영국의 전기자동차 전지 음극 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

United Kingdom Electric Vehicle Battery Anode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1636503

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

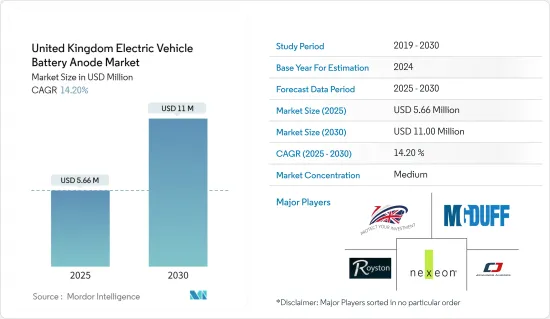

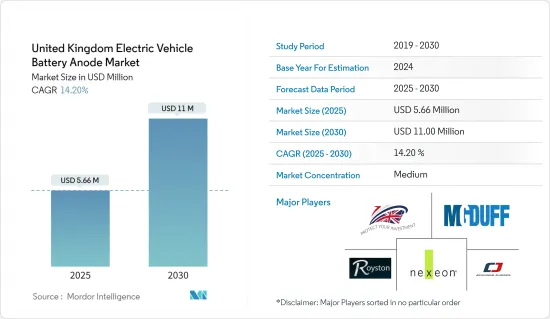

영국의 전기자동차 전지 음극 시장 규모는 2025년에 566만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 14.2%로, 2030년에는 1,100만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

중기적으로는 정부의 야심찬 목표와 이에 대응하는 투자로 전기차의 보급이 진행되고 시장은 그 혜택을 받게 됩니다.

그러나 토지 비용, 원료 물류, 전지 제조에 대한 보조금의 부재와 같은 과제는 시장 확대를 방해할 수 있습니다.

음극 재료의 연구개발이 진행 중이므로 시장은 유망한 성장 가능성이 있습니다.

영국 전기자동차 전지 음극 시장 동향

리튬 이온 전지가 시장을 독점

리튬 이온 전지는 전기자동차(EV) 혁명의 최전선에 있습니다. 뛰어난 에너지 밀도와 긴 수명으로 자동차 산업이 지속 가능한 에너지 솔루션으로 전환하는 가운데 매우 중요한 요소가 되고 있습니다. 영국에서는 리튬 이온 전지 부문의 연구개발이 증가하고 있습니다.

2023년 9월 영국 전기화학 에너지 저장 연구의 최고 기관인 패러데이 연구소는 리튬 이온 개념에 중점을 둔 4개의 주요 전지 연구 프로젝트에 2,100만 달러를 투자할 것이라고 발표했습니다. 이러한 투자는 음극 제조의 미래 수요를 강화하고 있습니다.

또한 영국은 리튬 광상을 이용하는 대기업을 유치하고 있으며, 이러한 움직임은 자국 내 리튬 이온 전지 생산을 강화할 것으로 예상됩니다. 예를 들어, 2023년 6월, 산업 광물의 지도자인 프랑스의 다국적 기업인 Imerys SA는 British Lithium 주식의 80%를 취득했습니다. 이 민간 기업은 운모 화강암에서 전지 리튬을 지속적으로 추출하는 최전선에 있습니다. 양사의 제휴는 영국 최초의 전지 등급 탄산 리튬의 종합적인 생산 회사를 설립하는 것을 목표로 합니다.

역사적으로 리튬 이온 전지의 가격이 급락함에 따라 관련 부품, 특히 음극 수요가 급증하고 있습니다. Bloomberg NEF에 따르면 2023년 리튬 이온 전지의 평균 가격은 139달러/KWh로 2014년 이후 5배라는 엄청난 가격 하락을 기록했습니다. 가격 하락으로 인한 신속한 변화는 음극 시장의 성장에 좋은 징조입니다.

리튬 이온 전지와 음극 생산의 이러한 동향을 감안할 때, 인도의 전기자동차 전지 음극 시장은 향후 수년간 성장할 잠재력을 갖추고 있습니다.

