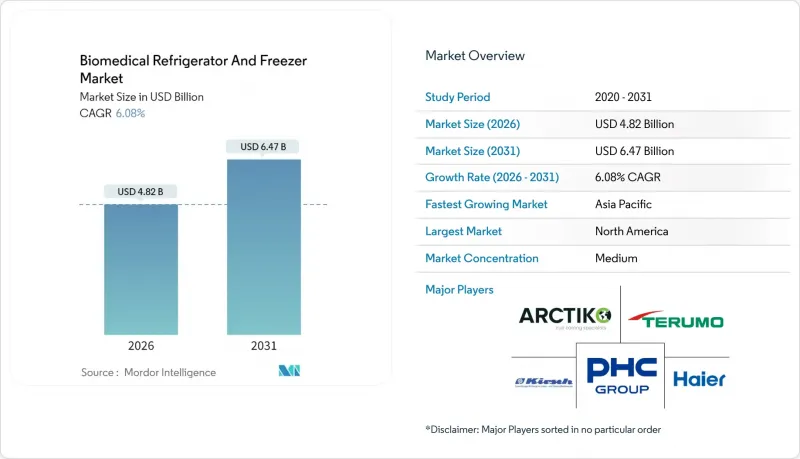

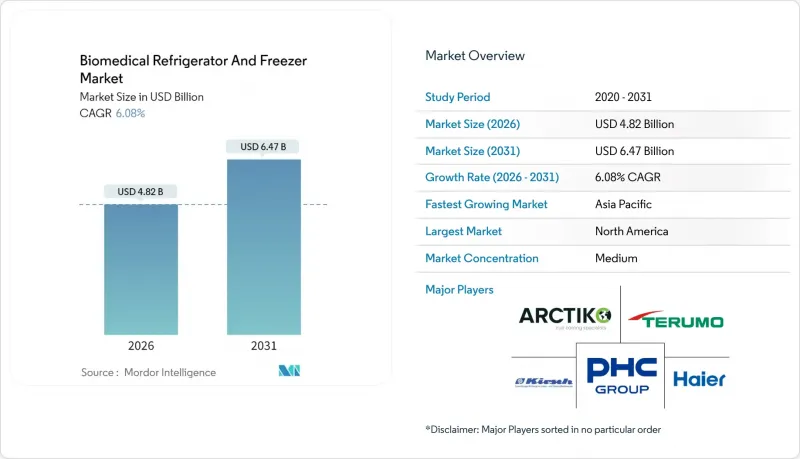

바이오 의료용 냉장고 및 냉동고 시장은 2025년에 45억 4,000만 달러로 평가되었고, 2026년 48억 2,000만 달러에서 2031년까지 64억 7,000만 달러에 이를 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 6.08%로 예상됩니다.

이러한 성장은 초정밀 온도 제어가 필요한 세포 및 유전자 치료에 대한 투자 증가, 세계 백신 보관 요건의 강화, 휴대용 IoT 지원 콜드체인 자산이 필요한 분산형 임상시험으로의 전환이 가속화되고 있음을 반영합니다. 압축기 기술은 여전히 설치 용량의 대부분을 차지하고 있지만, 지속가능성 규제로 인해 자기 냉동 기술 및 기타 무냉매 기술이 급속히 보급되고 있습니다. 공급망 회복탄력성은 반복적으로 언급되는 주제입니다. 헬륨 부족은 극저온 용량을 제약하는 반면, 반도체 부족은 스마트 냉동고의 리드타임을 연장하고 있습니다. 그 결과, 구매자들은 냉각 성능뿐만 아니라 부품의 추적성, 원격 모니터링, 다운타임을 제한하는 예지보전 기능에 대해서도 벤더를 평가하게 되었습니다.

