시험, 검사 및 인증 서비스 시장 : 기회, 성장 요인, 업계 동향 분석, 예측(2025-2034년)

Testing, Inspection and Certification (TIC) Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1871279

리서치사:Global Market Insights Inc.

발행일:2025년 10월

페이지 정보:영문 220 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

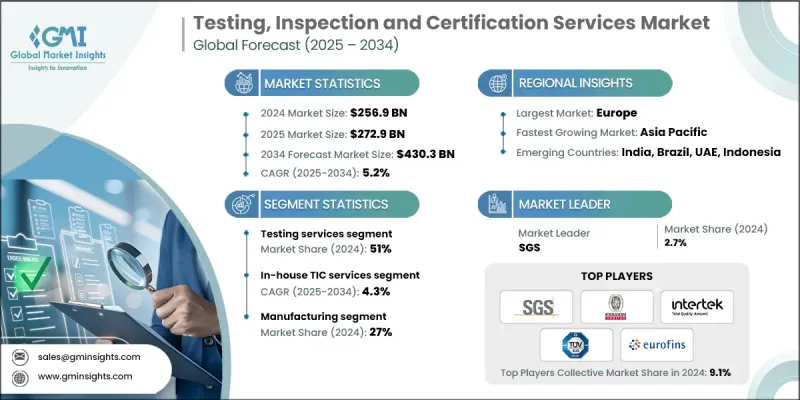

세계의 시험, 검사 및 인증 서비스 시장은 2024년에 2,569억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 5.2%로 성장하여 4,303억 달러에 달할 것으로 예측되고 있습니다.

TIC 서비스 시장은 제조업, 에너지, 건설, 소비재 등 다양한 산업에서 제품의 품질, 안전성, 컴플라이언스를 확보하는데 있어서 매우 중요한 역할을 하고 있습니다. 이러한 서비스는 제조업체가 자사 제품이 국내외 기준을 충족하는지 확인하고 세계 시장에 진입하기 전에 일관성, 안전성 및 신뢰성을 보장하는 데 도움이 됩니다. 국제 무역이 확대되는 가운데 TIC 서비스는 위험 최소화, 소비자 신뢰 유지, 업무 효율성 향상에 필수적입니다. 특히 자동차, 의료, 식품, 전자기기 등의 분야에서 규제 준수의 중요성이 높아지는 가운데, TIC 서비스에 대한 안정적인 수요가 지속적으로 만들어지고 있습니다. 세계 정부 기관 및 민간 기업은 제품이 엄격한 품질, 성능 및 환경 규제를 충족하는지 확인하기 위해 이러한 서비스에 의존합니다. 국제무역의 복잡성과 안전기준에 대한 기대감이 높아짐에 따라 기업은 독립적인 TIC 제공업체에 대한 의존도를 더욱 높여주고 있으며, 이는 세계 시장 성장을 더욱 강화하고 있습니다.

시장 범위

시작 연도

2024년

예측 기간

2025-2034년

시작 금액

2,569억 달러

예측 금액

4,303억 달러

CAGR

5.2%

북미, 유럽, 아시아태평양 등 각 지역의 정부 규제에 따라 제3자 기관에 의한 TIC 서비스 수요가 가속화되고 있습니다. 각국 및 지역의 당국은 국내 및 수출에 있어서 소비자의 건강을 지키고 환경의 안전을 확보하기 위해 일관된 제품 시험 및 인증을 요구하고 있습니다. 제조업체는 컴플라이언스 평가를 처리하기 위해 인증을 받은 TIC 서비스 제공업체와의 제휴를 추진하고 있으며, 이를 통해 국제 무역 기준을 효율적으로 충족시킬 수 있습니다. 독립적인 시험 및 인증은 제품이 수입 규제 및 지역 기술 요구사항을 충족함을 입증하고 기업이 시장을 더욱 빠르게 출시할 뿐만 아니라 고액의 리콜 및 수출 거부 위험을 줄이는 데 도움이 됩니다.

