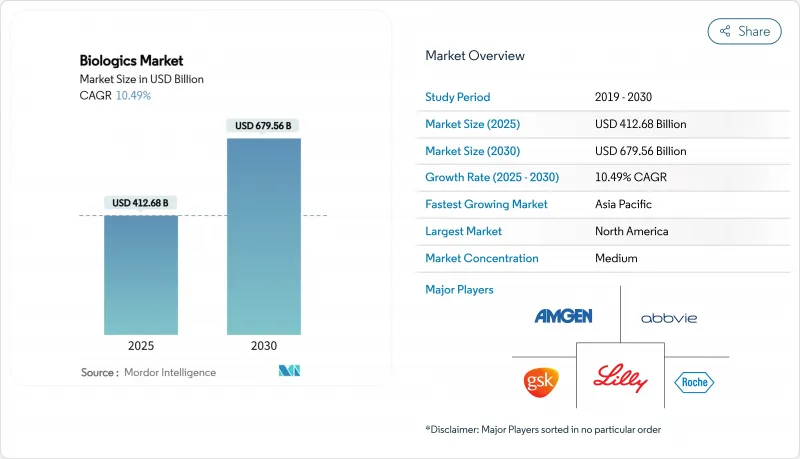

생물제제 시장 규모는 2025년에 4,126억 8,000만 달러, 2030년에는 6,795억 6,000만 달러로 성장할 것으로 예상됩니다.

고정밀 암 치료제, 차세대 단일클론항체, 유전자 기반 치료제에 대한 왕성한 수요가 이 시장 확대에 박차를 가하고 있습니다. 만성 질환의 이환율 증가, 규제 지정 가속화, 벤처 기업의 지속적인 자금 조달로 인해 이러한 복잡한 치료제는 연구 파이프라인에서 일상 진료로 전환하고 있습니다. 2024년 이후, 150억 달러를 넘는 제조 투자가 노스캐롤라, 덴마크, 독일에 새로운 생산 능력을 구축하고, 생산자는 최근 공급 병목 현상을 완화할 수 있습니다. 동시에 이노베이터는 속도와 초기 비용 절감을 양립시키기 위해 연속 관류와 일회용 바이오리액터를 채택하고, 지불자는 지출을 억제하기 위해 바이오시밀러의 채택을 늘리고 있습니다.

암,자가면역질환, 대사성질환은 저분자 의약품으로는 더 이상 대처할 수 없는 복잡한 경로를 나타냅니다. 생물학적 제형의 종양 적용은 면역요법이 더 빠른 치료 라인으로 이동함에 따라 36.54%의 점유율을 차지하며 13.78%의 연평균 복합 성장률(CAGR)을 기록하고 있습니다. 새로운 B 세포 고갈 항체로 치료를 받은 류마티스 관절염 환자는 87%의 플레어 완화를 보고하고 우수한 임상적 대조군을 보였습니다. 당뇨병·비만증 치료제인 GLP-1 효능제가 공급량을 상회했기 때문에 노보놀 디스크는 41억 달러를 새로운 필 피니쉬 스페이스에 투입합니다. 희소질환 치료제에는 희소질병 우대조치가 적용되어 프리미엄 가격이 설정되므로 소규모이면서 수익성이 높은 틈새가 많이 창출되고 있습니다.

FDA의 간소화된 호환성 지침을 통해 바이오시밀러 개발 기업은 분석적 동일성이 입증된 경우 스위칭 테스트를 피할 수 있게 되었습니다. 흑색종 치료제인 lifileucel과 혈우병 B 치료제인 fidanacogene elaparvovec 등 2024년에 승인된 7개의 세포 및 유전자 치료제의 RMAT와 획기적인 라벨로 승인까지의 기간이 단축되었습니다. 중국의 국가 의약품 감독 관리국이 그 과정을 근본적으로 검토한 결과, 아케소는 ivonescimab을 세계 표준을 넘는 데이터로 상시할 수 있게 되었습니다.

노보 노르디스크의 클레이튼 공장 확장과 엘라이 릴리의 위스콘신 공장 확장(30억 달러)에서 볼 수 있듯이 하나의 생물제제 공장에는 10억 달러 이상의 자본이 필요합니다. 일회용 시스템은 제조 시간을 단축하는 것, 빈번한 가방 교환과 특수 메디움은 운전 경비를 증가시킵니다. 엔드 투 엔드 프로그램은 10-15년에 이르며, 시험만으로는 3억 달러가 소요될 수 있으며, 소규모 바이오벤처의 참여는 제한됩니다. CHO 배지, 수지, 무균 주사기 공급 병목은 비용을 밀어 올리고 일정을 위협합니다. 스케일업 중에 편차가 발생하면 제품의 무결성이 저하되므로 엄격한 공정 검증이 필수적이며 비용이 많이 듭니다.

단일클론항체는 2024년 생물제제 시장 규모의 66.43%에 해당하는 2,744억 달러에 기여하여 수십년에 걸친 제조 개량의 혜택을 받고 있습니다. 이 클래스는 종양,자가 면역, 염증 용도 및 그 예측 가능한 약리 작용이 폭넓은 지불자에게 받아들여지고 있습니다. 대조적으로, 유전자 기반의 생물학적 제제는 혈우병 및 유전성 망막 질환에 대한 첫 번째 클래스의 승인에 힘입어 2030년까지 연평균 복합 성장률(CAGR)이 12.32%가 됩니다. 백신은 각국 정부가 유행 대책에 자금을 제공하는 동안 안정적인 기둥으로 계속되는 반면, 유전자 재조합 단백질은 성숙한 바이오시밀러의 가격 하락 압력에 직면하고 있습니다.

파이프라인에 대한 투자는 동종 CAR-T와 줄기세포 제형을 검증한 2024년 7건의 신규 FDA 승인에서 알 수 있듯이 세포 기반 치료법에 기울고 있습니다. ADC와 다특이성 항체는 표적 도메인을 세포독성 또는 면역조절 페이로드와 융합시켜 정밀 종양학을 확장합니다. 현재 250개가 넘는 단백질 공학 프로그램이 반감기, 조직 침투성, 면역원성 프로파일을 최적화하고 있습니다. 이러한 변화는 생물제제 시장의 가치 제안을 강화하고 치료 범위를 확대하며 지속적인 2자리 성장을 야기합니다.

2024년 생물제제 시장 규모의 36.54%는 암 영역이며, 체크포인트 억제제, ADC, CAR-T 요법의 급속한 보급을 반영하여 CAGR은 13.78%로 상승합니다. 자가면역 질환은 차세대 이중특이적 항체가 TNF 억제제에 비해 우수한 질병 대조군을 보이기 때문에 이에 따릅니다. 감염증 생물제제 예방 백신을 넘어 바이러스나 세균의 위협에 대한 노출 후 치료제로 발전합니다.

대사·내분비 질환은 GLP-1 작용제의 적응증이 만성적인 체중관리로 확대되고, 150억 달러를 넘는 세계적인 생산능력 프로젝트가 시동함으로써 규모가 확대됩니다. 안과 영역에서는 한 번의 투여로 지속적인 효과를 가져오는 유전자 치료로부터 이익을 얻을 수 있는 전망입니다. 희귀 질병의 파이프라인은 희소 질병 우대 조치에 의해 박차가 걸리고, 대응 가능한 환자 수영장이 퍼지고 있습니다. 다양한 용도를 겸비함으로써 하나의 치료 영역이 연화되어도 생물제제 시장의 회복력이 강화됩니다.

2024년 생물제제 시장 점유율은 북미가 40.54%를 차지했고 선두를 유지합니다. 이 지역은 150억 달러 이상을 새로운 생산 능력에 투입해 노보놀디스크, 엘라이 릴리, 암젠을 중심으로 한 조사 트라이앵글을 세계적인 허브로 변모시켰습니다. 보급이 성숙함에 따라 CAGR 9.8%로 성장이 완만해지는 것, 바이오시밀러가 정착함에 따라 경쟁의 격렬함이 증가합니다.

아시아태평양은 중국, 일본, 인도가 약사 규제를 개선하고 바이오 의약품 제조에 투자하고 있기 때문에 CAGR 11.54%로 가장 빠르게 성장하고 있습니다. 중국의 승인 일정은 합리화되어 있기 때문에 국내 기업은 구미의 기존 기업에 과제하는 혁신적인 암 치료제를 상시할 수 있습니다. 일본은 세제우대조치와 공적자금을 활용해 트랜스레이셔널리서치를 지원하고 한국 삼성은 CDMO의 능력을 세계에 수출하고 있습니다. 인도는 바이오시밀러와 초기 단계의 프로젝트에서 저비용 인재를 활용하여 이 지역의 발자취를 더욱 크게 하고 있습니다.

성숙한 바이오시밀러 프레임워크와 높은 공중위생비를 배경으로 유럽은 안정된 CAGR 9.2%를 유지. 독일과 스위스는 복잡한 항체의 고가치 생산을 받아들이고 있으며, 아일랜드와 덴마크는 유리한 법인세제로 다국적 기업의 진출을 유치하고 있습니다. 인구동태의 고령화와 만성질환의 만연이 수요를 뒷받침하고, EU 전역에서의 규제가이드의 조화가 시장 진입 마찰을 줄이고 있습니다.

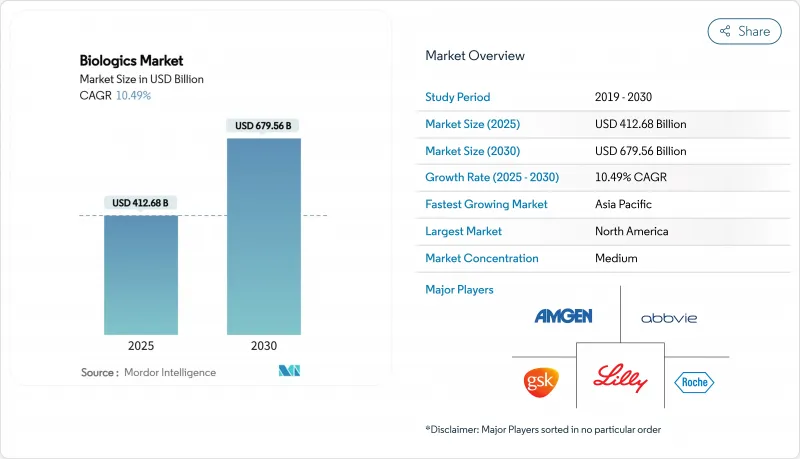

The biologics market size reached USD 412.68 billion in 2025 and is projected to advance to USD 679.56 billion by 2030, reflecting a 10.49% CAGR over the forecast period.

Strong demand for precision oncology agents, next-generation monoclonal antibodies, and gene-based therapeutics steers this expansion. Heightened chronic disease prevalence, accelerated regulatory designations, and sustained venture funding continue to move these complex therapies from research pipelines into routine care. Manufacturing investment exceeding USD 15 billion since 2024 builds new capacity in North Carolina, Denmark, and Germany, positioning producers to ease recent supply bottlenecks. At the same time, innovators adopt continuous perfusion and single-use bioreactors to combine speed with lower upfront costs, while payers increasingly embrace biosimilars to contain spending.

Cancer, autoimmune disorders, and metabolic diseases present complex pathways that small-molecule drugs no longer address fully. Oncology uses of biologics command 36.54% share and post a 13.78% CAGR as immunotherapies move into earlier treatment lines. Rheumatoid arthritis patients treated with novel B-cell depletion antibodies report 87% flare reduction, illustrating superior clinical control. GLP-1 agonists for diabetes and obesity have outstripped supply, prompting Novo Nordisk to commit USD 4.1 billion to new fill-finish space. Rare disease therapies enjoy orphan incentives that allow premium pricing, creating many small but profitable niches.

The FDA's streamlined interchangeability guidance lets biosimilar developers bypass switching studies if analytical sameness is proven. RMAT and breakthrough labels shortened timelines for seven cell and gene therapies cleared in 2024, including lifileucel for melanoma and fidanacogene elaparvovec for hemophilia B. EMA alignment with U.S. policy now delivers simultaneous trans-Atlantic launches, trimming duplication costs. China's National Medical Products Administration has overhauled its process, enabling Akeso to bring ivonescimab forward with data that outperforms global standards.

