유럽의 전기자동차 전지 음극 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Europe Electric Vehicle Battery Anode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1636506

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

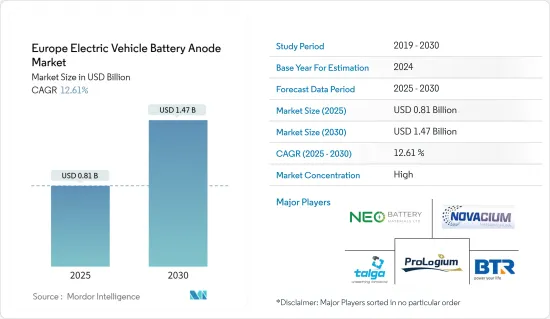

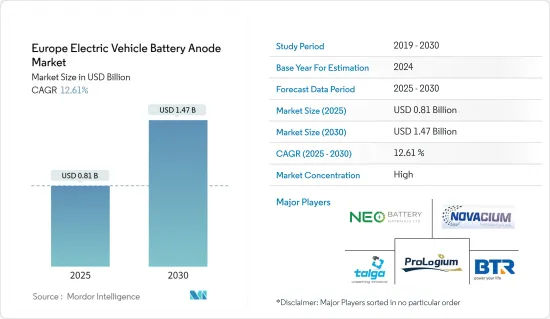

유럽의 전기자동차 전지 음극 시장 규모는 2025년에 8억 1,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 12.61%로, 2030년에는 14억 7,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

향후 몇 년간 유럽의 전기자동차 전지 음극 시장은 전기자동차 보급 확대, 전지 원료의 비용 저하(리튬 이온 전지 가격 하락으로 이어질 수 있음), 정부의 지원 시책에 견인되어 성장이 예상됩니다.

반대로, 원료 매장량 한계와 공급망 격차 등의 과제는 유럽의 전기자동차용 전지 음극 시장의 성장을 방해할 가능성이 있습니다.

그러나, 전지 음극 기술의 발전과 전기자동차의 장기 목표는 유럽 전기자동차 전지 음극 시장의 진출기업에 큰 기회를 주고 있습니다.

유럽의 주요 진출기업 중 프랑스는 유럽 전기자동차 전지 음극 시장에서 현저한 성장을 이룰 것으로 예상됩니다.

유럽 전기자동차 전지 음극 시장 동향

리튬 이온 전지 부문이 시장을 독점

리튬 이온 전지 산업의 초기에는 소비자용 전자 기기가 주요 시장이었습니다. 그러나 시간이 지남에 따라 전기자동차(EV) 제조업체는 리튬 이온 전지의 주요 소비자로 부상했습니다. 이 EV 부문에서 리튬 이온 전지 수요 증가는 전지 음극 재료 시장을 강화했습니다.

지난 10년간 유럽에서는 특히 자동차 부문에서 리튬 이온 전지의 채택이 급증하고 있습니다. 프랑스, 영국, 독일, 이탈리아, 스페인 등 국가에서는 우수한 용량 대 중량비로 인해 리튬 이온 이차 전지 선호도가 높아지고 있습니다. 게다가 EV에 탑재되는 리튬 전지는 NOX, CO2, 기타 온실가스를 배출하지 않기 때문에 기존의 내연기관(ICE) 차량에 비해 환경 부하가 크게 낮습니다. 이러한 장점을 바탕으로 유럽의 여러 국가는 리튬 이온 기술 주도의 EV를 적극적으로 추진하고 보조금과 정부의 이니셔티브를 통해 전기자동차 전지 음극 시장의 개척을 촉진하고 있습니다.

Bloomberg는 2023년 전기자동차(EV)에 사용되는 리튬 이온 전지 팩의 세계 평균 가격이 전년 대비 13% 감소한 139달러/kWh로 하락했다고 보도했습니다. 이 하락은 이전 가격 상승 추세를 따릅니다. 지속적인 기술 진보와 생산 효율성 향상으로 인해 가격은 앞으로도 하락 기조를 지속할 것으로 예상됩니다. 예측에 따르면 2025년에는 113달러/kWh로 내려가고, 2030년에는 80달러/kWh까지 더욱 급락합니다. 이러한 동향은 예측 기간 동안 유럽 전기자동차 전지 음극 시장에서 리튬 이온 전지 부문의 우위를 강화합니다.

국제에너지기구(IEA)에 따르면 리튬 이온 전지 기술을 주로 이용하는(공유 95% 이상) 영국의 전기자동차 판매 대수는 2022년 37만대에서 2023년 45만대에 이릅니다. 이러한 전기자동차 부문의 견고한 성장을 감안할 때, 리튬 이온 전지는 그 명확한 이점으로 인해 유럽의 전기자동차 전지 음극 시장에서 큰 점유율을 얻을 것으로 예상됩니다.

