ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

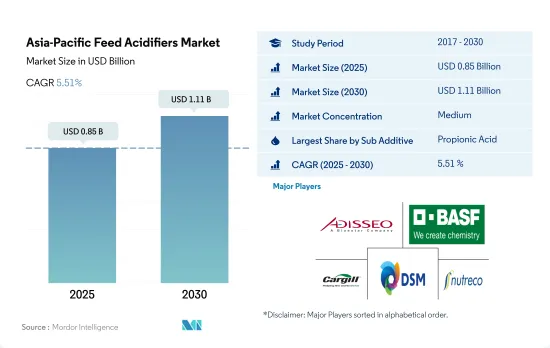

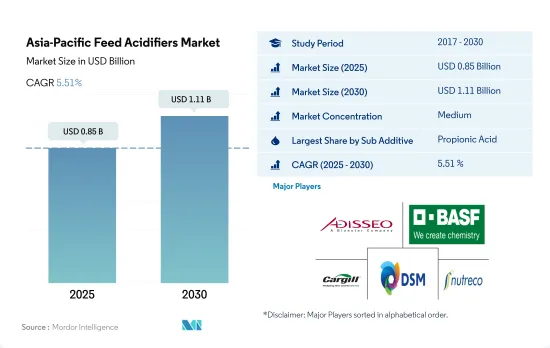

아시아태평양의 사료용 산미료 시장 규모는 2025년에 8억 5,000만 달러, 2030년에는 11억 1,000만 달러에 달할 것으로 예상되며, 예측 기간(2025-2030년) 동안 5.51%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다.

아시아태평양 사료 첨가제 시장의 산성화제 부문은 2022년 7.0%의 시장 점유율을 차지했습니다. 이 그룹의 첨가제는 사료의 성능을 개선하고 병원성 유기체 및 독성 대사 산물의 섭취를 감소시키기 때문에 동물 영양학에서 높은 평가를 받고 있습니다. 사료 산미료 중 프로피온산은 영양 흡수를 개선하고 병원성 미생물을 감소시키는 역할로 인해 아시아태평양에서 2017-2022년 47.8% 성장하여 2022년 2억 3,800만 달러의 큰 시장 가치를 차지했습니다.

가금류는 2022년 아시아태평양의 사료용 산미료 시장에서 시장 점유율 49.9%를 차지하며 이 지역에서 가장 큰 동물 유형 부문이 되었습니다. 이 부문은 성장을 가속하고 신진대사와 사료 섭취량을 증가시키며 유해한 병원균에 대한 내성을 제공하는 가금류에서 사료용 산미료의 사용량이 많기 때문에 예측 기간 동안 CAGR 6.1%를 나타낼 것으로 예상됩니다.

인도네시아는 2017-2022년 사료 생산량이 21.5% 증가하였고, 예측 기간 동안 젖산과 관련하여 6.5%의 가장 빠른 성장률을 나타낼 것으로 예상됩니다. 젖산은 배합사료에 첨가하면 소화관 건강, 소화율, 영양 이용률을 개선하는 데 도움이 됩니다.

중국은 2017-2022년 가금류 사육두수가 1.6% 증가함에 따라 2022년 산성화제 시장에서 44.2%의 가장 큰 시장 점유율을 차지했습니다.

위의 요인과 동물 영양에서 사료용 산미료의 중요성에 따라 아시아태평양의 사료용 산미료 시장은 예측 기간 동안 CAGR 5.5%를 나타낼 것으로 예상됩니다.

아시아태평양은 사료용 산미료 시장에서 괄목할 만한 성장세를 보이고 있으며, 중국, 인도, 일본이 시장 점유율 1위를 차지하고 있으며, 2022년에는 이들 국가들이 이 지역 시장 점유율의 59.3%를 차지했습니니다. 특히 중국은 2022년 시장 규모가 3억 2,180만 달러였고, 2029년에는 4억 6,810만 달러에 달할 것으로 예상됩니다. 중국의 점유율이 높은 이유는 가축 사육두수가 많기 때문에 2022년 중국은 아시아태평양 가금류 사육두수의 39.7%를 차지했습니다.

