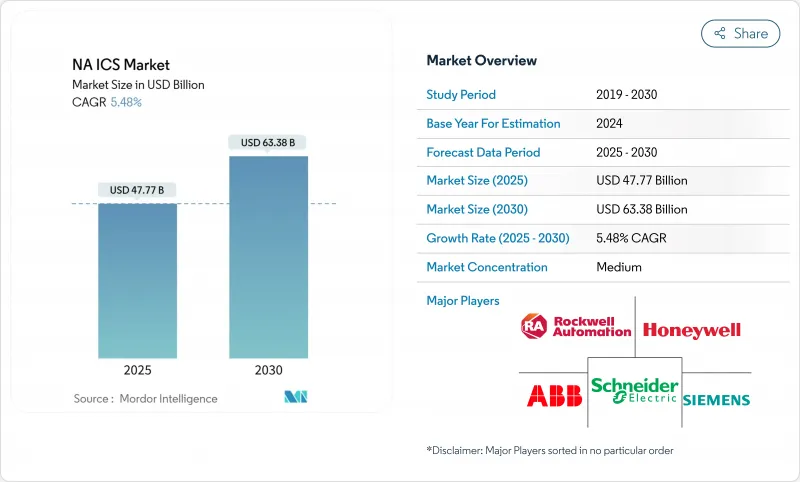

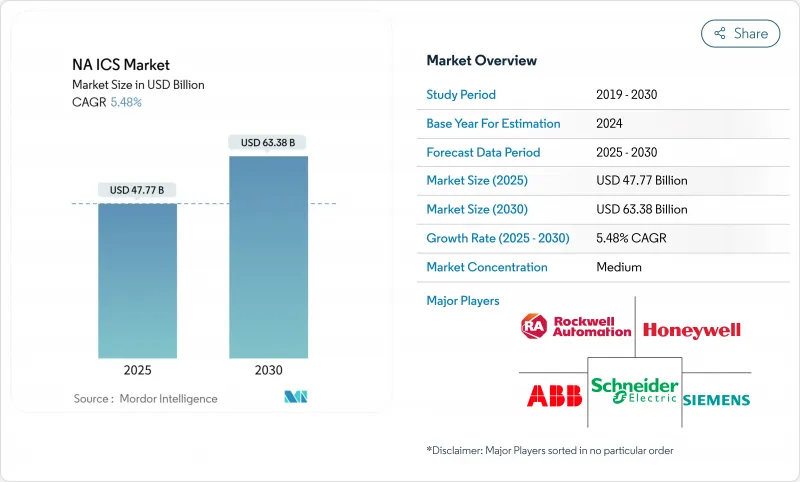

북미의 산업용 제어 시스템 시장 규모는 2025년에 477억 7,000만 달러, 2030년에는 CAGR 5.48%를 나타내 633억 8,000만 달러에 달할 것으로 예상됩니다.

하드웨어는 PLC, 분산 제어 하드웨어, I/O 모듈에 대한 꾸준한 투자에 힘입어 2024년에는 57.2%로 최대 판매 점유율을 유지했습니다. 미국 CHIPS법은 4,500억 달러의 반도체 능력 투자를 발표하고 부품 부족을 완화하고 새로운 자동화 전개에 박차를 가하고 있습니다. 산업용 이더넷은 2024년에 설치된 통신의 48.9%를 차지했지만, 공장이 유연한 접속성을 요구하는 가운데, 무선 프로토콜은 CAGR 10.4%를 나타낼 전망입니다. 클라우드 배포는 CAGR 9.31%로 확대되지만 대기 시간에 민감한 제어 루프와 엄격한 보안 정책으로 인해 설치의 81%는 사내 구축 상태로 유지됩니다. 자동차 제조업체는 수요의 18.6%를 차지하고 있지만 품질 설계 의무화가 진행되는 가운데 CAGR 9.1%로 가장 빠르게 성장하는 최종 사용자는 의약품입니다.

