ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

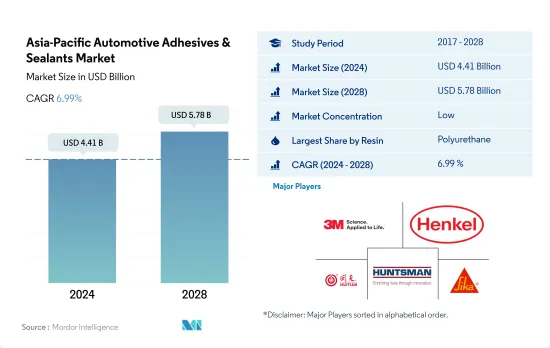

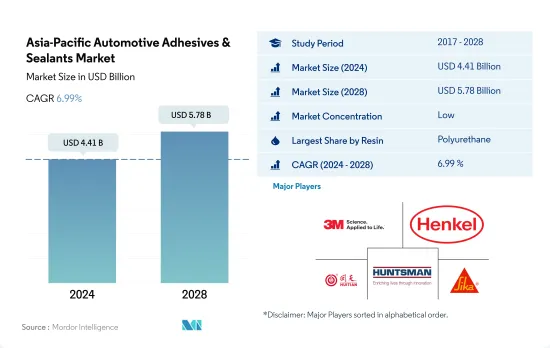

아시아태평양의 자동차용 접착제 및 실란트 시장 규모는 2024년 44억 1,000만 달러, 2028년에는 57억 8,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2024-2028년) CAGR 6.99%로 성장할 것으로 예측됩니다.

자동차 산업에서 지속가능성 채택과 EV 생산 증가로 시장 수요 촉진

아시아태평양의 자동차 접착제 및 실란트 시장에서 폴리우레탄 수지는 가장 큰 점유율을 차지합니다. 북미에는 많은 생산 시설이 있기 때문에 폴리우레탄 접착제의 사용 범위는 다른 수지보다 높습니다. 2017년부터 2019년까지 자동차 생산 감소로 소비 성장률은 약 5% 감소했습니다. COVID-19 팬데믹 이후 소비 성장률은 전년 대비 10% 상승했습니다. 폴리우레탄 접착제는 2022년부터 2028년까지의 예측 기간 동안 CAGR 4.5%를 나타낼 것으로 예상됩니다.

에폭시 접착제와 아크릴 접착제도 아시아태평양 자동차용 접착제 시장에서 큰 존재감을 보이고 있습니다. 에폭시 접착제는 제2위의 소비 재료이며, 예측 기간 2022-2028년까지 CAGR 약 4.2%를 나타낼 것으로 예상됩니다.

시아노아크릴레이트와 실리콘 실란트 등의 접착제는 증가 경향에 있습니다. 그 결과 향후 수년간 수요 증가로 이어질 가능성이 있습니다.

주요 자동차 제조업체인 중국이 시장 주도권을 잡을 것으로 예상됩니다.

아시아태평양은 세계 최대의 자동차 생산국이며, 중국, 인도, 일본 등 국가가 세계의 주요 자동차 생산국 중 하나입니다.

2020년에는 중국, 인도, 말레이시아, 일본, 인도네시아 등 많은 국가가 COVID-19 팬데믹의 영향을 받았습니다.

아시아태평양은 접착제 및 실란트의 생산으로 성장하고 있는 지역이며, 그 중에서도 중국은 국내의 고품질 생산 설비에 의해 자동차용 접착제 및 실란트의 최대 생산국입니다. 인도도 자동차 생산 대국이며, 2022년에는 2021년 대비 6.5% 증가한 610만대의 자동차 생산이 전망되고 있습니다.

많은 국가가 전기자동차를 추진하는 정책을 실시하고 있기 때문에 이 지역에서는 전기자동차의 생산이 증가하고 있습니다 중국과 인도는 전기자동차의 성장시장입니다.

아시아태평양의 자동차 접착제 및 실란트 시장 동향

전기차의 보급이 업계를 견인

아시아태평양의 자동차 산업은 자동차 판매 대수가 크게 늘어나고 있으며, 시장을 견인하는 산업 중 하나입니다.

