United Kingdom Oil And Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1640341

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

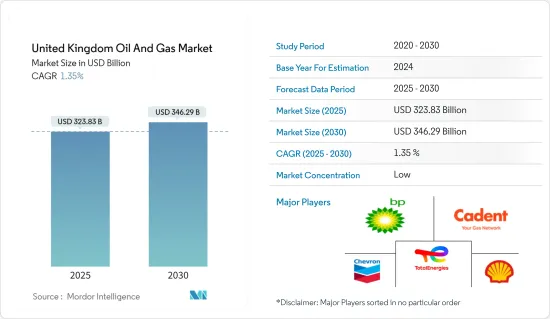

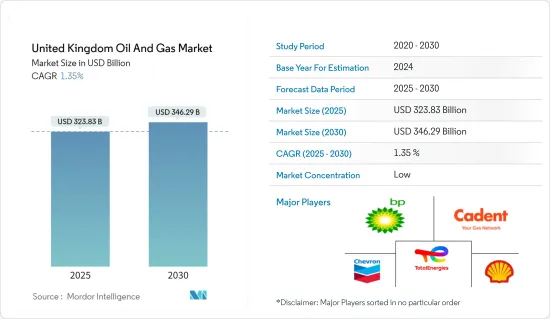

영국의 석유 및 가스 시장 규모는 2025년에 3,238억 3,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 1.35%로, 2030년에는 3,462억 9,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

중기적으로는 영국의 석유 및 가스 생산 증가와 석유 및 가스 인프라 개발 투자 증가가 예측 기간 동안 조사 대상 시장을 견인할 것으로 보입니다.

한편 신재생에너지기술의 성장과 최근 지정학적 동향에 따른 석유 및 가스가격의 변동은 예측 기간 동안 시장 개척을 억제할 것으로 예상됩니다.

그럼에도 불구하고 국가에서 새로운 석유 및 가스전이 발견되면 예측 기간 동안 조사 대상 시장에 큰 비즈니스 기회가 생길 것으로 기대됩니다.

영국의 석유 및 가스 시장 동향

업스트림 부문이 시장을 독점할 전망

영국은 북해에 상당한 석유 및 가스 매장량을 보유하고 있으며 이는 수십 년 동안 주요 생산원이 되었습니다. 매장량은 감소하고 있으나 현재도 계속적인 탐광 및 생산 노력이 필요한 상당량의 자원을 가지고 있습니다.

영국은 북해에서 해양 탐사 및 생산을 위한 인프라가 충분히 발달하였습니다. 이 인프라에는 해상 플랫폼, 파이프라인, 저장 시설이 포함됩니다. 이러한 인프라의 존재는 석유 및 가스 자원의 효율적인 채굴과 운송을 가능하게 하기 때문에 업스트림 기업에게 경쟁 우위를 제공합니다.

또한 영국은 북해에서 해양 석유 및 가스 사업의 오랜 역사를 가지고 있으며, 그 결과 석유 및 가스 자원의 탐사 및 생산에 관한 주요 기술적 전문 지식이 개발되었습니다. 업계는 시추 기술, 유층 관리, 생산 최적화 등의 분야에서 지식과 경험을 축적해 왔습니다. 이러한 전문 지식으로 영국은 석유 업스트림 사업에서 우위를 차지하고 있습니다.

세계 에너지 통계 보고서에 따르면 2022년 영국의 원유 생산량은 일량 77만 8,000배럴로 2021년에 비해 거의 11% 감소했습니다. 이 감소의 주된 이유는 북해의 매장량의 감소입니다. 이에 대항하기 위해 영국 기업은 다른 지역의 석유 및 가스 생산을 탐사하기 시작했습니다.

예를 들어, 2023년 2월 영국의 현지 업스트림 기업인 델타 에너지 회사는 라이선스 P2252의 펜사콜라 지역에서 중요한 석유 및 가스 매장지를 발견했다고 발표했습니다. 이 회사는 잠재적인 천연가스 저장층에 300bcf 이상의 천연가스가 존재한다고 발표하였습니다.

따라서 위의 관점에서 예측 기간 동안 영국 업스트림 부문은 석유 및 가스 시장을 독점할 것으로 예상됩니다.

