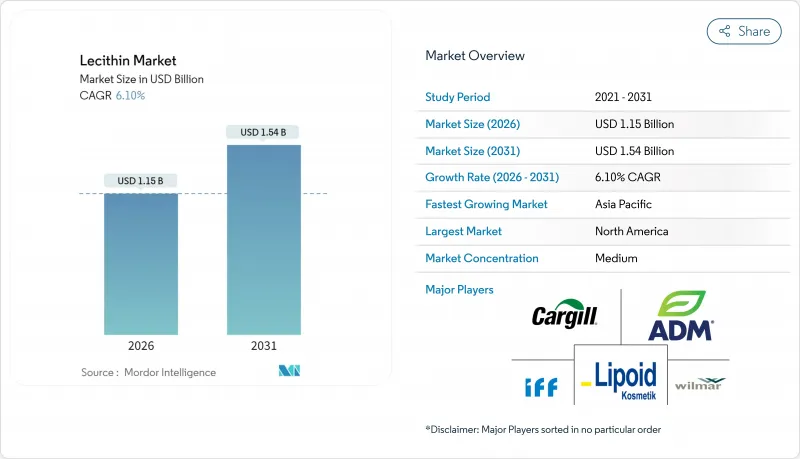

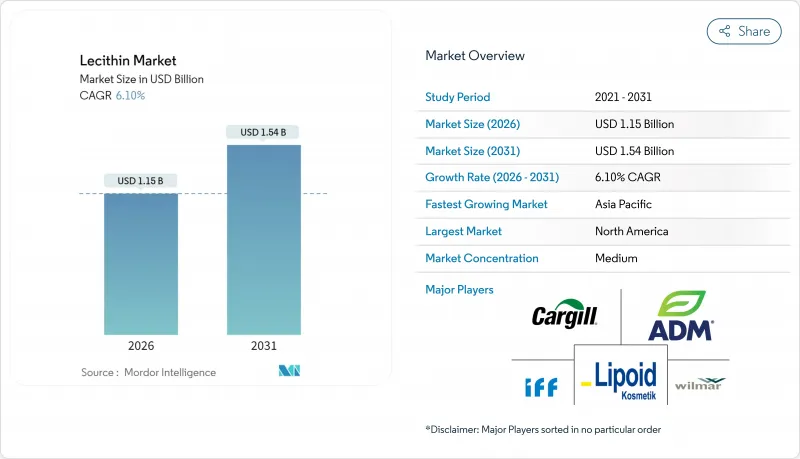

레시틴 시장은 2025년 10억 8,000만 달러로 평가되었고, 2026년에는 11억 5,000만 달러로 성장할 전망이며, 2026-2031년 CAGR 6.1%로 성장을 지속하여, 2031년까지 15억 4,000만 달러에 달할 것으로 예측되고 있습니다.

가공 식품의 천연 유화제 채용 확대, 엄격한 클린 라벨 규제, 의약품 등급 인지질의 침투 심화가 수요의 견조한 상승 경향을 지원하고 있습니다. 병행하여, 제약 기업에 의한 레티신의 의약품 전달 기술 및 인지 기능 건강 제품에 대한 용도 확대가, 고순도 부문의 평균 판매 가격을 밀어 올리고 있습니다. 비유전자 재조합(비GMO) 특성과 클린 라벨 처방에 있어서 알레르겐 프리 특성에 의해 해바라기 레시틴은 현저한 성장을 이루고 있습니다. 북미 및 유럽의 식품 및 음료 제조업체에서는 유전자 변형 원료에 대한 우려가 높아지는 가운데, 대두 유래에서 해바라기 유래의 레시틴으로의 이행이 진행되고 있습니다. 해바라기 레시틴은 중성 풍미 특성과 높은 인지질 함량으로 식물성 유제품, 베이커리 제품, 과자 제품에 적합합니다. 제약 산업에서도 리포솜형 약물 전달 시스템에서 해바라기 레시틴의 사용이 증가하고 있으며, 고순도 및 추적 성 요구가 고순도 레시틴 부문의 성장을 이끌고 있습니다.