5억 3,700만 명 이상의 성인이 당뇨병을 앓고 있으며, 이들 중 상당수는 2℃에서 8℃ 범위에서 보관해야 하는 인슐린을 필요로 합니다. 이 단일 치료제의 보관 요구 사항만으로도 의료용 냉장고 및 냉동고 시장에는 지속적인 주문이 계속 유입되고 있습니다. 정부 주도의 비감염성 질병 대책 프로그램에 따라, 특히 인도와 동남아시아에서는 의약품 등급 냉장실 설치에 대한 자금 지원이 이루어지고 있습니다. 한편, 유럽 병원에서는 추가 바닥 면적을 필요로 하지 않고 생물학적 제제, 백신, 혈액제제를 분리 보관할 수 있는 멀티존 캐비닛으로 업데이트가 진행되고 있습니다. 종양병동도 성장의 거점입니다. 온도 변동에 민감한 단일 클론 항체 한 묶음은 대체 비용이 7만 달러가 넘을 수 있어 이중화 압축기, 배터리 백업, 24시간 365일 클라우드 텔레메트리에 대한 투자 의욕을 높이고 있습니다.

CAR-T 치료제, CRISPR 편집 세포 제품, 체외 유전자 치료제는 제조부터 환자 투약까지 -150℃ 이하의 온도 관리가 필수적입니다. 액체 질소를 사용하지 않고 -165℃를 유지하는 융착식 냉동고가 보급되고 있습니다. 이는 실험실 안전 점검을 간소화하고 운영 비용을 절감하기 위함입니다. 현재 물류 체인에는 GPS와 연속 온도 데이터 스트림이 내장되어 있어 이식 코디네이터는 기증자의 심장이 국내를 횡단하는 동안 규정된 2 ℃ - 8 ℃의 온도 범위 내에 있는지 여부를 실시간으로 확인할 수 있습니다. FDA의 2024년 세포치료제 제조 가이드라인 등 규제 가이드라인이 단계적으로 강화될 때마다 장비 사양의 기준이 높아져 균일성과 빠른 온도 회복을 증명할 수 없는 구형 냉동고의 교체가 가속화되고 있습니다.

최신형 초저온 냉동고(ULT)는 5만 달러의 가격대를 형성하고 있으며, 연간 유지보수 계약비는 구매 가격의 15%에 달하는 경우가 많습니다. 80℃ 냉동고 1대는 하루 15kWh를 소비하며, 미국의 평균 상업용 요금으로 환산하면 연간 1,500달러의 에너지 비용에 해당합니다. 소규모 진료소나 NGO는 초기 자본 예산에 대한 부담을 피하기 위해 구매를 미루거나 리스를 선택하는 경우가 많습니다. 아프리카와 남아시아 일부 지역에서는 의료기기에 대한 관세가 15%를 초과하는 경우도 있어 수입 관세가 문제를 더욱 복잡하게 만들고 있습니다. 이러한 요인으로 인해 특히 가격에 민감한 지역에서는 업데이트 주기가 길어지고 첨단 IoT 지원 장치의 보급이 늦어지고 있습니다.

2025년 기준, 바이오 메디컬용 냉장고 및 냉동고 시장에서 실험실용 냉장고가 23.12%로 가장 큰 점유율을 차지했습니다. 이는 임상, 학술, 산업을 막론하고 거의 모든 의료시설에서 시약, 백신, 환자 검체를 2℃-8℃ 범위에서 보관해야 하기 때문입니다. 이들 장비에는 현재 마이크로프로세서 제어장치, 도어 개폐 센서, 온도변화를 ±1℃ 이내로 억제하는 팬 보조 기류 시스템이 표준으로 장착되어 있습니다. 한편, 바이오뱅크, 위탁개발기관, 병원 병리검사실이 세포주, 줄기세포, mRNA 치료제의 저온보관 능력을 확대함에 따라 ULT(초저온) 카테고리는 10.25%의 연평균 복합 성장률(CAGR)로 성장하고 있습니다. ULT 냉동고는 이미 11억 1,000만 달러 규모의 생물의학용 냉장고 및 냉동고 시장 규모를 차지하고 있으며, 그 점유율은 더욱 높아질 것으로 예측됩니다. 이는 ATMP(첨단치료의약품) 규제 신청 시 -80℃ 이하 보관에 대한 검증이 요구되기 때문입니다.

혈장 냉동고 및 혈액은행용 냉장고는 수혈센터의 노후화된 설비 교체로 인해 한 자릿수 성장세를 유지하고 있습니다. 한편, 상온에서 10분 이내에 -40℃까지 냉각하는 틈새 장비인 쇼크프리저는 첨단 암 연구 프로토콜에서 새로운 수요를 발견하고 있습니다. 제조업체들은 클라우드 대시보드와 4시간 이내 현지 기술자 대응을 보장하는 서비스 수준 계약을 번들로 제공하는 경우가 증가하고 있으며, 이 기능은 특히 고처리량 코로나19 유전체 모니터링 연구소에서 높은 평가를 받고 있습니다.