자동차 제조업체는 유연성과 가동률을 높이기 위해 단편화된 제어 레이어를 통합 아키텍처로 대체하고 있습니다. 아우디의 미국 바디샵은 프라이빗 클라우드에 연결된 Siemens Simatic S7-1500V 가상 컨트롤러를 채택하여 IT와 OT 워크플로우를 통합하여 전환 시간을 단축했습니다. 국내 공장 중 기능을 완전히 자동화하고 있는 것은 31%에 불과하며 근대화의 여지가 큰 것이 부각되고 있습니다. Kimberly-Clark의 점진적인 PLC에서 DCS로의 전환은 사이버 보안을 지원하는 플랫폼을 통합하면서 10년에 걸쳐 매년 1라인씩 다운타임을 제한하는 신중한 속도를 보여줍니다.

OT 시설의 93%가 지난 12개월 동안 침입을 보고했으며, 영역, 도관 및 지속적인 모니터링을 정의하는 ISA/IEC 62443 프레임워크의 급속한 보급을 촉진하고 있습니다. 2025년 2월 ANSI/ISA-62443-2-1 업데이트에서는 성숙도 모델이 도입되어 자산 소유자가 위험 프로파일에 맞게 제어를 조정할 수 있습니다. 유틸리티 기업과 이산 제조업체 모두 다층 방어를 구축하여 계획외 정지 및 보험료를 삭감하고 있습니다.

1990년대에 건설된 플랜트는 여전히 공급업체별 버스에 의존하며 데이터 수집 및 클라우드 연결을 복잡하게 합니다. 피닉스 컨택트는 셧다운을 최소화하기 위해 점진적인 I/O 마이그레이션을 조언하고 있지만 통합 작업자는 수천 개의 레거시 레지스터를 최신 객체 모델에 매핑해야 합니다. Wood PLC는 프로세스 사이트의 수명주기가 30년이기 때문에 전반적인 교환은 현실적이지 않으며 소유자는 수년 동안 듀얼 스택 아키텍처에 자금을 제공해야 한다고 지적합니다.

하드웨어는 PLC 랙, DCS 노드 및 모터 드라이브의 지속적인 주문에 견인되어 2024년 매출의 57.2%를 차지했습니다. ABB의 프로세스 자동화 부문의 2024년 매출은 68억 달러로 자본 설비에 대한 지속적인 의욕을 보여주었습니다. OPC UA와 MQTT를 통합한 하니웰의 ControlEdge PLC와 같이 에지 분석을 컨트롤러에 통합함으로써 프리미엄 SKU의 매출이 증가하고 있습니다.

라이프사이클 지원 아웃소싱과 함께 서비스 규모는 작고 CAGR 8.9%로 급속히 확대되고 있습니다. 로크웰 오토메이션 수명 주기 서비스 수주 잔여는 2024년 9월에 17억 달러에 달했는데, 이는 가용성 향상과 관련된 비용을 달성하는 성과 기반 계약에 대한 수요를 반영합니다. 2025년까지 350만 명의 사이버 보안 담당자가 부족하다는 기술 부족은 보수 계약과 원격 감시 계약을 밀어 올려 북미 산업용 제어 시스템 업계의 경상 수익을 상승시킵니다.

PLC는 2024년에 북미 산업용 제어 시스템 시장 규모의 31.4%를 차지하여 결정론적 제어와 입증된 신뢰성을 평가했습니다. 로크웰의 Logix 컨트롤러 제품군은 이 지역의 자동차와 식품 라인을 지원합니다. 공급업체는 현재 네이티브 CIP-Security 및 TLS 암호화 기능을 갖춘 PLC를 출하하고 있으며 게이트웨이에 대한 의존도를 줄이고 있습니다.

MES 플랫폼은 로트 레벨 계보와 주문에서 배치로의 동기화를 요구하는 제조업체에 의해 CAGR 7.6%를 나타낼 전망입니다. Industry 4.0의 도입으로 연결된 장치는 2024년에 전 세계 170억 대로 두배로 늘어나 MES가 실용적인 생산 KPI로 변환하는 데이터세트가 생성되었습니다. 자동차 OEM은 MES를 사용하여 로봇 페인팅, 배터리 조립, 최종 검사를 조정하고 출시주기를 단축하며 전사적 자원 계획을 연결합니다.