시험 서비스 분야는 2024년에 51%의 점유율을 차지했습니다. 이러한 서비스는 의료, 제조, 전자 기기, 소비재 부문에서 널리 활용되며 성능의 정확성과 안전성을 보장합니다. 시험은 국내 및 국제 기준에 대한 적합성을 확인하는 데 필수적인 단계로 계속되고 있습니다. 한편, 검사 서비스는 건설, 농업 등의 산업에서 널리 채택되어 시장 투입 전에 제품의 안전성, 품질의 일관성, 규제 기준에의 적합성을 검증합니다.

사내 TIC 서비스 부문은 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 4.3%로 성장할 것으로 예측됩니다. 많은 기업들은 직접 감독을 유지하고 독점 정보를 보호하기 위해 TIC 업무를 사내에서 수행하는 것을 선호합니다. 사내 서비스는 보다 신속한 대응, 품질 보증에 대한 고급 관리, 내부 컴플라이언스 시스템과의 일관성을 제공합니다. 이 방법에 투자하는 조직은 시험연구소의 설립, 전문기기의 도입, 기술적 전문지식의 확보에 자본을 투입하여 세계 기준에 준거를 유지하면서 효율적이고 기밀성 높은 서비스 제공을 실현하고 있습니다.

미국의 시험, 검사 및 인증 서비스 시장은 2024년 637억 달러 규모에 달했습니다. 이 나라 시장의 성장은 주로 제조업에 의해 견인되고 있으며, 생산기준의 유지, 규제 준수, 제품 신뢰성 확보에 있어서 TIC 서비스에 대한 의존도가 높은 것이 배경에 있습니다. 자동차, 전자기기, 기계 등의 중요한 산업을 지원하는 당 업계의 역할은 제품의 무결성을 유지하고 국제 시장에서 경쟁력을 지속시키는 데 매우 중요합니다.

세계의 테스트, 검사, 인증(TIC) 서비스 시장에서 주요 기업으로는 TUV SUD, SGS, DEKRA, 유로핀스, 뷰로 베리타스, BSI, DNV, TUV Rheinland, Intertech, UL Solutions 등이 있습니다. TIC 서비스 시장에서 사업을 전개하는 기업은 서비스 포트폴리오와 지리적 범위를 확대하기 위해 합병, 인수, 전략적 제휴를 통해 세계 존재감을 강화하고 있습니다. 주요 기업은 테스트 정밀도 향상, 납기 단축, 효율화를 도모하기 위해 자동화, 디지털 플랫폼, AI 기반 검사 툴에 많은 투자를 하고 있습니다. 많은 기업들이 강화되는 환경 규제에 대응하고 지속가능성을 중시한 테스트 및 컴플라이언스 솔루션을 도입하고 있습니다. 신재생에너지, 자율주행차, 스마트제조 등 신규 분야에서의 능력 확대도 중요한 초점이 되고 있습니다.

목차

제1장 조사 방법

시장 범위와 정의

조사 설계

조사 접근

데이터 수집 방법

데이터 마이닝의 출처

세계

지역별/국가별

기본 추정치와 계산

기준연도 계산

시장 추정에서의 주요 동향

1차 조사 및 검증

1차 정보

예측

조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률 분석

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

엄격한 제품 안전·품질 규제 시행 강화

신흥 경제국의 산업화와 제조업 생산량 증가

인증을 받고 지속 가능한 제품에 대한 소비자의 인식과 수요 증가

디지털 및 원격 검사 기술(AI, IoT, 블록체인) 도입

업계의 잠재적 위험 및 과제

복잡한 테스트 환경에서 높은 운영 비용과 서비스 비용

지역 간의 인증 기준의 차이

시장 기회

신재생에너지, 전기자동차, 그린테크놀로지 분야에서의 TIC서비스 확대

사이버 보안 및 디지털 시스템 인증에 대한 수요 증가

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신의 상황

현재의 기술 동향

신규기술

특허 분석

지속가능성과 환경면

탄소발자국 평가

순환형 경제의 통합

전자폐기물 관리 요건

친환경 이니셔티브

이용 사례와 응용 사례

베스트 케이스 시나리오

비용 편익 분석 프레임워크

사내 대응과 외부 위탁의 TIC 서비스 비용 비교

총소유비용(TCO) 분석

시장 투입까지의 시간에 대한 영향 평가

컴플라이언스 리스크 완화의 가치 분석

디지털과 기존 서비스 제공의 비용 모델 비교

시장 성숙도와 기술 도입 상황의 분석

지역별 TIC 시장 성숙도 평가

기술 도입 곡선과 도입 스케줄

디지털 전환 준비도 지수

규제 조화의 진행 상황 분석

업계 벤치마크 조사

고객요건 및 조달분석

벤더 선정 기준 및 벤치마킹 프레임워크

컴플라이언스 비용 최적화 전략

ROI 분석 및 성과 지표

리스크 관리 및 사업 계속 요건

디지털 능력 평가 프레임워크

품질 보증 및 인증 요건

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

합병 및 인수

제휴 및 협업

신제품 발매

사업 확대 계획과 자금 조달

제5장 시장 추정 및 예측 : 서비스별, 2021년-2034년

주요 동향

시험 서비스

전자기 호환성 시험

전기 안전 및 성능 시험

기계·재료 시험

기타

검사 서비스

출하 전 검사 및 위탁 검사

산업 시설 및 설비 점검

건설 및 인프라 검사

기타

인증 서비스

제품 인증

경영 시스템 인증

인재 인증

기타

교정 서비스

기기 보정

계량학 및 측정 기준

기타

기타

제6장 시장 추정 및 예측 : 제공원별, 2021년-2034년

주요 동향

사내 TIC 서비스

내부 시험 및 품질 관리 연구소

자사 검사·인증 부문

기업 연구개발 부문 및 컴플라이언스 시험 센터

기타

외부 위탁 TIC 서비스

독립적인 제3자 TIC 제공업체

계약 기반 시험소

외부검사기관 및 인증기관

기타

제7장 시장 추정 및 예측 : 최종 용도별, 2021년-2034년

주요 동향

제조업

산업용 기계·설비의 시험

품질 관리 및 공장 감사

공급 체인 및 부품 검증

에너지·유틸리티

재생에너지 시스템의 시험

스마트 그리드 및 배터리 인증

원자력발전소의 안전검사

석유 및 가스 자산의 건전성 평가

식음료

식품안전 및 위생검사

포장 및 표시의 컴플라이언스

공급망의 추적성과 원산지 검증

유기 인증 및 지속가능성 인증

자동차

전기차 시험 및 인증

자율주행차 검증

커넥티드카용 사이버 보안 시험

차량 검사 및 형식 인정

화학제품

화학 조성 및 순도 시험

위험물 인정

환경 및 규제 준수 감사

건설 및 인프라

건축 재료 시험

구조 건전성 검사

그린빌딩 및 지속가능성 인증

헬스케어 및 생명과학

생체 적합성 시험 및 멸균 시험

의약품 및 임상시험의 검증

의료기기 및 소프트웨어의 밸리데이션

항공우주 및 방위산업

항공기 부품 인증

방어 시스템 및 군사 규격 시험

우주 시스템의 인정

소비재

전기 기기의 안전 시험

장난감, 섬유, 화장품 인증

소비자 보호 및 품질 보증

기타

제8장 시장 추정 및 예측 : 지역별, 2021년-2034년

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

북유럽 국가

러시아

아시아태평양

중국

인도

일본

호주

한국

동남아시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제9장 기업 프로파일

주요 세계 기업

Bureau Veritas

DEKRA

DNV

Eurofins Scientific

Intertek

SGS

TUV Rheinland

TUV SUD

Regional Champions

APAVE

BSI

Centre Testing International

CCIC

CSA

Lloyd's Register

SOCOTEC

UL Solutions

신흥기업 및 전문기관

ALS

Applus Services

Element Materials Technology

Kiwa

NSF International

QIMA

RINA

SHW

영문 목차

영문목차

The Global Testing, Inspection, and Certification (TIC) Services Market was valued at USD 256.9 billion in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 430.3 billion by 2034.

The TIC services market plays a vital role in ensuring product quality, safety, and compliance across diverse industries, including manufacturing, energy, construction, and consumer goods. These services help manufacturers verify that their products meet both domestic and international standards, guaranteeing consistency, safety, and reliability before entering global markets. As global trade expands, TIC services are becoming essential in minimizing risk, maintaining consumer trust, and enhancing operational efficiency. The increasing importance of regulatory compliance, particularly in sectors such as automotive, healthcare, food, and electronics, continues to drive steady demand for TIC services. Governments and private entities worldwide depend on these services to ensure that products meet stringent quality, performance, and environmental regulations. The rising complexity of international trade and heightened safety expectations are pushing companies to rely more on independent TIC providers, further strengthening market growth globally.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$256.9 Billion

Forecast Value

$430.3 Billion

CAGR

5.2%

Government mandates across regions like North America, Europe, and Asia-Pacific are accelerating demand for third-party TIC services. National and regional authorities require consistent product testing and certification to protect consumer health and ensure environmental safety, both domestically and for exports. Manufacturers increasingly partner with accredited TIC service providers to handle compliance assessments, enabling them to meet international trade standards efficiently. Independent testing and certification validate that products adhere to import regulations and regional technical requirements, helping companies gain faster market access and reduce the risk of costly recalls or export rejections.

The testing services segment held a 51% share in 2024. These services are widely applied across healthcare, manufacturing, electronics, and consumer goods sectors to ensure performance accuracy and safety. Testing remains an essential step in confirming compliance with both local and international standards. Inspection services, on the other hand, are widely adopted in industries such as construction and agriculture to verify product safety, quality consistency, and compliance with regulatory norms before market release.

The in-house TIC services segment is projected to grow at a CAGR of 4.3% from 2025 to 2034. Many companies prefer to perform TIC operations internally to maintain direct oversight and safeguard proprietary information. In-house services also provide faster turnaround times, greater control over quality assurance, and alignment with internal compliance frameworks. Organizations investing in this approach often allocate capital to establish testing laboratories, specialized equipment, and technical expertise, ensuring efficient and confidential service delivery while maintaining adherence to global standards.

U.S. Testing, Inspection, and Certification (TIC) Services Market generated USD 63.7 billion in 2024. The country's market growth is primarily driven by the manufacturing sector, which depends heavily on TIC services for maintaining production standards, regulatory compliance, and product reliability. The industry's role in supporting critical sectors such as automotive, electronics, and machinery underscores its importance in maintaining product integrity and sustaining competitiveness in international markets.

Key companies operating in the Global Testing, Inspection and Certification (TIC) Services Market include TUV SUD, SGS, DEKRA, Eurofins, Bureau Veritas, BSI, DNV, TUV Rheinland, Intertek, and UL Solutions. Companies operating in the Testing, Inspection, and Certification (TIC) Services Market are strengthening their global presence through mergers, acquisitions, and strategic alliances to expand their service portfolios and geographical reach. Leading firms are heavily investing in automation, digital platforms, and AI-based inspection tools to improve testing accuracy, reduce turnaround time, and enhance efficiency. Many are adopting sustainability-driven testing and compliance solutions in response to growing environmental regulations. Expanding capabilities in emerging sectors such as renewable energy, autonomous vehicles, and smart manufacturing has also become a key focus.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Regional

2.2.2 Service

2.2.3 Sourcing

2.2.4 End Use

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Growing enforcement of stringent product safety and quality regulations

3.2.1.2 Rising industrialization and manufacturing output in emerging economies

3.2.1.3 Increased consumer awareness and demand for certified, sustainable products

3.2.1.4 Adoption of digital and remote inspection technologies (AI, IoT, blockchain)

3.2.2 Industry pitfalls and challenges

3.2.2.1 High operational and service costs for complex testing environments

3.2.2.2 Variability in certification standards across regions

3.2.3 Market opportunities

3.2.3.1 Expansion of TIC services in renewable energy, EVs, and green technologies

3.2.3.2 Growing demand for cybersecurity and digital system certification

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Technology and innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Patent analysis

3.9 Sustainability & environmental aspects

3.9.1 Carbon Footprint Assessment

3.9.2 Circular Economy Integration

3.9.3 E-Waste Management Requirements

3.9.4 Green Manufacturing Initiatives

3.10 Use cases and applications

3.11 Best-case scenario

3.12 Cost-Benefit Analysis Framework

3.12.1 In-House vs Outsourced TIC services cost comparison

3.12.2 Total Cost of Ownership (TCO) analysis

3.12.3 Time-to-market impact assessment

3.12.4 Compliance risk mitigation value analysis

3.12.5 Digital vs traditional service delivery cost models