2025년 북미는 전 세계 매출의 26.95%를 차지했습니다. 2026년 2월부터 시행되는 FDA 품질 관리 개혁에 따라 의료기기 제조업체는 ISO 13485를 준수해야 합니다. 선견지명이 있는 병원이나 CRO는 인증 취득의 번거로움을 피하기 위해 기존 시설의 사전 업데이트를 진행하고 있습니다. 미국에는 주요 바이오의약품 클러스터가 집중되어 있어 막대한 저온저장 용량을 소비하고 있습니다. 써모피셔의 20억 달러에 달하는 여러 거점에 대한 투자는 지속적인 수요에 대한 확신을 보여줍니다. 반도체 부족은 여전히 하방 리스크이며, Wi-Fi 지원 온도 로거 제조업체의 약 80%가 12개월의 리드타임을 보고하고 있어 스마트 캐비닛 도입에 걸림돌이 되고 있습니다.

아시아태평양은 의료 시스템 설비 투자와 활발한 임상 연구 아웃소싱 분야를 배경으로 6.75%의 가장 빠른 CAGR을 기록했습니다. 중국에서는 바이오 제조의 현지화가 진행되고 있고, 인도에서는 수혈 서비스가 확대되고 있으며, 인도네시아에서는 다자간 자금을 활용하여 태양광 직접 구동 컴프레서를 탑재한 농촌용 백신 냉장고가 도입되고 있습니다. 지역 정부는 콜드체인 업그레이드를 감염병 대책 전반과 함께 진행하는 경우가 많으며, 초기 설비 조달을 실질적으로 지원하고 있습니다. 국내 제조는 확대 추세에 있으며, 중국 업체들은 현재 ENERGY STAR 인증을 획득한 초저온 모델을 아세안 전역에 수출하고 있어 가격 경쟁이 심화되는 동시에 제품 혁신도 촉진하고 있습니다.

유럽에서는 엄격한 환경 정책을 배경으로 꾸준한 성장을 이루고 있습니다. EU의 프레온류 단계적 감축 규제로 인해 GWP가 높은 냉매의 사용이 억제되고, 연구소에서는 자연냉매 압축기 및 신흥 자기열 시스템으로 전환이 진행되고 있습니다. 콜드체인 테크놀로지스는 네덜란드에 A+++ 에너지 효율 등급을 획득한 공장을 설립하여 당일 배송이 가능하도록 했습니다.

The Biomedical refrigerator & freezer market was valued at USD 4.54 billion in 2025 and estimated to grow from USD 4.82 billion in 2026 to reach USD 6.47 billion by 2031, at a CAGR of 6.08% during the forecast period (2026-2031).

This growth reflects rising investments in cell and gene therapies that rely on ultra-precise temperature control, stricter global vaccine-storage mandates, and an accelerating shift toward decentralized clinical trials that require portable, IoT-enabled cold-chain assets. Compressor technology still underpins most installed capacity, yet sustainability regulations are propelling rapid adoption of magnetic refrigeration and other refrigerant-free approaches. Supply-chain resilience is a recurring theme: helium scarcity constrains cryogenic capacity, while semiconductor shortages lengthen lead times for smart freezers. As a result, buyers now evaluate vendors not only on cooling performance but also on component traceability, remote monitoring, and predictive-maintenance features that limit downtime.

More than 537 million adults live with diabetes, and many require insulin that must remain between 2 °C and 8 °C. This single-therapy storage requirement alone keeps a continuous stream of orders flowing into the biomedical refrigerator & freezer market. Government-sponsored non-communicable disease programs are funding the installation of new pharmaceutical-grade cold rooms, particularly in India and Southeast Asia, while European hospitals are upgrading to multi-zone cabinets that can segregate biologics, vaccines, and blood products without requiring additional floor space. Oncology wards are another growth node; a single batch of temperature-excursion-sensitive monoclonal antibodies can exceed USD 70,000 in replacement cost, which heightens willingness to pay for redundant compressors, battery backups, and 24/7 cloud telemetry.

