유럽의 차량용 접착제 및 실란트 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

Europe Automotive Adhesives & Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1692583

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

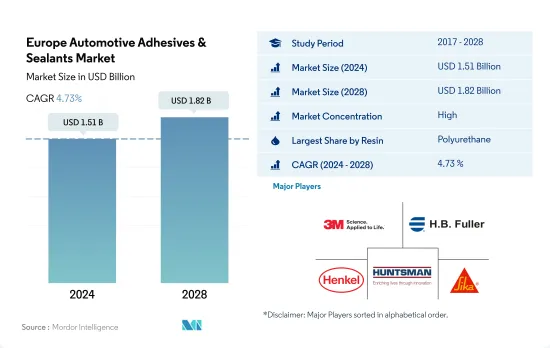

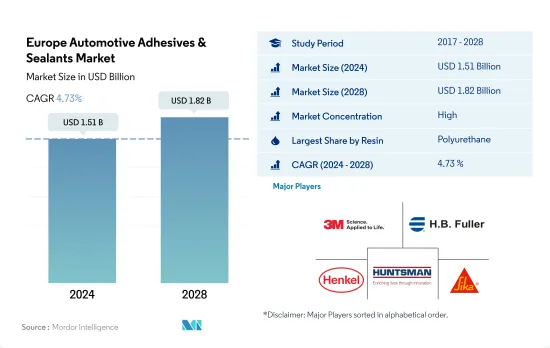

유럽의 차량용 접착제 및 실란트 시장 규모는 2024년에 15억 1,000만 달러로 추정되고, 2028년에는 18억 2,000만 달러에 이를 것으로 예측되며, 예측 기간(2024-2028년)의 CAGR은 4.73%를 나타낼 것으로 예측됩니다.

자동차 업체들의 차량 전동화 전환 증가로 시장 성장 촉진

폴리우레탄, 에폭시, 아크릴 수지는 유럽 차량용 접착제 및 실란트 시장에서 큰 비중을 차지합니다. 폴리우레탄 수지는 자동차 산업에서 고탄성 폼 시트, 경질 폼 단열 패널, B필러, 헤드라이너, 서스펜션 절연체, 범퍼 및 기타 경 상용차, 승용차, 전기차의 내부 부품 제조에 가장 일반적으로 사용되기 때문에 점유율이 더 높습니다.

유럽에서는 독일, 러시아, 폴란드, 프랑스, 영국, 벨기에, 이탈리아 등의 국가에서 에폭시 수지의 사용이 증가하고 있습니다. 이들 국가의 자동차 생산 능력과 함께 자동차 부품에 경량 수지의 사용량도 증가했습니다. 2021년 경상용차 생산량은 210만 대로 2020년 대비 1% 증가했습니다.

이 지역 정부가 시행하는 엄격한 배기가스 규범과 업체들의 차량 전기화로의 전환은 예측 기간 동안 유럽 자동차 접착제 시장의 성장을 촉진 할 것으로 예상됩니다. 이 시장은 전통적인 금속 용접에 비해 자동차 접착제가 제공하는 이점으로 인해 상당한 성장을 보일 것으로 예상됩니다. 자동차 접착제는 또한 차량의 소음, 거칠기 및 진동을 줄이고 편안한 주행을 제공합니다. 따라서 이러한 요인으로 인해 시장은 예측 기간 (2022-2028)동안 4.57 %의 CAGR을 기록 할 것으로 예상됩니다.

전기자동차 제조를 촉진하기 위해 이산화탄소 배출을 줄이기 위한 정부 법안으로 시장 수요 증가

유럽의 차량용 접착제 및 실란트 수요는 글로벌 차량 표준의 변화와 서유럽의 수요 감소, 국제 무역 분쟁으로 인해 2018년과 2019년에 소폭 감소했습니다. 2020년 유럽의 자동차 접착제 및 실란트 수요는 코로나19 팬데믹으로 인한 운영 및 공급망 제한으로 차량 생산량이 2019년 2,156만 대에서 2020년 1,690만 대로 감소하면서 20% 감소했습니다.

독일은 통합된 가치 사슬과 R&D 인프라가 뒷받침하는 대규모 제조 능력으로 인해 유럽 국가 중 차량용 접착제 및 실란트 수요에서 가장 큰 비중을 차지하고 있습니다. 2021년 독일은 유럽에서 생산된 전체 차량의 최대 20%에 해당하는 330만 대를 생산했습니다.

폴리우레탄과 에폭시 기반 접착제 및 실란트는 차량의 하중 지지력을 향상시키는 구조용 접착제로 사용할 수 있기 때문에 이 지역에서 가장 일반적으로 사용됩니다. 또한 전기 절연과 함께 내열성 및 내화학성을 갖추고 있어 PCB(인쇄 회로 기판) 애플리케이션에 이상적입니다. 2021년에는 8,500만 킬로그램의 폴리우레탄 기반 제품이 소비되었으며, 2028년에는 3.16%의 연평균 성장률로 1억 560만 킬로그램에 이를 것으로 예측됩니다.

