북미의 사료 산제 시장 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

North America Feed Acidifiers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1685939

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

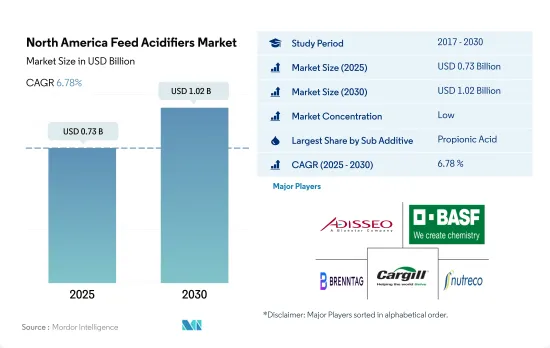

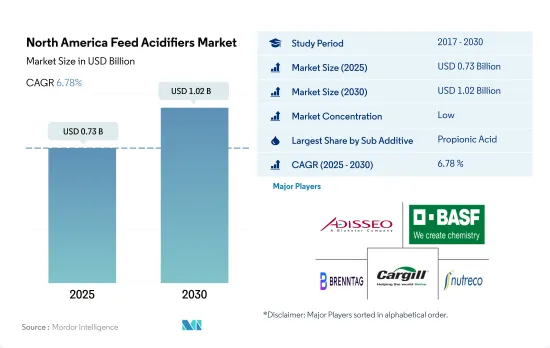

북미의 사료 산제 시장 규모는 2025년에 7억 3,000만 달러로 추정되고, 2030년에는 10억 2,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2030년) CAGR은 6.78%를 나타낼 전망입니다.

사료 산제는 동물의 성장을 촉진하고 신진대사를 증가시키며 유해한 병원균에 대한 저항력을 제공하는 동시에 항생제 의존도를 줄이는 데 중요한 역할을 합니다. 북미의 사료 산제 시장은 2022년 전체 사료 첨가제 시장의 7.1%를 차지하며 2018년에 비해 2019년에는 18.8% 증가했습니다.

미국은 사료 생산량 증가와 육류 및 유제품 시장 성장에 따른 수요 증가로 인해 2022년 북미의 사료 산제 시장의 70%를 차지하며 압도적인 점유율을 기록했습니다. 전체 사료 산제 중 프로피온산이 2022년 약 20억 달러로 가장 많이 사용되었으며, 푸마르산과 젖산이 그 뒤를 이어 각각 시장의 25%와 22.8%를 차지했습니다.

반추동물용 제품에 대한 높은 수요로 인해 사료용 프로피온산 부문은 2022년 38.8%를 차지하며 가장 큰 점유율을 차지할 것으로 예상됩니다. 미국은 사료 산제 시장에서 가장 빠르게 성장하는 국가로, 예측 기간 동안 7%의 연평균 성장률(CAGR)이 예상됩니다. 육류, 특히 가금류와 돼지고기에 대한 수요 증가, 유제품에 대한 수요 증가, 양식 재배 증가는 향후 몇 년 동안 미국의 사료 산제 시장을 주도 할 것으로 예상됩니다.

육류 및 해산물에 대한 수요 증가와 동물 생산성에서 사료 첨가제의 이점에 대한 인식 증가는 특히 미국에서 북미의 사료 산제 시장의 주된 촉진요인입니다.

북미의 사료 산제 시장은 최근 꾸준히 성장해 왔으며, 2022년에는 세계 시장의 7.1%를 차지했으며, 그 시장 규모는 6억 5,000만 달러였습니다.

모든 동물종 중에서 반추동물이 사료 산제의 가장 큰 사용자이며, 이 부문은 2032년에 2억 3,000만 달러의 시장 가치를 차지할 것으로 예상됩니다.

미국은 북미에서 가장 큰 사료 산제 시장으로 2022년 전체 시장 점유율의 70%를 차지할 것으로 예상됩니다.

산제 유형 중 프로피온산, 푸마르산 및 젖산이 북미에서 가장 일반적으로 사용되며 가치 기준으로 전체 지역 시장의 각각 37.1%, 25.1% 및 22.7%를 차지합니다. 이러한 산제의 인기는 사료의 기호성을 높여 사료 섭취량을 늘리기 위한 다양한 동물의 효능 및 적용과 밀접한 관련이 있습니다.

