ASEAN의 전기자동차 배터리 애노드 시장 : 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

ASEAN Electric Vehicle Battery Anode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1636502

리서치사:Mordor Intelligence

발행일:2025년 01월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

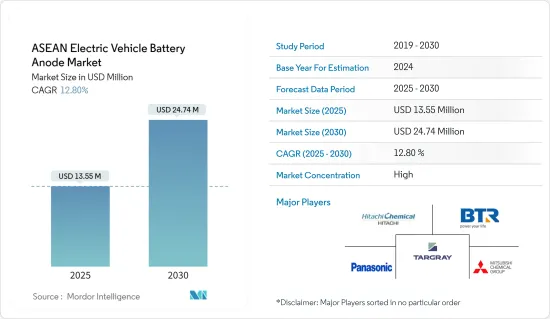

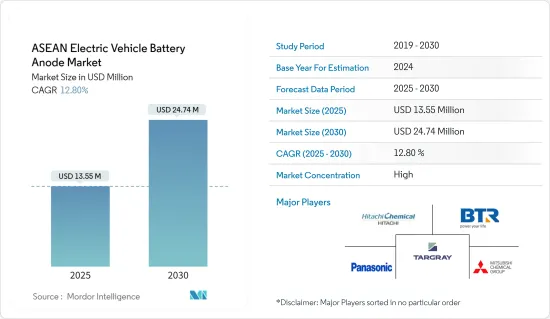

ASEAN의 전기자동차 배터리 애노드 시장 규모는 2025년 1,355만 달러, 2030년 2,474만 달러로 추정되며, 예측 기간(2025-2030년)중 CAGR은 12.8%에 달할 것으로 예측됩니다.

주요 하이라이트

향후 수년간 ASEAN의 전기자동차 배터리 애노드 시장은 전기차 보급 확대, 리튬 이온 배터리 원료 비용 저하, 정부 지원 정책 등의 요인으로 성장할 전망입니다.

그러나 원재료의 매장량에 한계가 있다는 것과 공급 체인의 격차 등의 과제는 시장의 확대를 방해할 가능성이 있습니다.

그러나 배터리 재료의 기술 진보가 진행되고 전기자동차의 장기 목표가 의욕적이기 때문에 ASEAN의 전기자동차 배터리 애노드 시장에는 큰 비즈니스 기회가 기다리고 있습니다.

ASEAN 국가들 중 인도네시아는 전기자동차 배터리 애노드 시장의 주요 기업으로 부상할 것으로 보입니다.

ASEAN의 전기자동차 배터리 애노드 시장 동향

리튬 이온 배터리 부문이 시장을 독점

처음에는, 동남아시아의 리튬 이온 배터리 산업은 주로 가전 분야를 대상으로 했습니다. 이것은 이 지역이 업계 기업 대부분과 리튬 이온 배터리에 필수적인 광물의 본거지이기 때문인 것이 주된 이유였습니다. 그러나 시간이 지남에 따라 큰 변화가 일어났습니다. 전기자동차(EV) 제조업체가 가전부문을 능가하기 시작했고, 리튬이온 전지의 주요 소비자로서 대두해, 납 축전지나 기타 전지 유형을 능가했습니다. 이러한 변화는 ASEAN 국가에서의 EV 판매의 급증과 리튬 이온 배터리와 이와 관련된 전기자동차 배터리 애노드 시장에 대한 투자의 급증이 주요 요인이 되고 있습니다.

인도네시아, 태국, 싱가포르, 베트남 등 국가에서는 지난 수십 년간 특히 자동차 분야에서 리튬 이온 배터리 기술이 급성장해 왔습니다. ASEAN 국가에서는 주로 탁월한 용량 대 중량비로 리튬 이온 이차 전지에 대한 지원이 증가하고 있습니다. 게다가 EV에 탑재되는 리튬 전지는 NOX, CO2, 기타 온실가스를 배출하지 않기 때문에 기존의 내연기관(ICE) 차량에 비해 환경 부하가 크게 낮습니다. 이러한 이점을 바탕으로 ASEAN 국가들은 EV의 보급과 전지 부극의 현지 제조 시장의 개척을 적극적으로 추진하고 있습니다.

