아시아태평양의 전기자동차용 전지 음극 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

Asia Pacific Electric Vehicle Battery Anode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1636507

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

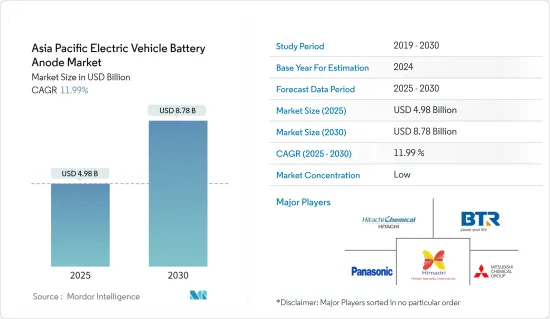

아시아태평양의 전기자동차 전지 음극시장 규모는 2025년 49억 8,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 11.99%로, 2030년에는 87억 8,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

향후 수년간 아시아태평양의 전기자동차용 전지 음극 시장은 전기자동차 보급 확대, 전지 원료 비용의 저하(리튬 이온 전지의 저가격화로 이어짐), 정부의 지원 시책 등의 요인에 의해 성장할 전망입니다.

반대로 원료의 매장량 한계와 공급망 격차 등의 과제는 시장의 확대를 방해할 가능성이 있습니다.

그러나 전지 음극 기술의 진보와 전기자동차의 장기 목표는 시장 진출기업에 큰 기회를 가져다줍니다.

아시아태평양의 주요 진출기업 중 인도는 전기자동차 전지 음극 시장에서 현저한 성장을 이루는 국가로 부상하고 있습니다.

아시아태평양 전기자동차 전지 음극 시장 동향

리튬 이온 전지 부문이 시장을 독점

리튬 이온 전지 산업 초기에 리튬 전지의 주요 시장은 소비자 전자 제품이었으나 세월이 지나면서 현저한 변화가 일어났습니다. 전기자동차(EV) 제조업체가 리튬 이온 전지의 주요 소비자로서 대두해 아시아태평양에서의 EV 판매의 급증이 그 원동력이 되었습니다.

지난 10년간 아시아태평양에서는 특히 자동차 부문에서 리튬 이온 전지의 채택이 급증하고 있습니다. 중국, 인도, 일본, 인도네시아 등 국가에서는 우수한 용량 대 중량비 때문에 리튬 이온 이차 전지의 선호도가 높아지고 있습니다. 또한 EV에 사용되는 리튬 전지는 NOX, CO2 및 기타 온실가스를 배출하지 않으므로 기존의 내연기관(ICE) 차량에 비해 환경 부하가 크게 낮습니다. 이 장점을 인식하고 많은 국가들이 EV의 보급을 촉진하고 보조금과 정부의 이니셔티브를 통해 전기자동차 전지 음극 시장의 개척을 촉진하고 있습니다.

2023년 5월, 전기자동차용 전지의 양극 및 음극 시장에서 유명한 Himadri Speciality Chemical Ltd.는 Sicona Battery Technologies Pty Ltd.에 1,032만 호주 달러의 전략적 투자를 실시해 12.79%의 주식을 확보했다고 발표 했습니다. 시드니에 본사를 둔 Sicona는 리튬 이온(Li-ion) 전지의 음극에 필수적인 기술을 제공하여 이동성 부문과 재생 가능 에너지 저장에 모두 기여합니다.

전기자동차의 보급이 진행됨에 따라 리튬 이온 전지 양극 시장은 크게 성장하고 있습니다. 게다가 음극 기술의 진보가 동시장 확대를 더욱 추진하게 됩니다.

국제에너지기구(IEA)에 따르면 중국의 전지식 전기자동차 판매량은 2023년 540만대에 이르며, 그 95% 이상이 리튬 이온 전지 기술에 의존해 전년 대비 22.7% 증가를 기록하고 있습니다. 이러한 전지 전기자동차 부문의 강력한 성장을 감안할 때, 리튬 이온 전지는 그 명확한 이점으로 아시아태평양 전기자동차 전지 음극 시장에서 큰 점유율을 얻을 것으로 예측됩니다.

2024년 8월, BTR 신재료 그룹은 인도네시아에서 새로운 리튬 이온 전지용 음극재 공장을 가동했습니다. 동사는 이 시설이 완전히 확대되면 중국 이외에서 가장 큰 음극재 생산 기지가 될 것으로 발표하였습니다. 4억 7,800만 달러의 투자를 통한 1기 건설은 연간 8만 톤의 음극재 생산 능력을 기대하고 있습니다. 2024년 말에 시작되는 두 번째 단계에서는 2억 9,900만 달러가 추가 투자되어 시설의 생산량을 다양화하고, 전기차, 소비자용 전자기기용 전지, 에너지 저장 시스템용으로 음극재를 공급하는 것이 목적입니다. 이러한 전략적 움직임은 아시아태평양 EV 전지 음극 시장에서 EV 리튬 이온 전지의 우위를 높이고 있습니다.