2024년 6월, Stora Enso와 Altris는 유럽에서 지속가능한 전지 가치사슬과 공급망을 수립하기 위한 제휴를 발표했습니다. 양사의 제휴는 Stors Enso의 경질 탄소 솔루션인 Lignode를 Altris의 나트륨 이온 전지 셀의 음극재로 통합하는 데 중점을 둡니다. 이 전지는 주행용 및 거치형 전원 저장용으로 설계되었습니다. Stora Enso가 설명하는 Lignode는 펄프 제조 재료인 리그닌 기반 지속가능한 경질 탄소입니다. 이 새로운 음극 재료는 리튬 이온 전지와 나트륨 이온 전지 모두와 호환되며, 기존의 음극 솔루션에 비해 보다 지속가능한 옵션입니다.

이러한 신흥국 시장의 개발을 고려하면, 향후 몇 년간 리튬 이온 전지 부문이 유럽의 전기자동차용 전지 음극 시장을 독점할 것이 확실시되고 있습니다.

유럽 전기자동차 전지 음극 시장을 독점하는 프랑스

선진국의 대표격인 프랑스는 최근 온실가스 배출량의 대폭 절감이라는 엄청난 과제에 당면하고 있습니다. 신재생에너지원을 에너지믹스에 통합하는 것 외에 프랑스는 기후 변화와의 싸움에서 중요한 전략으로 자동차 배출에 대한 노력을 우선하고 있습니다. 이 초점은 EV용 전지 음극 시장의 진출기업에 유리한 기회를 가져왔습니다. 수많은 외국 기업들이 프랑스로 진출하여 지속적으로 제조 능력을 확대하고 있습니다.

2024년 10월 14일, Paris Motor Show에서 리튬 세라믹 전지 기술 혁신의 최고 선두주자인 ProLogium Technology가 100% 실리콘 복합 음극을 채용한 세계 최초의 EV용 전지를 발표했습니다. 이 획기적인 전지는 단 8.5분만에 충전할 수 있습니다. 이러한 진보는 EV용 전지의 음극 재료의 기술 혁신에 적극적으로 노력하고 있는 유럽의 음극 시장이 급성장하고 있음을 뒷받침하고 있습니다.

2024년 5월, 청정 에너지 기술 기업인 AnteoTech는 유명 전기자동차 제조업체가 동사의 전지 음극 기술을 프로토타입 전지에 채용한다고 밝혔습니다. 스트라스부르에서 개최된 제14회 국제선진자동차전지회의(AABC)에서 AnteoTech는 EV1의 프로젝트 관리팀과의 회의를 포함해 전지 제조업체와 회담을 실시했습니다. 세계 전기자동차 제조업체인 EV1은 차량에 AnteoTech XTM 기술의 통합을 평가했습니다. AnteoTech는 EV1이 Anteo XTM이 투입 비용을 줄일 뿐만 아니라 독자적인 음극 성능을 향상시킬 수 있음을 확인했다고 강조합니다.

2024년 8월, 실리카와 실리콘을 기반으로 하는 음극 재료의 녹색 엔지니어링에 주력하는 프랑스 자회사인 Novacium SAS는 전지 혁신에서 매우 중요한 이정표에 도달했습니다. 흑연과 정제된 3세대(GEN3) 실리콘계 음극을 결합한 동사의 최신 전지는 4,030 mAh 이상의 용량을 달성했으며 이는 18650 Batteries의 세계 기록 4,095mAh에 육박합니다. 이 위업으로 Novacium SAS는 4,000mAh를 초과하는 1만 8,650개의 전지용량을 보고한 세계 3개 기업 중 1개가 되었습니다. 이러한 이정표는 프랑스 EV 전지 음극재 시장 전망을 강화하는 것입니다.

국제에너지기구(IEA)의 데이터에 따르면 2023년 프랑스 전기차 판매량은 47만대에 달하며 2022년 34만대에서 증가하며 95% 이상이 리튬 이온 전지 기술에 의존하고 있습니다. 이러한 전기자동차 부문의 급성장을 감안할 때, 리튬 이온 전지는 그 명확한 이점 때문에 프랑스 전기자동차 전지 음극 시장에서 상당한 점유율을 차지합니다.

그 결과, 이러한 신흥국 시장의 개척에 의해 프랑스는 향후 수년간, 유럽의 전기자동차용 음극 시장에서 매우 중요한 위치를 차지하게 됩니다.