이 지역의 자동차 판매 대수는 생산 대수와 함께 크게 감소하고 있어 이 때문에 접착제의 이용이 영향을 받고 있습니다. COVID-19의 유행에 의해 전년대비 -10.2%를 기록했습니다. 제조시설의 조업정지와 공급체인의 혼란에 의한 자동차부품의 부족이 생산수준을 제약하였습니다.

아시아태평양의 EV 시장은 접착제 시장에 있어 또 하나의 성장 기회가 됩니다. 대규모 생산국입니다. 2016년부터 2021년까지 상용 전기자동차의 대수는 562,603대에서 1,116,382대로 증가하여 약 98%의 성장률을 기록했습니다.

아시아태평양의 자동차 접착제 및 실란트 산업 개요

아시아태평양의 자동차 접착제 및 실란트 시장은 단편화되어 있으며 상위 5개사에서 13.25%를 차지하고 있습니다. 시장의 주요 기업에는 3M, Henkel AG & Co. KGaA, Hubei Huitian New Materials, Huntsman International LLC, Sika AG(알파벳순)가 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

최종 사용자 동향

자동차

규제 프레임워크

호주

중국

인도

인도네시아

일본

말레이시아

싱가포르

한국

태국

밸류체인과 유통채널 분석

제5장 시장 세분화

수지

아크릴

시아노아크릴레이트

에폭시

폴리우레탄

실리콘

VAE 및 EVA

기타 수지

기술

핫멜트

반응성

실란트

용제계

UV 경화형 접착제

수성

국가명

호주

중국

인도

인도네시아

일본

말레이시아

싱가포르

한국

태국

기타 아시아태평양

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

3M

Arkema Group

Dow

HB Fuller Company

Henkel AG & Co. KGaA

Hubei Huitian New Materials Co. Ltd

Huntsman International LLC

SHINSUNG PETROCHEMICAL

Sika AG

ThreeBond Holdings Co., Ltd.

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계의 접착제 및 실란트 산업의 개요

개요

Porter's Five Forces 분석 프레임워크(산업 매력도 분석)

세계의 밸류체인 분석

성장 촉진요인, 억제요인, 기회

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

JHS

영문 목차

영문목차

The Asia-Pacific Automotive Adhesives & Sealants Market size is estimated at 4.41 billion USD in 2024, and is expected to reach 5.78 billion USD by 2028, growing at a CAGR of 6.99% during the forecast period (2024-2028).

The adoption of sustainability in the automotive industry coupled with growing EV production to aid market demand

Across the Asia-Pacific automotive adhesives and sealants market, polyurethane resins account for the largest share. The scope of polyurethane adhesive in North America is higher than other resins since the region includes many production facilities. From 2017 to 2019, the consumption growth rate declined by about -5% due to a reduction in automotive production. After the COVID-19 pandemic, the consumption growth rate rose by 10% Y-o-Y. Polyurethane adhesives are expected to record a CAGR of 4.5% during the forecast period 2022 to 2028.

Epoxy and acrylic adhesives also have a significant presence in the Asia-Pacific automotive adhesives market. However, for epoxy, the upcoming year could be a great challenge as the raw materials used to produce epoxy adhesives are hazardous in nature and, thus, are getting regulated by government bodies in the region, such as AICS, PICCS, IECSC, and NZIoC. Epoxy adhesive is the second-largest consumed material and is expected to record a CAGR of about 4.2% during the forecast period 2022-2028. The epoxy adhesives segment is followed by the acrylic adhesives segment, which is expected to record a CAGR of about 4.5% during the forecast period 2022-2028.

Adhesives such as cyanoacrylate and silicone sealants are on a growing trend. The adoption of sustainability in the automotive industry is increasing significantly, and EV production is increasing to a large extent. As a result, the usage of these adhesives for electronic component assembly in automobiles is increasing, which, as a result, may lead to increased demand over the coming years. Cyanoacrylate and silicone adhesives are expected to record CAGRs of above 3.41% and 4.05%, respectively, in terms of volume during the forecast period 2022-2028.

China to hold the pole position in the market owing to being major automobile manufacturer

The Asia-Pacific is the largest producer of vehicles in the world, as countries like China, India, and Japan are among the major vehicle producers across the globe. Vehicle production in the region was expected to grow by 5.9% in 2022 from 47.9 million units in 2021.

