유럽의 사료 산미제 시장(2025-2030년) : 시장 점유율 분석, 산업 동향, 통계 및 성장 예측

Europe Feed Acidifiers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1685850

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

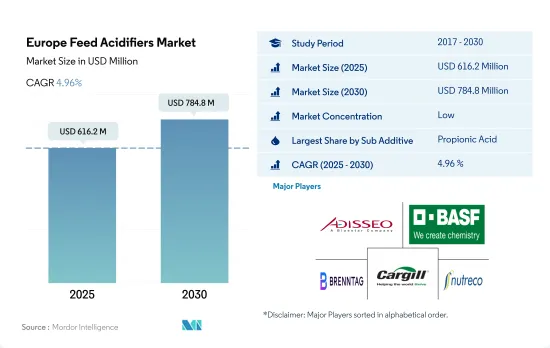

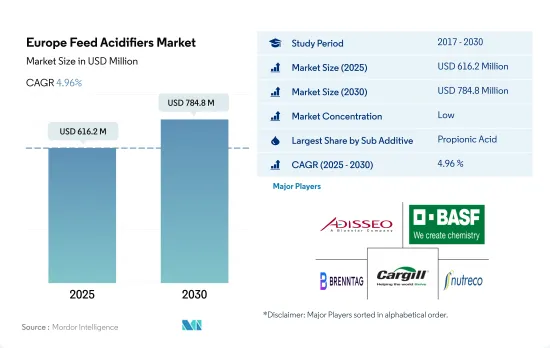

유럽의 사료 산미제 시장 규모는 2025년에 6억 1,620만 달러로 추정되며, 2030년에는 7억 8,480만 달러에 이를 것으로 예측되고, 예측 기간(2025-2030년)의 CAGR은 4.96%로 예상됩니다.

산미제는 사료의 기능성을 높이고 병원성 생물과 독성 대사물의 흡수를 억제하기 위해 필요한 동물 영양의 중요한 요소입니다.

조사 지역에서 가장 널리 사용되는 산미제는 프로피온산으로, 2022년 시장가치는 1억 8,270만 달러였으며, 이 부문은 예측 기간 중에 CAGR 5%를 나타낼 것으로 예측되고 있습니다.

가금류는 유럽 사료 산미제 시장에서 가장 큰 동물종 부문이며, 2022년 시장 점유율의 35.4%를 차지하였고 CAGR 5.0%를 나타낼 것으로 예측되고 있습니다. 사료 산미제는 성장을 가속하고 대사를 높이며 사료 섭취량을 증가시키고 유해한 병원체에 대한 저항력을 부여하기 위해 가금류용으로 널리 사용되고 있습니다.

젖산과 푸마르산은 예측 기간 중에 CAGR 5.1%를 기록하여 이 지역에서 가장 급성장할 분야로 예상됩니다.

스페인, 독일, 프랑스는 유럽의 주요 시장이며, 2022년 시장 점유율은 총 45.3%로 사료 생산량 전체의 12.1%를 차지하였습니다.

유럽은 사료 산미제의 주요 시장 중 하나이며, 사료 산미제는 동물 영양에서 사료 기능을 향상시키고 병원성 생물과 독성 대사 산물의 흡수를 감소시키는 데 중요한 역할을 합니다. 2022년 현재 사료 산미제는 금액 기준으로 유럽 사료 첨가물 시장의 7.0%를 차지하고 있으며 2017년부터 2022년 사이에 12.9% 증가했습니다.

유럽에서는 스페인, 독일, 프랑스, 러시아가 사료 산미제의 주요 시장이며, 특히 스페인은 2022년에 8,180만 달러라는 큰 시장 가치를 보유하였습니다. 스페인의 시장 점유율이 높은 이유는 2022년 사료 생산량이 전년 대비 2.5% 증가했기 때문입니다.

독일도 사료 산미제의 주요 시장이며 2022년 시장 가치는 8,140만 달러를 달성하였고 예측 기간 중에 CAGR 4.6%를 나타낼 것으로 예측되고 있습니다.

예측 기간 동안 유럽의 사료 산미제 시장에서는 영국이 CAGR 5.8%로 가장 급성장할 것으로 예측되고 있습니다.