리튬 이온 전지 부문의 이러한 진보를 감안하면, 아시아태평양의 전기자동차용 전지 음극재 시장은 향후 수년간 크게 성장할 것으로 예상됩니다.

아시아태평양 시장을 독점하는 인도

파리 협정과 유엔 SDGs의 일환으로 인도 정부는 세계 플랫폼에서 온실가스 배출을 줄이기 위해 노력하고 있습니다. 전기자동차(EV)의 보급을 촉진하고 인도를 EV용 전지 제조의 세계의 거점으로 자리매김하기 위해 인도 정부는 전기자동차 전지와 관련 음극 시장의 진출기업에 리베이트, 인센티브, 수입 양허를 도입했습니다.

2024년 3월 15일, 인도 정부는 전기자동차 제조 계획(SMEC)을 승인했습니다. 이 구상은 신규 그린필드 전기자동차 제조 공장을 설립하는 자동차 제조업체에 수입 관세의 양허를 주는 것입니다. 이 계획에서 제조업체는 연간 8,000대까지 EV를 5년간 15%의 경감 관세로 수입할 수 있습니다. 이 우대 정책은 인가를 받은 지 3년 이내에 자국 내 생산능력을 확립할 것을 조건으로 하고 있습니다. 그 결과, 이러한 개발이 EV용 리튬 이온 전지 기술의 대두를 뒷받침해 인도에서의 음극재의 성장을 직접적으로 가속하고 있습니다.

잠재력과 정부의 강력한 지원으로 인도는 전기자동차 시장을 목표로 하는 기업들에게 뛰어난 제조 기지로 부상하고 있습니다. 예를 들어, Epsilon Advanced Materials는 2024년 9월 미국과 인도에 각각 연산 3만 톤의 공장을 설립할 계획을 발표했습니다. 이들 공장은 중국 외부 최대의 음극재 생산공장이 되어 인도가 전기자동차 전지 음극재의 대규모 공급자로 등극하게 됩니다.

2024년 9월, 전지 재료의 주요 기업인 Epsilon Advanced Materials는 카르나타카 주에도 최첨단 전기자동차 전지 음극재 제조 시설을 설립할 의향을 밝혔습니다. 투자 예정액은 900억 루피(약 106억 달러)로 연간 생산 능력은 9만 톤을 목표로 합니다. 투자 전략은 두 단계로 전개됩니다. Epsilon Group의 매니징 디렉터가 자세히 설명한 바와 같이, 최초 투자액은 400억 루피(약 47억 달러)이고 계속되는 제2단계에서의 추가 투자액은 500억 루피(약 59억 달러)입니다.

2024년 1월, HEG Limited의 자회사에서 LNJ Bhilwara 그룹 산하의 Advanced Carbons Company(TACC)는 매디아 프라데시주 데와스 주 서소다 마을에 흑연 양극 제조 장비를 출시했습니다. 동사는 2022년 이 그린필드 프로젝트에 약 1,850억 루피(약 21억 달러)를 투자했습니다. 100에이커 부지에 퍼져 있는 이 시설은 연간 2만톤의 양극재를 생산하여 에너지 저장과 이동성의 급증하는 수요에 대응할 예정입니다.

2023년 인도 정부는 전기자동차(EV)용 전지 팩의 평균 가격이 13% 크게 하락해 전년부터 139달러/kWh까지 떨어졌습니다고 지적했습니다. 기술의 발전과 제조 효율이 향상됨에 따라 전지 팩 가격은 더욱 감소하고 2025년에는 113달러/kWh, 2030년에는 80달러/kWh까지 하락할 것으로 예상됩니다. 이러한 동향으로 인도에서 리튬 이온 전기자동차 전지 음극 시장의 중요성이 증가하고 있습니다.

이러한 신흥국 시장의 개척에 의해 인도는 향후 수년간, 리튬 이온 전지 음극 시장에서 지배적인 지위를 확립할 것으로 예상됩니다.

아시아태평양 전기자동차용 음극 산업 개요

아시아태평양 전기자동차 전지 음극 시장은 적정 수준으로 나뉘어 있습니다. 시장의 주요 기업(순서부동)에는 BTR New Material Group, Himadri Speciality Chemical Ltd., Hitachi Chemical Company Ltd, Panasonic Holdings Corporation, Epsilon Advanced Materials Pvt. Ltd. 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 범위

시장의 정의

전제조건

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

서문

2029년까지 시장 규모와 수요 예측(단위 : 달러)

최근 동향과 개발

정부의 규제와 시책

시장 역학

촉진요인

전기자동차 보급 확대

유리한 정부 시책

리튬 이온 전지 가격 저하

억제요인

공급망 격차

공급망 분석

산업의 매력 - Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 진입업자의 위협

대체품의 위협 제품 및 서비스

경쟁 기업간 경쟁 관계

투자 분석

제5장 시장 세분화

전지 유형별

리튬 이온

납축전지

기타

재료 유형별

실리콘

흑연

리튬

기타

지역별

중국

인도

일본

말레이시아

인도네시아

태국

베트남

기타 아시아태평양

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 개요

BTR New Material Group Co., Ltd

Shenzhen Dynanonic Co., Ltd.

Mitsubishi Chemical Group Corporation

Hitachi Chemical Company Ltd

Northern Graphite Corporation

Panasonic Corporation

Targray Technology International Inc.

Epsilon Advanced Materials Pvt. Ltd.

Himadri Speciality Chemical Ltd

기타 유력 기업 목록

시장 순위/점유율(%) 분석

제7장 시장 기회와 앞으로의 동향

진행중인 음극재 조사와 진보

CSM

영문 목차

영문목차

The Asia Pacific Electric Vehicle Battery Anode Market size is estimated at USD 4.98 billion in 2025, and is expected to reach USD 8.78 billion by 2030, at a CAGR of 11.99% during the forecast period (2025-2030).

Key Highlights

In the coming years, the Asia Pacific Electric Vehicle Battery Anode Market is poised for growth, driven by factors such as the rising adoption of electric vehicles, decreasing costs of battery raw materials (leading to lower prices for Li-ion batteries), and supportive government policies.

Conversely, challenges like limited raw material reserves and gaps in the supply chain may hinder the market's expansion.

However, advancements in battery anode technologies and ambitious long-term electric vehicle targets present significant opportunities for market players.

Among the key players in the Asia-Pacific region, India stands out as a country poised for notable growth in the electric vehicle battery anode market.

Asia Pacific Electric Vehicle Battery Anode Market Trends

Lithium-ion Battery Segment to Dominate the Market

In the early decades of the lithium-ion battery industry, the primary market for lithium batteries was consumer electronics. However, over the years, a notable shift took place. Electric vehicle (EV) manufacturers emerged as the leading consumers of lithium-ion batteries, driven by surging EV sales in the Asia-Pacific region.

Over the past decade, the Asia-Pacific has seen a meteoric rise in the adoption of lithium-ion batteries, especially in the automotive sector. Countries like China, India, Japan, and Indonesia are increasingly favoring lithium-ion rechargeable batteries due to their superior capacity-to-weight ratio. Moreover, lithium batteries used in EVs do not emit NOX, CO2, or other greenhouse gases, resulting in a significantly lower environmental impact compared to traditional internal combustion engine (ICE) vehicles. Recognizing this advantage, numerous countries are promoting EV adoption and fostering the development of the Electric Vehicle Battery anode Market through subsidies and government initiatives.

In May 2023, Himadri Speciality Chemical Ltd., a prominent player in the EV Battery Cathode and Anode market, announced a strategic investment of AUD 10.32 million in Sicona Battery Technologies Pty Ltd, securing a 12.79 percent stake. Sicona, based in Sydney, offers technology crucial for the anodes (negative electrodes) of lithium-ion (Li-ion) batteries, serving both the mobility sector and renewable energy storage.

As electric vehicle adoption continues to rise, the lithium-ion battery cathode market is poised for substantial growth. Additionally, advancements in anode technologies are set to further propel this market expansion.

According to the International Energy Agency (IEA), battery electric vehicle sales in China hit 5.4 million in 2023, with over 95% relying on Li-ion battery technology, marking a 22.7% increase from the previous year. Given this robust growth in the battery electric vehicle sector, lithium-ion batteries, with their distinct advantages, are projected to capture a significant share of the Asia-Pacific Electric Vehicle Battery Anode Market.

In August 2024, BTR New Material Group inaugurated its new anode materials plant for lithium-ion batteries in Indonesia. The company claims that, once fully expanded, this facility will be the largest anode production site outside of China. The first construction phase, supported by a USD 478 million investment, is designed for an annual production capacity of 80,000 tons of anode material. A second phase, commencing at the end of 2024 with an additional USD 299 million investment, aims to diversify the facility's output, supplying anode materials for electric vehicles, appliance batteries, and energy storage systems. Such strategic moves underscore the growing dominance of EV Li-ion batteries in the Asia-Pacific EV Battery Anode Market.

Given these advancements in the lithium-ion battery sector, the market for anode materials in the Asia-Pacific region's electric vehicle battery market is set for significant growth in the coming years.