필리핀과 베트남의 승용차 판매량은 2023년에는 2022년 대비 각각 16.4%와 2.8% 증가했습니다. 이것은 리튬 이온 전기자동차 부문 기업, 나아가 ASEAN 각국의 전기자동차 배터리 애노드 시장의 선수에게 좋은 징조입니다.

2023년 12월, 태국의 유명한 석유 및 가스 복합 기업인 PTT는 리튬 이온 배터리 생산에 나섰습니다. 이 이니셔티브는 전기자동차 브랜드 'Neta'공급망을 구축하고 태국이 확대하는 그린카 시장을 활용하는 PTT의 광범위한 전략을 따릅니다. PTT 관계자는 합작 파트너인 NV Gotion가 방콕의 남동쪽에 위치한 라용 현에 리튬 이온 배터리 생산 라인을 설립했다고 발표했습니다. 이 시설은 현재 연간 2기가와트의 생산 능력을 자랑하고 있으며, 가까운 미래에는 8기가와트까지 규모를 확대하는 야심찬 계획을 세우고 있습니다.

2024년 7월 인도네시아는 최초의 리튬 이온 EV 배터리 공장 개소를 축하했습니다. 동남아시아 최대의 경제대국이며 세계에서 가장 풍부한 리튬이온 전지광물을 생산하는 인도네시아는 세계의 전기차 공급체인에서 전략적 위치에 자리잡고 있습니다. 한국의 대기업 LG Energy Solution(LGES)과 Hyundai Motor Group의 합작사업인 이 공장은 연간 10기가와트(GWh)라는 경이적인 리튬이온 배터리 셀을 생산할 예정입니다. 이러한 중요한 개발은 ASEAN의 전기자동차 배터리 애노드 시장의 이해 관계자에게 유리합니다.

태국 자동차 연구소(TAI)의 데이터에 따르면 태국에서는 전기차 등록 대수가 현저하게 급증하고 있습니다. 2023년 등록 대수는 17만대에 달하고, 2022년 8만 4,570대에서 크게 급증했습니다. 이러한 자동차의 95% 이상이 리튬 이온 기술을 동력원으로 하고 있다는 점을 감안할 때, 이 성장은 태국의 전기자동차 배터리 애노드 시장에서의 리튬 이온 분야의 우위성을 강조하고 있습니다.

결론적으로, 리튬 이온 배터리 부문이 시장 세분화의 전기자동차 배터리 애노드 시장을 독점한다는 것을 강하게 보여줍니다.

시장을 독점하는 인도네시아

인도네시아는 2030년까지 CO2 배출량을 29% 줄이는 것을 목표로 하고 있으며, 이는 약 3억 300만 톤에 해당합니다. 이산화탄소 배출과 화석연료 의존에 대한 우려가 커지고 있는 가운데 인도네시아는 전기자동차(EV)의 도입을 실행가능한 해결책으로 간주하고 있습니다. 이 시프트는 이 나라의 전기자동차 배터리 애노드 시장에 큰 기회를 가져올 것입니다.

게다가 인도네시아 정부는 전 세계 주요 EV 제조업체들에게 국내 투자를 적극적으로 추진하고 있습니다. 예를 들어, 2024년 5월 발리에서 개최된 세계수 포럼에서 인도네시아의 해사 및 투자 담당 조정상은 Tesla의 CEO가 인도네시아 정부에 EV 배터리 공장의 설치를 제안하고 있음을 밝혔습니다. 이 움직임은 자카르타를 EV 음극재 생산에서 지배적인 지역으로 대두시키려는 야망을 크게 뒷받침할 것으로 보입니다.

2023년 11월, 미국과 인도네시아는 전기자동차(EV) 배터리에 필수적인 금속 거래에 중점을 둔 중요한 광물에 초점을 맞춘 파트너십 구축을 중심으로 협의했습니다.