육류 및 육류 제품에 대한 수요 증가와 1 인당 육류 소비 및 가축 인구 증가는 예측 기간 동안 6.7%의 CAGR로 북미의 사료 산제 시장을 주도 할 것으로 예상됩니다.

북미의 사료 산제 시장 동향

붉은 육류보다 가금육 소비가 높고 미국은 세계 최대 계란 및 가금육 생산국으로 가금육 생산 수요를 주도하고 있습니다.

북미 가금류 산업은 지난 몇 년 동안 크게 성장하여 2017년부터 2022년까지 가금류 사육 마릿수가 5.0% 증가할 것으로 예상됩니다. 이러한 성장은 주로 가금육 및 기타 가금류 제품에 대한 수요 증가에 기인합니다. 미국은 세계 최대 가금육 생산국이자 두 번째로 큰 수출국이자 주요 계란 생산국으로서 북미 가금류 산업을 지배하고 있습니다. 미국은 2022년 북미 지역 전체 가금류 생산량의 62.0%를 차지했습니다. 가금류 산업의 높은 수익률은 새로운 가금류 생산자들을 끌어들여 이 지역의 생산자 수를 늘리고 있습니다.

금류, 특히 육계는 다른 가축에 비해 성숙이 빠르고 시장 중량이 높아 대량으로 생산됩니다. 육계를 포함한 가금류는 좁은 공간에서도 사육이 가능하기 때문에 생산자는 좁은 땅을 포함한 다양한 환경에서 가금류를 사육할 수 있습니다.

가금류 육류 소비량은 소고기나 돼지고기보다 훨씬 높습니다. 붉은 육류 섭취와 관련된 건강 위험이 증가함에 따라 더 많은 사람들이 가금류를 더 살코기 있고 건강한 단백질 공급원으로 선택하고 있습니다. 국내외 시장에서 가금류 제품에 대한 수요 증가와 가금류 생산량 증가는 예측 기간 동안 시장의 성장을 더욱 촉진할 것으로 예상됩니다.

소매업의 확장과 고품질 해산물에 대한 수요로 인해 다량 영양소와 미량 영양소가 풍부한 양식 사료에 대한 수요가 증가하고 있습니다.

북미 지역의 양식 사료 생산량은 2022년 전 세계 생산량의 3.8%에 불과할 정도로 극히 일부분을 차지합니다. 영양학적으로 균형 잡힌 사료에 대한 수요 증가에 대응하기 위해 이 지역의 사료 제조업체들은 2022년 220만 톤에서 2029년 260만 톤으로 생산량을 늘릴 계획입니다. 양식 어종에 제공되는 배합 사료에는 집중적인 사육 조건에서 건강한 성장에 필요한 다량 영양소와 미량 영양소가 포함되어 있어 아태 지역의 양식 사료 수요 증가에 기여하고 있습니다.

2022년 사료 생산량의 73.2%를 차지한 어류는 사료 생산 측면에서 가장 눈에 띄는 어종입니다. 인간 식단에서 생선의 건강상의 이점에 대한 인식이 높아지고, 식품 소비 패턴이 변화하고, 소매 부문이 확대되고, 국제 시장에서의 높은 수요가 이 지역의 생선 생산량 증가에 기여하고 있습니다.

캐나다의 양식업 생산자들은 2020년에 3억 9,380만 달러를 사료에 지출했으며, 이는 2016년 대비 6.6% 증가한 수치로 고품질 수산물 사료에 대한 수요가 증가하고 있음을 보여줍니다. 전반적으로 다양한 수산물에 대한 수요 증가와 양식 어종에 대한 영양적으로 균형 잡힌 사료의 필요성이 향후 북미 양식 사료 생산의 성장을 견인할 것으로 예상됩니다.