In 2020, many countries, including China, India, Malaysia, Japan, and Indonesia, were impacted by the COVID-19 pandemic. The consumption of automotive adhesives and sealants declined by nearly 13.3% compared to 2019 due to the shutdown of production facilities, the closing of international borders, and raw material shortages in several countries.

Asia-Pacific is a growing region in the production of adhesives and sealants, of which China is the largest producer of automotive adhesives and sealants owing to the high-quality production facilities in the country. China has over 100 adhesives and sealants manufacturers supplying products worldwide. India is also a leading producer of vehicles, and it was expected to produce 6.1 million units of vehicles in 2022, which is 6.5% more than in 2021.

The production of electric vehicles is increasing in the region due to the policies implemented by many countries to promote electric vehicles. China and India are the growing markets for electric vehicles. These factors are expected to drive the demand for automotive adhesives and sealants in the forecast period. For instance, electric vehicle production in China amounted to 1.11 million units in 2021, an increase of 1.05% more than in 2020.

Increasing adoption of electric vehicles to drive the industry

The Asia-Pacific automotive industry is one of the leading industries in the market, as the sales of automotive vehicles are largely increasing. Among all the countries, China is the largest automotive producer, accounting for about 57% of the regional production, followed by Japan with 17%, India with 10%, and South Korea with 8%.

Vehicle sales in the region have majorly declined along with production, owing to which the utilization of adhesives has been impacted. While the Y-o-Y variation in 2017-18 was -1.8%, it fell further by -6.4% in 2018-19. In 2019-20, regional production was again impacted negatively and recorded a -10.2% decline from the previous year due to the COVID-19 pandemic. The shutdown of manufacturing facilities and the shortage of vehicle components due to disruptions in the supply chain constrained the production level. However, in 2021, the demand for automobiles rose again and is expected to continue, thereby increasing the utilization of adhesives across the region over the forecast period.

The EV market in Asia-Pacific offers another opportunity for the adhesives market to grow. The rising production and adoption of EVs and hybrid vehicles are boosting the usage of adhesives for electronic component assembly in vehicles. China is the largest producer of EVs globally as well as across the region. From 2016 to 2021, the volume of commercial electric vehicles increased from 562,603 to 1,116,382 units, recording a growth rate of about 98%. These factors are expected to increase the demand for adhesives and result in the higher market growth over the forecast period.

Asia-Pacific Automotive Adhesives & Sealants Industry Overview

The Asia-Pacific Automotive Adhesives & Sealants Market is fragmented, with the top five companies occupying 13.25%. The major players in this market are 3M, Henkel AG & Co. KGaA, Hubei Huitian New Materials Co. Ltd, Huntsman International LLC and Sika AG (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 End User Trends

4.1.1 Automotive

4.2 Regulatory Framework

4.2.1 Australia

4.2.2 China

4.2.3 India

4.2.4 Indonesia

4.2.5 Japan

4.2.6 Malaysia

4.2.7 Singapore

4.2.8 South Korea

4.2.9 Thailand

4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

5.1 Resin

5.1.1 Acrylic

5.1.2 Cyanoacrylate

5.1.3 Epoxy

5.1.4 Polyurethane

5.1.5 Silicone

5.1.6 VAE/EVA

5.1.7 Other Resins

5.2 Technology

5.2.1 Hot Melt

5.2.2 Reactive

5.2.3 Sealants

5.2.4 Solvent-borne

5.2.5 UV Cured Adhesives

5.2.6 Water-borne

5.3 Country

5.3.1 Australia

5.3.2 China

5.3.3 India

5.3.4 Indonesia

5.3.5 Japan

5.3.6 Malaysia

5.3.7 Singapore

5.3.8 South Korea

5.3.9 Thailand

5.3.10 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

6.4.1 3M

6.4.2 Arkema Group

6.4.3 Dow

6.4.4 H.B. Fuller Company

6.4.5 Henkel AG & Co. KGaA

6.4.6 Hubei Huitian New Materials Co. Ltd

6.4.7 Huntsman International LLC

6.4.8 SHINSUNG PETROCHEMICAL

6.4.9 Sika AG

6.4.10 ThreeBond Holdings Co., Ltd.

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

8.1 Global Adhesives and Sealants Industry Overview

8.1.1 Overview

8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)