2024년 9월 인도네시아 외무성은 전기자동차(EV) 배터리 생산에 필요한 중요한 광물의 협력 관계를 확대할 의향을 표명했으며, 이번에는 아프리카 국가와 협력하게 되었습니다. 인도네시아-아프리카 포럼(IAF)에서 외무성 사무국장은 EV 배터리뿐만 아니라 캐소드와 애노드 등의 관련 부품에도 중요한 광물의 엄청난 수요가 있음을 강조했습니다. 외무성은 특히 인도네시아 광업(MIND ID)과 탄자니아와의 리튬에서 활발한 협력 관계를 지적했습니다. 이러한 시도는 인도네시아 전기자동차 배터리 애노드 시장의 강력한 성장 가능성을 시사합니다.

유엔 COMTRADE의 데이터에 의하면, 배터리 광물이 풍부한 나라이면서도, 인도네시아의 리튬 이온 전지의 수입은 급증해, 고정되고 있습니다. 2023년 리튬 이온 배터리 수입액은 2,759만 달러에 이르렀으며, 2022년 2,757만 달러에서 약간 상승했습니다. 이 동향은 인도네시아의 EV 부문에서 리튬 이온 배터리의 왕성한 수요를 부각시키고 인도네시아의 전기자동차 배터리 애노드 제조 능력이 급성장하고 있음을 부각하고 있습니다.

2024년 5월, 호주 Syrah Resources Group은 모잠비크의 바라마 흑연 광업에서 10,000톤의 천연 흑연 미세 분말을 출하했습니다. 이 선적은 인도네시아에 있는 BTR New Energy Materials의 새로운 공장을 위한 것입니다. 인도네시아에서는 EV 배터리 생산과 이와 관련된 애노드재의 인프라 정비가 진행되고 있으며, 이번 출하는 3월에 시험적으로 보낸 컨테이너에 이어집니다. 이 움직임은 Syrah의 다각화 전략에서 매우 중요한 순간일 뿐만 아니라, 천연 흑연과 활성 에노드재(AAM)공급에 있어서의 세계적 리더로서의 지위를 확고하게 하는 것입니다.

이러한 개발을 통해 인도네시아가 아세안의 전기자동차 배터리 애노드 시장에서 발판을 굳히고 있다는 것이 분명합니다.

ASEAN의 전기자동차 배터리 애노드 산업 개요

ASEAN의 전기자동차 배터리 애노드 시장은 반고착화되고 있습니다. 시장의 주요 기업(순부동)에는 BTR New Material Group, Targray Technology International Inc., Mitsubishi Chemical Group, Hitachi Chemical Industry, Panasonic 등이 포함됩니다.

기타 혜택:

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

소개

2029년까지 시장 규모 및 수요 예측(단위: 달러)

최근 동향과 개발

정부의 규제와 정책

시장 역학

성장 촉진요인

전기자동차의 보급 확대

유리한 정부 정책

리튬 이온 전지의 가격 저하

억제요인

공급 체인의 갭

공급망 분석

업계의 매력도 - Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 진입업자의 위협

대체품의 위협 제품 및 서비스

경쟁 기업간 경쟁 관계

제5장 시장 세분화

배터리 유형별

리튬 이온

납축전지

기타 기술

재료 유형별

실리콘

흑연

리튬

기타 재료

지역별

말레이시아

인도네시아

태국

베트남

기타 ASEAN 국가

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

기업 프로파일

BTR New Material Group Co., Ltd

Shenzhen Dynanonic Co., Ltd.

Mitsubishi Chemical Group Corporation

Hitachi Chemical Company Ltd

Northern Graphite Corporation

Panasonic Corporation

Targray Technology International Inc.

Epsilon Advanced Materials Pvt. Ltd.

Volt14 Solutions Pte Ltd

List of Other Prominent Companies

Market Ranking/Share(%) Analysis

제7장 시장 기회와 앞으로의 동향

부극재에 있어서의 진행중의 조사와 진보

JHS

영문 목차

영문목차

The ASEAN Electric Vehicle Battery Anode Market size is estimated at USD 13.55 million in 2025, and is expected to reach USD 24.74 million by 2030, at a CAGR of 12.8% during the forecast period (2025-2030).

Key Highlights

In the coming years, the ASEAN Electric Vehicle Battery Anode Market is poised for growth, driven by factors such as the rising adoption of electric vehicles, decreasing costs of Li-ion battery raw materials, and supportive government policies.

However, challenges like limited raw material reserves and supply chain gaps may hinder the market's expansion.

Yet, with ongoing technological advancements in battery materials and ambitious long-term targets for electric vehicles, significant opportunities await players in the ASEAN Electric Vehicle Battery Anode Market.

Among the ASEAN nations, Indonesia is set to emerge as a leading player in the electric vehicle battery anode landscape.

ASEAN Electric Vehicle Battery Anode Market Trends

Lithium-ion Battery Segment to Dominate the Market

Initially, the lithium-ion battery industry in Southeast Asia primarily served the consumer electronics sector. This was largely due to the region being home to both a majority of industry players and the minerals essential for Li-ion batteries. However, a significant transformation occurred over time. Electric vehicle (EV) manufacturers began to eclipse the consumer electronics sector, emerging as the primary consumers of lithium-ion batteries, outpacing lead-acid and other battery types. This shift was predominantly fueled by surging EV sales in ASEAN countries and escalating investments in Li-ion batteries and the associated Electric Vehicle Battery Anode Market.

In nations such as Indonesia, Thailand, Singapore, and Vietnam, the past few decades have seen a meteoric rise of lithium-ion battery technology, especially in the automotive sector. ASEAN nations are increasingly favoring lithium-ion rechargeable batteries, primarily due to their superior capacity-to-weight ratio. Furthermore, lithium batteries in EVs do not emit NOX, CO2, or any other greenhouse gases, resulting in a significantly lower environmental impact compared to conventional internal combustion engine (ICE) vehicles. Given this advantage, ASEAN nations are actively promoting EV adoption and the development of local battery anode manufacturing markets.

Data from the Organisation Internationale des Constructeurs d'Automobiles highlights a positive trend: both the Philippines and Vietnam saw passenger vehicle sales grow by 16.4% and 2.8% respectively in 2023 compared to 2022. This bodes well for players in the Li-ion Electric Vehicle sector and, by extension, those in the Electric Vehicle Battery Anode Market across ASEAN countries.

In December 2023, PTT, a prominent oil and gas conglomerate from Thailand, ventured into lithium-ion battery production. This initiative aligns with PTT's broader strategy to create a supply chain for its electric vehicle brand, Neta, and capitalize on Thailand's expanding green car market. PTT officials announced that their joint venture partner, NV Gotion, has established a lithium-ion battery production line in Rayong province, southeast of Bangkok. The facility currently boasts a production capacity of 2 gigawatt-hours per year, with ambitious plans to scale up to 8 gigawatt-hours in the near future, directly catering to the surging demand and subsequently fueling the nation's EV Battery Anode Market.

In July 2024, Indonesia celebrated the inauguration of its first Li-ion EV battery plant. As the largest economy in Southeast Asia and home to the world's richest Li-ion battery minerals, Indonesia is strategically positioning itself in the global electric vehicle supply chain. This plant, a joint venture between South Korean titans LG Energy Solution (LGES) and Hyundai Motor Group, is set to produce a staggering 10 Gigawatt hours (GWh) of Li-ion battery cells annually. Such a significant development augurs well for stakeholders in the ASEAN Electric Vehicle Battery Anode Market.

Data from the Thailand Automotive Institute (TAI) reveals a remarkable surge in electric vehicle registrations in Thailand. In 2023, registrations reached 170,000, a significant jump from 84,570 in 2022. Given that over 95% of these vehicles are powered by Li-ion technology, this growth underscores the dominance of the Li-ion segment in Thailand's Electric Vehicle Battery Anode Market.

In conclusion, the evidence strongly indicates that the lithium-ion battery segment is poised to dominate the ASEAN Electric Vehicle Battery Anode Market.