India to Dominate the Market in Asia Pacific

As part of the Paris Agreement and the United Nations SDGs, the Government of India has committed to reducing GHG emissions on global platforms. To bolster the adoption of Electric Vehicles (EVs) and position India as a global hub for EV battery manufacturing, the government has introduced rebates, incentives, and import concessions for players in the electric vehicle batteries and associated anode markets.

On March 15, 2024, the Indian government approved the Scheme for Manufacturing of Electric Cars (SMEC). This initiative offers concessional import duties to automakers establishing new greenfield electric vehicle manufacturing plants. Under the scheme, manufacturers can import up to 8,000 EVs annually at a reduced duty of 15% for five years. This concession is granted on the condition that they establish domestic production capabilities within three years of receiving approval. Consequently, these developments are bolstering the rise of Li-ion battery technology for EVs, directly fueling the growth of anode materials in India.

Given its vast potential and robust government backing, India is emerging as a prime manufacturing hub for companies eyeing the electric vehicle market. For instance, in September 2024, Epsilon Advanced Materials announced plans to set up two plants, each boasting a capacity of 30,000 tonnes per annum-one in the United States and the other in India. These facilities are poised to be the largest producers of anode material outside of China, marking India's debut as a large-scale supplier of electric vehicle battery anode material.

In September 2024, Epsilon Advanced Materials, a key player in battery materials, disclosed its intent to set up another cutting-edge EV battery anode material manufacturing unit in Karnataka. With a projected investment of INR 9,000 crore (~USD 10.6 billion), the facility targets an annual production capacity of 90,000 tonnes. The investment strategy unfolds in two phases: an initial INR 4,000 crore (~USD 4.7 billion) infusion, followed by an additional INR 5,000 crore (~USD 5.9 billion) in the second phase, as detailed by Epsilon Group's Managing Director.

In January 2024, the Advanced Carbons Company (TACC), a HEG Limited subsidiary and part of the LNJ Bhilwara group, launched its graphite anode manufacturing unit in Sirsoda village, Dewas district, Madhya Pradesh. The company had earmarked approximately INR 1850 crores (~USD 2.1 billion) for this greenfield project back in 2022. Spread over 100 acres, the facility is poised to churn out 20,000 metric tonnes of anode material annually, meeting the surging demands of energy storage and mobility.

In 2023, the Government of India noted a significant 13% drop in average battery pack prices for electric vehicles (EVs), bringing them down to USD 139/kWh from the previous year. With ongoing technological advancements and enhanced manufacturing efficiencies, projections indicate a further decline in battery pack prices, forecasting USD 113/kWh by 2025 and an ambitious drop to USD 80/kWh by 2030. Such trends underscore the growing significance of the Lithium-ion Electric Vehicle Battery Anode Market in India.

Given these developments, India is poised to emerge as a dominant player in the studied market in the coming years.

Asia Pacific Electric Vehicle Battery Anode Industry Overview

The Asia Pacific Electric Vehicle Battery Anode Market is moderately fragmented. Some of the major players in the market (in no particular order) include BTR New Material Group Co., Ltd., Himadri Speciality Chemical Ltd., Hitachi Chemical Company Ltd, Panasonic Holdings Corporation, and Epsilon Advanced Materials Pvt. Ltd., among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 The Growing Adoption of Electric Vehicles

4.5.1.2 Favorable Government Policies

4.5.1.3 Decreasing Price of Lithium-ion Batteries

4.5.2 Restraints

4.5.2.1 The Supply Chain Gap

4.6 Supply Chain Analysis

4.7 Industry Attractiveness - Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

4.8 Investment Analysis

5 MARKET SEGMENTATION

5.1 By Battery type

5.1.1 Lithium-ion

5.1.2 Lead-acid

5.1.3 Other Technologies

5.2 By Material Type

5.2.1 Silicon

5.2.2 Graphite

5.2.3 Lithium

5.2.4 Other Materials

5.3 Geography

5.3.1 China

5.3.2 India

5.3.3 Japan

5.3.4 Malaysia

5.3.5 Indonesia

5.3.6 Thailand

5.3.7 Vietnam

5.3.8 Rest of Asia Pacific

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 BTR New Material Group Co., Ltd

6.3.2 Shenzhen Dynanonic Co., Ltd.

6.3.3 Mitsubishi Chemical Group Corporation

6.3.4 Hitachi Chemical Company Ltd

6.3.5 Northern Graphite Corporation

6.3.6 Panasonic Corporation

6.3.7 Targray Technology International Inc.

6.3.8 Epsilon Advanced Materials Pvt. Ltd.

6.3.9 Himadri Speciality Chemical Ltd

6.4 List of Other Prominent Companies

6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Ongoing Research and Advancement in Anode Material