사료 생산과 가축 인구 증가가 유럽 시장 성장 촉진요인입니다.

유럽 사료 산미제 시장 동향

유럽은 세계 3위의 가금육 수출국이며, 육계 생산은 가금육 생산의 82.6%를 차지하고 이는 가금육 생산 수요를 촉진할 것으로 예상됩니다.

유럽은 세계적인 닭고기 생산 및 수출국이며, 2021년의 연간 닭고기 생산량은 약 1,340만 톤이었습니다. 하지만 유럽 시장은 증가하는 세계 수요를 따라잡지 못하고 있습니다. 유럽에서 가장 큰 닭고기 생산국은 폴란드(생산량의 19.2%, 250만 톤), 프랑스(12.5%, 160만 톤), 스페인(12.3%), 독일(12%), 이탈리아(10.4%) 순입니다.

EU 지역 내에서는 육계 생산이 2021년의 가금육 생산 전체의 대부분(82.6%)을 차지하였고, 이어서 오리육이 3.3%였습니다. 또한, 러시아, 프랑스, 네덜란드, 우크라이나, 폴란드, 그리고 영국이 전체적으로 50% 이상을 차지했습니다. 산란계의 하위 부문은 달걀 소비 증가에 의해 유럽 전역에서 성장을 이루고 있으며 2017년의 5,864톤에서 2021년에는 613만 5,000톤으로 증가하였습니다.

가금육의 세계 4위 수입국이자 세계 3위 수출국인 유럽은 세계의 가금육 시장에 있어서 중요한 참가국입니다. 2021년 유럽 연합은 약 225만 2000톤에 달하는 가금육을 영국, 가나, 우크라이나 등 여러 나라에 수출했습니다.

82%를 차지하는 양어용 사료의 높은 수요와 수산물의 수입 급증이 양식용 배합 사료에 끼치는 부정적인 영향

2022년에 유럽은 세계의 양식용 배합 사료 생산에서 8.0%라는 큰 점유율을 차지하였고 생산량은 450만 톤에 이르렀습니다. 이는 질병 가능성을 줄이고 사료 효율을 높이기 위해 영양학적으로 균형잡힌 사료에 대한 수요가 증가하면서 발생하였습니다.

유럽의 주요 양식 사료 생산국은 튀르키예, 영국, 네덜란드, 스페인, 이탈리아, 프랑스이며, 이 지역의 2021년 양식종 생산량은 1,740만 톤이었으며 2018년에 비해 1.7%의 성장을 보였습니다. 인구와 1인당 수산물 소비량 증가가 이 지역의 양식 생산을 견인하고 있습니다.

수산 양식 사료 생산은 어류 사료가 압도적으로 많았으며 2022년의 점유율은 82%를 차지하였고 이어서 새우 사료가 4.3%, 기타 수생종 사료가 13.7%였습니다. 어류 사료는 다른 수산종에 비해 생산량이 더 많습니다.

유럽 사료 산미제 산업 개요

유럽의 사료 산미제 시장은 세분화되어 주요 5개사에서 37.31%를 차지하고 있습니다. 이 시장 주요 기업은 Adisseo, BASF SE, Brenntag SE, Cargill Inc., SHV (Nutreco NV) 입니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

가축 수

가금류

반추동물

양돈

사료 생산

수산 양식

가금류

반추동물

양돈

규제 프레임워크

프랑스

독일

이탈리아

네덜란드

러시아

스페인

튀르키예

영국

밸류체인과 유통채널 분석

제5장 시장 세분화

부첨가물

푸마르산

젖산

프로피온산

기타 산미제

동물

수산 양식

하위 동물별

어류

새우

기타 양식종

가금류

하위 동물별

육계

산란계

기타 조류

반추동물

하위 동물별

육우

젖소

기타 반추동물

양돈

기타 동물

국가명

프랑스

독일

이탈리아

네덜란드

러시아

스페인

튀르키예

영국

기타 유럽

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

Adisseo

Alltech, Inc.

BASF SE

Borregaard AS

Brenntag SE

Cargill Inc.