가공 식품 업계에서는 천연 유래 유화제로의 전환이 진행되고 있으며, 제품 안정성 유지와 클린 라벨 요건 달성에 있어서 레시틴은 필수 성분이 되고 있습니다. 소비자들 사이에서 편리성이 높고, 보존성이 뛰어나며, 빨리 먹을 수 있는 식품에 대한 기호가 높아지고 있기 때문에 균일성을 유지하고, 식감을 향상시키며, 보존 기간을 연장하는 유화제 및 안정제에 대한 수요가 증가하고 있습니다. 콩, 해바라기 씨앗, 계란과 같은 천연 원료에서 추출한 레시틴은 유화제, 분산제 및 습윤제로 여러 기능을 수행하며 제조업체에게 다용도 및 비용 효율성을 제공합니다. 클린 라벨 운동은 식품 제조 업체가 합성 대체품보다 레시틴과 같은 천연 첨가제를 선택하도록 촉구하고 시장 수요를 증가시키고 있습니다. 미국 노동 통계국에 따르면, 2023년에 미국 가정이 베이커리 제품에 평균 574달러를 지출하고 있는 것에서도 분명한 바와 같이, 가공 식품 및 포장 식품에 대한 소비자 지출은 견조하게 추이하고 있습니다.

동물 영양 분야는 레시틴 수요의 중요한 성장 영역이며, 규제 당국의 승인 및 축산 생산성 향상에 대한 입증된 효과가 이를 지원합니다. 미국 식품의약국(FDA)의 21 CFR Part 573 규제는 동물 사료 용도 분야에서 레시틴의 안전성을 확인하고 사료 제조업체에 대한 명확한 규제 프레임워크를 제공하며 업계 전반에서 일관된 구현을 보장합니다. 레시틴에 함유된 인지질은 단위 동물의 지방 소화를 촉진하여, 축산 경영에 있어서 성장률 및 사료 효율의 향상으로 이어집니다. 수산 양식 산업은 레시틴과 같은 기능성 사료 원료 수요를 견인하는 주요 분야입니다. 유엔 식량농업기관(FAO)의 보고에 따르면 2022-2023년 세계의 양식 생산량은 1억 3,090만 톤에 이르렀고, 수산 및 양식 총생산량 2억 2,320만 톤에 차지하는 비율은 2020년 대비 4% 증가했습니다. 이 성장에 따라, 기존 사료 원료를 대신하는 지속 가능한 식물 유래 대체품의 채용이, 수산 사료 및 동물 사료 산업에 요구되는 압력이 강해지고 있습니다.

레시틴 시장은 콩, 해바라기 씨앗, 계란 등 원료 가격의 변동으로 인해 큰 제약에 직면하고 있습니다. 이러한 1차 정보는 기상 조건, 지정학적 문제, 무역 정책, 공급망 혼란 등 다양한 요인의 영향을 받기 쉬운 상황입니다. 예를 들어, 미국, 브라질, 우크라이나와 같은 주요 생산 지역의 비정상적인 기상과 가뭄은 작물의 수확량을 줄이고 레시틴 생산 원료의 가용성과 비용에 영향을 줄 수 있습니다. 또한 레시틴은 오일 씨앗의 가공에서 얻어지기 때문에 식용유 시장 전체의 변화도 레시틴 가격에 영향을 미칩니다. 소비 패턴의 변화 및 바이오연료 규제 등에 의한 대두유와 해바라기유 수요 변동은 레시틴 공급량 및 가격 설정에 영향을 미칩니다. 이 불안정성은 제조업체가 안정적인 비용 구조와 이익률을 유지하는 데 어려움을 낳습니다. 생산 비용의 상승은 특히 가격에 민감한 시장에서 합성 유화제에 대한 레시틴의 경쟁력에도 영향을 미칩니다.