유럽 전기자동차 전지 음극 산업 개요

유럽 전기자동차 전지 음극 시장은 적정 수준으로 통합되어 있습니다. 시장의 주요 기업(순서부동)에는 BTR New Material Group, Novacium SAS, ProLogium Technology, Talga Group, NEO Battery Materials Ltd 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 범위

시장의 정의

전제조건

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

서문

2029년까지 시장 규모와 수요 예측(단위 : 달러)

최근 동향과 개발

정부의 규제와 시책

시장 역학

촉진요인

전기자동차 보급 확대

유리한 정부 시책

리튬 이온 전지 가격 저하

억제요인

공급망 격차

공급망 분석

산업의 매력 - Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 진입업자의 위협

대체품의 위협 제품 및 서비스

경쟁 기업간 경쟁 관계

제5장 시장 세분화

전지 유형별

리튬 이온

납축전지

기타

재료 유형별

실리콘

흑연

리튬

기타

지역별

프랑스

영국

독일

스페인

이탈리아

북유럽 국가

기타 유럽

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 개요

BTR New Material Group Co., Ltd

Novacium SAS

ProLogium Technology Co., Ltd

Talga Group

NEO Battery Materials Ltd

IPCEI European Battery Innovation

Vianode

Epsilon Advanced Materials Pvt. Ltd.

Altech Batteries Ltd

기타 유력 기업 목록

시장 순위/점유율(%) 분석

제7장 시장 기회와 앞으로의 동향

진행중인 음극재 조사와 진보

CSM

영문 목차

영문목차

The Europe Electric Vehicle Battery Anode Market size is estimated at USD 0.81 billion in 2025, and is expected to reach USD 1.47 billion by 2030, at a CAGR of 12.61% during the forecast period (2025-2030).

Key Highlights

In the coming years, the Europe electric vehicle battery anode market is poised for growth, driven by the rising adoption of electric vehicles, decreasing costs of battery raw materials (leading to lower prices for Li-ion batteries), and supportive government policies.

Conversely, challenges such as limited raw material reserves and gaps in the supply chain may hinder the growth of the Europe electric vehicle battery anode market.

However, advancements in battery anode technologies and ambitious long-term targets for electric vehicles present significant opportunities for players in the European electric Vehicle Battery Anode Market.

Among the key players in Europe, France is set to experience notable growth in the Europe electric vehicle battery anode market.

Europe Electric Vehicle Battery Anode Market Trends

Lithium-ion Battery Segment to Dominate the Market

In the early days of the lithium-ion battery industry, consumer electronics were the primary market. However, over time, electric vehicle (EV) manufacturers emerged as the leading consumers of these batteries, driven by a surge in EV sales, particularly in plug-in hybrid electric vehicles (PHEVs). This growing demand for lithium-ion batteries in the EV sector bolstered the market for battery anode materials.

Over the past decade, Europe has seen a meteoric rise in the adoption of lithium-ion batteries, especially in the automotive sector. Countries like France, the UK, Germany, Italy, and Spain are increasingly favoring lithium-ion rechargeable batteries, due to their superior capacity-to-weight ratio. Moreover, lithium batteries in EVs produce no emissions of NOX, CO2, or other greenhouse gases, resulting in a significantly lower environmental impact compared to traditional internal combustion engine (ICE) vehicles. Recognizing this advantage, several European nations are actively promoting lithium-ion technology-driven EVs and fostering the development of the Electric Vehicle Battery Anode Market through subsidies and government initiatives.

Bloomberg reported that in 2023, global average prices for lithium-ion battery packs used in electric vehicles (EVs) fell to USD 139/kWh, a 13% drop from the previous year. This decline followed a trend of rising prices in earlier years. With ongoing technological advancements and improved manufacturing efficiencies, prices are projected to continue their downward trajectory. Forecasts indicate a price drop to USD 113/kWh by 2025, and an even steeper decline to USD 80/kWh by 2030. Such trends bolster the dominance of the lithium-ion battery segment in Europe's Electric Vehicle Battery Anode Market during the forecast period.

According to the International Energy Agency (IEA), in 2023, electric vehicle sales in the United Kingdom, predominantly utilizing lithium-ion battery technology (over 95% share), reached 450,000, up from 370,000 in 2022. Given this robust growth in the battery electric vehicle sector, lithium-ion batteries, with their distinct advantages, are poised to capture a significant share of Europe's Electric Vehicle Battery Anode Market.