북미의 사료 산제 산업 개요

북미의 사료 산제 시장은 단편화되어 주요 5개사에서 25.96%를 차지하고 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

동물 사육 수

가금류

반추동물

돼지

사료 생산

양식

가금류

반추동물

돼지

규제 프레임워크

캐나다

멕시코

미국

밸류체인과 유통채널 분석

제5장 시장 세분화

하위 산제

푸마르산

젖산

프로피온산

기타

동물

양식

하위 동물별

어류

새우

어류

기타

가금류

하위 동물별

육계

레이어

기타

반추동물

하위 동물별

육우

젖소

기타 반추동물

돼지

기타 동물

국가명

캐나다

멕시코

미국

기타 북미

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일.

Adisseo

Alltech, Inc.

BASF SE

Bio Agri Mix

Brenntag SE

Cargill Inc.

EW Nutrition

Kemin Industries

SHV(Nutreco NV)

Yara International ASA

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Five Forces 분석 프레임워크

세계의 밸류체인 분석

세계 시장 규모와 DRO

출처 및 참고문헌

도표 목록

주요 인사이트

데이터 팩

용어집

HBR

영문 목차

영문목차

The North America Feed Acidifiers Market size is estimated at 0.73 billion USD in 2025, and is expected to reach 1.02 billion USD by 2030, growing at a CAGR of 6.78% during the forecast period (2025-2030).

Feed acidifiers are important in promoting animal growth, increasing metabolism, and providing resistance to harmful pathogens while reducing dependence on antibiotics. The North American feed acidifiers market accounted for 7.1% of the total feed additives market in 2022, an 18.8% increase in 2019 compared to 2018. This high share was attributed to the increased market value of probiotic types due to increased feed production.

The United States dominated the North American feed acidifiers market, accounting for 70% in 2022, mainly due to higher feed production and demand from the country's growing meat and dairy product markets. Among all feed acidifiers, propionic acid was most significantly used, valued at almost USD 0.2 billion in 2022, followed by fumaric acid and lactic acid, accounting for 25% and 22.8% of the market, respectively.

Ruminants held the largest share of the feed propionic acid segment, accounting for 38.8% in 2022 due to the high demand for ruminant products. The United States is the fastest-growing country in the feed acidifiers market, with a projected CAGR of 7% during the forecast period. The increasing demand for meat, especially poultry and pork, the rising demand for dairy products, and the growing aquaculture cultivation are expected to drive the country's feed acidifiers market in the coming years.

The rising demand for meat and seafood and increasing awareness about the benefits of feed additives in animal productivity are the major drivers of the North American feed acidifiers market, especially in the United States.

The North American feed acidifiers market has grown steadily in recent years, and in 2022, it accounted for 7.1% of the global market, with a value of USD 0.65 billion. The use of acidifiers in animal feed has expanded due to the rising demand for meat and meat products, which resulted in an 18.7% increase in the market's value in 2019 compared to 2018.

Among all animal types, ruminants are the biggest users of feed acidifiers, and the segment accounted for a market value of USD 0.23 billion in 2022. This trend was mainly due to the high demand from dairy industries. The poultry segment followed closely behind, with a market share of 35.4% in 2022. However, swine is emerging as the fastest-growing segment, expected to record a CAGR of 6.7% during the forecast period due to the positive impact of probiotics on animal health.

The United States is the largest feed acidifiers market in North America, accounting for 70% of the total market share in 2022. It is also the fastest-growing country in the North American feed acidifiers market, expected to witness a CAGR of 7% during the forecast period.

Among acidifier types, propionic acid, fumaric acid, and lactic acid are the most commonly used in North America, accounting for 37.1%, 25.1%, and 22.7%, respectively, of the total regional market by value. The popularity of these acidifiers is closely linked to their benefits and application in different animals for enhancing feed intake by increasing the palatability of feed.

The increase in demand for meat and meat products and the rising per capita meat consumption and livestock population are estimated to drive the North American feed acidifiers market with a CAGR of 6.7% during the forecast period.

North America Feed Acidifiers Market Trends

Higher consumption of poultry meat than red meat and the United States is globally largest producer of eggs and poultry meat is driving the demand for poultry production

The North American poultry industry has experienced significant growth over the past few years, with the poultry headcount increasing by 5.0% from 2017 to 2022. This growth is largely due to the increasing demand for poultry meat and other poultry products. The United States dominates the North American poultry industry as the world's largest producer and second-largest exporter of poultry meat and a major egg producer. The United States accounted for 62.0% of the region's total poultry production in 2022. The high-profit margin in the industry is attracting new poultry producers, leading to an increase in the number of producers in the region. For example, Canada's number of egg producers increased from 1,062 in 2016 to 1,205 in 2021.

Poultry birds, especially broiler meat, are produced in large quantities due to their quick maturity and market weight, which is faster than other livestock. Poultry birds, including broilers, can be raised in small spaces, making it possible for producers to raise poultry in a variety of environments, including small plots of land. These advantages make poultry production more feasible. Mexican poultry production increased by 12% in 2022 from the previous year.

Poultry meat consumption is significantly higher than that of beef or pork. More people are choosing poultry as a leaner, healthier source of protein due to the rising health risks linked to eating red meat. This trend is expected to continue, driving the growth of the region's poultry industry. The increasing demand for poultry products from both domestic and international markets and rising poultry production are expected to further drive the growth of the market during the forecast period.

Expansion of retail industry, and demand for high-quality seafood is increasing the demand for macro-nutrients and micro-nutrients rich aquaculture feed

Aquaculture feed production in North America accounted for a small fraction of global production, representing only 3.8% in 2022. However, the demand for diverse seafood products is driving local aquaculture production. Feed production grew by 9.2% between 2017 and 2022. In response to the increasing demand for nutritionally balanced feed, feed millers in the region plan to increase production from 2.2 million metric tons in 2022 to 2.6 million metric tons in 2029. The compound feed offered to aquaculture species contains the macro and micronutrients needed for healthy growth under intensive rearing conditions, thus contributing to the increased demand for aquaculture feed in the region.

Fish, which accounted for 73.2% of feed production in 2022, is the most prominent species in terms of feed production. The rising awareness of the health benefits of fish in the human diet, changing food consumption patterns, the expanding retail sector, and high demand in the international market are contributing to the growth of fish production in the region. Fish feed production is expected to increase from 1.6 million metric tons in 2022 to 1.9 million metric tons in 2029 as producers focus on nutritional management to ensure the health and performance of their animals.

Canada's aquaculture producers spent USD 393.8 million on feed in 2020, a 6.6% increase from 2016, demonstrating the increasing demand for high-quality aquatic food. Overall, the increasing demand for diverse seafood products and the need for nutritionally balanced feed for aquaculture species are expected to drive the growth of aquaculture feed production in North America in the coming years.

North America Feed Acidifiers Industry Overview

The North America Feed Acidifiers Market is fragmented, with the top five companies occupying 25.96%. The major players in this market are Adisseo, BASF SE, Brenntag SE, Cargill Inc. and SHV (Nutreco NV) (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Animal Headcount

4.1.1 Poultry

4.1.2 Ruminants

4.1.3 Swine

4.2 Feed Production

4.2.1 Aquaculture

4.2.2 Poultry

4.2.3 Ruminants

4.2.4 Swine

4.3 Regulatory Framework

4.3.1 Canada

4.3.2 Mexico

4.3.3 United States

4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

5.1 Sub Additive

5.1.1 Fumaric Acid

5.1.2 Lactic Acid

5.1.3 Propionic Acid

5.1.4 Other Acidifiers

5.2 Animal

5.2.1 Aquaculture

5.2.1.1 By Sub Animal

5.2.1.1.1 Fish

5.2.1.1.2 Shrimp

5.2.1.1.3 fish

5.2.1.1.4 Other Aquaculture Species

5.2.2 Poultry

5.2.2.1 By Sub Animal

5.2.2.1.1 Broiler

5.2.2.1.2 Layer

5.2.2.1.3 Other Poultry Birds

5.2.3 Ruminants

5.2.3.1 By Sub Animal

5.2.3.1.1 Beef Cattle

5.2.3.1.2 Dairy Cattle

5.2.3.1.3 Other Ruminants

5.2.4 Swine

5.2.5 Other Animals

5.3 Country

5.3.1 Canada

5.3.2 Mexico

5.3.3 United States

5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).