전기차 보급을 위한 정부의 지원

영국 정부는 2050년까지 순 탄소 배출량을 0으로 하는 야심찬 목표를 내걸고 있으며, 특히 운송 부문에서의 배출 감축에 중점을 두고 있습니다. 에너지안보 및 넷제로부에 따르면 자국 내 운수부문은 온실가스 배출량의 약 29.1%를 차지하며 다양한 부문 중에서 가장 큰 배출원이 되고 있습니다. 이러한 배경에서 영국이 전기자동차를 추진함으로써 향후 몇 년간 전지 부품, 특히 음극에 대한 수요가 높아질 것으로 예상됩니다.

예를 들어 2024년 1월 정부는 자동차 제조업체를 대상으로 하는 제로 방출 차량(ZEV) 의무화를 도입했습니다. 이 이니셔티브는 소비자에게 전기자동차 옵션을 넓히는 동시에 제조업체에게 확실성을 제공하는 것을 목표로 합니다.

게다가 이 의무화는 제조업체의 제로 배출 차량(ZEV) 판매 비율을 단계적으로 끌어올리는 것을 규정하고 있습니다. 2024년에 22%라는 목표로 시작하여 2030년까지 80%, 2035년까지 100%를 목표로 하고 있습니다. 이러한 단계적 목표를 달성함으로써 예측 기간 동안 전기자동차 전지와 그 부품(양극 등) 수요가 대폭 증가하게 됩니다.

또한 영국에서는 전기자동차 보급의 동향이 두드러집니다. 국제에너지기구의 데이터에 따르면 2023년 동국의 전기자동차 판매대수는 45만대에 달하고, 전년 대비 21.62%의 대폭 증가를 기록했습니다. 이러한 추세를 근거로 동국의 전기차 수요는 더욱 성장하고 양극시장도 상승할 가능성이 높습니다.

결론적으로 현재의 동향과 예측을 바탕으로 영국의 전기자동차 전지 음극 시장은 당분간 상승할 것으로 예상됩니다.

영국 전기자동차 전지 음극 산업 개요

영국 전기자동차 전지 음극 시장은 부분 통합되어 있습니다. 주요 기업(순서부동)으로는 UK Anodes LTD, Jennings Anodes, MG Duff International Ltd, Royston Lead, Nexeon 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 범위

시장의 정의

전제조건

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

서문

2029년까지 시장 규모와 수요 예측(단위 : 10억 달러)

최근 동향과 개발

정부의 규제와 시책

시장 역학

촉진요인

전기차 도입을 지원하는 정부의 시책

리튬 이온 전지 가격 저하

성장 억제요인

유럽 대륙 내 전지 제조용 원료와 관련 자원 부족

공급망 분석

PESTLE 분석

투자 분석

제5장 시장 세분화

전지 유형

납축전지

리튬 이온 전지

기타 전지 유형

재료

흑연

실리콘

기타

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 개요

UK Anodes LTD

Jennings Anodes

MG Duff International Ltd

Royston Lead

Nexeon Ltd

Tata Group

DKL Metals Ltd

Impalloy Ltd.

Nextrode

Phillips 66

제7장 시장 기회와 앞으로의 동향

음극재 연구개발

CSM

영문 목차

영문목차

The United Kingdom Electric Vehicle Battery Anode Market size is estimated at USD 5.66 million in 2025, and is expected to reach USD 11.00 million by 2030, at a CAGR of 14.2% during the forecast period (2025-2030).

Key Highlights

Over the medium term, the increasing adoption of electric vehicles due to the government's In the medium term, the market is poised to benefit from the rising adoption of electric vehicles, spurred by the government's ambitious targets and corresponding investments.

However, challenges such as land costs, logistics for raw materials, and the absence of subsidies for battery manufacturing may hinder the market's expansion.

Ongoing research and development in anode materials present promising growth avenues for the market.