In June 2024, Stora Enso and Altris unveiled their partnership aimed at establishing a sustainable battery value and materials chain in Europe. Their collaboration focuses on integrating Stora Enso's Lignode, a hard carbon solution, as an anode material in Altris' sodium-ion battery cells. These cells are designed for both motive and stationary power storage. Lignode, as described by Stora Enso, is a sustainable hard carbon derived from lignin, a pulp manufacturing byproduct. This novel anode material boasts compatibility with both lithium-ion and sodium-ion batteries, marking it as a more sustainable choice compared to conventional anode solutions.

Given these developments, it's evident that the lithium-ion battery segment is set to dominate Europe's Electric Vehicle Battery Anode Market in the coming years.

France to Dominate the Electric Vehicle Battery Anode Market in Europe

France, a leading developed nation, has taken on the monumental challenge of significantly reducing its greenhouse gas emissions in recent years. In addition to integrating renewable energy sources into its energy mix, France has prioritized tackling vehicular emissions as a key strategy in its fight against climate change. This focus has opened up lucrative opportunities for players in the EV battery anode market. Numerous foreign companies have set up operations in France, consistently expanding their manufacturing capabilities.

On October 14th, 2024, at the Paris Motor Show, ProLogium Technology, a frontrunner in lithium ceramic battery innovation, unveiled the world's first EV battery featuring a 100% silicon composite anode. This revolutionary battery can be charged in a mere 8.5 minutes. Such advancements underscore the burgeoning anode market in Europe, with companies actively innovating in EV battery anode materials.

In May 2024, AnteoTech, a clean energy tech firm, revealed that a prominent electric vehicle maker will adopt its battery anode technology in their prototype batteries. At the 14th International Advanced Automotive Battery Conference (AABC) in Strasbourg, AnteoTech held talks with battery manufacturers, including a meeting with EV1's project management team. EV1, a global electric vehicle manufacturer, is evaluating the integration of Anteo XTM technology into its vehicles. AnteoTech highlights that EV1 has confirmed that Anteo XTM not only reduces their input costs but also boosts the performance of their proprietary anode.

In August 2024, Novacium SAS, a French subsidiary focused on green engineering of silica and silicon-based anode materials, reached a pivotal milestone in battery innovation. Their latest batteries, combining graphite with a refined third-generation (GEN3) silicon-based anode, achieved a capacity of over 4,030 mAh. This is nearing the world record of 4,095 mAh for 18650 batteries. With this feat, Novacium SAS becomes one of only three companies worldwide to report 18650 battery capacities surpassing 4,000 mAh. Such milestones bolster the prospects of the EV battery anode material market in France.

Data from the International Energy Agency (IEA) reveals that in 2023, France saw electric vehicle sales hit 470,000, up from 340,000 in 2022, with over 95% relying on Li-ion battery technology. Given this surge in the battery electric vehicle sector, lithium-ion batteries, with their distinct advantages, are poised to command a substantial share of the Electric Vehicle Battery Anode Market in France.

Consequently, these developments position France as a pivotal player in the European Electric Vehicle Battery Anode Market in the coming years.

Europe Electric Vehicle Battery Anode Industry Overview

The Europe Electric Vehicle Battery Anode Market is moderately consolidated. Some of the major players in the market (in no particular order) include BTR New Material Group Co., Ltd., Novacium SAS, ProLogium Technology Co., Ltd, Talga Group, and NEO Battery Materials Ltd, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 The Growing Adoption of Electric Vehicles

4.5.1.2 Favorable Government Policies

4.5.1.3 Decreasing Price of Lithium-ion Batteries

4.5.2 Restraints

4.5.2.1 The Supply Chain Gap

4.6 Supply Chain Analysis

4.7 Industry Attractiveness - Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 By Battery type

5.1.1 Lithium-ion

5.1.2 Lead-acid

5.1.3 Other technology

5.2 By Material Type

5.2.1 Silicon

5.2.2 Graphite

5.2.3 Lithium

5.2.4 Other Materials

5.3 Geography

5.3.1 France

5.3.2 United Kingdom

5.3.3 Germany

5.3.4 Spain

5.3.5 Italy

5.3.6 Nordic countries

5.3.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 BTR New Material Group Co., Ltd

6.3.2 Novacium SAS

6.3.3 ProLogium Technology Co., Ltd

6.3.4 Talga Group

6.3.5 NEO Battery Materials Ltd

6.3.6 IPCEI European Battery Innovation

6.3.7 Vianode

6.3.8 Epsilon Advanced Materials Pvt. Ltd.

6.3.9 Altech Batteries Ltd

6.4 List of Other Prominent Companies

6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Ongoing Research and Advancement in Anode Material