Kemin Industries

MIAVIT Stefan Niemeyer GmbH

SHV(Nutreco NV)

Yara International ASA

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Porter's Five Forces 분석 프레임워크

세계의 밸류체인 분석

세계 시장 규모와 DRO

정보원과 참고문헌

도표 목록

주요 인사이트

데이터 팩

용어집

CSM

영문 목차

영문목차

The Europe Feed Acidifiers Market size is estimated at 616.2 million USD in 2025, and is expected to reach 784.8 million USD by 2030, growing at a CAGR of 4.96% during the forecast period (2025-2030).

Acidifiers are a crucial component of animal nutrition as they enhance feed performance and reduce the uptake of pathogenic organisms and toxic metabolites. In Europe, the acidifiers market held a share of 7.0% in the total feed additives market in 2022, with a market value increase of 12.9% between 2017 and 2022.

Propionic acid was the most widely used acidifier in the region, with a market value of USD 182.7 million in 2022, and the segment is projected to record a CAGR of 5% during the forecast period. It improves nutrient absorption and reduces pathogenic microbes, making it an ideal choice for animal feed.

Poultry is the largest animal type segment in the European feed acidifiers market, and it accounted for 35.4% of the market share value in 2022. The segment is projected to register a CAGR of 5.0% during the forecast period. Feed acidifiers are extensively used in poultry birds to promote growth, increase metabolism, increase feed intake, and provide resistance to harmful pathogens.

Lactic acid and fumaric acid are expected to be the fastest-growing segments in the region, recording a CAGR of 5.1% during the forecast period. Lactic acid helps improve gastrointestinal tract health in animals, digestibility, and high nutrient utilization when added to the compound feed.

Spain, Germany, and France are the major markets in Europe, and they together held a market share of 45.3% in 2022. Spain's higher share was attributed to the country's higher feed production, with 12.1% of the total feed production in the region in 2022. Based on increased feed production and the importance of feed acidifiers in animal nutrition, the market is projected to record a CAGR of 4.9% during the forecast period.

The European region is one of the key markets for feed acidifiers, as it plays a crucial role in improving feed performance in animal nutrition and reducing the uptake of pathogenic organisms and toxic metabolites. As of 2022, feed acidifiers accounted for 7.0% of the European feed additives market in terms of value, and they increased by 12.9% between 2017 and 2022.

Spain, Germany, France, and Russia are the major markets for feed acidifiers in the European region, with Spain, in particular, holding a significant market value of USD 81.8 million in 2022. The high share of Spain was due to the increased feed production by 2.5% in 2022 compared to the previous year. Spain's market value is anticipated to reach USD 116.4 million in 2029, with a CAGR of 5.2% during the forecast period.

Germany is also a major market for feed acidifiers, with a market value of USD 81.4 million in 2022. This is projected to register a CAGR of 4.6% during the forecast period. This growth is attributed to the increased feed production in Germany by 0.9% between 2020 and 2022.

The United Kingdom is expected to be the fastest-growing country in the feed acidifiers market in the European region during the forecast period, with a CAGR of 5.8%. This is due to the increased livestock population and feed production in the country, with total feed production increasing by 4.7% between 2017 and 2022.

The increased feed production and livestock population are the key drivers for the market in the European region. As of 2022, the total feed production in Europe was 262.9 million metric tons, which increased by 2.0% from 2017. Consequently, the market is anticipated to register a CAGR of 4.9% during the forecast period.

Europe Feed Acidifiers Market Trends

Europe is 3rd largest exporter of poultry meat and broiler meat production accounted for 82.6% of poultry meat production which is expected to drive the demand for poultry production

Europe is a prominent global poultry meat producer and exporter, and it had an estimated annual poultry meat production of approximately 13.4 million metric tons in 2021. Despite being the second-most consumed meat in the region at 26.9 kg per capita per year, European poultry production has not kept pace with rising global demand. The largest poultry meat producers in the European region include Poland (accounting for 19.2% of production, or 2.5 million metric tons), France (12.5%, or 1.6 million metric tons), Spain (12.3%), Germany (12%), and Italy (10.4%).

Within the European Union, broiler meat production constituted the majority (82.6%) of total poultry meat production in 2021, followed by duck meat at 3.3%. Europe's poultry flock numbered approximately 2.45 billion birds in 2021, with Russia, France, the Netherlands, Ukraine, Poland, and the United Kingdom collectively comprising more than 50% of the population. The layer sub-segment is experiencing growth across Europe due to increased egg consumption, which rose to 6,135 thousand metric tons in 2021 from 5,864 metric tons in 2017.

As the fourth-largest importer and the third-largest exporter of poultry meat, Europe is a significant participant in the global poultry meat market. In 2021, the European Union exported roughly 2,252 thousand metric tons (carcass weight) of poultry meat to various countries, including the United Kingdom, Ghana, and Ukraine. The rising production of poultry birds, increasing demand for poultry products, and growing consumption of eggs are expected to be the key drivers of market growth in Europe.

High demand for fish feed which accounted for 82% and surge in seafood imports had a negative impact on compound feed for aquaculture

In 2022, Europe held a significant share of 8.0% in the global aquaculture compound feed production, with a production volume of 4.5 million metric tons. Compound feed production saw a notable increase of 15% between 2018 and 2022, driven by the growing demand for nutrient-balanced feed to reduce disease risk and improve feed efficiency. However, aquaculture feed production observed a decline of 21.2% in 2018, which may have been influenced by the surge in seafood imports and the relatively low prices of imported seafood, impacting the European compound feed market in 2018.

The major aquaculture feed producers in Europe are Turkey, the United Kingdom, the Netherlands, Spain, Italy, and France, and the region produced 17.4 million metric tons of aquaculture species in 2021, indicating a growth of 1.7% since 2018. The growth was attributed to the rise in population and per capita seafood consumption, which is driving aquaculture production in the region. This, in turn, propels the demand for compound feed, which is expected to increase by 18.2% during the forecast period (2023-2029).

Fish feed dominated aquaculture feed production, accounting for 82% share in 2022, followed by shrimp feed and other aquatic species feed, with shares of 4.3% and 13.7%, respectively, in the region. Fish food is the most consumed aquatic food across the region, and it is highly produced in comparison to other aquatic species. The expanding aquaculture industry, the rising demand for seafood and aquaculture products, and the growing awareness regarding quality meat are the major factors augmenting the growth of the market studied.

Europe Feed Acidifiers Industry Overview

The Europe Feed Acidifiers Market is fragmented, with the top five companies occupying 37.31%. The major players in this market are Adisseo, BASF SE, Brenntag SE, Cargill Inc. and SHV (Nutreco NV) (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Animal Headcount

4.1.1 Poultry

4.1.2 Ruminants

4.1.3 Swine

4.2 Feed Production

4.2.1 Aquaculture

4.2.2 Poultry

4.2.3 Ruminants

4.2.4 Swine

4.3 Regulatory Framework

4.3.1 France

4.3.2 Germany

4.3.3 Italy

4.3.4 Netherlands

4.3.5 Russia

4.3.6 Spain

4.3.7 Turkey

4.3.8 United Kingdom

4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

5.1 Sub Additive

5.1.1 Fumaric Acid

5.1.2 Lactic Acid

5.1.3 Propionic Acid

5.1.4 Other Acidifiers

5.2 Animal

5.2.1 Aquaculture

5.2.1.1 By Sub Animal

5.2.1.1.1 Fish

5.2.1.1.2 Shrimp

5.2.1.1.3 Other Aquaculture Species

5.2.2 Poultry

5.2.2.1 By Sub Animal

5.2.2.1.1 Broiler

5.2.2.1.2 Layer

5.2.2.1.3 Other Poultry Birds

5.2.3 Ruminants

5.2.3.1 By Sub Animal

5.2.3.1.1 Beef Cattle

5.2.3.1.2 Dairy Cattle

5.2.3.1.3 Other Ruminants

5.2.4 Swine

5.2.5 Other Animals

5.3 Country

5.3.1 France

5.3.2 Germany

5.3.3 Italy

5.3.4 Netherlands

5.3.5 Russia

5.3.6 Spain

5.3.7 Turkey

5.3.8 United Kingdom

5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).