Indonesia to Dominate the Market

Indonesia aims to cut CO2 emissions by 29%, equating to approximately 303 million tons, by the year 2030. With rising concerns over carbon emissions and reliance on fossil fuels, Indonesia views the introduction of electric vehicles (EVs) as a viable solution. This shift is poised to unlock substantial opportunities for the Electric Vehicle Battery Anode Market in the nation.

Moreover, the Indonesian government is actively courting major global EV players to invest domestically. For instance, in May 2024, at the World Water Forum in Bali, Indonesia's coordinating minister for maritime affairs and investment revealed that Tesla's CEO is contemplating a proposal from the Indonesian government to set up an EV battery plant in the nation. This move would significantly bolster Jakarta's ambition to emerge as a dominant player in EV anode production.

In November 2023, discussions between the U.S. and Indonesia centered on forging a partnership focused on critical minerals, with an emphasis on trading metals essential for electric vehicle (EV) batteries.

In September 2024, the Indonesian Foreign Affairs Ministry expressed its intent to expand collaborations on critical minerals for EV battery production, this time engaging with African nations. At the Indonesia-Africa Forum (IAF), the ministry's Director General underscored Indonesia's vast demand for critical minerals, not only for EV batteries but also for related components like cathodes and anodes. The ministry also pointed out an active collaboration in lithium, especially between Mining Industry Indonesia (MIND ID) and Tanzania. These endeavors hint at a robust growth potential for Indonesia's Electric Vehicle Battery Anode Market.

Data from the United Nations COMTRADE reveals that even as a nation rich in battery minerals, Indonesia's imports of Li-ion batteries have surged and remained elevated. In 2023, the value of imported Li-ion batteries reached USD 27.59 million, a slight uptick from USD 27.57 million in 2022. This trend underscores a strong demand for Li-ion batteries in Indonesia's EV sector and highlights the nation's burgeoning capacity for Electric Vehicle Battery Anode manufacturing.

In May 2024, Australia's Syrah Resources Group dispatched 10,000 metric tons of natural graphite fines from its Balama graphite operation in Mozambique. The shipment was destined for BTR New Energy Materials' new plant in Indonesia. As Indonesia ramps up its infrastructure for EV battery production and associated anode materials, this shipment follows a trial container sent in March. This move not only marks a pivotal moment in Syrah's diversification strategy but also cements its position as a global leader in supplying natural graphite and active anode materials (AAM).

Given these developments, it's evident that Indonesia is solidifying its foothold in the ASEAN Electric Vehicle Battery Anode Market.

ASEAN Electric Vehicle Battery Anode Industry Overview

The ASEAN Electric Vehicle Battery Anode Market is semi-consolidated. Some of the major players in the market (in no particular order) include BTR New Material Group Co., Ltd., Targray Technology International Inc., Mitsubishi Chemical Group Corporation, Hitachi Chemical Company Ltd, and Panasonic Corporation, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 The Growing Adoption of Electric Vehicles

4.5.1.2 Favorable Government Policies

4.5.1.3 Decreasing Price of Lithium-ion Batteries

4.5.2 Restraints

4.5.2.1 The Supply Chain Gap

4.6 Supply Chain Analysis

4.7 Industry Attractiveness - Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 By Battery type

5.1.1 Lithium-ion

5.1.2 Lead-acid

5.1.3 Other technology

5.2 By Material Type

5.2.1 Silicon

5.2.2 Graphite

5.2.3 Lithium

5.2.4 Other Materials

5.3 Geography

5.3.1 Malaysia

5.3.2 Indonesia

5.3.3 Thailand

5.3.4 Vietnam

5.3.5 Rest of ASEAN Countries

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 BTR New Material Group Co., Ltd

6.3.2 Shenzhen Dynanonic Co., Ltd.

6.3.3 Mitsubishi Chemical Group Corporation

6.3.4 Hitachi Chemical Company Ltd

6.3.5 Northern Graphite Corporation

6.3.6 Panasonic Corporation

6.3.7 Targray Technology International Inc.

6.3.8 Epsilon Advanced Materials Pvt. Ltd.

6.3.9 Volt14 Solutions Pte Ltd

6.4 List of Other Prominent Companies

6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Ongoing Research and Advancement in Anode Material