Targeted Protein Degradation Market by Type [PROTACs (Vepdegestrant, Bavdegalutamide), SERDs (Elacestrant), Molecular Glues (Mezigdomide), LDD, LYTAC/ATAC], Indication (Oncology, Inflammatory), Formulation (Oral), End User - Global Forecast to 2035

상품코드:1801772

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 354 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

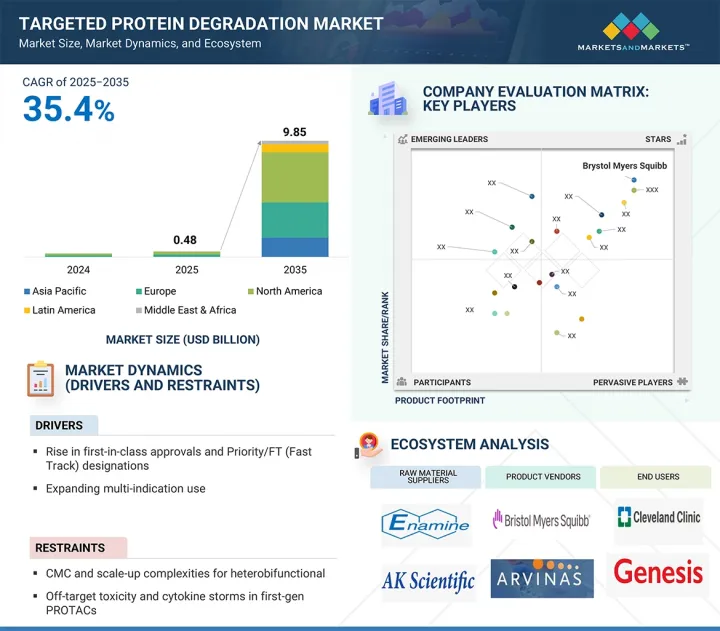

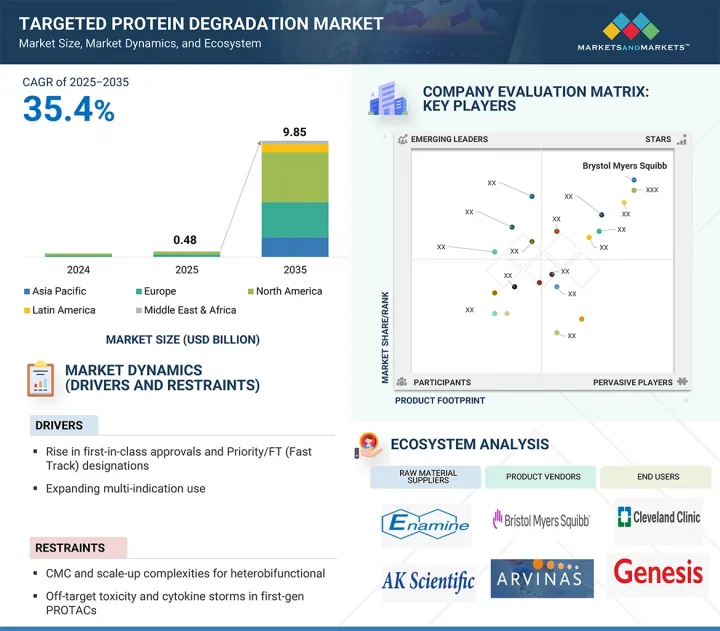

세계의 표적 단백질 분해 시장 규모는 2025년 추정 4억 8,000만 달러에서 2035년까지 98억 5,000만 달러에 이를 것으로 예측되며, 2025-2035년 CAGR은 35.4%를 나타낼 전망입니다.

조사 범위

조사 대상 연도

2024-2035년

기준 연도

2024년

예측 기간

2025-2035년

단위

10억 달러

부문

유형, 치료 적응증, 제형, 최종 사용자, 지역

대상 지역

북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카

표적 단백질 분해 시장 확대는 주로 자본 유입, 대형 제약사 제휴, 그리고 다양한 적응증 확대에 의해 촉진되어 왔습니다. 그러나 CMC(핵산·단백질·단백질 분해) 및 이종이식 의약품(Heterobifunctional)과 지적재산권(IP) 분쟁으로 인한 규모 확장의 복잡성은 시장 성장을 억제할 것으로 예측됩니다.

치료 적응증 부문에서는 암 부문이 2024년에 가장 높은 CAGR을 나타냈습니다.

암 부문은 모든 치료 적응증 부문 중에서 표적 단백질 분해 시장에서 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 이 급성장은 세계의 암 이환율 증가, 과거에는 치료 불가능하다고 여겨지고 있던 질환의 원인이 되는 단백질을 표적으로 하는 치료법에 대한 긴급의 요구에 의한 것입니다. PROTACs와 분자 접착제를 포함한 TPD 기술은 중요한 발암성 단백질을 억제하는 대신 분해함으로써 보다 완전하고 지속적인 치료 효과를 제공하는 획기적인 접근법을 제공합니다. 여러 바이오테크놀러지 기업과 제약 기업이 전립선암, 유방암, 폐암, 혈액암, 고형암 등 암을 적응증으로 한 TPD 후보약의 개발을 진행하고 있습니다. Arvinas, Kymera Therapeutics, Nurix Therapeutics, C4 Therapeutics 등의 업계 리더들은 AR, ER, STAT3, BTK 등 중요한 암 관련 단백질을 표적으로 하는 임상 단계 분해제를 개발하고 있습니다. 또한 주요 제약 기업과의 파트너십과 규제 당국의 지원 증가로 개발 일정이 가속화되고 있습니다.

정밀의료에 대한 주목의 높아짐, 암 이환율의 상승, 기존 요법의 한계에 의해 암부문은 표적 단백질 분해 시장을 독점할 전망입니다. TPD 설계, 바이오마커 통합, 병용요법에 있어서의 지속적인 기술 혁신이 성장을 더욱 촉진하고, 이 시장에서 가장 역동적이고 유망한 응용 분야로서의 암의 역할을 확고한 것으로 보입니다.

최종 사용자별로, 가정 관리 환경 부문은 표적 단백질 분해 시장에서 가장 높은 CAGR을 나타냈습니다.

2024년, 환자 중심의 편리하고 비용 효율적인 치료 옵션에 대한 수요가 증가함에 따라, 재택 케어 환경 부문이 표적 단백질 분해 시장에서 가장 빠르게 성장하는 최종 사용자 부문으로 부상했습니다. 이러한 추세에 기여하는 주요 요인 중 하나는 경구 TPD 제형의 개발의 진행이며, 이는 환자가 집에 있을 때 암이나 자가면역 질환과 같은 복잡한 병리학을 관리할 수 있습니다. 병원에서 투여해야 하는 기존의 생물학적 제형과는 달리, 경구분해제는 빈번한 통원을 필요로 하지 않으며 안전하고 효과적인 치료를 가능하게 하며 환자의 컴플라이언스와 QOL을 크게 향상시킵니다. 재택 치료로의 전환은 원격 환자 모니터링 및 원격 의료 플랫폼과 같은 디지털 건강 기술의 통합을 통해 더욱 향상되고, 의사는 실시간으로 치료 반응을 추적하고 부작용을 관리 할 수 있습니다. 의료 시스템은 병원 부담을 줄이고 치료비를 억제하기 위해 재택 관리 모델을 적극적으로 장려합니다. 많은 표적 단백질 분해제가 후기 임상개발을 거쳐 규제 당국의 승인을 얻고 있기 때문에 재택 케어의 우위성은 강해질 것으로 예측됩니다. 편의성, 확장성, 현대 의료 제공 모델과의 일관성으로 인해, 가정 관리 환경은 진화하는 치료 상황에서 TPD 치료의 중요하고 확장되는 채널이 됩니다.

북미가 2025-2030년 세계의 표적 단백질 분해 시장에서 가장 큰 점유율을 차지할 전망입니다.

북미는 생명공학 혁신의 탄탄한 기반, 유리한 규제 상황, 활발한 투자 활동을 통해 표적 단백질 분해 시장에서 가장 큰 점유율을 차지했습니다. 이 지역에는 Arvinas, Kymera Therapeutics, Nurix Therapeutics, C4 Therapeutics 등 최첨단 분해 기술을 임상 개발로 추진하는 선구적인 TPD 기업이 있습니다. 또한 Bristol Myers Squibb 및 Pfizer와 같은 주요 제약 회사는 공동 연구 및 사내 연구 개발을 통해 TPD 파이프라인을 적극적으로 확대하고 있습니다. 이 지역은 성숙한 의료 인프라, 최상급 학술 연구 기관에 대한 접근, 신규 치료법의 조기 채용으로부터 혜택을 누리고 있습니다.

이 보고서는 세계의 표적 단백질 분해 시장에 대한 조사 분석을 통해 주요 성장 촉진요인과 억제요인, 경쟁 구도, 미래 동향 등의 정보를 제공합니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요한 지견

표적 단백질 분해 시장 개요

북미의 표적 단백질 분해 시장 : 분해약 유형별, 국가별(2030년)

표적 단백질 분해 시장 : 지리적 성장 기회

표적 단백질 분해 시장 : 신흥 시장 vs. 선진 시장

제5장 시장 개요

서론

시장 역학

성장 촉진요인

성장 억제요인

기회

과제

기술 분석

주요 기술

보완 기술

인접 기술

고객사업에 영향을 주는 동향/혼란

가격 설정 분석

ELACESTRANT(ORSERDU)의 가격 설정에 관한 정성적인 인사이트(2024년)

향후 신규 표적 단백질 분해제의 가격 설정에 관한 정성적인 인사이트

ELACESTRANT(ORSERDU)의 상환 시나리오

미국

유럽

밸류체인 분석

생태계 분석

특허 분석

파이프라인 분석

규제 분석

지역별 규제기관, 정부기관, 기타 조직

규제 틀

주요 컨퍼런스 및 이벤트(2025-2026년)

Porter's Five Forces 분석

주요 이해관계자와 구매 기준

투자 및 자금조달 시나리오

표적 단백질 분해 시장에 대한 AI/생성형 AI의 영향

표적 단백질 분해 시장에 대한 미국 관세의 영향(2025년)

서론

주요 관세율

가격의 영향 분석

국가/지역에 미치는 영향

최종 이용 산업에 미치는 영향

제6장 표적 단백질 분해 시장 : 분해약 유형별

서론

분자 접착

MEZIGDOMIDE(CC-92480)

IBERDOMIDE(CC-220)

SERD

ELACESTRANT

GIREDESTRANT(GDC9545)

CAMIZESTRANT(AZD9833)

PROTAC

VEPDEGESTRANT(ARV-471)

LUXDEGALUTAMIDE

BGB-16673

NX-5948

KT-474

LDD/BIDAC

LYTAC/ATAC

AUTAC/ATTEC

제7장 표적 단백질 분해 시장 : 치료 적응증별

서론

종양학

염증성 질환

기타 질환

제8장 표적 단백질 분해 시장 : 제형별

서론

경구 제형

정제

캡슐

주사제

제9장 표적 단백질 분해 시장 : 최종 사용자별

서론

병원 및 전문 클리닉

장기 요양 시설

재택 간호 환경

제10장 표적 단백질 분해 시장 : 지역별

서론

북미

북미의 거시경제 분석

미국

캐나다

유럽

유럽의 거시경제 분석

독일

영국

프랑스

이탈리아

스페인

기타 유럽

아시아태평양

아시아태평양의 거시경제 분석

중국

일본

인도

한국

호주

기타 아시아태평양

라틴아메리카

라틴아메리카의 거시 경제 분석

브라질

멕시코

기타 라틴아메리카

중동 및 아프리카

중동 및 아프리카의 거시경제 분석

GCC 국가

기타 중동 및 아프리카

제11장 경쟁 구도

서론

주요 진입기업의 전략/강점

수익 분석(2028-2030년)

시장 점유율 분석(2030년)

기업 평가 및 재무 지표

브랜드/제품 비교

기업 평가 매트릭스 : 주요 기업(2024년)

기업의 평가 매트릭스 : 스타트업/중소기업(2024년)

경쟁 시나리오

제12장 기업 프로파일

주요 기업

BRYSTOL-MYERS SQUIBB COMPANY

THE MENARINI GROUP

ARVINAS

BEONE MEDICINES

NURIX THERAPEUTICS, INC.

KYMERA THERAPEUTICS, INC.

C4 THERAPEUTICS, INC.

ASTRAZENECA

F. HOFFMANN-LA ROCHE LTD

BAYER AG

CAPTOR THERAPEUTICS

RANOK THERAPEUTICS CO. LTD.

PFIZER INC.

NOVARTIS AG

FOGHORN THERAPEUTICS

기타 기업

MONTE ROSA THERAPEUTICS

BIOTHERYX, INC.

CULLGEN

NEOMORPH

LYCIA THERAPEUTICS

PHOTYS THERAPEUTICS

PLEXIUM, INC.

SEED THERAPEUTICS, INC.

AVILAR THERAPEUTICS, INC.

AUTOMERA

제13장 부록

KTH

영문 목차

영문목차

The global targeted protein degradation market is projected to reach USD 9.85 billion by 2035 from an estimated USD 0.48 billion in 2025, at a CAGR of 35.4% from 2025 to 2035.

Scope of the Report

Years Considered for the Study

2024-2035

Base Year

2024

Forecast Period

2025-2035

Units Considered

Value (USD billion)

Segments

By Type, Therapeutic Indication, Formulation, End User, and Region

Regions covered

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa

The expansion of the targeted protein degradation market has been predominantly fueled by Capital inflows & big-pharma tie-ups, and multi-indication expansion. However, CMC & scale-up complexity for heterobifunctional and IP disputes are expected to restrain market growth.

The oncology segment reported the highest CAGR in the therapeutic indications segment in 2024.

Based on therapeutic indications, the market is categorized into oncology, inflammatory diseases, and other therapeutic indications. Oncology is projected to exhibit the highest CAGR in the targeted protein degradation Market among all therapeutic indication segments. This rapid growth is driven by the increasing global burden of cancer and the urgent need for therapies that can target disease-causing proteins once considered undruggable. TPD technologies, including PROTACs and molecular glue degraders, offer a revolutionary approach by degrading, rather than inhibiting key oncogenic proteins, leading to more complete and durable therapeutic responses. Several biotech and pharmaceutical companies are advancing TPD candidates specifically for oncology indications, including prostate, breast, lung, hematologic, and solid tumors. Industry leaders, such as Arvinas, Kymera Therapeutics, Nurix Therapeutics, and C4 Therapeutics, are developing clinical-stage degraders targeting critical cancer-related proteins like AR, ER, STAT3, and BTK. Additionally, big pharma partnerships and increasing regulatory support are accelerating development timelines.

With a growing focus on precision medicine, rising cancer incidence, and limitations of existing therapies, the oncology segment is poised to dominate the targeted protein degradation market. Continued innovation in TPD design, biomarker integration, and combination therapies will further drive growth and solidify oncology's role as the most dynamic and promising application area in this market.

The homecare settings segment registered the highest CAGR in the targeted protein degradation market by end user.

The targeted protein degradation market is segmented by end users into hospitals & specialty clinics, long-term care facilities, and home care settings. In 2024, the home care settings segment emerged as the fastest-growing end-user segment in the targeted protein degraders (TPD) market, driven by the growing demand for patient-centric, convenient, and cost-effective treatment options. One of the key factors contributing to this trend is the increasing development of oral TPD formulations, which allow patients to manage complex conditions like cancer and autoimmune diseases from the comfort of their homes. Unlike traditional biologics requiring hospital administration, oral degraders enable safe, effective treatment without the need for frequent clinic visits, significantly improving patient compliance and quality of life. The shift toward home-based care is further supported by the integration of digital health technologies, including remote patient monitoring and telehealth platforms, which allow physicians to track treatment response and manage side effects in real time. Healthcare systems are actively encouraging homecare models to reduce hospital burden and control treatment costs. As more targeted protein degraders progress through late-stage clinical development and gain regulatory approval, the dominance of home care settings is expected to strengthen. With their convenience, scalability, and alignment with modern healthcare delivery models, home care environments represent a vital and expanding channel for TPD therapies in the evolving treatment landscape.

North America accounted for the largest share in the global targeted protein degradation market from 2025 to 2030.

North America accounted for the largest share in the targeted protein degradation market, driven by a strong foundation in biotechnology innovation, a favorable regulatory landscape, and significant investment activity. The region is home to several pioneering TPD companies, including Arvinas, Kymera Therapeutics, Nurix Therapeutics, and C4 Therapeutics, which are advancing cutting-edge degrader technologies into clinical development. In addition, major pharmaceutical firms such as Bristol Myers Squibb and Pfizer are actively expanding their TPD pipelines through collaborations and internal R&D. The region benefits from a mature healthcare infrastructure, access to top-tier academic research institutions, and early adoption of novel therapeutic modalities. The US Food and Drug Administration (FDA) has shown increasing recognition of TPD-based therapies, granting designations that facilitate faster development and approval. Furthermore, the growing emphasis on oral and home-based treatments aligns well with healthcare delivery models in North America.

These factors collectively position North America as a key driver of innovation, commercialization, and clinical advancement in the global TPD market, making it the fastest-growing regional segment.

The primary interviews conducted for this report can be categorized as follows:

By Respondent: Supply Side- 70% and Demand Side- 30%

By Designation: Managers- 45%, CXO and Directors- 30%, and Executives- 25%

By Region: North America- 30%, Europe- 30%, Asia Pacific- 30%, Latin America- 5%, and the Middle East & Africa- 5%

Key Companies

Key players in the targeted protein degradation market include Bristol Myers Squibb (US), Arvinas (US), BeiGene (US), Nurix (US), Kymera (US), C4 Therapeutics (US), Stemline Therapeutics (US), AstraZeneca (UK), F. Hoffmann-La Roche Ltd (Switzerland), Bayer (Vividion) (Germany), Captor Therapeutics (Poland), Ranok Therapeutics (US), Pfizer (US), Novartis (Switzerland), and Foghorn Therapeutics (US).

Research Coverage

This research report categorizes the targeted protein degradation market, by type [molecular glue (mezigdomide, Iberdomide), SERDs (Elacestrant, Giredestrant, Camizestrant), PROTAC (Vepdegestrant, Bavdegalutamide, BGB-16673, NX-5948, KT-474), LDD/BiDAC, LYTAC/ATAC, Autophhagy-targeting chimeras] therapeutic indication (oncology, inflammatory diseases, and others), Formulation (oral formulationsand injections), end user (hospitals & speciality clinics, long-term care facility and home care settings) and region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa).

The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the targeted protein degradation market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products, solutions, key strategies, collaborations, partnerships, and agreements. New approvals/launches, collaborations, acquisitions, and recent developments associated with the targeted protein degradation market.

Reasons to buy this report

The report will help market leaders and new entrants by providing them with the closest approximations of the revenue numbers for the overall targeted protein degradation market and its subsegments. It will also help stakeholders better understand the competitive landscape and gain more insights to better position their businesses and make suitable go-to-market strategies. This report will enable stakeholders to understand the market's pulse and provide them with information on the key market drivers, restraints, opportunities, and challenges.

The report provides insights on the following pointers:

Analysis of key drivers (Increasing first-In-class approvals with priority/FT designations, expanding multi-indication use, increasing capital inflows and big-pharma collaborations, and technological advancements in degrader design and discovery) restraints (CMC and scale-up complexity for heterobifunctionals, off-target toxicity and cytokine storms in first-gen PROTACs, and IP disputes), opportunities (Growing adoption of CNS and immunology degraders in clinics, development of next-gen ligases with tissue-selective expression, and increasing NDA filing for innovative degraders), and challenges (Limited ligase expression and strict regulatory guidelines) influencing the growth of the market.

Service Development/Innovation: Detailed insights on upcoming technologies, research & development activities in the targeted protein degradation market

Market Development: Comprehensive information about lucrative markets across varied regions

Market Diversification: Exhaustive information about untapped geographies, recent developments, and investments in the targeted protein degradation market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players. A detailed analysis of the key industry players has been done to provide insights into their key strategies, product launches/ approvals, acquisitions, partnerships, agreements, collaborations, other recent developments, investment and funding activities, brand/product comparative analysis, and vendor valuation and financial metrics of the targeted protein degradation market.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 STAKEHOLDERS

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Objectives of secondary research

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Breakdown of primaries (supply- and demand-side participants)

2.1.2.2 Key objectives of primary research

2.2 MARKET SIZE ESTIMATION

2.2.1 GLOBAL MARKET SIZE ESTIMATION

2.2.1.1 Company revenue analysis (Bottom-up approach)