아시아태평양의 사료용 산미료 시장에서 가장 큰 동물 종은 가금류로 2022년 시장 점유율은 50%, 돼지가 31%, 반추 동물이 9.7%를 차지했습니다. 가금류와 돼지의 높은 시장 점유율은 상업적 재배가 활발하고 식품 산업에서 육류와 계란에 대한 수요가 높기 때문입니다. 가금류는 예측 기간 동안 가장 빠르게 성장할 것으로 예상됩니다. 암탉, 새우, 어류는 더 빠른 속도로 성장하고 있으며, 예측 기간 동안 각각 6.6%, 6.4%, 6.2%의 연평균 복합 성장률(CAGR)을 나타낼 것으로 예상됩니다.

이 지역에서 가장 많이 소비되는 사료용 산미료는 프로피온산과 푸마르산으로 각각 32.7%와 26.8% 시장 점유율을 차지하고 있습니다. 이는 높은 보급률과 가금류 및 양식용 사료의 높은 이용률과 관련이 있습니다.

예측 기간 동안 일본과 인도네시아는 아시아태평양의 사료용 산미료 시장에서 가장 빠르게 성장하는 부문으로, 양국의 사료 생산량 증가로 인해 각각 6.3%의 연평균 복합 성장률(CAGR)을 나타낼 것으로 예상됩니다. 아시아태평양의 사료용 산미료 시장은 산성화제 사용량 증가로 인해 예측 기간 동안 연평균 5.5%의 성장률을 보일 것으로 예상됩니다.

아시아태평양의 사료용 산미료 시장 동향

아시아태평양 개발도상국의 가처분 소득 증가, 양계업에 대한 정부 지원 제도, 중국이 최대 계란 생산국이라는 점 등이 아시아태평양의 양계 인구 증가에 기여하고 있습니다.

아시아태평양은 세계 농업 부문의 대부분을 차지하고 있으며, 가금류는 가장 큰 부문으로 2022년 세계 가금류 생산량의 42.4%를 차지했습니다. 가금류 소비는 인도, 베트남 등 신흥국의 인기 상승, 급속한 도시화, 가처분 소득 증가에 힘입어 2021년 가금류 인구는 2017년 대비 37.3% 증가했습니다.

2021년에는 중국, 인도네시아, 인도가 각각 39.7%, 25.3%, 5.7% 시장 점유율을 차지하며 이 지역의 가금류 시장에서 큰 비중을 차지했습니다. 이러한 가금류 제품 수요 증가는 계란과 육류에 대한 수요 증가와 양계 산업을 지원하는 정부 제도에 기인합니다. 예를 들어, 인도 축산 및 낙농부는 가금류 사업을 지원하는 자본 기금 제도를 도입하여 농가를 교육하고 수확물의 품질을 향상시켜 시장 성장을 가속할 것으로 기대되고 있습니다.

중국은 세계 최대의 계란 생산국으로 소비량과 생산량이 세계 생산량의 40% 이상을 차지하며, 9억 마리가 넘는 산란계와 연간 6,000만 마리의 병아리를 부화시키는 중국 최대의 산란계 사육 센터를 통해 산란계 사육은 괄목할 만한 성장을 기록했습니다.

이 지역의 육계 생산은 닭고기에 대한 소비자 수요 증가로 인해 빠르게 성장하고 있습니다. 예를 들어, 필리핀의 경우 2021년 닭고기 생산량은 2017년 대비 2.2% 증가했습니다. 이 지역의 닭고기 생산량은 닭고기에 대한 소비자의 선호도 변화와 닭고기 산업의 급속한 발전으로 인해 증가할 것으로 예상되며, 이는 사료 첨가제에 대한 수요를 증가시킬 수 있습니다.