CAR-T, CRISPR-edited cell products, and ex vivo gene therapies must often be maintained at temperatures below -150 °C from manufacturing to the bedside. Fusion-style freezers that forgo liquid nitrogen while maintaining temperatures of -165 °C are gaining traction because they ease lab safety checks and reduce operating expenses. Logistics chains now embed GPS and continuous-temperature data streams, allowing a transplant coordinator to verify, in real-time, whether a donor heart remains within its mandated 2 °C to 8 °C temperature envelope during cross-country flights. Each incremental regulatory guideline, such as the FDA's 2024 cell-therapy manufacturing guidance, elevates the equipment specification baseline and accelerates replacement of legacy freezers that cannot document uniformity or rapid temperature recovery.

A state-of-the-art ULT freezer can list for USD 50,000, and annual service contracts often reach 15% of the purchase price. Electricity adds a further burden: one 80 °C box may consume 15 kWh per day, equivalent to USD 1,500 in yearly energy expenses at average US commercial rates. Smaller clinics and NGOs often defer purchases or opt for leasing to avoid upfront capital budget hits. Import tariffs compound the challenge in Africa and parts of South Asia, where duties can exceed 15% on medical equipment. These factors lengthen replacement cycles and slow penetration of advanced IoT-enabled units, especially in price-sensitive geographies.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Laboratory refrigerators captured the largest slice of the Biomedical refrigerator & freezer market in 2025 at 23.12% because virtually every clinical, academic, and industrial health facility must store reagents, vaccines, or patient samples within the 2 °C-8 °C band. These units now ship with microprocessor controllers, door-opening sensors, and fan-assisted airflow that keeps temperature variance below +-1 °C. At the same time, the ULT category is growing at a 10.25% CAGR as biobanks, contract-development organizations, and hospital pathology labs expand cryogenic capacity for cell lines, stem cells, and mRNA therapeutics. ULT freezers already account for USD 1.11 billion of the Biomedical refrigerator & freezer market size, and their share will climb because regulatory filings for ATMPs require validated sub--80 °C storage audits.

Plasma freezers and blood bank refrigerators sustain mid-single-digit growth by replacing aging stock in transfusion centers, whereas shock freezers-niche devices that drop from ambient to -40 °C within 10 minutes-are finding new demand in advanced oncology research protocols. Manufacturers increasingly bundle cloud dashboards and service-level agreements that guarantee four-hour on-site technician response, a feature especially valued by high-throughput COVID-19 genomic surveillance labs.

The Biomedical Refrigerator and Freezer Market is Segmented by Product Type (Plasma Freezers, Blood Bank Refrigerators, and More), Refrigeration Technology (Compressor-Based, Absorption/Adsorption, Magnetic Refrigeration, Stirling Engine), End User (Hospitals & Clinics, Blood Banks, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

North America generated 26.95% of worldwide revenue in 2025. FDA quality-management reforms, effective February 2026, require device makers to harmonize with ISO 13485; forward-thinking hospitals and CROs are pre-emptively replacing legacy stock to avoid qualification headaches. The United States also houses leading biopharma clusters that consume significant cryogenic capacity; Thermo Fisher's USD 2 billion multi-site investment underscores confidence in sustained demand. Semiconductor shortages remain a downside risk; nearly 80% of manufacturers report 12-month lead times for Wi-Fi-enabled temperature-loggers, hampering rollouts of smart cabinets.

Asia Pacific records the fastest 6.75% CAGR on the strength of health-system capital spending and a thriving clinical-research outsourcing sector. China scales local biomanufacturing, India expands transfusion services, while Indonesia receives multilateral funding to install rural vaccine fridges with solar-direct-drive compressors. Regional governments often bundle cold-chain upgrades with broader infectious-disease preparedness, effectively underwriting initial equipment procurement. Domestic manufacturing is ramping: Chinese vendors now export ENERGY STAR-certified ULT models across ASEAN, intensifying price competition but also driving product innovation.

Europe grows steadily on the back of stringent environmental policies. EU F-gas phase-down regulations discourage high-GWP refrigerants, pushing labs toward natural-refrigerant compressors or emerging magnetocaloric systems. Cold Chain Technologies opened a Netherlands plant with an A+++ energy rating, allowing same-day distribution.