A single biologics plant demands capital above USD 1 billion, as illustrated by Novo Nordisk's Clayton expansion and Eli Lilly's USD 3 billion Wisconsin site. Although single-use systems reduced build time, frequent bag changeovers and specialized media lift operating expense. End-to-end programs span 10-15 years and can cost USD 300 million in trials alone, limiting small biotech participation. Supply bottlenecks in CHO media, resins, and sterile syringes inflate costs and threaten scheduling. Any deviation during scale-up risks product integrity, making rigorous process validation essential and expensive.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Monoclonal antibodies contributed USD 274.4 billion, equal to 66.43% of the biologics market size in 2024, benefiting from decades of manufacturing refinement. The class spans oncology, autoimmune, and inflammatory uses, and its predictable pharmacology supports broad payer acceptance. In contrast, gene-based biologics post a 12.32% CAGR through 2030, propelled by first-in-class approvals for hemophilia and inherited retinal diseases. Vaccines remain a steady pillar as governments fund pandemic readiness, while recombinant proteins face downward price pressure from mature biosimilars.

Pipeline investment tilts toward cell-based modalities, evidenced by seven fresh FDA approvals in 2024 that validated allogeneic CAR-T and stem cell products. ADCs and multispecific antibodies broaden precision oncology by fusing targeting domains with cytotoxic or immune-modulatory payloads. Over 250 protein-engineering programs now optimize half-life, tissue penetration, and immunogenicity profiles. These shifts collectively raise the biologics market value proposition and expand therapeutic range, underwriting sustained double-digit growth.

Oncology accounted for 36.54% of the biologics market size in 2024 and will rise at a 13.78% CAGR, mirroring rapid uptake of checkpoint inhibitors, ADCs, and CAR-T therapies. Autoimmune conditions follow, as next-generation bispecific antibodies demonstrate superior disease control relative to TNF inhibitors. Infectious disease biologics develop beyond prophylactic vaccines into post-exposure therapeutics against viral and bacterial threats.

Metabolic and endocrine disorders add scale as GLP-1 agonists extend indications to chronic weight management, triggering worldwide capacity projects valued above USD 15 billion. Ophthalmology stands to gain from gene therapy that delivers durable benefit after a single administration. Rare disease pipelines, spurred by orphan incentives, deepen the addressable patient pool. Collectively, diversified applications reinforce resilience in the biologics market even if one therapeutic area softens.

The Biologics Market Report is Segmented by Product (Monoclonal Antibodies, Vaccines, and More), Application (Oncology, Autoimmune & Inflammatory, and More), Source (Mammalian Cell-Culture, and More), Manufacturing Technology (Single-Use Bioreactors, and More), End-User (Pharmaceutical & Biotech Companies, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America sustained leadership with 40.54% biologics market share in 2024, buoyed by robust reimbursement, venture capital depth, and an FDA that expedites breakthrough designations. The region channels more than USD 15 billion into new capacity, transforming the Research Triangle into a global hub anchored by Novo Nordisk, Eli Lilly, and Amgen. Although growth moderates to 9.8% CAGR as penetration matures, competitive intensity rises as biosimilars take hold.

Asia-Pacific delivers the quickest 11.54% CAGR as China, Japan, and India refine regulatory pathways and invest in biomanufacturing. China's streamlined approval timeline allows domestic players to launch innovative oncology biologics that challenge Western incumbents. Japan leverages tax incentives and public funding to support translational research, while South Korea's Samsung Biologics exports CDMO capacity globally. India capitalizes on low-cost talent for biosimilar and early-phase projects, further enlarging the region's footprint.

Europe maintains steady 9.2% CAGR on the back of mature biosimilar frameworks and high public health spending. Germany and Switzerland host high-value production for complex antibodies, whereas Ireland and Denmark entice multinational expansions via favorable corporate tax regimes. Aging demographics and chronic disease prevalence sustain underlying demand, and pan-EU harmonization of regulatory guidance reduces market entry friction.