양식 기술 향상, 사료 공장 확장, 인도 정부의 이니셔티브이 양식용 사료 생산량 증가에 기여하고 있습니다.

아시아태평양은 세계 양식 사료 생산 시장의 주요 기업이며, 어류와 새우가 주요 생산 품목이며, 2021년 이 지역은 3,760만 톤의 양식 사료를 생산하여 지역 전체 사료 생산량의 8.7%를 차지하였습니다. 이 지역의 여러 국가들은 증가하는 수요에 대응하기 위해 기술 발전과 사료 사용량 증가를 통해 양식 생산의 확대와 집약화에 주력하고 있습니다.

예를 들어, 인도는 생산 확대를 위해 수산부에 대한 예산 배정을 늘렸습니다. 양식용 사료는 어류가 큰 비중을 차지하고 있으며, 농지의 양식장 전환, 양식 기술 향상, 생산 집약화로 인해 2022년에는 2017년 대비 66% 증가한 3,110만 톤을 차지했습니다. 새우 사료 생산량은 2022년 이 지역 양식 사료 생산량의 4.2%를 차지했으며, 이 지역의 일부 국가들이 인증된 지속 가능한 수산물 생산량을 늘리기 위해 많은 정부 이니셔티브를 통해 자급자족형 양식 시스템을 도입하기 시작함에 따라 예측 기간 동안 빠르게 증가할 것으로 예상됩니다.

중국은 아시아태평양의 수산 사료 시장을 독점하고 있으며, 더 높은 용량의 사료 공장이 증가함에 따라 2022년에는 시장 점유율의 51.2%를 차지했습니다. 예를 들어, AB Agri는 중국에서 9번째 사료 공장을 설립하여 연간 24만 톤의 생산 능력을 갖추게 되었습니다. 양식 생산량 증가, 양식업 확대, 사료 소비 증가 등의 요인이 예측 기간 동안 이 지역의 양식 사료 생산량 증가를 촉진할 것으로 예상됩니다.

아시아태평양의 사료용 산미료 산업 개요

아시아태평양의 사료용 산미료 시장은 적당히 통합되어 있으며, 상위 5개 기업이 42.36%의 점유율을 차지하고 있습니다. 이 시장의 주요 업체는 다음과 같습니다. Adisseo, BASF SE, Cargill Inc., DSM Nutritional Products AG, SHV(Nutreco NV)(가나다순).

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 오퍼

제3장 서론

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

동물 마릿수

가금류

반추동물

돼지

사료 생산

수산양식

가금류

반추동물

양돈

규제 프레임워크

호주

중국

인도

인도네시아

일본

필리핀

한국

태국

베트남

밸류체인과 유통 채널 분석

제5장 시장 세분화

부첨가물 별

푸마르산

젖산

프로피온산

기타 산미료

동물별

수산양식

하위 동물별

어류

새우

기타 수산양식 종

가금류

하위 동물별

브로일러

레이어

기타 조류

반추동물

하위 동물별

육우

젖소

기타 반추동물

돼지

기타 동물

국가별

호주

중국

인도

인도네시아

일본

필리핀

한국

태국

베트남

기타 아시아태평양

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 개요(세계 레벨 개요, 시장 레벨 개요, 주요 사업 부문, 재무, 직원 수, 주요 정보, 시장 랭크, 시장 점유율, 제품 및 서비스, 최근 동향 분석 포함).

Adisseo

BASF SE

Brenntag SE

Cargill Inc.

DSM Nutritional Products AG

EW Nutrition

Kemin Industries

MIAVIT Stefan Niemeyer GmbH

SHV(Nutreco NV)

Yara International ASA

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계의 개요

개요

Five Forces 분석 프레임워크

세계 밸류체인 분석

세계 시장 규모와 DRO

정보원과 참고 문헌

도표 리스트

주요 인사이트

데이터 팩

용어집

LSH

영문 목차

영문목차

The Asia-Pacific Feed Acidifiers Market size is estimated at 0.85 billion USD in 2025, and is expected to reach 1.11 billion USD by 2030, growing at a CAGR of 5.51% during the forecast period (2025-2030).

The acidifiers segment of the Asia-Pacific feed additives market held a 7.0% market share in 2022. This group of additives is highly valued in animal nutrition as it improves feed performance and reduces the uptake of pathogenic organisms and toxic metabolites. Among the feed acidifiers, propionic acid held a significant market value of USD 238.0 million in 2022, which grew by 47.8% between 2017 and 2022 in the Asia-Pacific region due to its role in improving nutrient absorption and reducing pathogenic microbes.

Poultry birds were the largest animal type segment in the region, with 49.9% of the market share value in the Asia-Pacific feed acidifiers market in 2022. This segment is projected to record a CAGR of 6.1% during the forecast period due to the higher usage of feed acidifiers in poultry birds, which promote growth, boost metabolism and feed intake, and provide resistance to harmful pathogens.

Indonesia is expected to register the fastest growth rate of 6.5% during the forecast period, with respect to lactic acid, due to a 21.5% increase in feed production between 2017 and 2022. Lactic acid helps improve gastrointestinal tract health, digestibility, and nutrient utilization when added to compound feed.

China held the largest market share of 44.2% with respect to the acidifiers market in 2022 due to the increased headcount of poultry by 1.6% in the country between 2017 and 2022.

Based on the above-mentioned factors and the importance of feed acidifiers in animal nutrition, the Asia-Pacific feed acidifiers market is anticipated to record a CAGR of 5.5% during the forecast period.

The Asia-Pacific witnessed significant growth in the feed acidifiers market, with China, India, and Japan being the top countries in terms of market share. In 2022, these countries collectively accounted for 59.3% of the market share in the region. China, particularly, had a market value of USD 321.8 million in 2022, which is expected to reach USD 468.1 million in 2029. The country's high share can be attributed to its large livestock population, with China accounting for 39.7% of the Asia-Pacific's poultry population in 2022.

Poultry birds were the largest animal types in the Asia-Pacific feed acidifiers market, with a 50% market share in 2022, followed by swine and ruminants at 31% and 9.7%, respectively. The higher market share for poultry birds and swine was due to their higher commercial cultivation and demand for meat and eggs in the food industry. Poultry birds are anticipated to witness the fastest growth during the forecast period. Layers, shrimp, and fish are growing at a faster pace, anticipated to register a CAGR of 6.6%, 6.4%, and 6.2%, respectively, during the forecast period.

Propionic and fumaric acid were the most consumed feed acidifier types in the region, with 32.7% and 26.8% market share, respectively. This was associated with their higher penetration rates and higher utilization of feed for poultry and aquaculture species.

During the forecast period, Japan and Indonesia are expected to be the fastest-growing segments in the Asia-Pacific feed acidifiers market, with a CAGR of 6.3% each, due to increased feed production in both countries. The Asia-Pacific feed acidifiers market is expected to grow at a CAGR of 5.5% during the forecast period, driven by an increase in the usage of acidifiers.

Asia-Pacific Feed Acidifiers Market Trends

The growing disposable income in developing countries of Asia-Pacific and government support schemes for poultry industry, and China is largest producer of eggs are helping in growth of poultry population in the region

Asia-Pacific dominated the global agricultural sector, with poultry being the largest segment, accounting for 42.4% of global poultry production in 2022. Poultry consumption is driven by a rise in popularity, rapid urbanization, and growing disposable incomes in developing countries such as India and Vietnam, which recorded a 37.3% increase in poultry population in 2021 compared to 2017.

In 2021, China, Indonesia, and India held a significant share of the poultry market in the region, with a market share of 39.7%, 25.3%, and 5.7%, respectively. This growth in demand for poultry products can be attributed to the increased demand for eggs and meat and government schemes that support the poultry industry. For instance, the Department of Animal Husbandry & Dairy in India is introducing capital fund schemes to support poultry businesses, educating farmers on improving their yield quality, which is expected to boost the market's growth.

China is the largest producer of eggs in the world, with consumption and production accounting for over 40% of global production. With over 900 million stock-laying hens and the country's largest layer poultry farming center hatching 60 million chicks per year, the country's layer farming recorded significant growth.

Broiler production in the region is rapidly growing due to the increased consumer demand for chicken meat. The Philippines, for instance, recorded a 2.2% increase in chicken meat production in 2021 compared to 2017. The region's poultry production is expected to increase, driven by a shift in consumer preferences toward poultry meat and the rapid development of the poultry industry, which in turn may boost the demand for feed additives.

Improvement in fish farming technologies, expansion in number of feed mills and Indian government initiatives are helping in increasing the aquaculture feed production

Asia-Pacific is a major player in the global aquaculture feed production market, with fish and shrimp being the primary products. In 2021, the region produced 37.6 million metric tons of aquaculture feed, which accounted for 8.7% of the region's total feed production. Several countries in the region are focusing on expanding their aquaculture production and intensification through technological advancements and increased use of feed to meet the growing demand.

For instance, India increased its budget allocation to the Department of Fisheries to boost production. Fish holds a significant share of aquaculture feed, accounting for 31.1 million metric tons in 2022, an increase from 66% compared to 2017 due to the conversion of agricultural land to aquaculture ponds, the improvement of fish farming technologies, and the intensification of production. Shrimp feed production accounted for 4.2% of the aquafeed production in the region in 2022, and it is expected to increase rapidly during the forecast period as some countries in the region started implementing a self-sufficient aquaculture system through a number of government initiatives to increase the production of certified sustainable seafood.

China dominates the aquafeed market in Asia-Pacific, accounting for 51.2% of the market share in 2022 due to an increase in the number of feed mills with higher capacities. For instance, AB Agri opened its ninth feed mill in China, a plant with an annual capacity of 240,000 tons. Factors such as an increase in aquaculture production, expansion of aqua farming, and rise in consumption of feed are expected to drive the growth of aquafeed production in the region during the forecast period.

Asia-Pacific Feed Acidifiers Industry Overview

The Asia-Pacific Feed Acidifiers Market is moderately consolidated, with the top five companies occupying 42.36%. The major players in this market are Adisseo, BASF SE, Cargill Inc., DSM Nutritional Products AG and SHV (Nutreco NV) (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Animal Headcount

4.1.1 Poultry

4.1.2 Ruminants

4.1.3 Swine

4.2 Feed Production

4.2.1 Aquaculture

4.2.2 Poultry

4.2.3 Ruminants

4.2.4 Swine

4.3 Regulatory Framework

4.3.1 Australia

4.3.2 China

4.3.3 India

4.3.4 Indonesia

4.3.5 Japan

4.3.6 Philippines

4.3.7 South Korea

4.3.8 Thailand

4.3.9 Vietnam

4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

5.1 Sub Additive

5.1.1 Fumaric Acid

5.1.2 Lactic Acid

5.1.3 Propionic Acid

5.1.4 Other Acidifiers

5.2 Animal

5.2.1 Aquaculture

5.2.1.1 By Sub Animal

5.2.1.1.1 Fish

5.2.1.1.2 Shrimp

5.2.1.1.3 Other Aquaculture Species

5.2.2 Poultry

5.2.2.1 By Sub Animal

5.2.2.1.1 Broiler

5.2.2.1.2 Layer

5.2.2.1.3 Other Poultry Birds

5.2.3 Ruminants

5.2.3.1 By Sub Animal

5.2.3.1.1 Beef Cattle

5.2.3.1.2 Dairy Cattle

5.2.3.1.3 Other Ruminants

5.2.4 Swine

5.2.5 Other Animals

5.3 Country

5.3.1 Australia

5.3.2 China

5.3.3 India

5.3.4 Indonesia

5.3.5 Japan

5.3.6 Philippines

5.3.7 South Korea

5.3.8 Thailand

5.3.9 Vietnam

5.3.10 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).