신재생에너지 성장이 시장을 억제할 전망

영국은 저탄소 경제로의 전환이라는 야심찬 목표를 세우고 있습니다. 탄소 가격, 신재생에너지 인센티브, 배출기준 엄격화 등 정부의 정책과 규제는 신재생에너지의 개발과 채용을 촉진하기 위한 것입니다. 이러한 정책은 특히 발전 및 운송과 같은 신재생에너지로 대체 가능한 분야에서 석유 및 가스 수요를 감소시킬 수 있습니다.

게다가 신재생에너지 부문이 계속 확대됨에 따라 엄청난 투자가 이루어질 것으로 예상되며 이로 인해 석유 및 가스 산업에서 자금이 유출되어 기존의 석유 및 가스 프로젝트가 자금을 확보하기 더 어려워 질 수 있습니다. 투자자는 신재생에너지 프로젝트가 장기적으로 재무적으로 실행가능하며 환경적으로도 지속 가능하다고 보고, 신규 석유 및 가스탐사 생산 프로젝트에 대한 투자를 줄일 가능성이 있습니다.

예를 들어 국제재생가능에너지기구에 따르면 2022년 영국의 재생가능에너지 설비 용량은 2021년 대비 7% 이상 증가했습니다. 2022년 재생가능 에너지 설비 용량은 2021년 4,890만 kW에 비해 5,200만 kW를 초과했습니다.

2022년 12월, 베스타스는 영국의 Infinergy가 소유한 Limekiln 프로젝트를 위해 108MW를 주문했다고 발표했습니다. 업무 범위에는 V136-4.5MW 터빈 설치, 공급 및 시운전이 포함되며 약 24기 정도의 터빈이 운용될 예정입니다. 설치 및 시운전은 2024년까지 완료될 예정입니다.

재생 가능 에너지의 성장은 석유 및 가스와 같은 화석 연료 수요 감소로 이어질 수 있습니다. 풍력, 태양광, 수력 등의 재생 가능 에너지원은 비용 경쟁이 격화되고 있어 보다 환경 친화적인 솔루션을 제공할 것으로 여겨지고 있습니다. 이러한 에너지 소비 패턴의 전환은 특히 재생 가능 에너지로의 전환이 용이한 분야에서 석유 및 가스 전체 수요를 감소시킬 수 있습니다.

따라서, 앞서 언급한 바와 같이 재생 가능 에너지원의 증가는 예측 기간 동안 영국 석유 및 가스 시장의 성장을 방해할 것으로 예상됩니다.

영국 석유 및 가스 산업 개요

영국의 석유 및 가스 시장은 단편화되어 있습니다. 이 시장의 주요 기업(순서부동)에는 Shell PLC, BP PLC, TotalEnergies SE, Chevron Corporation, Cadent Gas Ltd. 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월 간 애널리스트 지원

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

소개

2028년까지 시장 규모 및 수요 예측(단위 : 달러)

석유 및 천연가스의 생산량과 2028년까지의 예측

최근 동향과 개발

정부의 규제와 정책

시장 역학

촉진요인

국내 석유 및 가스 생산량

석유 및 가스 인프라 개발 투자

억제요인

신재생에너지 성장

공급망 분석

PESTLE 분석

제5장 시장 세분화

섹터별

업스트림

미드스트림

다운스트림

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 프로파일

Shell PLC

BP PLC

TotalEnergies SE

Chevron Corporation

Cadent Gas Ltd

ESSO UK Limited

BG Group Limited

Valaris PLC

Centrica PLC

Dana Petroleum E&P Limited

제7장 시장 기회와 앞으로의 동향

새로운 석유 및 가스전의 발견

CSM

영문 목차

영문목차

The United Kingdom Oil And Gas Market size is estimated at USD 323.83 billion in 2025, and is expected to reach USD 346.29 billion by 2030, at a CAGR of 1.35% during the forecast period (2025-2030).

Key Highlights

Over the medium term, the country's increasing oil and gas production and increasing investments in oil and gas infrastructure developments are expected to drive the market studied during the forecast period.

On the other hand, the growth of renewable energy technologies and volatility in oil and gas prices due to recent geopolitical developments are expected to restrain the growth of the market studied during the forecast period.