이는 2030년까지 온실가스 배출량을 55% 이상 줄이겠다는 유럽 위원회의 기후 목표의 일환입니다. 'Fit for 55'법안은 2030년까지 자동차의 CO2 배출량을 55%, 승합차는 50% 감축하는 목표를 설정하고 있습니다. 이 규제로 인해 전기자동차에 대한 수요가 증가했으며, 자동차 전자 제품에도 사용할 수 있는 PU, 아크릴, 실리콘 기반 제품에 대한 수요가 예측 기간 동안 증가할 것으로 예상됩니다.

유럽의 차량용 접착제 및 실란트 시장 동향

전기자동차 활성화를 위한 정부 지원 정책으로 산업 규모 확대될 것

유럽 1인당 GDP는 3만 4,230달러로, 2022년 성장률은 전년 대비 1.6%입니다. 자동차산업부문이 GDP 전체에서 차지하는 비율은 약 2%입니다. 2021년 유럽의 자동차 생산량은 승용차 81%, 상용차 17%, 기타 2%입니다.

2020년에는 독일, 이탈리아, 스페인, 러시아, 영국을 포함한 많은 유럽 국가들이 코로나19 팬데믹의 영향을 받았습니다. 팬데믹으로 인해 공급망 중단, 국가 봉쇄, 칩 부족이 발생하여 유럽 내 자동차 생산에 영향을 미쳤습니다. 자동차 생산량은 2019년에 비해 22% 급감했습니다.

미국은 유럽에서 25.3%의 자동차를 수입하고 있으며, 2021년 미국 전체 자동차 수입의 10.3%를 독일이, 4.7%를 영국이 차지하며 미국의 주요 수입국 중 하나가 되었습니다. 2022년 초에는 러시아의 우크라이나 침공으로 인해 신차 판매가 20.5% 감소했으며, 이는 차량 생산에도 반영되었습니다. 2022년 1분기 유럽 자동차 시장은 지난해 같은 기간에 비해 10.6% 감소했습니다.

자동차 생산 대수는 많은 유럽 국가들이 전기자동차에 새로운 투자를 하고 있기 때문에 기간 중(2022-2027년)에 CAGR 2.25%로 성장할 전망입니다.

유럽의 차량용 접착제 및 실란트 산업 개요

유럽의 차량용 접착제 및 실란트 시장은 상당히 통합되어 있으며 상위 5개 기업에서 66.71%를 차지하고 있습니다. 이 시장의 주요 업체는 3M, H.B. Fuller Company, Henkel AG & Co. KGaA, Huntsman International LLC, Sika AG(알파벳 순으로 정렬)입니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건 및 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

최종 사용자 동향

자동차

규제 프레임워크

EU

러시아

밸류체인과 유통채널 분석

제5장 시장 세분화

수지

아크릴

시아노아크릴레이트

에폭시

폴리우레탄

실리콘

VAE 및 EVA

기타

기술

핫멜트

반응성

실란트

용매

UV 경화형 접착제

수성

국가명

프랑스

독일

이탈리아

러시아

스페인

영국

기타 유럽

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

3M

Arkema Group

AVERY DENNISON CORPORATION

DELO Industrie Klebstoffe GmbH & Co. KGaA

Dow

HB Fuller Company

Henkel AG & Co. KGaA

Huntsman International LLC

Illinois Tool Works Inc.

Sika AG

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계의 접착제 및 실란트 산업 개요

개요

Five Forces 분석 프레임워크(산업 매력도 분석)

세계의 밸류체인 분석

성장 촉진요인, 억제요인, 기회

출처 및 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

HBR

영문 목차

영문목차

The Europe Automotive Adhesives & Sealants Market size is estimated at 1.51 billion USD in 2024, and is expected to reach 1.82 billion USD by 2028, growing at a CAGR of 4.73% during the forecast period (2024-2028).

Increasing shift toward vehicle electrification by automobile players to propel market growth

Polyurethane, epoxy, and acrylic resins account for a large share of the European automotive adhesives and sealants market. The share of polyurethane resins is higher as they are most commonly used in the automotive industry to manufacture high-resilience foam seating, rigid foam insulation panels, B-pillars, headliners, suspension insulators, bumpers and other interior parts of light commercial vehicles, cars, and electric vehicles.

In Europe, the usage of epoxy resins is increasing in countries like Germany, Russia, Poland, France, the United Kingdom, Belgium, and Italy. The use of lightweight resins in automotive vehicle parts increased along with automotive vehicle production capacities in these countries. In 2021, the production of light commercial vehicles increased to 2.1 million units, an increase of 1% over 2020. Thus, the usage of acrylic, silicone, and other resin-based adhesives and sealants increased in the region.

The stringent emission norms implemented by governments in the region and the shift toward vehicle electrification by players are expected to boost the growth of the European automotive adhesives market over the forecast period. The market is expected to witness significant growth owing to the benefits offered by automotive adhesives over traditional metal welding. Automotive adhesives also reduce the noise, harshness, and vibration of the vehicle and provide comfortable driving. Hence, owing to such factors, the market is estimated to register a CAGR of 4.57% during the forecast period (2022-028).

Government legislations to reduce Co2 emissions to boost electric vehicle manufacturing in turn boosting market demand

Europe's automotive adhesives and sealants demand declined slightly in 2018 and 2019 due to changes in global vehicle standards and demand falls in western Europe and international trade conflicts. In 2020, Europe's automotive adhesives and sealants demand decreased by 20% as vehicle production fell from 21.56 million units in 2019 to 16.9 million units in 2020 due to operational and supply chain restrictions caused by the COVID-19 pandemic.

Germany has the largest share of the demand for automotive adhesives and sealants among European countries due to its large manufacturing capacity, which is supported by the integrated value chain and R&D infrastructure of the country. In 2021, Germany manufactured 3.3 million units which constitute up to 20% of the total vehicles manufactured in Europe.

Polyurethane and epoxy-based adhesives and sealants are most commonly used in the region because they can be used as structural adhesives to enhance the load-bearing capacity of the vehicle. They also offer heat and chemical resistance along with electric insulation, which makes them ideal for PCB (Printed Circuit Board) applications. In 2021, 85 million kilograms of polyurethane-based products were consumed, and by 2028 this is expected to reach 105.6 million kilograms with a CAGR of 3.16%.

As part of the European commission's climate goals to reduce greenhouse house emissions by at least 55% by 2030. The legislation 'Fit for 55' sets targets to reduce CO2 emissions from cars by 55% and vans by 50% by 2030. This regulation has boosted the demand for electric vehicles, which in turn is expected to boost the demand for PU, acrylic, and silicone-based products in the forecast period, as they can also be used in automotive electronics.

Europe Automotive Adhesives & Sealants Market Trends

Supportive government initiatives to promote electric vehicles will raise the industry size

Europe has a GDP of 34,230 USD per capita with a growth rate of 1.6% y-o-y in 2022. The automotive industry sector contributes a percentage of around 2% of the total GDP. The European vehicle production comprises 81% passenger vehicles, 17% commercial vehicles, and 2% other vehicles in 2021.

In 2020, many European countries were affected by the COVID-19 pandemic, including Germany, Italy, Spain, Russia, and the United Kingdom. The pandemic resulted in supply chain disruptions, lockdowns in the countries, and chip shortages which affected automotive production in Europe. The production of vehicles sharply declined by 22% compared to 2019.

The United States imports 25.3% worth of cars from Europe and became one of the leading importers of the United States, where Germany accounted for 10.3% and the United Kingdom for 4.7% of total imports of vehicles in the country in 2021. At the beginning of 2022, the sale of the new vehicle dropped by 20.5% due to the invasion of Ukraine by Russia, which reflected in vehicle production as well. In the first quarter of 2022, the European automotive market was down by 10.6% compared to the same period last year.

Vehicle production is likely to grow with a CAGR of 2.25% during the period (2022 to 2027) due to the new investments being made in electric vehicles by many European countries. For instance, Spain is going to invest USD 5.1 billion in electric vehicle production.

Europe Automotive Adhesives & Sealants Industry Overview

The Europe Automotive Adhesives & Sealants Market is fairly consolidated, with the top five companies occupying 66.71%. The major players in this market are 3M, H.B. Fuller Company, Henkel AG & Co. KGaA, Huntsman International LLC and Sika AG (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 End User Trends

4.1.1 Automotive

4.2 Regulatory Framework

4.2.1 EU

4.2.2 Russia

4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

5.1 Resin

5.1.1 Acrylic

5.1.2 Cyanoacrylate

5.1.3 Epoxy

5.1.4 Polyurethane

5.1.5 Silicone

5.1.6 VAE/EVA

5.1.7 Other Resins

5.2 Technology

5.2.1 Hot Melt

5.2.2 Reactive

5.2.3 Sealants

5.2.4 Solvent-borne

5.2.5 UV Cured Adhesives

5.2.6 Water-borne

5.3 Country

5.3.1 France

5.3.2 Germany

5.3.3 Italy

5.3.4 Russia

5.3.5 Spain

5.3.6 United Kingdom

5.3.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

6.4.1 3M

6.4.2 Arkema Group

6.4.3 AVERY DENNISON CORPORATION

6.4.4 DELO Industrie Klebstoffe GmbH & Co. KGaA

6.4.5 Dow

6.4.6 H.B. Fuller Company

6.4.7 Henkel AG & Co. KGaA

6.4.8 Huntsman International LLC

6.4.9 Illinois Tool Works Inc.

6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

8.1 Global Adhesives and Sealants Industry Overview

8.1.1 Overview

8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)