대두 레시틴은 확립된 공급망 및 세계의 대두 가공 인프라에 의한 비용 우위성을 배경으로 2025년에는 64.78%라는 압도적인 시장 점유율을 차지하고 있습니다. 해바라기 레시틴은 비유전자 재조합(비GMO) 특성과 알레르겐 프리라는 특징이 소비자의 건강 지향이나 높아지는 시장 수요와 합치해, 2026-2031년 CAGR 7.65%로 가장 급속한 성장이 전망되는 원료 부문입니다. 계란 레시틴은 우수한 기능성이 요구되는 전문 용도, 특히 의약품 및 고급 식품 분야에서의 지위를 유지하면서 높은 부가가치 부문에서 안정적인 실적을 보여줍니다.

기존의 원료 공급원에 영향을 미치는 공급망의 혼란 시기에는, 유채 레시틴은 유력한 대체 원료로 부상하여 제조업체에게 추가 조달 유연성을 제공합니다. 캐놀라 레시틴을 포함한 대체 원료는 카길사의 미국 식품의약국(FDA)에 의한 일반적으로 안전하다고 인정되는(GRAS) 판정 등의 규제 승인을 통해 시장 존재감을 확대하여 유기 및 비유전자 재조합 제품에서의 폭넓은 사용을 가능하게 하고 있습니다.

식품용 레시틴은 2025년에 56.62% 시장 점유율을 차지했고, 주로 제빵, 제과 및 유제품 분야에 있어서 유화 솔루션으로서 가공 식품 산업에 공헌하고 있습니다. 본 원료는 식품 가공 공정에서 매우 높은 범용성을 발휘합니다. 의약품 등급 레시틴은 2026-2031년 CAGR 9.02%의 성장이 전망되고 있습니다. 이것은 약물 전달 시스템과 영양 보충제 제제에서의 사용 확대가 주요 요인입니다. 의약품 분야는 레시틴의 입증된 안전성 프로파일과 다양한 용도에 대한 미국 식품의약국(FDA)의 승인에 의해 확대되고 있습니다. 규제 당국의 승인은 의약품 제제 전체에서 시장 성장의 가능성을 강화하고 있습니다.

화장품 및 산업 용도를 포함한 기타 등급에서도 제조업체가 비 전통적인 용도에 레시틴을 도입함에 따라 성장 기회가 탄생했습니다. 아메리칸 레시틴 컴퍼니 등의 기업은 대두 레시틴이나 해바라기 레시틴 유래의 포스파티딜세린 등, 특수한 유도체를 개발하는 것으로 의약품 등급 부문을 추진하고 있습니다. 이 제형은 엄격한 의약품 품질 기준 및 사양을 준수합니다. 높은 부가가치 유도체를 통해 공급업체는 의약품 용도에서 프리미엄 가격과 이익률을 향상시킴으로써 혜택을 누릴 수 있습니다.

북미는 2025년 시점에서 레시틴 시장의 35.21%를 차지하는 압도적 점유율을 유지했으며, 천연 유화제를 권장하는 미국 식품의약국(FDA)의 엄격한 규제가 이를 지원하고 있습니다. 이 지역은 대두 및 캐놀라 유압착 시설에 대한 대규모 투자와 식물성 식품 시장 투입 증가에 의해 생산 능력의 균형을 유지하고 있습니다. 보충제에 대한 높은 소비자 지출은 뇌 건강 제품에서 고품질 인지질의 채택을 촉진합니다. 아시아태평양은 2026-2031년 8.38%의 연평균 복합 성장률(CAGR)로 최고 성장률을 보였습니다. 중국의 보충제 산업 확대 및 인도의 베이커리 체인 개발은 표준 및 고급 레시틴 제품 모두에 대한 수요를 견인하고 있습니다.

아시아태평양은 2026-2031년 연평균 복합 성장률(CAGR) 8.38%로 가장 빠르게 성장하는 지역으로 부상하고 있습니다. 특히 인지 기능 건강 및 심혈관 건강 제품에 대한 레시틴 용도를 주로 하는 중국의 영양보조식품 시장은 지역 수요 증가에 크게 기여하고 있습니다. 이 지역의 가공식품 제조 기반은 비용 효율이 우수한 유화 솔루션에 대한 엄청난 수요를 창출하고 있으며, 건강 효과에 대한 소비자 의식의 고조가 다양한 용도에 있어서 프리미엄 레시틴의 사용을 뒷받침하고 있습니다.

유럽에서는 수량 및 가치의 두 부문에서 균형이 유지됩니다. 유럽식품안전기관(EFSA)의 규제와 유전자 변형(GMO)에 대한 우려로 해바라기 레시틴 및 나타네 레시틴에 대한 수요가 높아지고 있습니다. 동유럽의 생산자는 지정학적 문제의 해결을 기다려야 하지만 해바라기 생산 지역에 가깝다는 장점을 살리고 있습니다. 남미는 브라질의 콩 생산량을 배경으로 주요 공급 기지 역할을 합니다. 중동 및 아프리카에서는 식품 가공 산업의 확대 및 기능성 성분에 대한 소비자 의식이 높아짐에 따라 성장 가능성이 있습니다. 그러나 인프라 제약 및 정비되지 않은 규제 프레임워크는 성숙 시장에 비해 시장 성장을 여전히 제한하고 있습니다.

The lecithin market is expected to grow from USD 1.08 billion in 2025 to USD 1.15 billion in 2026 and is forecast to reach USD 1.54 billion by 2031 at 6.1% CAGR over 2026-2031.

Rising uptake of natural emulsifiers in processed foods, stringent clean-label regulations, and deepening penetration of pharmaceutical-grade phospholipids keep demand on a solid upward path. In parallel, pharmaceutical companies extend lecithin's reach into drug-delivery and cognitive-health products, lifting average selling prices in the high-purity segment. Sunflower lecithin is experiencing significant growth due to its non-GMO status and allergen-free properties in clean-label formulations. Food and beverage manufacturers in North America and Europe are transitioning from soy-based to sunflower-derived lecithin as consumers become more concerned about genetically modified ingredients. The neutral flavor profile and high phospholipid content of sunflower lecithin make it suitable for plant-based dairy, bakery, and confectionery products. The pharmaceutical industry is also increasing its use of sunflower lecithin in liposomal drug delivery systems, where high purity and traceability requirements drive growth in the high-purity lecithin segment.

The processed food industry is shifting toward natural emulsifiers, making lecithin an essential ingredient for maintaining product stability while meeting clean-label requirements. The increasing consumer preference for convenient, shelf-stable, and ready-to-eat food products has created a higher demand for emulsifying and stabilizing agents that maintain consistency, improve texture, and extend shelf life. Lecithin, extracted from natural sources such as soybeans, sunflower seeds, and eggs, serves multiple functions as an emulsifier, dispersing agent, and wetting agent, providing manufacturers with versatility and cost efficiency. The clean-label movement has encouraged food producers to choose natural additives like lecithin over synthetic alternatives, increasing its market demand. Consumer spending on processed and packaged foods remains strong, as evidenced by U.S. households spending an average of USD 574 on bakery products in 2023, according to the Bureau of Labor Statistics .

Animal nutrition applications represent a significant growth area for lecithin demand, supported by regulatory approvals and demonstrated benefits in livestock productivity. The Food and Drug Administration (FDA)'s 21 CFR Part 573 regulations confirm lecithin's safety for animal feed applications, providing a clear regulatory framework for feed manufacturers and ensuring consistent implementation across the industry . The phospholipid content in lecithin improves fat digestion in monogastric animals, resulting in better growth rates and feed efficiency in livestock operations. The aquaculture industry has become a major driver of demand for functional feed ingredients like lecithin. The Food and Agriculture Organization of the United Nations (FAO) reports that global aquaculture production reached 130.9 million tons in 2022/23, contributing to a total fisheries and aquaculture output of 223.2 million tons, representing a 4% increase from 2020 . This growth has increased pressure on aquafeed and animal feed industries to incorporate sustainable, plant-based alternatives to conventional feed ingredients.

The lecithin market faces significant constraints due to fluctuating raw material prices, particularly soybeans, sunflower seeds, and eggs. These primary sources are vulnerable to various factors, including weather conditions, geopolitical issues, trade policies, and supply chain disruptions. For instance, extreme weather events or droughts in major producing regions such as the United States, Brazil, or Ukraine can reduce crop yields, affecting the availability and cost of lecithin production materials. The volatility in the broader edible oil market also influences lecithin prices, as lecithin is derived from oilseed processing. Changes in soybean or sunflower oil demand, whether from shifting consumption patterns or biofuel regulations, affect lecithin supply and pricing. This instability creates challenges for manufacturers in maintaining stable cost structures and profit margins. The increased production costs also affect lecithin's competitiveness against synthetic emulsifiers, particularly in price-sensitive markets.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Soy lecithin holds a dominant 64.78% market share in 2025, supported by established supply chains and cost benefits from the global soybean processing infrastructure. Sunflower lecithin represents the fastest-growing source segment with a projected 7.65% CAGR during 2026-2031, driven by its non-GMO status and allergen-free characteristics that align with consumer health preferences and increasing market demands. Egg lecithin maintains its position in specialized applications requiring superior functionality, particularly in pharmaceutical and premium food products, while demonstrating consistent performance in high-value segments.

Rapeseed lecithin has emerged as a viable alternative during supply chain disruptions affecting conventional sources, offering manufacturers additional sourcing flexibility. Alternative sources, including canola lecithin, have expanded their market presence through regulatory approvals, such as Cargill's Food and Drug Administration (FDA) Generally Recognised as Safe (GRAS) determination, enabling broader use in organic and non-GMO formulations.

Food grade lecithin holds 56.62% market share in 2025, primarily serving the processed food industry with emulsification solutions across bakery, confectionery, and dairy applications. The ingredient demonstrates significant versatility in food processing operations. Pharmaceutical grade lecithin projects a 9.02% CAGR during 2026-2031, driven by its increasing use in drug delivery systems and nutraceutical formulations. The pharmaceutical segment expands through lecithin's proven safety profile and Food and Drug Administration (FDA) approval for various applications. The regulatory acceptance strengthens market growth potential across pharmaceutical formulations.

Additional grades, including cosmetic and industrial applications, present growth opportunities as manufacturers implement lecithin in non-traditional uses. Companies such as American Lecithin Company advance the pharmaceutical-grade segment by developing specialized derivatives, including phosphatidylserine from soy and sunflower lecithins. These formulations comply with stringent pharmaceutical quality standards and specifications. The high-value derivatives enable suppliers to benefit from premium pricing and enhanced profit margins in pharmaceutical applications.

The Lecithin Market is Segmented by Source (Soy, Sunflower, and More), by Grade (Food Grade, Pharmaceutical Grade, and Others), by Form (Liquid, Powder, and Others), by Nature (Organic, and Conventional), by Application (Food and Beverage, Animal Feed, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America holds a dominant 35.21% share of the lecithin market in 2025, supported by strict Food and Drug Administration (FDA) regulations favoring natural emulsifiers. The region maintains balanced capacity through significant investments in soybean and canola crushing facilities and increased plant-based food product launches. High consumer spending on supplements drives the adoption of premium phospholipids in brain-health products. Asia-Pacific demonstrates the highest growth rate with an 8.38% CAGR during 2026-2031. The expansion of China's supplement industry and India's bakery chains drives demand for both standard and premium lecithin products.

Asia-Pacific emerges as the fastest-growing region with a CAGR of 8.38% during 2026-2031, driven by expanding nutraceutical markets and rising disposable incomes that enable premium ingredient adoption. China's dietary supplement market, particularly for lecithin applications in cognitive health and cardiovascular wellness products, contributes significantly to regional demand expansion. The region's processed food manufacturing base generates substantial demand for cost-effective emulsification solutions, while increasing consumer awareness of health benefits supports premium lecithin usage in various applications.

Europe maintains a balanced approach between volume and value segments. European Food Safety Authority (EFSA) regulations and GMO concerns drive demand toward sunflower and rapeseed lecithin. Eastern European producers benefit from proximity to sunflower production regions, pending resolution of geopolitical issues. South America serves as a key supply center, leveraging Brazil's substantial soybean production. The Middle East and Africa present growth potential due to the expansion of food processing industries and rising consumer awareness of functional ingredients. However, infrastructure constraints and underdeveloped regulatory frameworks continue to limit market growth compared to mature markets.