Nevertheless, the discovery of new oil and gas fields across the country is expected to create significant opportunities in the market studied during the forecast period.

UK Oil & Gas Market Trends

Upstream Segment Expected to Dominate the Market

The United Kingdom has significant oil and gas reserves in the North Sea, which have been a major production source for several decades. Although the reserves have declined, they still present a substantial resource base that requires ongoing exploration and production efforts.

The United Kingdom has a well-developed infrastructure for offshore exploration and production in the North Sea. This infrastructure includes offshore platforms, pipelines, and storage facilities. The presence of this infrastructure provides a competitive advantage for upstream companies as it enables efficient extraction and transportation of oil and gas resources.

Moreover, the United Kingdom has a long history of offshore oil and gas operations in the North Sea, resulting in the development of significant technical expertise in the exploration and production of oil and gas resources. The industry has accumulated knowledge and experience in areas such as drilling techniques, reservoir management, and production optimization. This expertise gives the United Kingdom an advantage in upstream activities.

According to the statistical review of world energy, the United Kingdom produced 778 thousand barrels per day of crude oil in 2022, a decrease of almost 11% compared to 2021. The primary reason for this decline is the declining reserves in the North Sea. To counter this, companies in the United Kingdom have started exploring other regions for oiling gas production.

For instance, in February 2023, Delta Energy, a local upstream player in the United Kingdom, announced that they had made a significant oil and gas discovery at the Pensacola region on license P2252. The company claims that the potential natural gas reservoir has more than 300 bcf of natural gas in the reservoir.

Therefore, as per the points mentioned above, the upstream sector in the United Kingdom is expected to dominate the oil and gas market during the forecast period.

Growth of Renewables Expected to Restrain the Market

The United Kingdom has set ambitious targets to transition to a low-carbon economy. Government policies and regulations such as carbon pricing, renewable energy incentives, and stricter emission standards are designed to promote the development and adoption of renewable energy sources. These policies may reduce demand for oil and gas, particularly in sectors where renewable alternatives are feasible, such as power generation and transportation.

Moreover, as the renewable energy sector continues to expand, it attracts significant investment. This can divert capital from the oil and gas industry, making it more challenging for traditional oil and gas projects to secure funding. Investors may view renewable energy projects as more financially viable and environmentally sustainable in the long term, leading to a reduction in investment in new oil and gas exploration and production projects.

For instance, according to the International Renewable Energy Agency, in 2022, the installed renewable energy capacity in the United Kingdom increased by more than 7% compared to 2021. In 2022, the total renewable energy installed capacity crossed 52 GW compared to 48.9 GW in 2021.

In December 2022, Vestas announced that it had received an order for 108 MW for the Limekiln project owned by Infinergy in the United Kingdom. The work scope includes installing, supplying, and commissioning V136-4.5 MW turbines. The total number of turbines is nearly 24. The installation and commissioning is expected to be completed by 2024.

The growth of renewable energy can lead to a decline in demand for fossil fuels, including oil and gas. Renewable energy sources such as wind, solar and hydroelectric power are becoming increasingly cost-competitive and are considered more environment-friendly. This shift in energy consumption patterns can reduce the overall demand for oil and gas, particularly in sectors that can readily switch to renewable alternatives.

Therefore, as per the points discussed above, the increasing adaption of renewable energy sources is expected to hinder the growth of the UK oil and gas market during the forecast period.

UK Oil & Gas Industry Overview

The UK oil and gas market is fragmented. Some of the key players in the market (in no particular order) include Shell PLC, BP PLC, TotalEnergies SE, Chevron Corporation, and Cadent Gas Ltd.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2028

4.3 Crude Oil and Natural Gas Production and Forecast, till 2028

4.4 Recent Trends and Developments

4.5 Government Policies and Regulations

4.6 Market Dynamics

4.6.1 Drivers

4.6.1.1 Domestic Oil and Gas Production

4.6.1.2 Investments in Oil and Gas Infrastructure Development

4.6.2 Restraints

4.6.2.1 Growth of Renewable Energy

4.7 Supply Chain Analysis

4.8 PESTLE Analysis

5 MARKET SEGMENTATION

5.1 Sector

5.1.1 Upstream

5.1.2 Midstream

5.1.3 Downstream

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements