Global Semiconductor Equipment: Markets, Market Shares and Market Forecasts

상품코드:1473279

리서치사:Information Network

발행일:2026년 02월

페이지 정보:영문 325 Pages

라이선스 & 가격 (부가세 별도)

한글목차

세계의 반도체 업계 판매고는 2023년에 5,268억 달러에 달하며, 업계 사상 최고를 기록한 2022년 합계 5,741억 달러에서 8.2% 감소했습니다. 그러나 2023년 후반에 판매고는 회복했습니다. 실제로 4분기 판매고는 1,460억 달러로, 전년 같은 시기를 11.6%, 2023년 3분기를 8.4% 웃돌았습니다. 또한 2023년 12월 세계 판매고는 486억 달러로, 지난 달보다 1.5% 증가했습니다.

지역별로 보면 유럽은 2023년 연간 매출이 4.0% 증가하며 유일하게 성장한 지역으로 나타났습니다. 일본(-3.1%), 미주(-5.2%), 아시아태평양/기타(-10.1%), 중국(-14.0%) 등 다른 모든 시장은 2023년 연간 매출이 감소했으며, 2023년 12월 월간 매출은 중국(4.7% 증가), 미주(1.8% 증가), 아시아태평양/기타(0.3% 증가)를 기록했습니다. 태평양/기타(0.3% 증가)는 11월 대비 증가했지만, 일본(2.4% 감소), 유럽(3.9% 감소)은 감소했습니다.

2023년에는 몇 가지 반도체 제품 분야가 눈에 띄었습니다. 로직 제품 매출은 2023년 1,785억 달러로 매출 규모가 가장 큰 제품 분야가 되었습니다. 메모리 제품은 총 923억 달러로 매출 2위를 차지했습니다. 마이크로컨트롤러(MCU)는 11.4% 증가한 279억 달러를 기록했습니다. 또한 차량용 IC 매출은 전년 동기 대비 23.7% 증가한 422억 달러로 사상 최대치를 기록했습니다.

세계 경기 둔화와 과잉 지출은 2023년 반도체 공급과잉과 장비 붕괴를 불러일으키는 계기가 되었습니다. 현재 반도체 공장이 확장되고 새로운 반도체 공장이 계획되고 있는 가운데, 생산 능력의 대폭적인 확대가 진행 중입니다.

미국의 자급률을 높이고 아시아에 대한 의존도를 낮추기 위해 국내 제조시설에 500억 달러를 투자하겠다는 바이든 행정부의 추진으로 공급과잉과 생산능력 확대를 유발할 수 있는 다양한 움직임이 시작되었습니다.

세계 반도체 제조장비 시장에 대해 분석했으며, 시장의 기본 구조와 촉진요인 및 최신 상황, 전체적인 시장 규모 동향과 점유율 구조(2012-2023년), 유형별 상세 동향(총 24종), 주요 기업 개요(미국 6개사, 유럽 11개사, 아시아 26개사) 등의 정보를 정리하여 전해드립니다.

웨이퍼 프론트엔드(WFE) 장비 투자액 : 디바이스 최종 제품별(2020-2024년)

세계의 WFE 장비 시장의 시장 점유율 : 상위 5사와 기타 기업(2022년·2023년)

목차

제1장 서론

제2장 반도체 산업의 원동력

서론

파운드리

파운드리 설비 투자의 동향

파운드리의 매출 성장률

파운드리의 시장 점유율

매출 성장률 : 파운드리별

세계의 파운드리/로직 리소그래피의 수요

세계의 파운드리 설비의 수요 : 종류별

TSMC 웨이퍼 가격 : 노드별

파운드리 기술 : 선폭 로드맵

생산능력의 동향 : 선폭별

생산능력의 비율 : 지역별

메모리

DRAM 현재·향후 생산 능력 : 제조업체별

DRAM의 매출·수요 예측 : 용도별

DRAM의 시장 점유율

DRAM 설비 투자

NAND

NAND의 매출·수요 예측 : 용도별

NAND의 시장 점유율

3D NAND의 생산 능력

중국

중국의 반도체 인프라

중국의 반도체 시장

중국의 IC 생산

중국의 IC 소비

중국의 IC 생산/소비 비율

중국의 IC 수입 요건

중국의 IC 수요·공급

중국의 IC Fab의 생산 능력

중국의 IC Fab의 생산 능력 : 지역별

중국의 8인치·12인치 파브와 파운드리

중국의 IC Fab의 생산 능력 : 웨이퍼 사이즈별

중국의 IC Fab의 생산 능력 : 형상별

중국의 IC 생산 : 종류별

제3장 시장·사업 부문·점유율·예측

AMHS(자동 자재관리 장비)의 시장 점유율과 예측

CMP(화학 기계 평탄화)의 시장 점유율과 예측

세정 장비의 시장 점유율과 예측

플라즈마 스트립

스프레이 프로세서

웻 스테이션

박막 형성 장비의 시장 점유율과 예측

ALD(전자층 증착법)

에피택시

MOCVD(유기 화학 기상 증착)

LPCVD(감압 CVD : 비튜브)

LPCVD(감압 CVD : 튜브)

플라즈마 CVD(화학 증착법)

PVD(물리 증착법)

이온 주입 장비의 시장 점유율과 예측

리소그래피 장비의 시장 점유율과 예측

직접 묘화형 전자빔 리소그래피

마스크 제조 리소그래피

스테퍼

산화/확산 장비의 시장 점유율과 예측

포토레지스트 처리(트럭) 장비의 시장 점유율과 예측

RTP(래피드 서멀 프로세스) 장비의 시장 점유율과 예측

플라즈마 에칭 장비의 시장 점유율과 예측측

유전

도체

프로세스 제어장비의 시장 점유율과 예측

리소그래피 계측

박막 계측

웨이퍼 검사와 결함 리뷰

제4장 미국의 반도체 장비 공급업체 : 개요

Applied Materials

시장 분석에서 다루는 사업 분야

기업 개요

재무 지표

Axcelis Technologies

KLA

Lam Research

Mattson Technology

Opto Innovation

기업 개요 : Nanometrics

기업 개요 : Rudolph Technologies

Veeco

제5장 유럽의 반도체 장비 공급업체 : 개요

Aixtron

ASM International

ASML

Carl Zeiss

Camtek

EV Group

LPE

Mycronic

Nova Measuring Instruments9

Oerlikon/ Evatec

Semilab

제6장 아시아의 반도체 장비 공급업체 : 개요

ACM Research

Advantest

AMEC

Avaco

Canon

Canon Anelva

Daifuku

Ebara

Eugene Technology

Hitachi High-Technologies

Hitachi Kokusai Electric

Hwatsing

JEOL

Jusung Engineering

KC Tech

Lasertec

Murata Machinery

Murata Machinery

Nikon

Nippon Sanso

Nissin Ion Equipment

NuFlare Technology

Piotech

PSK

Raintree Scientific Instruments

Screen Semiconductor Solutions

SEMES

SEN

TES

Tokyo Electron

Tokyo Seimitsu

Topcon Technohouse

Toray Engineering

Ulvac

Ushio

Wonik IPS

KSA

영문 목차

영문목차

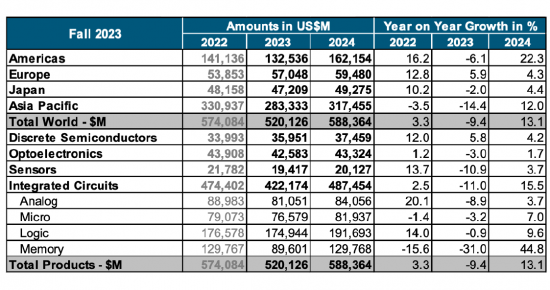

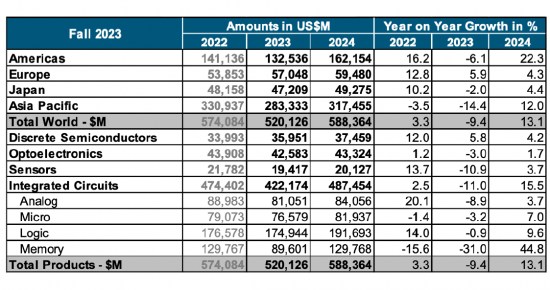

The Semiconductor Industry Association (SIA) announced global semiconductor

industry sales totaled $526.8 billion in 2023, a decrease of 8.2% compared to the 2022

total of $574.1 billion, which was the industry's highest-ever annual total. Sales picked

up during the second half of 2023. In fact, fourth-quarter sales of $146.0 billion were

11.6% more than the total from the fourth quarter of 2022 and 8.4% higher than the

total from third quarter of 2023. And global sales for the month of December 2023

were $48.6 billion, an increase of 1.5% compared to November 2023 total. Monthly

sales are compiled by the World Semiconductor Trade Statistics (WSTS) organization

and represent a three-month moving average. SIA represents 99% of the U.S.

semiconductor industry by revenue and nearly two-thirds of non-U.S. chip firms.

On a regional basis, Europe was the only regional market that experienced

annual growth in 2023, with sales there increasing 4.0%. Annual sales into all other

regional markets decreased in 2023: Japan (-3.1%), the Americas (-5.2%), Asia-

Pacific/All Other (-10.1%), and China (-14.0%). Sales for the month of December 2023

increased compared to November 2023 in China (4.7%), the Americas (1.8%), and Asia

Pacific/All Other (0.3%), but decreased in Japan (-2.4%) and Europe (-3.9%).

Several semiconductor product segments stood out in 2023. Sales of logic

products totaled $178.5 billion in 2023, making it the largest product category by sales.

Memory products were second in terms of sales, totaling $92.3 billion. Microcontroller

units (MCUs) grew by 11.4% to a total of $27.9 billion. And sales of automotive ICs

grew by 23.7% year-over-year to a record total of $42.2 billion.

Global economic slowdowns and capes overspend were catalysts for producing

an oversupply of semiconductors and an equipment meltdown in 2023. A significant

capacity expansion is underway as current fabs expand and new fabs are planned.

A push by the Biden administration to invest $50 billion on domestic

manufacturing facilities to improve US self-sufficiency and reduce reliance on Asia has

initiated a course that will likely result in oversupply and capacity expansion:

Intel

Arizona - Fab 42 expansion for 7nm capacity

Oregon - Fab D1X $3B Mod3 expansion; tools installed Aug. '21 to Feb. '22

New Mexico - $3.5B spend for advanced packaging

Israel - $10B 7nm fab; 2023 production

Ireland - spent additional $7B from 2019-2021 to expand to 7nm

Arizona Foundry $20B for 2 fabs (~35k wspm each) starting production in 2023 and 2024

Malaysia - $7B for advanced packaging fab expansion; 2024 production

TSMC

Fab 18 - 3nm $20B fab expected to be completed in 2023

Arizona Fab -$12B over time; 5nm initial phase to produce 20k wspm starting in 1Q24 with equipment installation commencing in 2H2022

Japan 22 / 28nm fab with Sony; $7B 45k wspm targeting late 2024 production

7/6nm & 28nm fab in Kaohsiung, Taiwan for 2024 production for a reported $10B; phase 1 = 40k wspm for 7nm and 6nm with phase 2 for 28nm

Samsung

Pyeongtaek line 3 (P3) equipment move-in expected to start in April 2022; rst 40-50k wspm 176L 3D NAND line, 130k-140k wspm DRAM and 10k-20k wspm 5nm foundry lines in 2H2022

Pyeongtaek P2 S5-1; 3nm 60k wspm in 2021 & ramp to 120k wspm in 2022

Pyeongtaek P2 S5-2; 3nm 60k wspm targeted production in 2024

U.S. $17B 5nm Foundry fab in Texas; expected 2H2024 production (120k wspm est.)

GlobalFoundries

$4 billion Singapore Module 7H 38k wspm starting wafer production in early-2023; full ramp end of 2023

$1B Malta New York fab expansion of 12,500 wspm; additional fab to double capacity

Spending $1.4B to expand capacity in U.S., Singapore, and Germany

SMIC

100k wspm 28nm & above fab for $8.87B in Shanghai; timing unknown

40k wspm 28nm & above fab in Shenzhen for $2.35B; production starting 2022

UMC

Fab 12A Phase 6 (P6) $3.5B plan for expansion; scheduled for production in 2Q23

Kioxia / Western Digital

Fab 7 in Mie Prefecture, Japan; expected production in late 2022 / early 2023

Kitakami (K2) fab at $18.4B expected completion in early 2023; use of Yokkaichi equip.?

Micron

DRAM - $7B fab in Japan expected to commence production in 2024

SK Hynix

$106B fab complex with 800k wspm capacity and 200k EUV - rst fab completed in 2025 Nanya

DRAM - $10.7B 10nm 110k wspm fab expected to be completed in 2023; production in 2024

Powerchip Semi (PSMC)

$10B 12-inch fab in the Tongluo Science Park; 100k wspm of 1x to 50nm technology will be put into production in stages beginning in 2023

Texas Instruments

RFAB2 - $850M fab coming online in 2H2022 with equipment over next few years

LFAB (acquired from Micron) - spend $3B of capex over time with target of coming online in early-2023 - more details in February at capital management call

North Texas Fab site (option for up to 4 fabs over time) - 1st & 2nd fab construction commencing in 2022 with First fab targeting production in 2025 (70k wspm estimated)

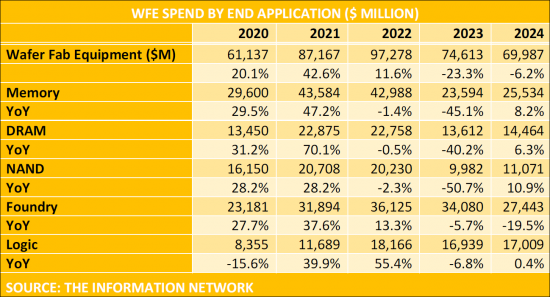

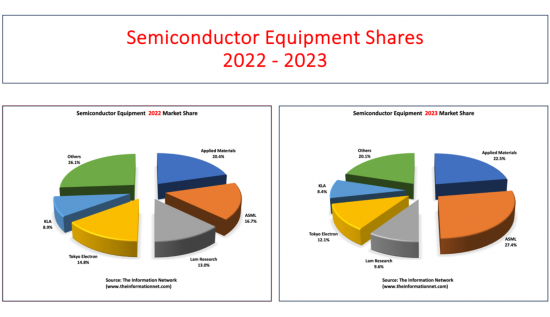

Wafer Front End equipment spend between 2020 and 2024 by device end product is shown below:

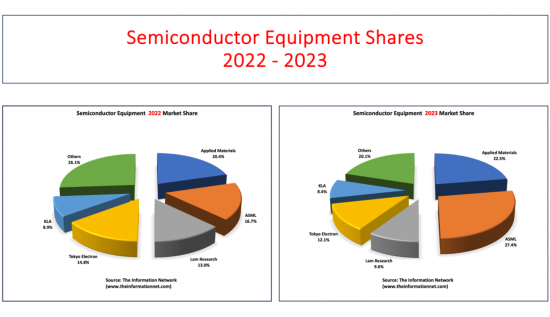

In Figure 1.1 below, we show market shares for the global WFE equipment

market for 2022 and 2023, listing shares for the Top 5 global equipment companies and

the other equipment companies in the market.

Report Coverage

This 325-page report analyzes and forecasts the semiconductor market for 24 different equipment types, including market shares for 2023 by type:

AMHS (Automated Material Handling Systems) Market

CMP (Chemical Mechanical Planarization) Market

Clean Market

Plasma Strip

Spray Processors

Wet Stations

Deposition Market

ALD

Epitaxy

MOCVD

LPCVD (non-tube)

LPCVD (tube)

PECVD

PVD

Ion Implantation Market

Lithography Market

Direct-Write E-Beam Lithography

Mask-Making Lithography

Steppers

Oxidation/Diffusion Market

Photoresist Processing (Track) Market

RTP Market

Plasma Etch Market

Dielectric

Conductor

Process Control Market

Lithography Metrology

Thin-Film Metrology

Wafer Inspection and Defect Review

The report in pdf format profiles 6 U.S., 11 European, and 26 Asian equipment companies.

An Excel File accompanies the report and covers Market Shares of each company by each equipment type between 2012 and 2023.

Driving forces of technology and geopolitics are analyzed and forecast by semiconductor type including China markets.

Table of Contents

Chapter 1. Introduction

Chapter 2. Semiconductor Industry Driving Forces

2.1. Introduction

2.2. Foundries

2.2.1. Foundry Capex Trends

2.2.2. Foundry Revenue Growth

2.2.3. Foundry Market Share

2.2.4. Revenue Growth by Foundry

2.2.5. Global Foundry / Logic Lithography Demand

2.2.6. Global Foundry Equipment Demand By Type

2.2.7. TSMC Wafer Price By Node

2.2.8. Foundry Technology Linewidth Roadmap

2.2.9. Capacity trend by linewidth

2.2.10. Capacity ratio by region

2.3. DRAM

2.3.1. Present and Future Capacity of DRAM by Manufacturer

2.3.2. DRAM Revenue Demand Forecast By Application

2.3.3. DRAM Market Shares

2.3.4. DRAM Capex

2.4. NAND

2.4.1. NAND Revenue Demand Forecast By Applications

2.4.2. NAND Market Shares

2.4.3 3D NAND Capacity

2.5. China

2.5.1. China's Semiconductor Infrastructure

2.5.2. China's Semiconductor Market

2.5.3. China's IC Production

2.5.4. China's IC Consumption

2.5.5. China's IC Production/Consumption Ratio

2.5.6. China's IC Import Requirements

2.5.7. China's IC Supply/Demand

2.5.8. China's IC Fab Capacity

2.5.9. China's IC Fab Capacity by Region

2.5.10. China's 8- And 12-Inch Fabs and Foundries

2.5.11. China's IC Fab Capacity by Wafer Size

2.5.12. China's IC Fab Capacity by Geometry

2.5.13. China's IC Production by Type

Chapter 3. Market Business Sectors Shares and Forecast

3.1. AMHS Market Shares and Forecast

3.2. CMP Market Shares and Forecast

3.3. Clean Market Shares and Forecast

3.3.1. Plasma Strip

3.3.2. Spray Processors

3.3.3. Wet Stations

3.4. Deposition Market Shares and Forecast

3.4.1. ALD

3.4.2. Epitaxy

3.4.3. MOCVD

3.4.4. LPCVD (non-tube)

3.4.5. LPCVD (tube)

3.4.6. PECVD

3.4.7. PVD

3.5. Ion Implantation Market Shares and Forecast

3.6. Lithography Market Shares and Forecast

3.6.1. Direct-Write E-Beam Lithography

3.6.2. Mask-Making Lithography

3.6.3. Steppers

3.7. Oxidation/Diffusion Market Shares and Forecast

3.8. Photoresist Processing (Track) Market Shares and Forecast

3.9. RTP Market Shares and Forecast

3.10. Plasma Etch Market Shares and Forecast

3.10.1. Dielectric

3.10.2. Conductor

3.11. Process Control Market Shares and Forecast

3.11.1. Lithography Metrology

3.11.2. Thin-Film Metrology

3.11.3. Wafer Inspection and Defect Review

Chapter 4. U.S. Semiconductor Equipment Suppliers - Profiles

4.1. Applied Materials

4.1.1. Business Sectors Covered In The Market Analysis Chapter

4.1.2. Company Profile

4.1.3. Company Financials

4.2. Axcelis Technologies

4.1.2. Business Sectors Covered In The Market Analysis Chapter

4.2.2. Company Profile

4.2.3. Company Financials

4.3. KLA

4.3.1. Business Sectors Covered In The Market Analysis Chapter

4.3.2. Company Profile

4.3.3. Company Financials

4.4. Lam Research

4.4.1. Business Sectors Covered In The Market Analysis Chapter

4.4.2. Company Profile

4.4.3. Company Financials

4.5. Mattson Technology

4.5.1. Business Sectors Covered In The Market Analysis Chapter

4.5.2. Company Profile

4.5.3. Company Financials

4.6. Opto Innovation

4.6.1. Business Sectors Covered In The Market Analysis Chapter

4.6.2. Company Profile - Nanometrics

4.6.3. Sectors Covered In The Market Analysis Chapter

4.6.4. Company Profile - Rudolph Technologies

4.6.5. Company Financials

4.7. Veeco

4.7.1. Business Sectors Covered In The Market Analysis Chapter

4.7.2. Company Profile

4.7.3. Company Financials

Chapter 5. European Semiconductor Equipment Suppliers - Profiles

5.1. Aixtron

5.1.1. Business Sectors Covered In The Market Analysis Chapter

5.1.2. Company Profile

5.1.3. Company Financials

5.2. ASM International

5.2.1. Business Sectors Covered In The Market Analysis Chapter

5.2.2. Company Profile

5.2.3. Company Financials

5.3. ASML

5.3.1. Business Sectors Covered In The Market Analysis Chapter

5.3.2. Company Profile

5.3.3. Company Financials

5.4. Carl Zeiss

5.4.1. Business Sectors Covered In The Market Analysis Chapter

5.4.2. Company Profile

5.4.3. Company Financials

5.5. Camtek

5.5.1. Business Sectors Covered In The Market Analysis Chapter

5.5.2. Company Profile

5.5.3. Company Financials

5.6. EV Group

5.6.1. Business Sectors Covered In The Market Analysis Chapter

5.6.2. Company Profile

5.6.3. Company Financials

5.7. LPE

5.7.1. Business Sectors Covered In The Market Analysis Chapter

5.7.2. Company Profile

5.7.3. Company Financials

5.8. Mycronic

5.8.1. Business Sectors Covered In The Market Analysis Chapter

5.8.2. Company Profile

5.8.3. Company Financials

5.9. Nova Measuring Instruments9

5.9.1. Business Sectors Covered In The Market Analysis Chapter

5.9.2. Company Profile

5.9.3. Company Financials

5.10. Oerlikon / Evatec

5.10.1. Business Sectors Covered In The Market Analysis Chapter

5.10.2. Company Profile

5.10.3. Company Financials

5.11. Semilab

5.11.1. Business Sectors Covered In The Market Analysis Chapter

5.11.2. Company Profile

5.11.3. Company Financials

Chapter 6. Asian Semiconductor Equipment Suppliers - Profiles

6.1. ACM Research

6.1.1. Business Sectors Covered In The Market Analysis Chapter

6.1.2. Company Profile

6.1.3. Company Financials

6.2. Advantest

6.2.1. Business Sectors Covered In The Market Analysis Chapter

6.2.2. Company Profile

6.2.3. Company Financials

6.3. AMEC

6.3.1. Business Sectors Covered In The Market Analysis Chapter

6.3.2. Company Profile

6.3.3. Company Financials

6.4. Avaco

6.4.1. Business Sectors Covered In The Market Analysis Chapter

6.4.2. Company Profile

6.4.3. Company Financials

6.5. Canon

6.5.1. Business Sectors Covered In The Market Analysis Chapter

6.5.2. Company Profile

6.5.3. Company Financials

6.5.6. Canon Anelva

6.6.1. Business Sectors Covered In The Market Analysis Chapter

6.6.2. Company Profile

6.6.3. Company Financials

6.7. Daifuku

6.7.1. Business Sectors Covered In The Market Analysis Chapter

6.7.2. Company Profile

6.7.3. Company Financials

6.8. Ebara

6.8.1. Business Sectors Covered In The Market Analysis Chapter

6.8.2. Company Profile

6.8.3. Company Financials

6.9. Eugene Technology

6.9.1. Business Sectors Covered In The Market Analysis Chapter

6.9.2. Company Profile

6.9.3. Company Financials

6.10. Hitachi High-Technologies

6.10.1. Business Sectors Covered In The Market Analysis Chapter

6.10.2. Company Profile

6.1.3. Company Financials

6.10. Hitachi Kokusai Electric

6.11.1. Business Sectors Covered In The Market Analysis Chapter

6.11.2. Company Profile

6.11.3. Company Financials

6.12. Hwatsing

6.12.1. Business Sectors Covered In The Market Analysis Chapter

6.12.2. Company Profile

6.12.3. Company Financials

6.13. JEOL

6.13.1. Business Sectors Covered In The Market Analysis Chapter

6.13.2. Company Profile

6.13.3. Company Financials

6.14. Jusung Engineering

6.14.1. Business Sectors Covered In The Market Analysis Chapter

6.14.2. Company Profile

6.14.3. Company Financials

6.15. KC Tech

6.15.1. Business Sectors Covered In The Market Analysis Chapter

6.15.2. Company Profile

6.15.3. Company Financials

6.16. Lasertec

6.16.1. Business Sectors Covered In The Market Analysis Chapter

6.16.2. Company Profile

6.16.3. Company Financials

6.17. Murata Machinery

6.17.1. Business Sectors Covered In The Market Analysis Chapter

6.17.2. Company Profile

6.17.3. Company Financials

6.18. Murata Machinery

6.18.1. Business Sectors Covered In The Market Analysis Chapter

6.18.2. Company Profile

6.18.3. Company Financials

6.19. Nikon

6.19.1. Business Sectors Covered In The Market Analysis Chapter

6.19.2. Company Profile

6.19.3. Company Financials

6.20. Nippon Sanso

6.20.1. Business Sectors Covered In The Market Analysis Chapter

6.20.2. Company Profile

6.20.3. Company Financials

6.21. Nissin Ion Equipment

6.21.1. Business Sectors Covered In The Market Analysis Chapter

6.21.2. Company Profile

6.21.3. Company Financials

6.22. NuFlare Technology

6.22.1. Business Sectors Covered In The Market Analysis Chapter

6.22.2. Company Profile

6.22.3. Company Financials

6.23. Piotech

6.23.1. Business Sectors Covered In The Market Analysis Chapter

6.23.2. Company Profile

6.23.3. Company Financials

6.24. PSK

6.24.1. Business Sectors Covered In The Market Analysis Chapter

6.24.2. Company Profile

6.24.3. Company Financials

6.25. Raintree Scientific Instruments

6.25.1. Business Sectors Covered In The Market Analysis Chapter

6.25.2. Company Profile

6.25.3. Company Financials

6.26. Screen Semiconductor Solutions

6.26.1. Business Sectors Covered In The Market Analysis Chapter

6.26.2. Company Profile

6.26.3. Company Financials

6.27. SEMES

6.27.1. Business Sectors Covered In The Market Analysis Chapter

6.27.2. Company Profile

6.27.3. Company Financials

6.28. SEN

6.28.1. Business Sectors Covered In The Market Analysis Chapter

6.28.2. Company Profile

6.28.3. Company Financials

6.29. TES

6.29.1. Business Sectors Covered In The Market Analysis Chapter

6.29.2. Company Profile

6.29.3. Company Financials

6.30. Tokyo Electron

6.30.1. Business Sectors Covered In The Market Analysis Chapter

6.30.2. Company Profile

6.30.3. Company Financials

6.31. Tokyo Seimitsu

6.31.1. Business Sectors Covered In The Market Analysis Chapter

6.31.2. Company Profile

6.31.3. Company Financials

6.32. Topcon Technohouse

6.32.1. Business Sectors Covered In The Market Analysis Chapter

6.32.2. Company Profile

6.32.3. Company Financials

6.33. Toray Engineering

6.33.1. Business Sectors Covered In The Market Analysis Chapter

6.33.2. Company Profile

6.33.3. Company Financials

6.34. Ulvac

6.34.1. Business Sectors Covered In The Market Analysis Chapter

6.34.2. Company Profile

6.34.3. Company Financials

6.35. Ushio

6.35.1. Business Sectors Covered In The Market Analysis Chapter

6.35.2. Company Profile

6.35.3. Company Financials

6.36. Wonik IPS

6.36.1. Business Sectors Covered In The Market Analysis Chapter