The North American industrial control systems market size stands at USD 47.77 billion in 2025 and is projected to reach USD 63.38 billion by 2030, reflecting a 5.48% CAGR.

Hardware retains the largest revenue share at 57.2% in 2024, underpinned by steady investment in PLCs, distributed control hardware, and I/O modules. Demand is reinforced by the U.S. CHIPS Act, which has mobilized USD 450 billion of announced semiconductor capacity investments, easing component shortages and spurring new automation roll-outs. Industrial Ethernet accounted for 48.9% of installed communications in 2024, while wireless protocols advanced at a 10.4% CAGR as plants sought flexible connectivity. Although cloud deployments are expanding at 9.31% CAGR, 81% of installations remain on-premise because of latency-sensitive control loops and strict security policies. Automotive producers captured 18.6% of demand, yet pharmaceuticals are the fastest-growing end user at 9.1% CAGR as quality-by-design mandates intensify.

Automotive manufacturers are replacing fragmented control layers with unified architectures to boost flexibility and uptime. Audi's U.S. body shop adopted Siemens Simatic S7-1500V virtual controllers connected to its private cloud, merging IT and OT workflows and shortening change-over times. Only 31% of domestic factories have fully automated a function, highlighting large headroom for modernization. Kimberly-Clark's phased PLC-to-DCS migration illustrates the cautious pace: one line per year over a decade to limit downtime while embedding cybersecurity-ready platforms.

Ninety-three percent of OT facilities reported an intrusion in the past 12 months, prompting rapid uptake of ISA/IEC 62443 frameworks that define zones, conduits, and continuous monitoring. The February 2025 ANSI/ISA-62443-2-1 update introduced a maturity model, allowing asset owners to tailor controls to risk profiles. Utilities and discrete manufacturers alike are structuring multi-layer defenses, reducing unplanned outages and insurance premiums.

Plants built in the 1990s still rely on vendor-specific buses that complicate data acquisition and cloud connectivity. Phoenix Contact advises staged I/O migration to minimise shutdowns, yet integration crews must map thousands of legacy registers to modern object models-an effort that prolongs project timelines and inflates labor costs. Wood PLC notes that process-site lifecycles of 30 years make wholesale replacement impractical, obliging owners to fund dual-stack architectures for years.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Hardware contributed 57.2% of 2024 revenue, led by sustained orders for PLC racks, DCS nodes, and motor drives. ABB's Process Automation unit posted USD 6.8 billion of 2024 sales, showing continued appetite for capital equipment. Integration of edge analytics into controllers, such as Honeywell's ControlEdge PLC with embedded OPC UA and MQTT, is boosting sell-through of premium SKUs.

Services, though smaller, are scaling rapidly at 8.9% CAGR as owners outsource lifecycle support. Rockwell Automation's Lifecycle Services backlog reached USD 1.70 billion in September 2024, reflecting demand for outcome-based contracts that tie fees to availability gains. Skills shortages-3.5 million cybersecurity roles lacking by 2025-push maintenance and remote-monitoring agreements higher, elevating recurring revenue in the North American industrial control systems industry.

PLCs held 31.4% of the North American industrial control systems market size in 2024, valued for deterministic control and proven reliability. Rockwell's Logix controller family anchors automotive and food lines across the region. Vendors now ship PLCs with native CIP-Security and TLS encryption, reducing gateway dependencies.

MES platforms are expanding at 7.6% CAGR as manufacturers seek lot-level genealogy and order-to-batch synchronisation. Industry 4.0 roll-outs nearly doubled connected devices to 17 billion globally in 2024, creating data sets that MES converts into actionable production KPIs. Automotive OEMs use MES to coordinate robotic paint, battery assembly, and final inspection, shortening launch cycles and connecting enterprise resource planning.

The North American Industrial Control Systems Market Report is Segmented by Component (Hardware, Software, Services), Type of System (Supervisory Control & Data Acquisition, Distributed Control Systems, and More), Communication Protocol (Fieldbus, Industrial Ethernet, Wireless), Deployment Mode (On-Premise, Cloud, Hybrid), End-User Industry, and Geography. The Market Forecasts are Provided in Terms of Value (USD).