United Kingdom Electric Vehicle Battery Anode Market Trends

Lithium Ion Batteries to Dominate the Market

Lithium-ion batteries are at the forefront of the electric vehicle (EV) revolution. Their superior energy density and extended life cycle make them pivotal as the automotive industry pivots towards sustainable energy solutions. In the United Kingdom, research and development in the lithium-ion battery sector is gaining momentum.

In September 2023, the Faraday Institution, the United Kingdom's premier institute for electrochemical energy storage research, announced a USD 21 million investment spread across four key battery research projects, with a focus on lithium-ion initiatives. These investments are poised to bolster future demand for anode manufacturing.

Furthermore, the United Kingdom is drawing in major players to tap into its lithium deposits, a move anticipated to bolster domestic lithium-ion battery production. For example, in June 2023, French multinational Imerys S.A., a leader in industrial minerals, secured an 80% stake in British Lithium. This private firm is at the forefront of sustainably extracting battery-grade lithium from mica granite. Their collaboration aims to set up the UK's first integrated producer of battery-grade lithium carbonate.

Historically, as the prices of lithium-ion batteries have plummeted, the demand for related components, notably anodes, has surged. Bloomberg NEF reported that in 2023, the average price of lithium-ion batteries was USD 139 USD/KWh, marking a staggering fivefold price drop since 2014. This swift adoption, driven by falling prices, bodes well for the anode market's growth.

Given these trends in lithium-ion batteries and anode production, India's electric vehicle battery anode market is poised for growth in the coming years.

Government Support to Raise Adoption of Electric Vehicles

The United Kingdom government has set an ambitious goal to achieve net-zero carbon emissions by 2050, with a particular focus on reducing emissions from the transportation sector. According to the Department for Energy Security & Net-Zero, domestic transport accounted for approximately 29.1% of greenhouse gas emissions, making it the largest contributor among various sectors. In light of this, the UK's push for electric vehicles is anticipated to drive up the demand for battery components, especially anodes, in the coming years.

For instance, in January 2024, the government introduced a zero-emission vehicle (ZEV) mandate aimed at car manufacturers. This initiative seeks to provide manufacturers with greater certainty while broadening the selection of electric vehicles for consumers.

Furthermore, the mandate stipulates a gradual increase in the sales proportion of zero-emission vehicles (ZEVs) for manufacturers. Beginning with a target of 22% in 2024, the goal rises to 80% by 2030 and reaches a complete 100% by 2035. Meeting these phased targets is set to significantly boost the demand for electric vehicle batteries and their components, like anodes, during the forecast period.

Additionally, the trend of rising electric vehicle adoption in the United Kingdom is evident. Data from the International Energy Agency reveals that in 2023, the country's electric car sales hit 450,000 units, marking a substantial 21.62% increase from the prior year. Given this trajectory, the demand for electric vehicles in the country is poised for further growth, which in turn is likely to elevate the anode market.

In conclusion, given the current trends and projections, the UK Electric Vehicle Battery Anode Market is set for an upswing in the foreseeable future.

United Kingdom Electric Vehicle Battery Anode Industry Overview

The United Kingdom electric vehicle battery anode market is semi-consolidated. Some of the major players (not in particular order) include UK Anodes LTD, Jennings Anodes, MG Duff International Ltd, Royston Lead, and Nexeon.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD billion, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Government policies supporting adoption of electric vehicles

4.5.1.2 Declining Lithium-ion Battery Prices

4.5.2 Restraints

4.5.2.1 Lack of raw materials and associated resources on the European continent for manufacturing batteries

4.6 Supply Chain Analysis

4.7 PESTLE Analysis

4.8 Investment Analysis

5 MARKET SEGMENTATION

5.1 Battery Type

5.1.1 Lead Acid Batteries

5.1.2 Lithium-ion Batteries

5.1.3 Other Battery Types

5.2 Material

5.2.1 Graphite

5.2.2 Silicon

5.2.3 Others

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements